Fixed Income

This morning's employment report, particularly the downward revisions to prior months, strengthens our conviction that the US economy is headed for recession.

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

The risk-on soft-landing narrative dominated investors’ psyche last month and pro-cyclical assets topped the August return ranking. Asian currencies led the pack by a wide margin, while the dollar was the largest laggard. Markets pricing in an upcoming Fed…

The 2Y/10Y segment of the yield curve is flirting with un-inversion. Aggressive rate cut expectations have largely driven its steepening, with the 2-year Treasury yields falling nearly 100 bps over the past couple of months. Our colleagues at the Bank…

According to BCA Research’s European Investment Strategy service, an increase in borrowing costs will further weaken vulnerable corporate balance sheets. As suggested by their Corporate Health Monitors (CHMs), the health of High-Yield corporate balance sheets…

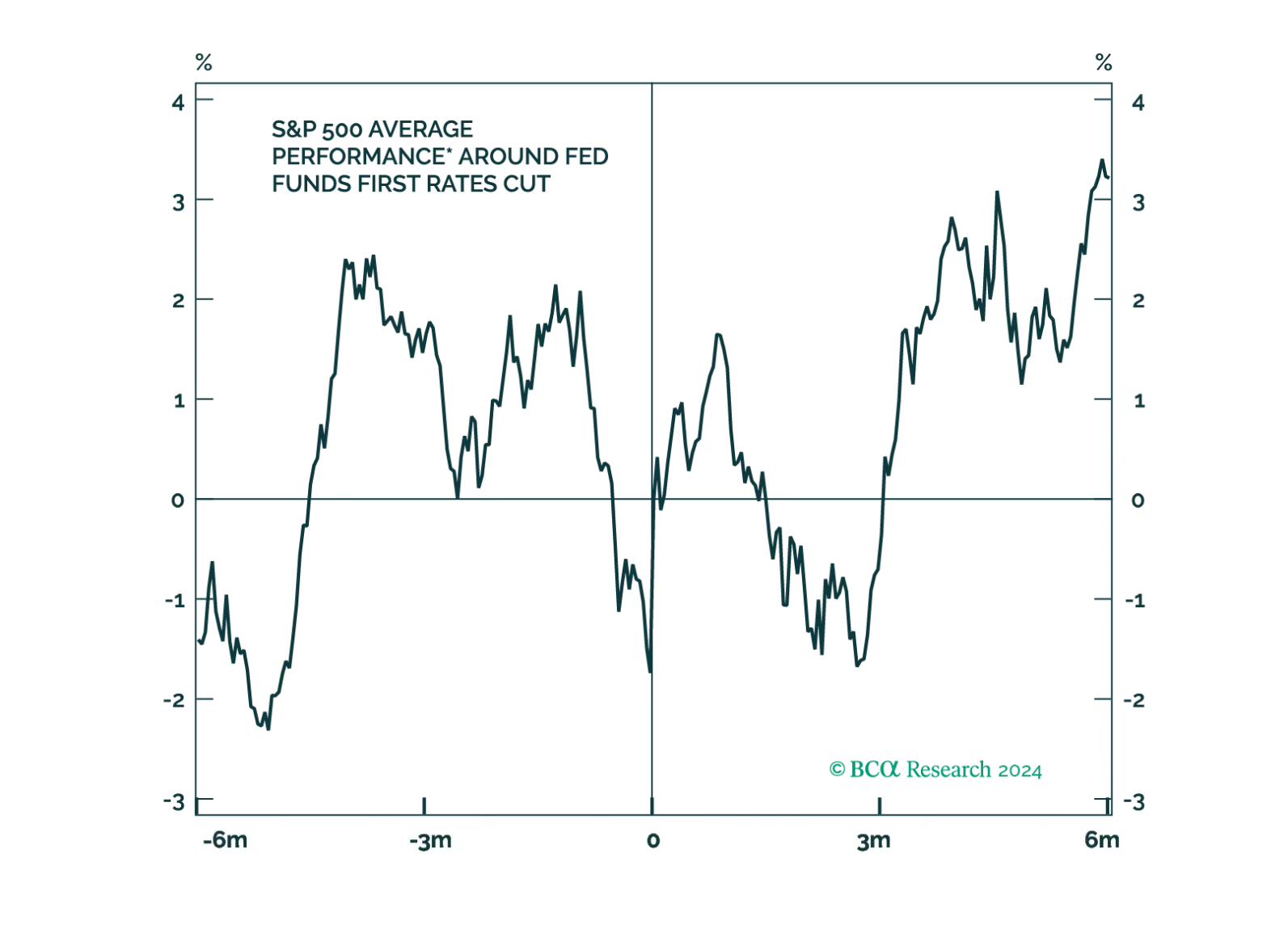

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

Our annual end-of-summer chartbook report traces the labor market deterioration that led us to downgrade equities at the beginning of August. It also highlights the soft-landing expectations that the credit and equity markets are discounting. We like the risk-reward profile of our newly defensive stance.

Last week, economists polled by Bloomberg revised their consensus 2024 US GDP forecasts upwards, from 2.3% to 2.5%. Government spending and private investment were both revised 0.3 ppts higher to 3.0% and 3.9%, respectively, while consumption growth forecasts…

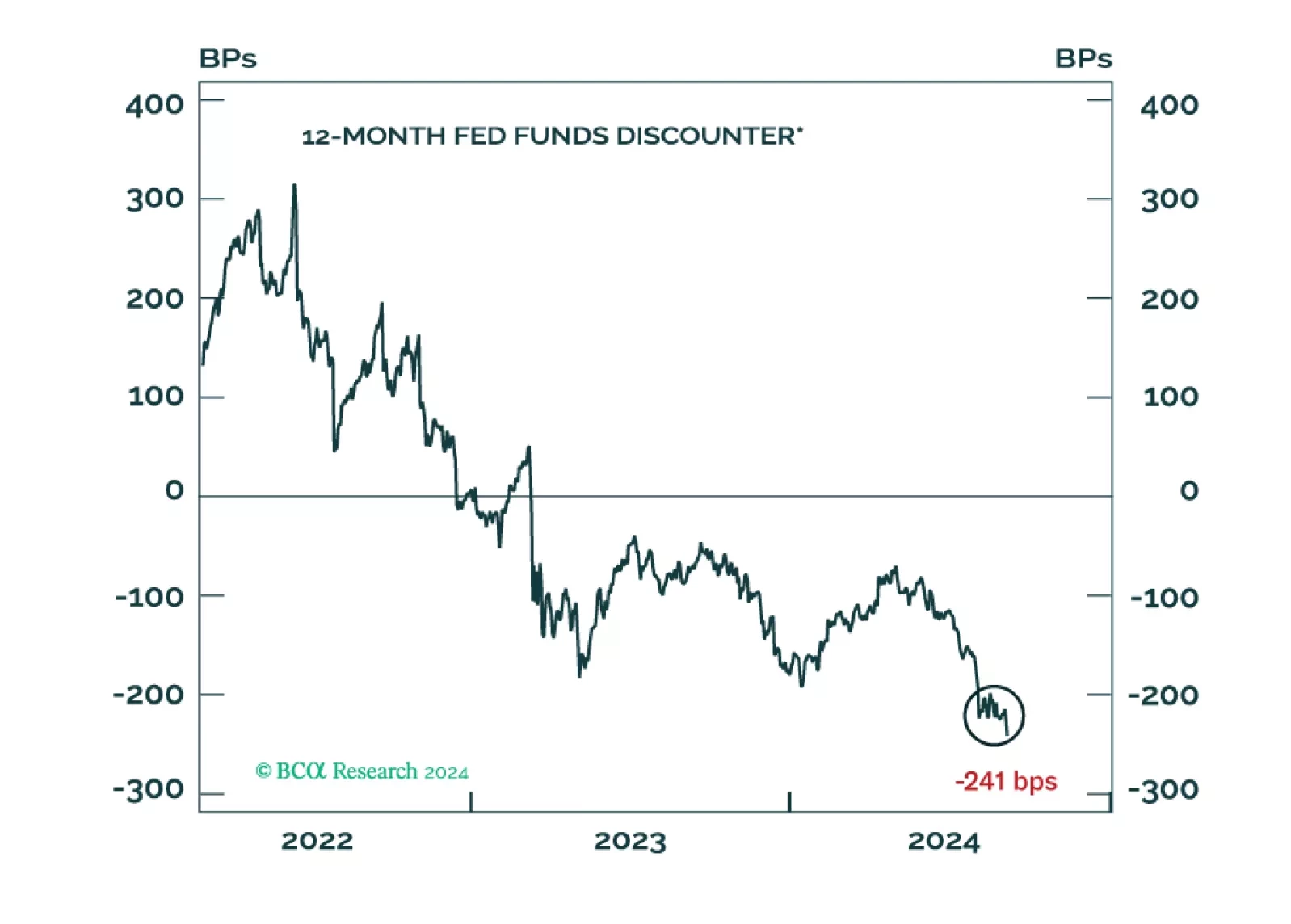

The market is currently expecting the Fed to cut rates by 100 bps over the course of 2024 and by another 120 bps throughout the first eight months of 2025. However, our Global Investment strategists expect the extent of 2024 rate cuts to undershoot…