Fixed Income

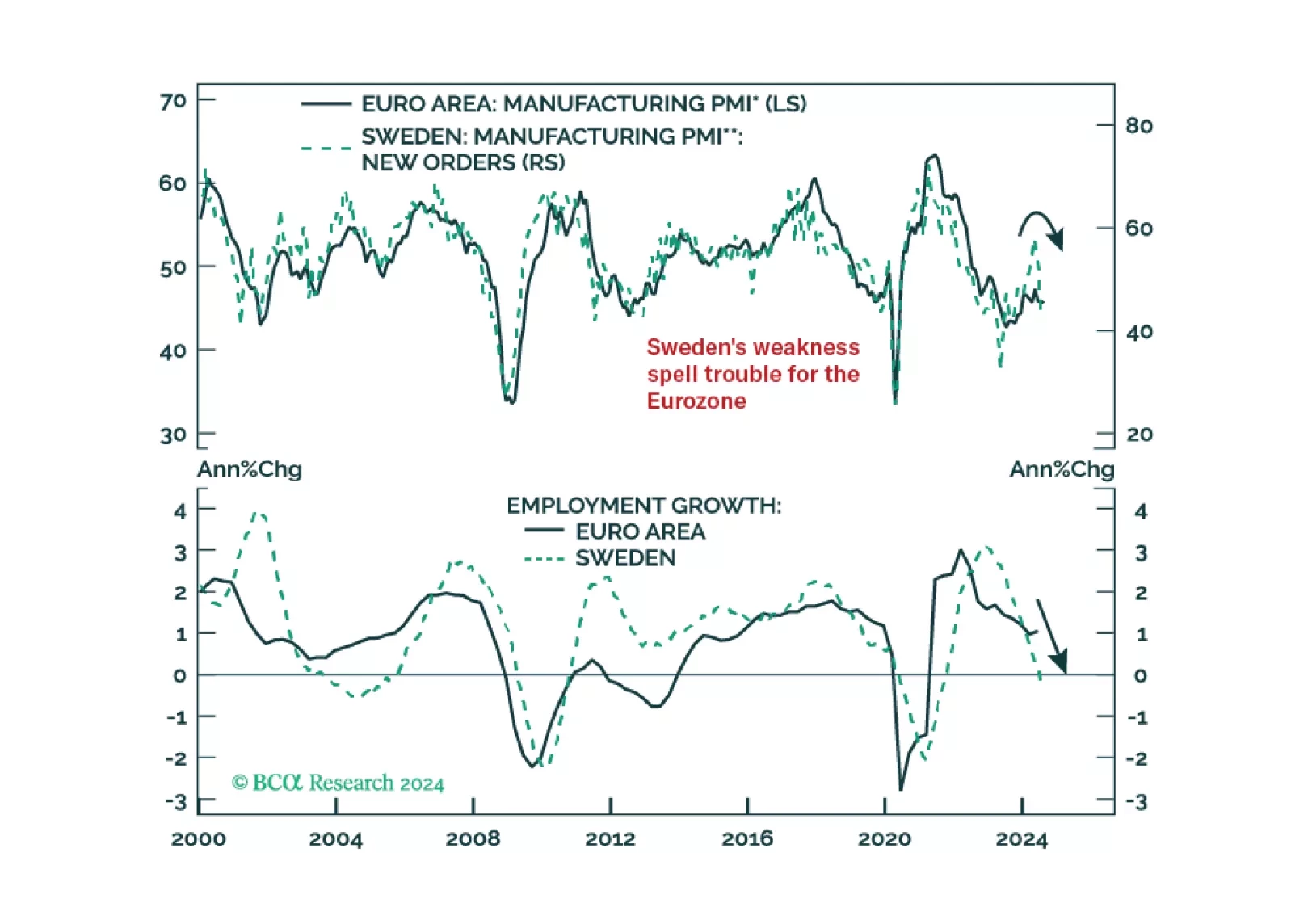

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

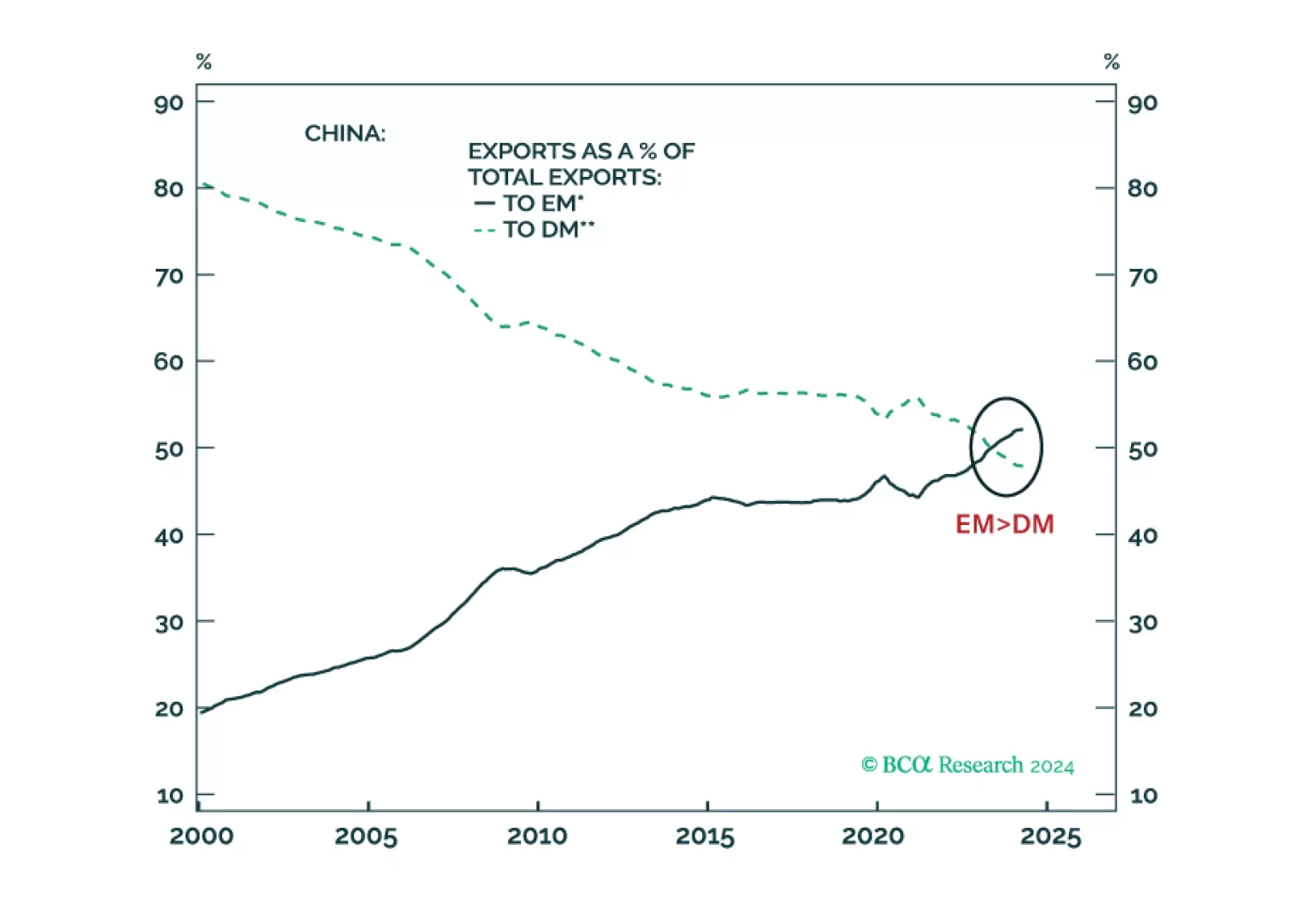

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

In this Special Report, we assess the impact of monetary policy tightening on major economies. Interest rate sensitive GDP already slowed significantly in response to the aggressive rate hiking cycle. Despite the beginning of policy easing, our forward-looking indicators suggest monetary policy will continue to weigh on the economy.

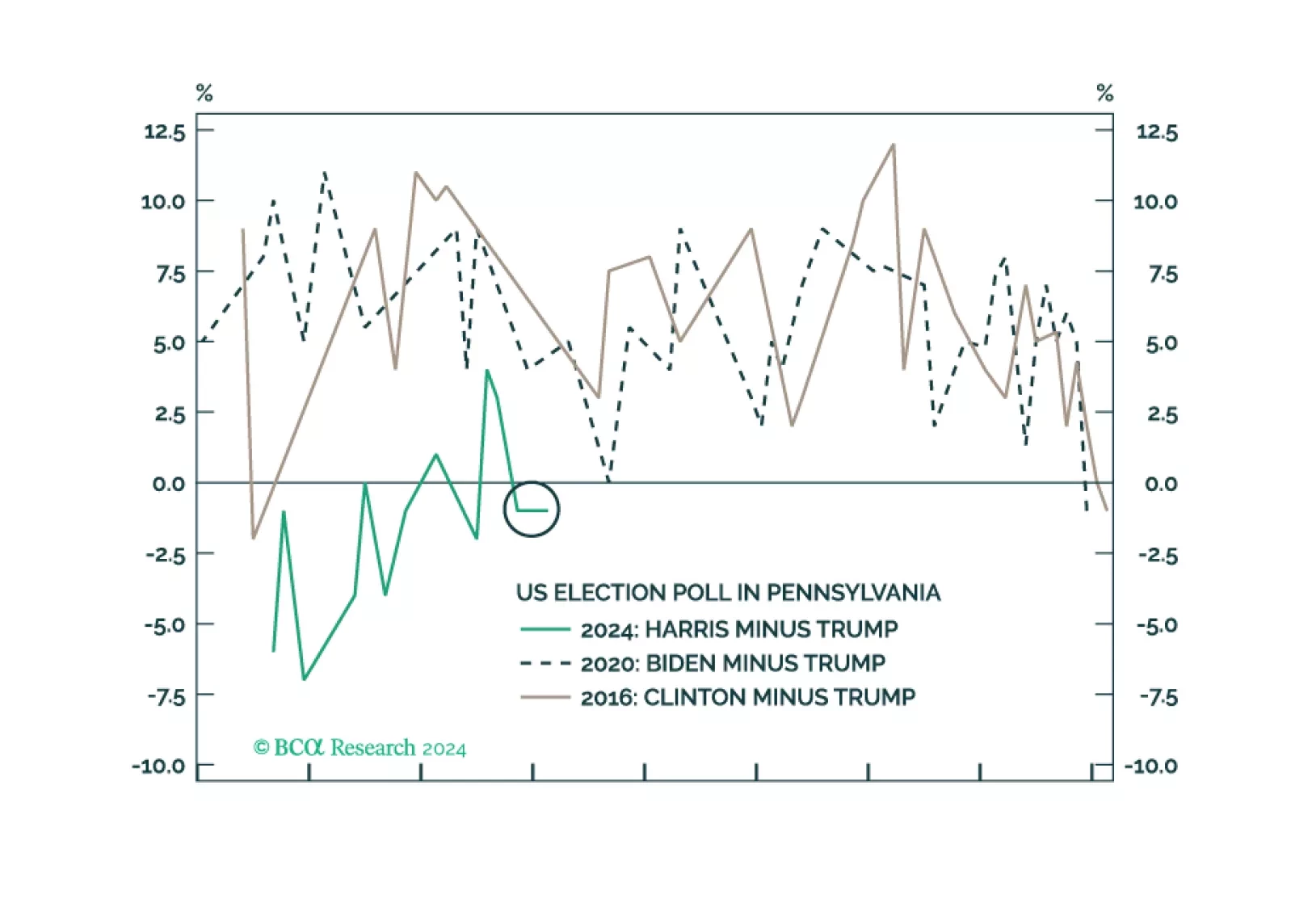

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

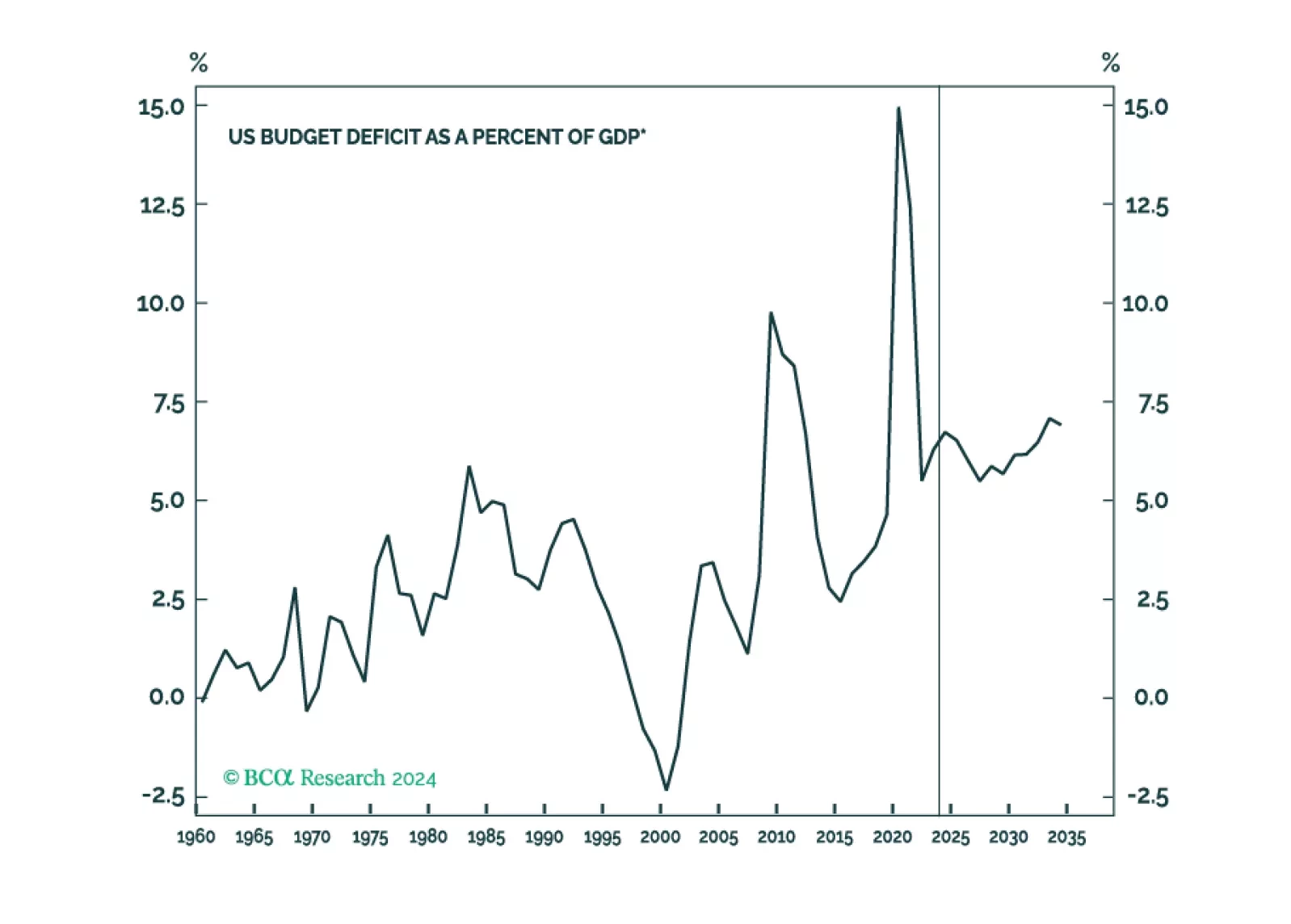

The US fiscal outlook is more unappetizing than it was before the pandemic, but we are not convinced that a difficult day of reckoning awaits. A Treasury market crisis is conceivable, but it is far from inevitable.

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.