Fixed Income

If the 2022 roadmap is any guide, equity markets and cyclical currencies will trough only after confirming that the peak in energy prices is in the rearview mirror. In the very near term, investors should focus on P&L preservation. Reduce exposure to equities, and seek refuge in gold, and inflation-linked bonds (ILBs). Amid a very different demand side than in 2022, today’s supply shock is unlikely to generate lasting inflation, and investors should fade rate-hike odds.

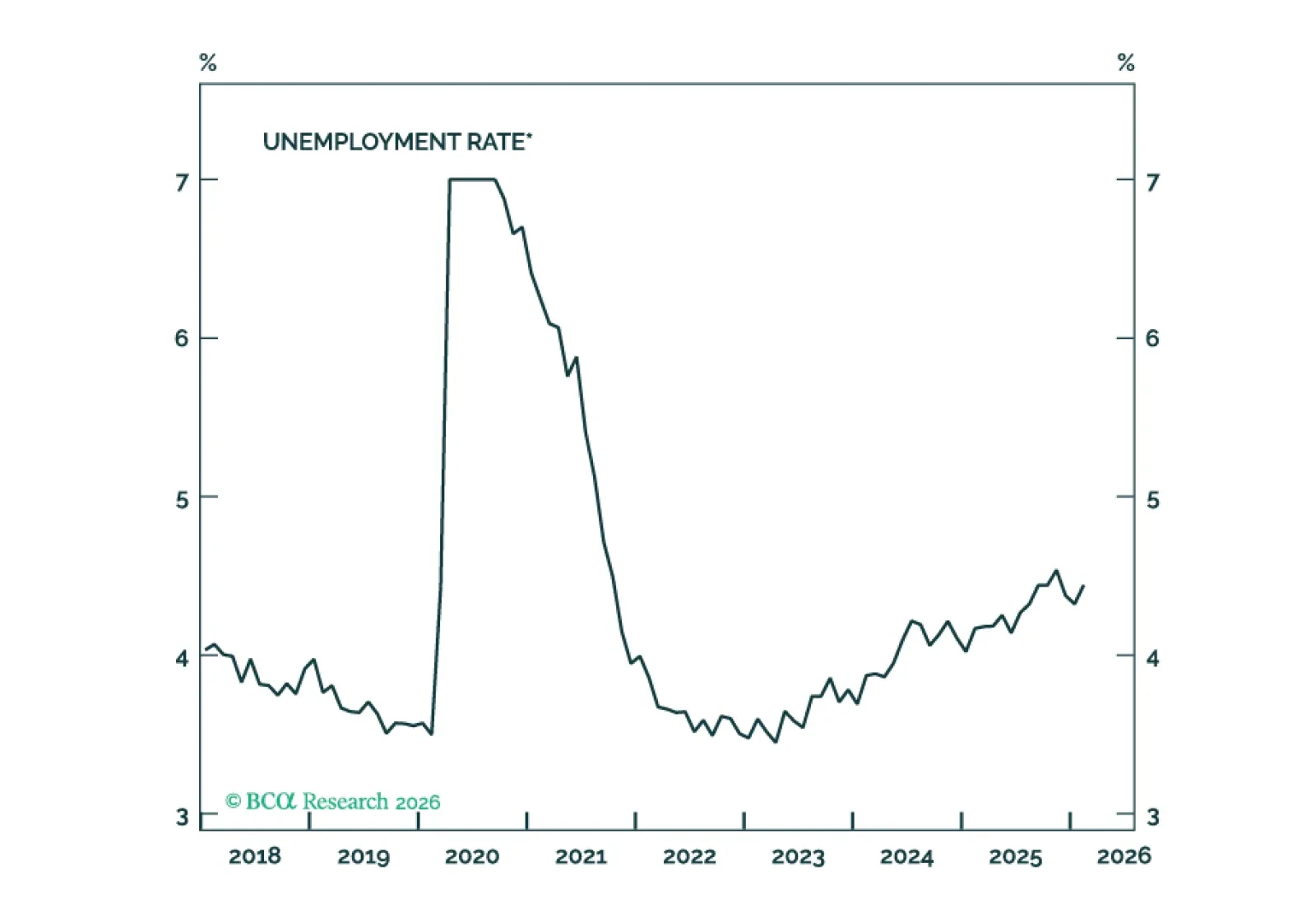

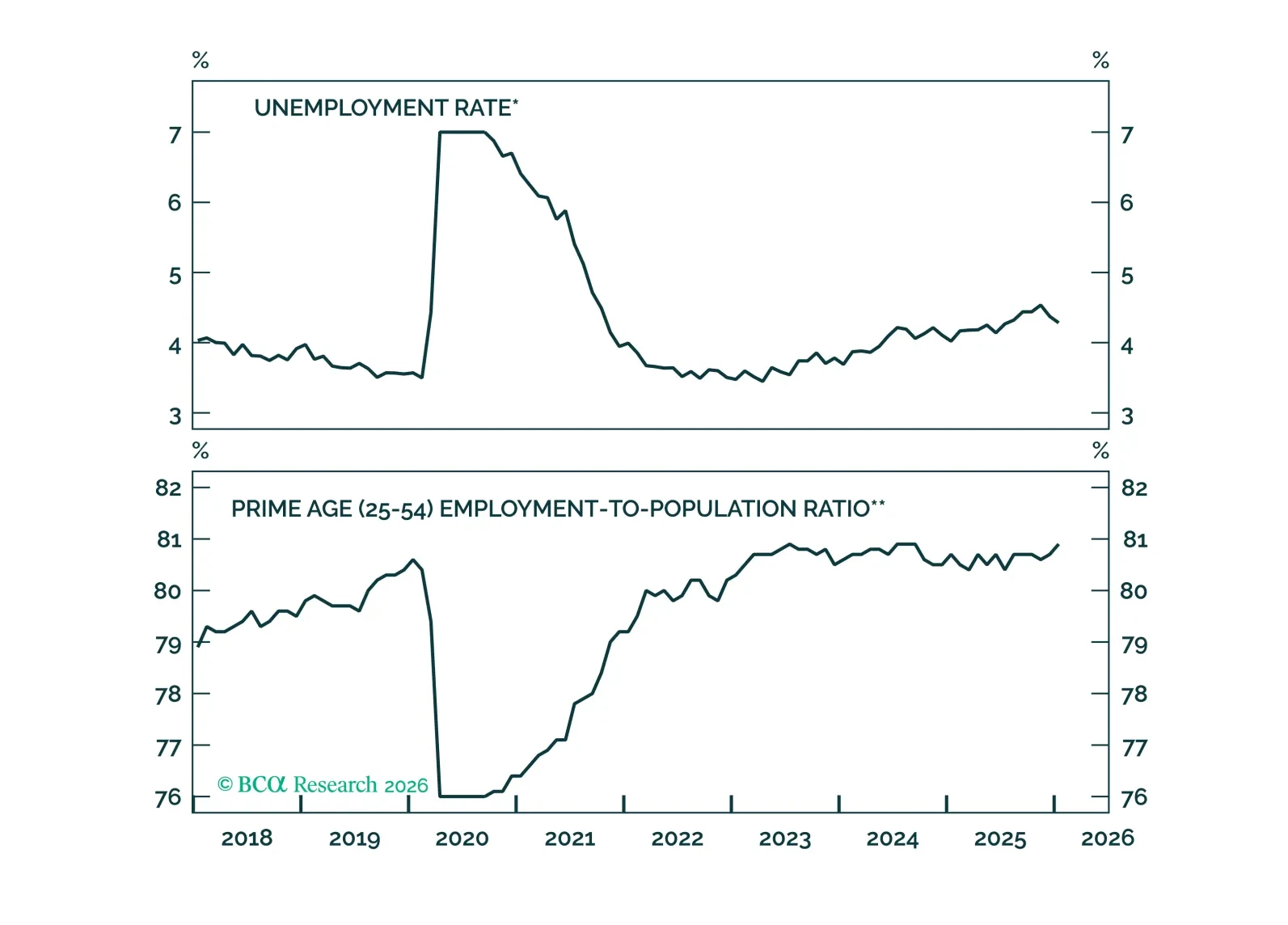

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

Iran doesn’t need to sink a single US warship; it could inflict much more damage by sinking the US stock and bond markets by disrupting shipping, trade, and oil tankers with decentralised low-tech drone warfare. We discuss why it is not the direct pain of higher oil prices, but the knock-on repercussions for stock and bond markets that could inflict the greater damage. Plus, a new tactical trade is to underweight Materials.

Our Portfolio Allocation Summary for March 2026.

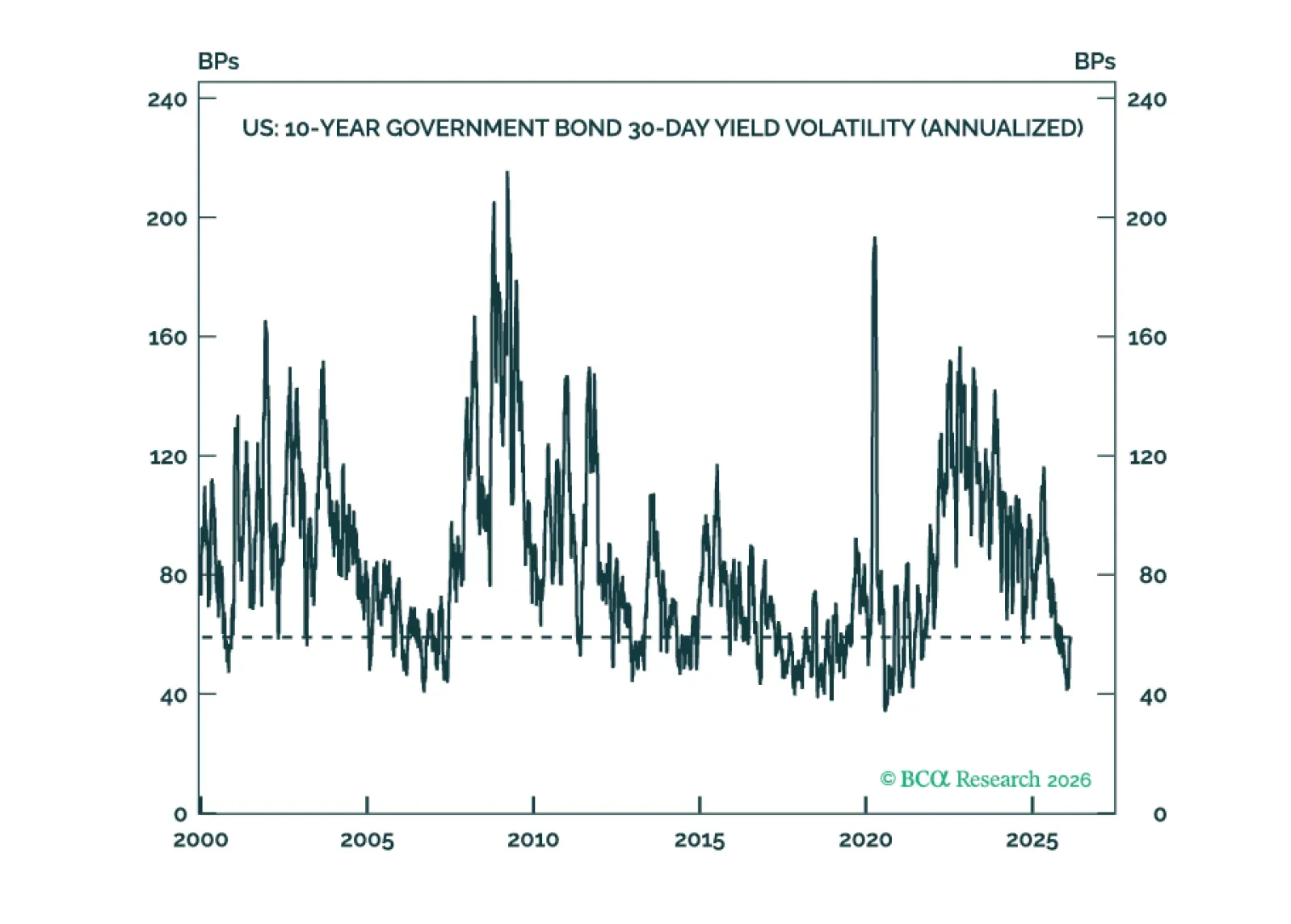

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

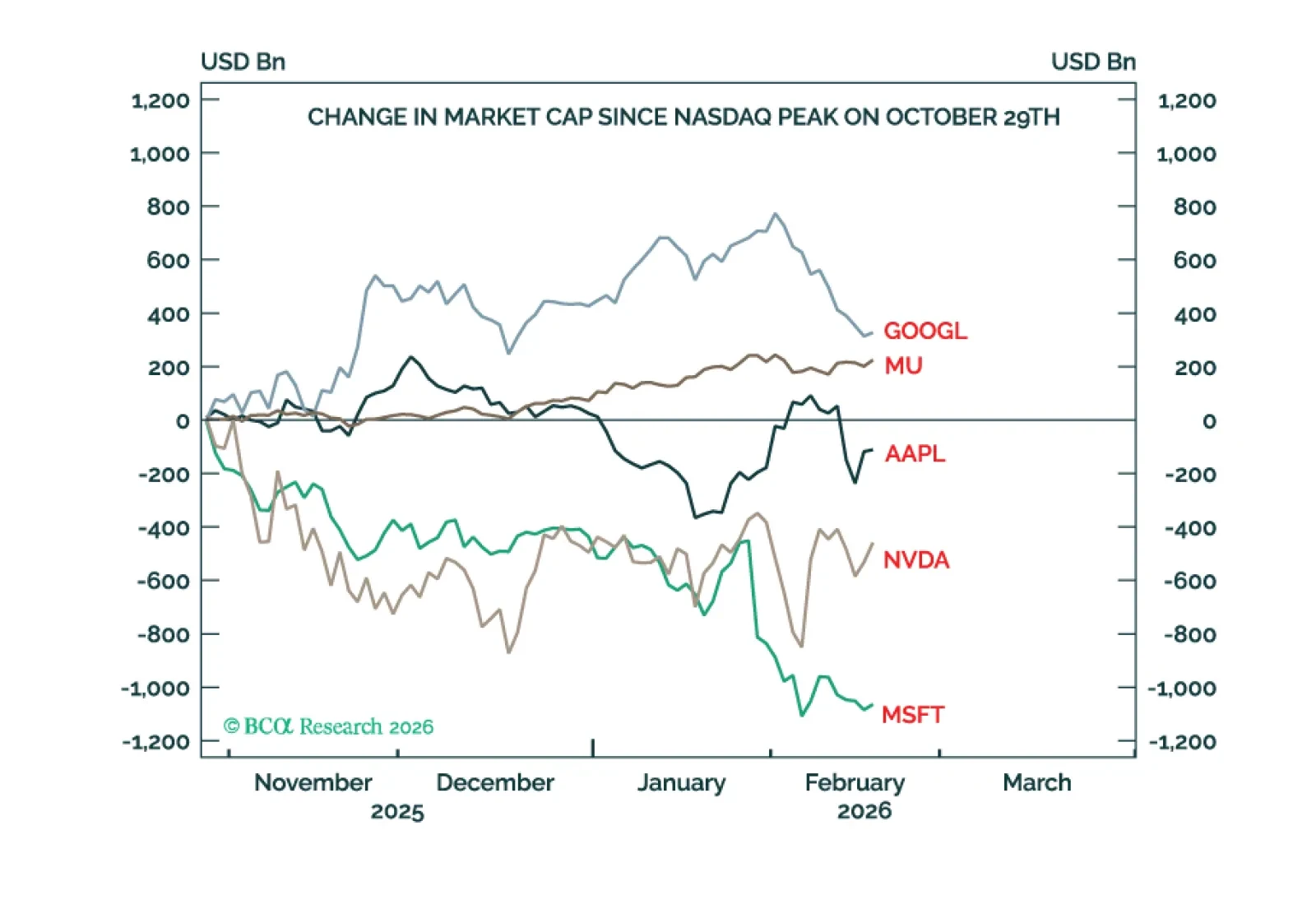

Tech has starkly underperformed other equity sectors and the tech-heavy US market has underperformed non-US markets, but global stocks are up and have comfortably outperformed bonds. This pattern of performances is likely to continue through the rest of 2026. Plus, two new tactical trades are: long coffee; and long ETH.

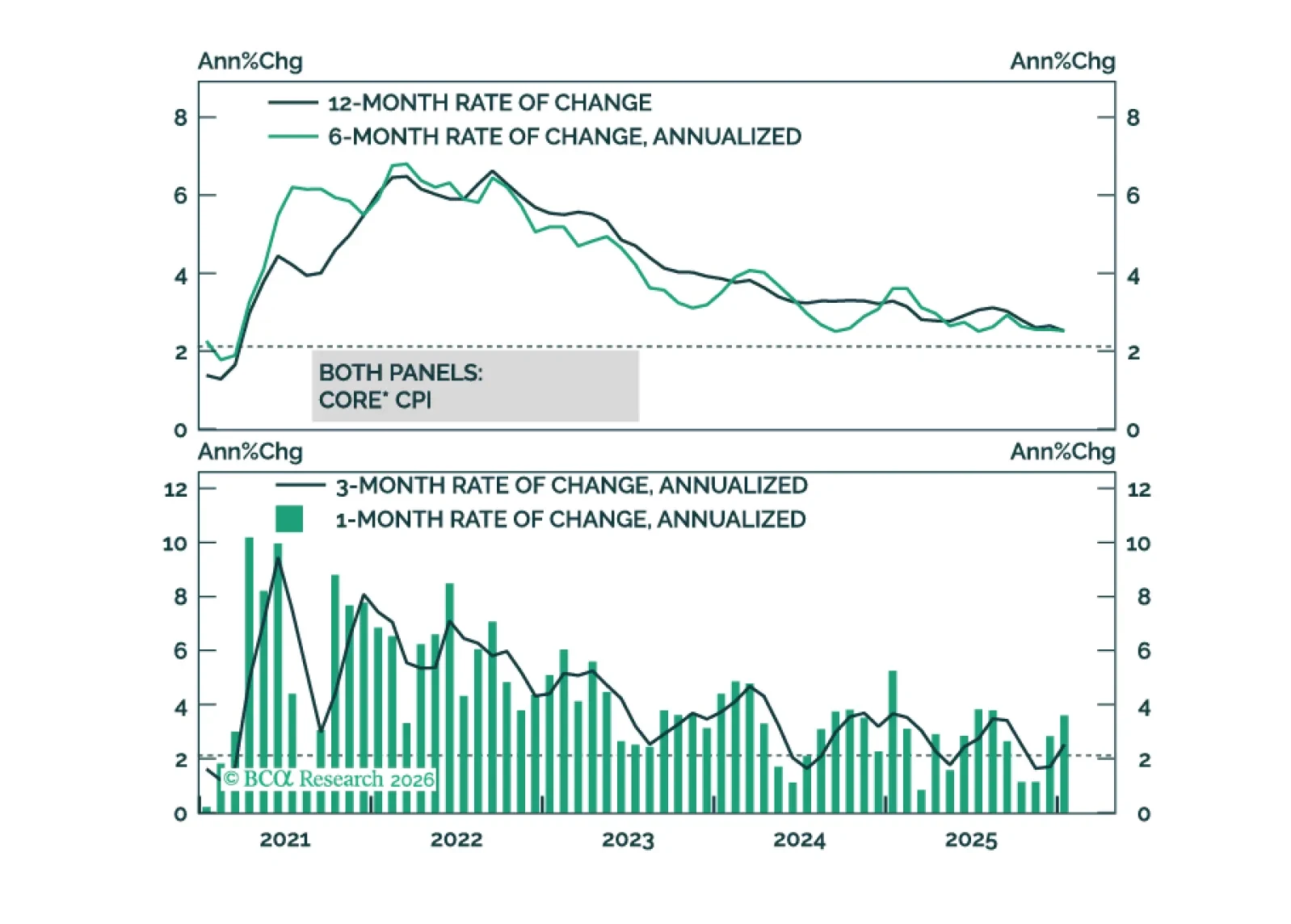

Core inflation will get close to the Fed’s 2% target by the end of this year.

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

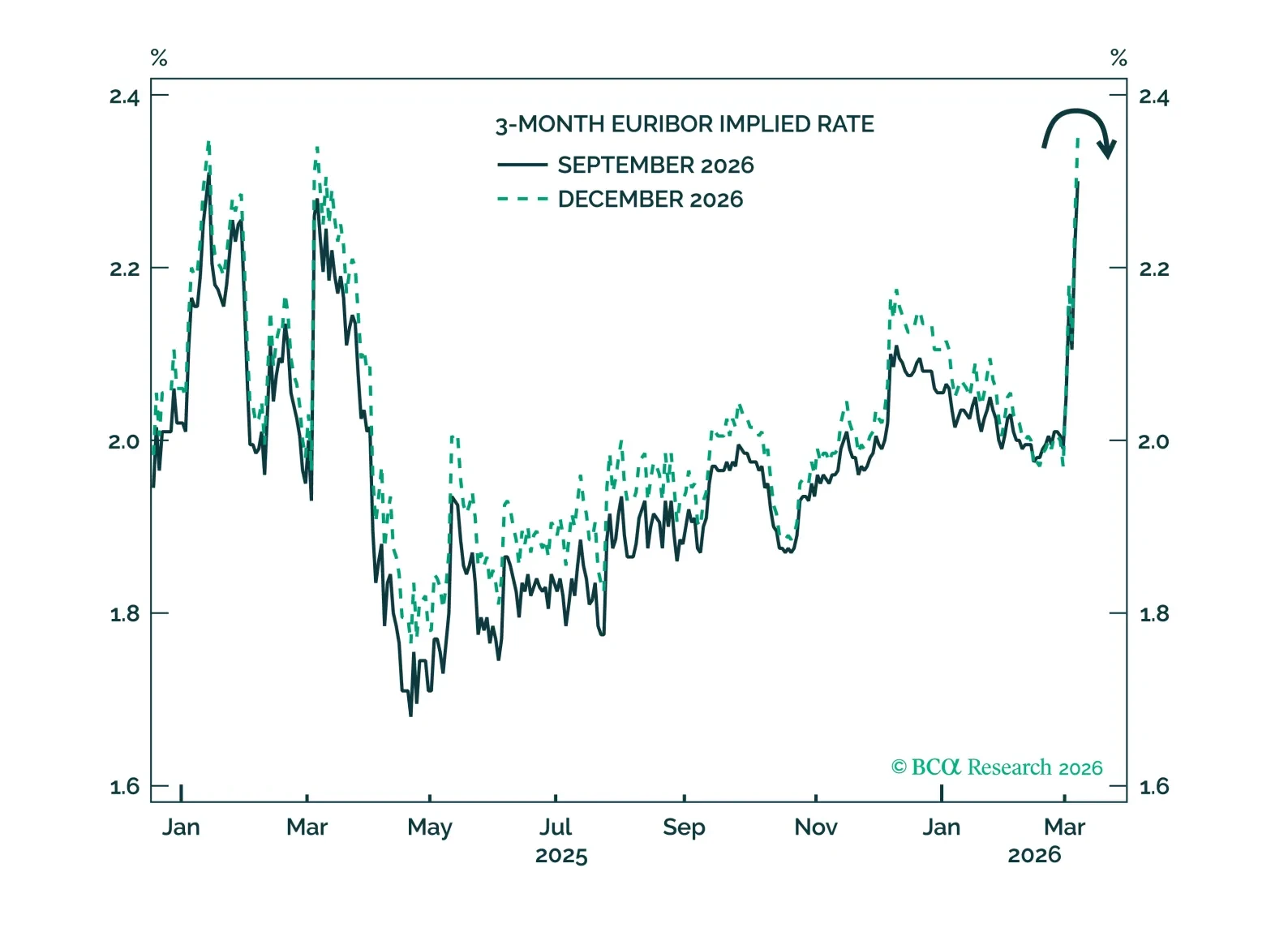

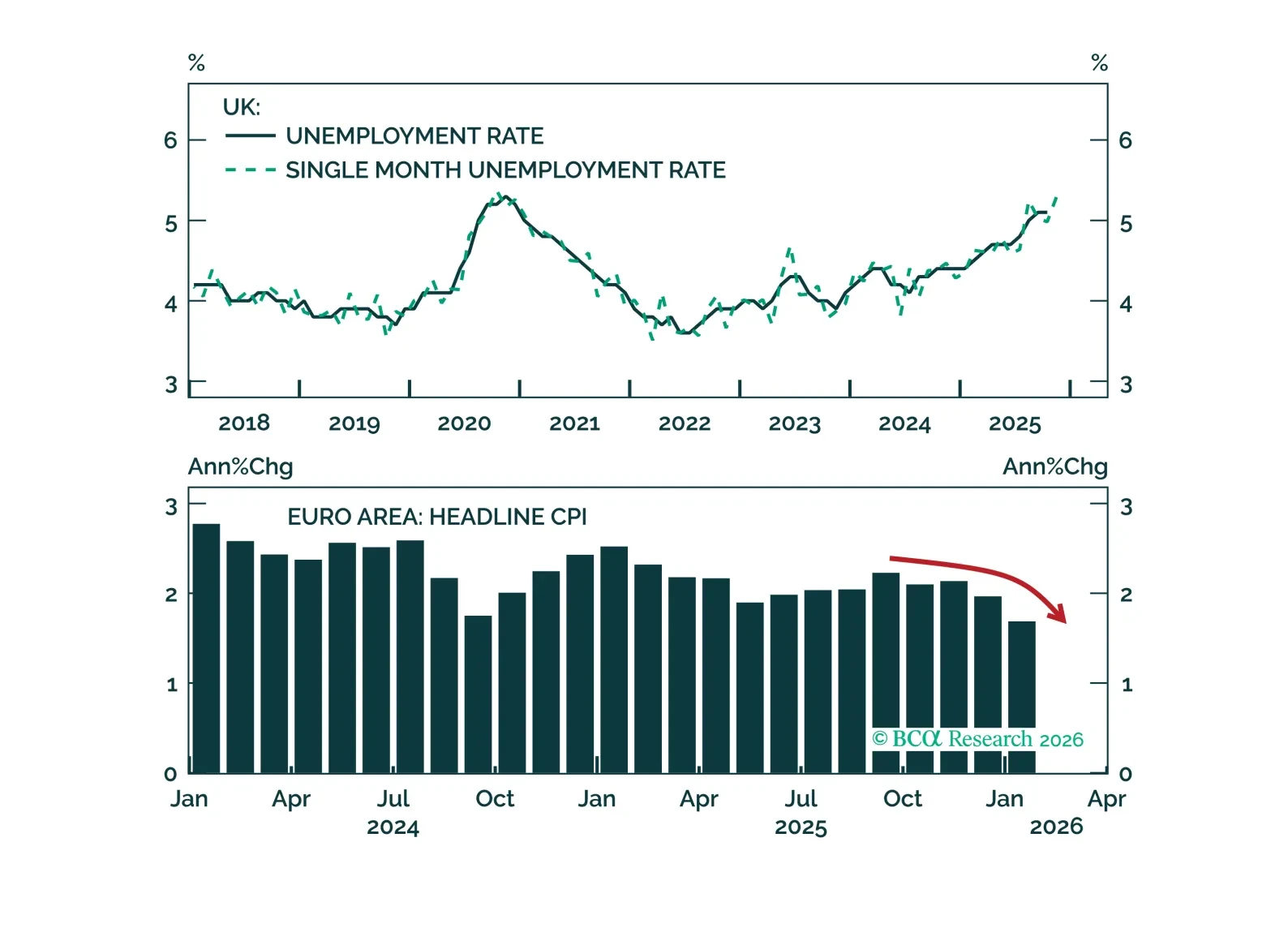

This week’s central bank meetings are a good reminder that monetary policy can still surprise. The Bank of England sounded more dovish, and the European Central Bank sounded complacent about the inflation undershoot. Meanwhile, the Reserve Bank of Australia hiked rates earlier this week. Investors should remain overweight UK Gilts, position for more ECB easing by going long the September 2026 3-month Euribor futures, and fade further rate hikes priced in Australia.

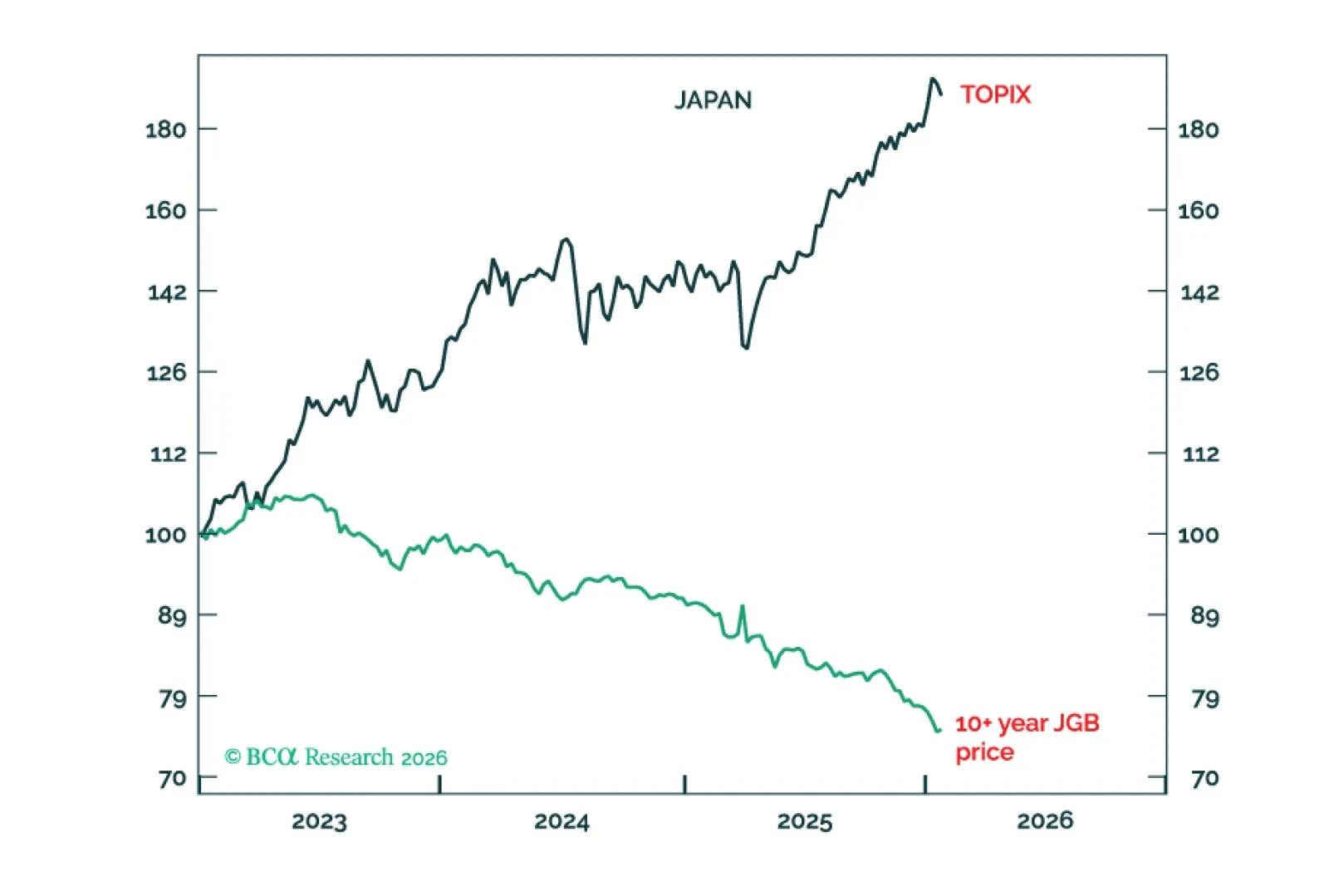

The US and Japan are in the same predicament: save the bond market or save the stock market? How this predicament will be resolved is the biggest global macro call of 2026-27. Plus: a new tactical trade is to go short AUD/JPY.