Fixed Income

The Australian CPI release for Q2 came in broadly within expectations. Headline CPI reaccelerated to 3.8%y/y from 3.6%y/y the previous quarter. Some of the narrower measures of inflation — trimmed-mean and weighted median CPI — came in below market…

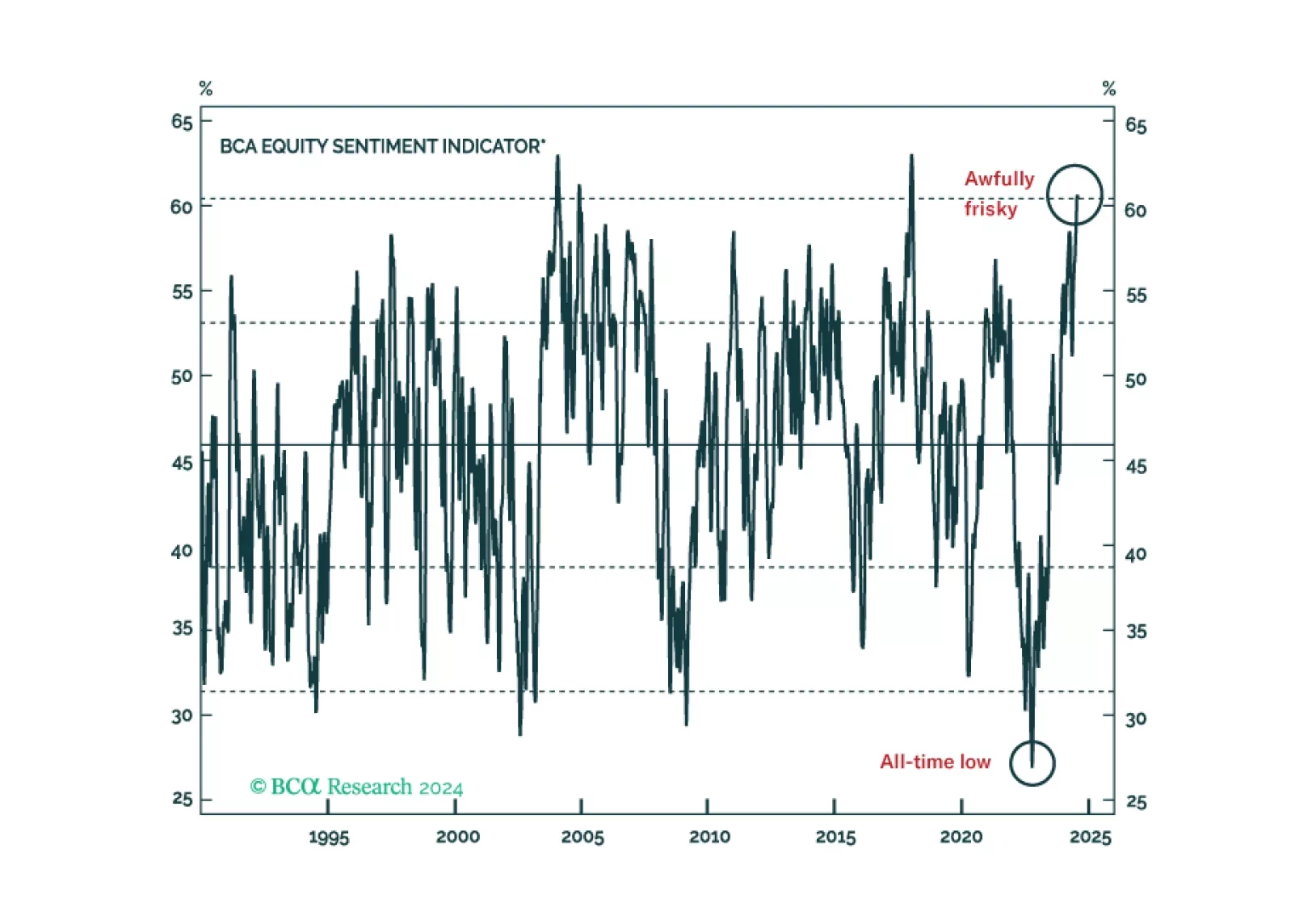

According to BCA Research’s Global Asset Allocation service, while the market action of the past few weeks is pointing to a return to a negative stock-bond correlation, more prints will be needed to confirm things are getting back to normal. The post-COVID…

Mounting evidence that the labor market is on its way to cracking checked two more boxes on our checklist, driving us to tactically downgrade equities to underweight while upgrading fixed income to overweight. Our tactical and cyclical (6-12 months) views are now aligned as our conviction that a recession will begin before year-end has increased.

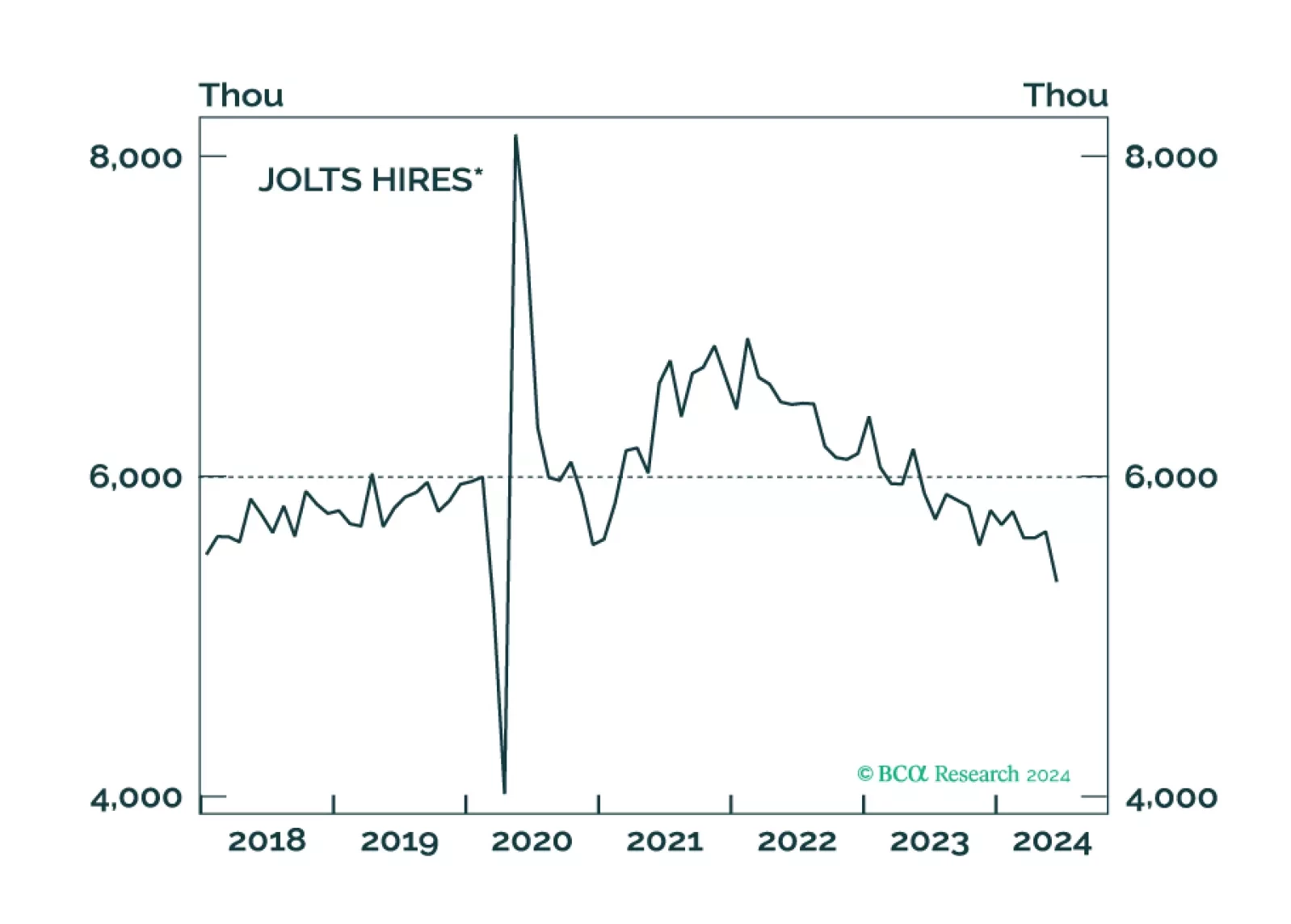

July nonfarm payrolls expanded by 114 thousand workers, a sharp slowdown from June’s downwardly revised 179 thousand, and significantly disappointing expectations of 175 thousand. The unemployment rate unexpectedly edged 0.2ppt higher to 4.3% in July,…

The ISM Manufacturing PMI disappointed in July. The headline index declined at a faster pace, from 48.5 to 46.8, disappointing expectations and extending a four-month contraction streak. Details were uninspiring. New orders dipped to 47.4 from 49.3,…

The Sahm Rule – a widely watched real-time recession indicator – signals the early stages of a recession when the 3-month moving average of the unemployment rate rises at least half a percentage point above its past 12-month low. The surprise rise in the…

A decisive risk-off mood dominated markets at the end of last week, amid disappointing payrolls, tech earnings and manufacturing PMIs. The Nasdaq and other tech-heavy stock markets such as Japan, Korea and Taiwan led the equity declines. Other pro-cyclical…

The Bank of England (BoE) lowered its policy rate by 25 basis points to 5% at its meeting on Thursday. While the move was expected, the governing board was split, voting 5 – 4 in favor of reducing the key interest rate. The BoE cut its policy rate despite…

No clear risk-on/risk-off pattern emerged from July’s market performance data. On the one hand, consistent with a risk-off environment, US bonds ranked highest in the monthly return distribution, while pro-cyclical industrial metals and oil lagged.…