Fixed Income

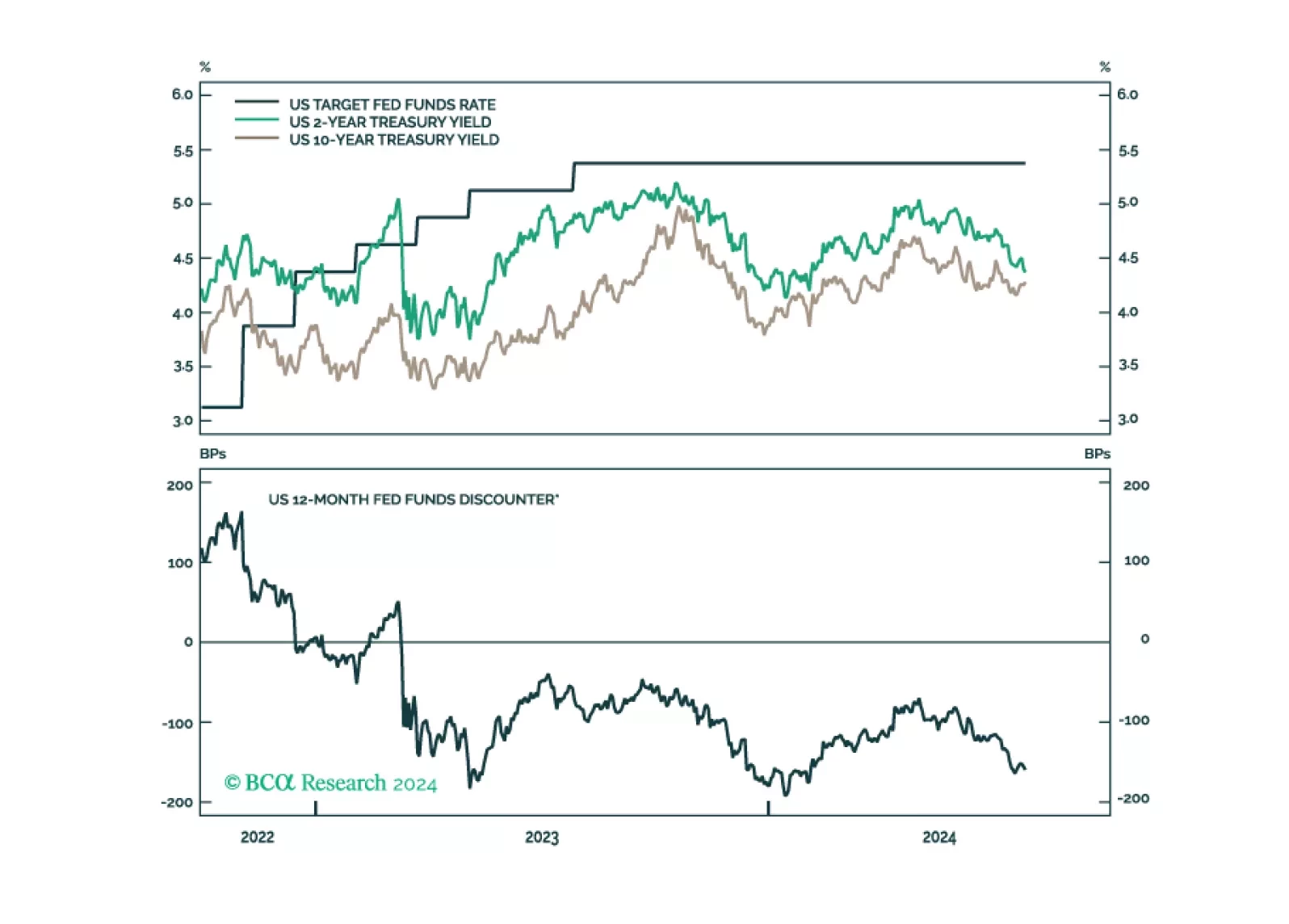

After this morning’s jobless claims number, we have now seen enough deterioration in our preferred labor market indicators to increase portfolio duration from “at benchmark” to “above benchmark”.

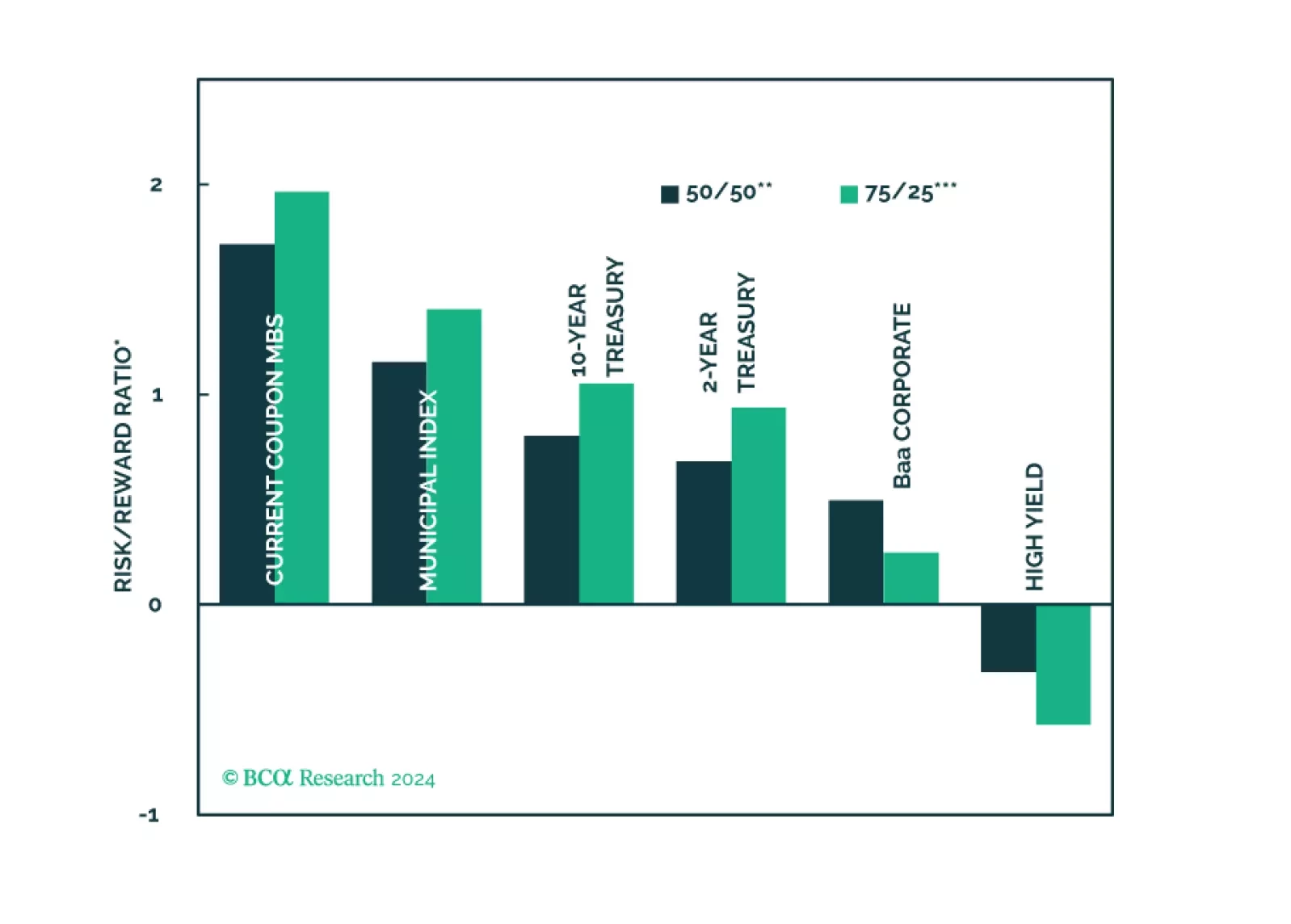

We calculate expected returns for several different US fixed income sectors with a focus on how municipal bonds stack up against the investment alternatives.

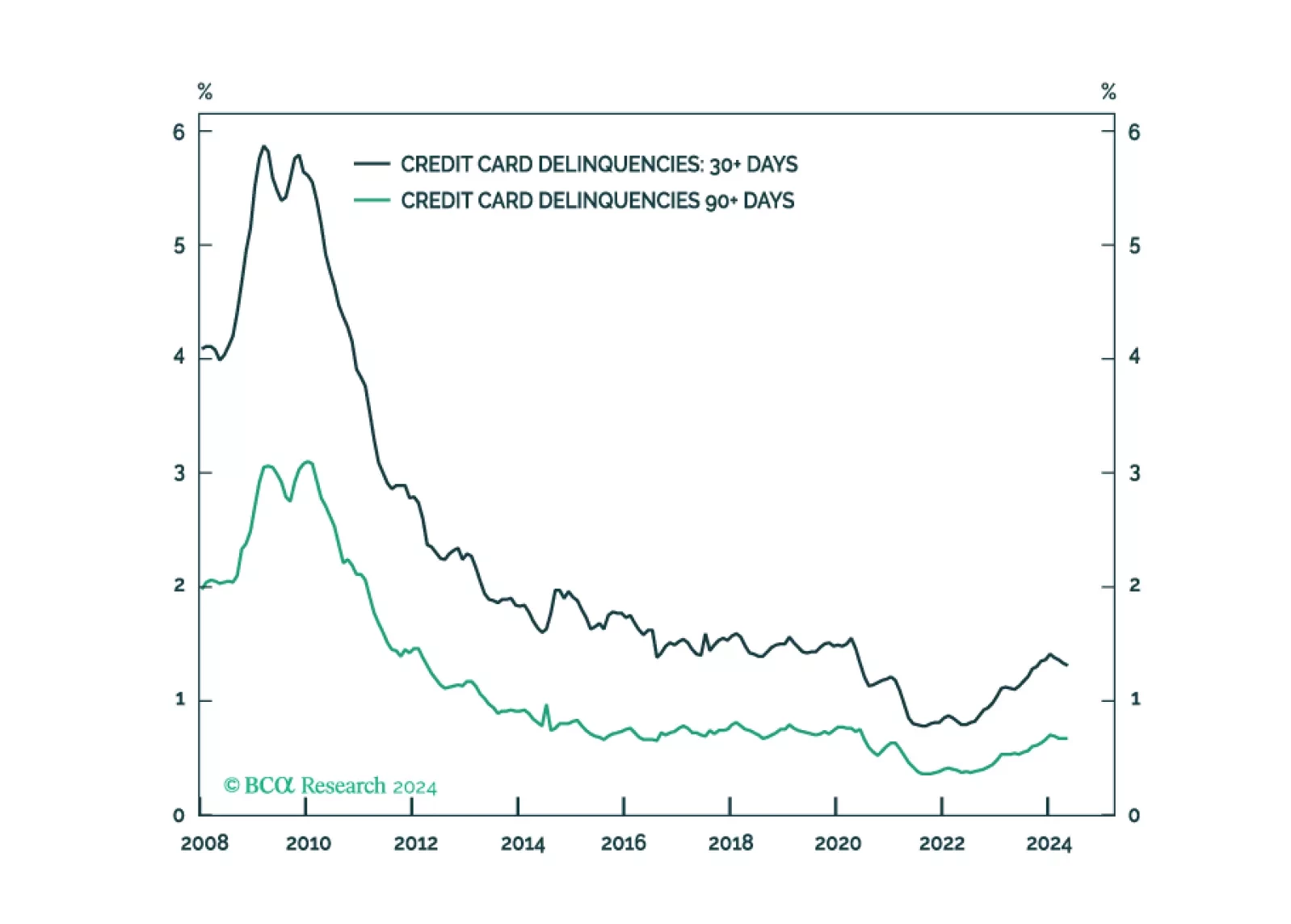

It’s status quo for the SIFI banks, as they don’t see consumer credit performance materially worsening from now-normalized levels and they are not meaningfully exposed to commercial real estate losses.

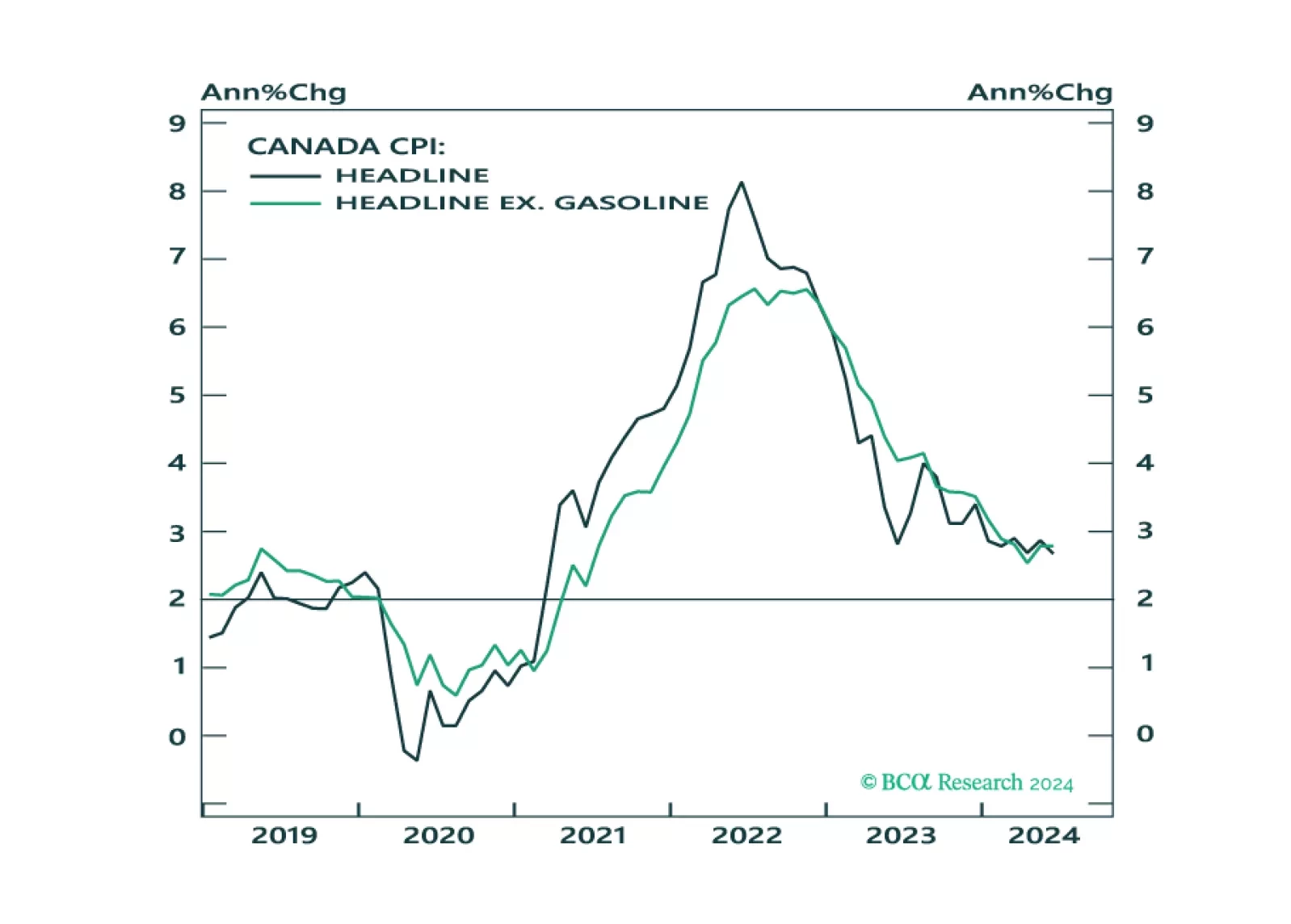

In this Insight, we look into the recent CPI release in Canada, and the possible implications for fixed-income market trades.

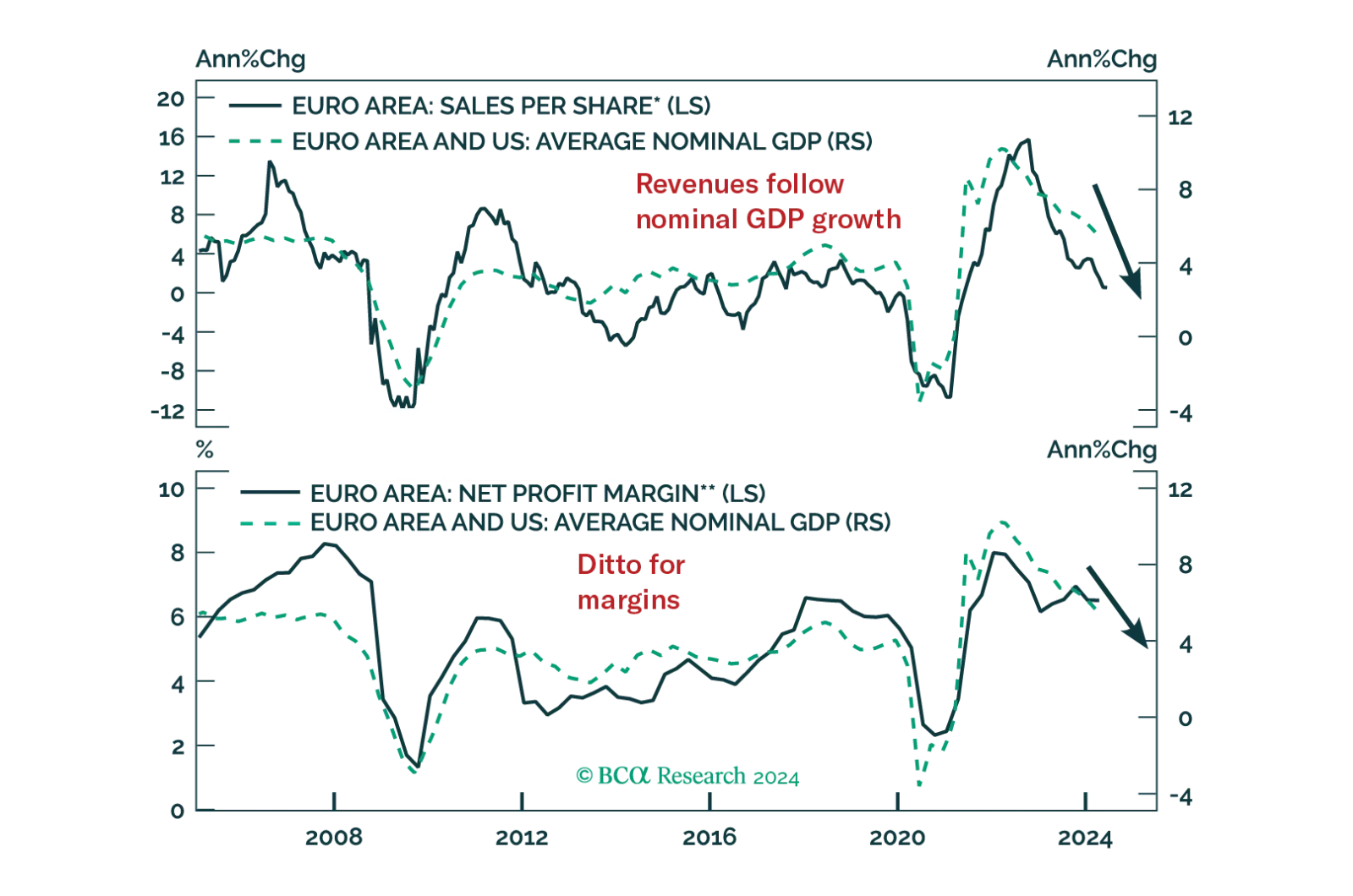

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?