Fixed Income

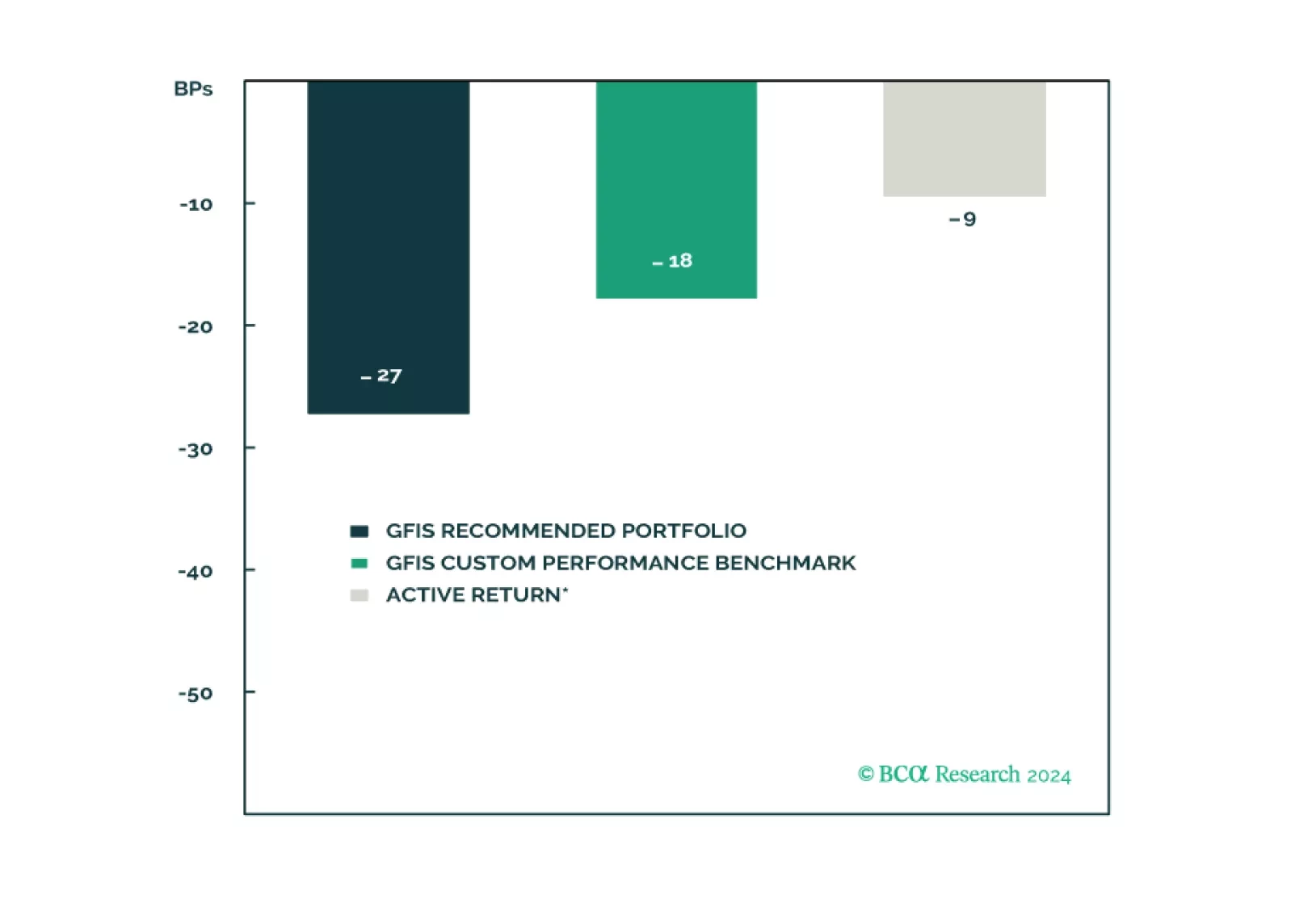

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.

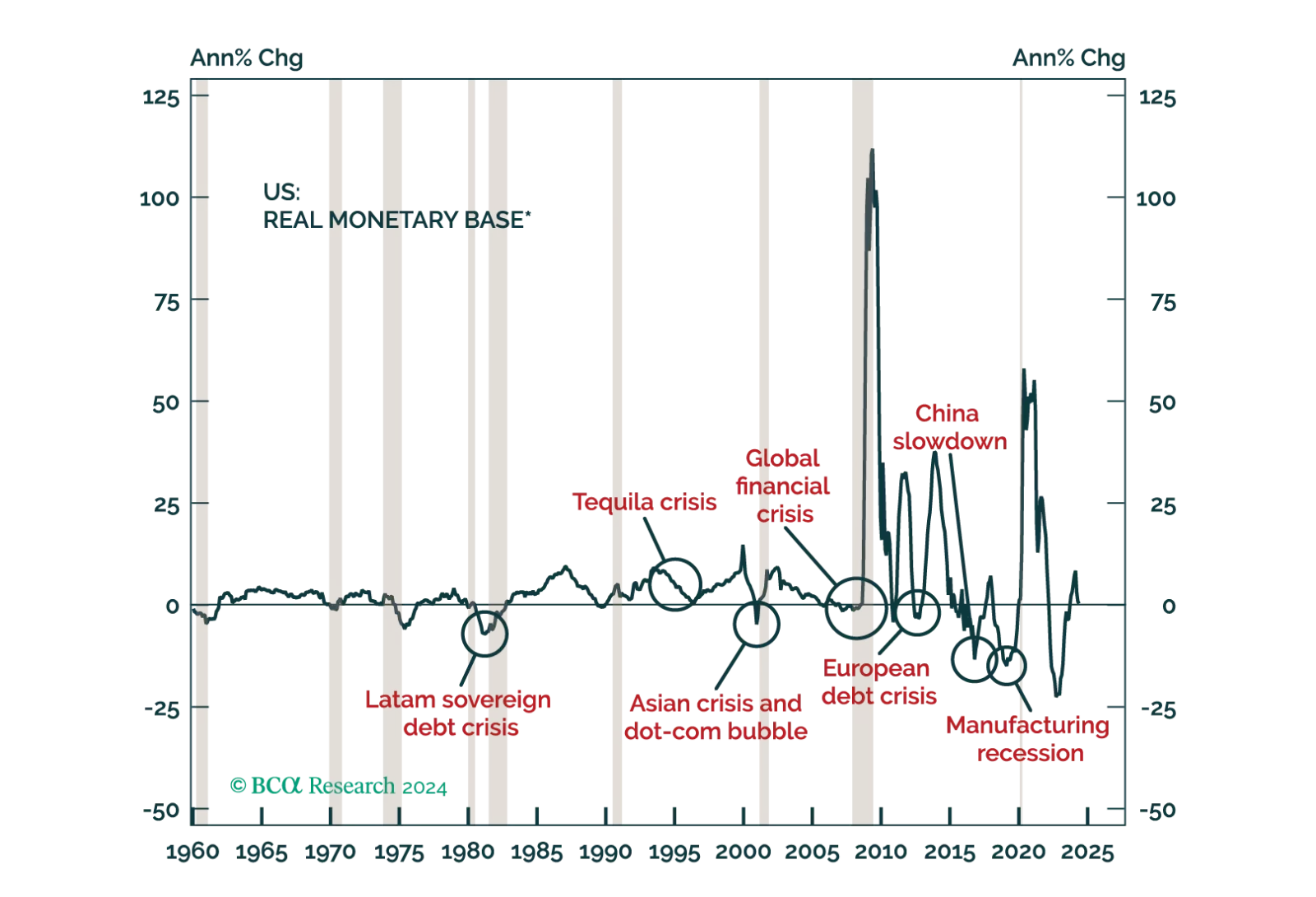

US dollar liquidity has been shrinking, which has important ramifications for global asset prices, including currencies. In this report, we delve into the process of dollar liquidity creation and the outlook for currencies over the next six-to-twelve months.

In light of last week’s employment report and this morning’s CPI, it’s time for the Federal Reserve to cut rates.

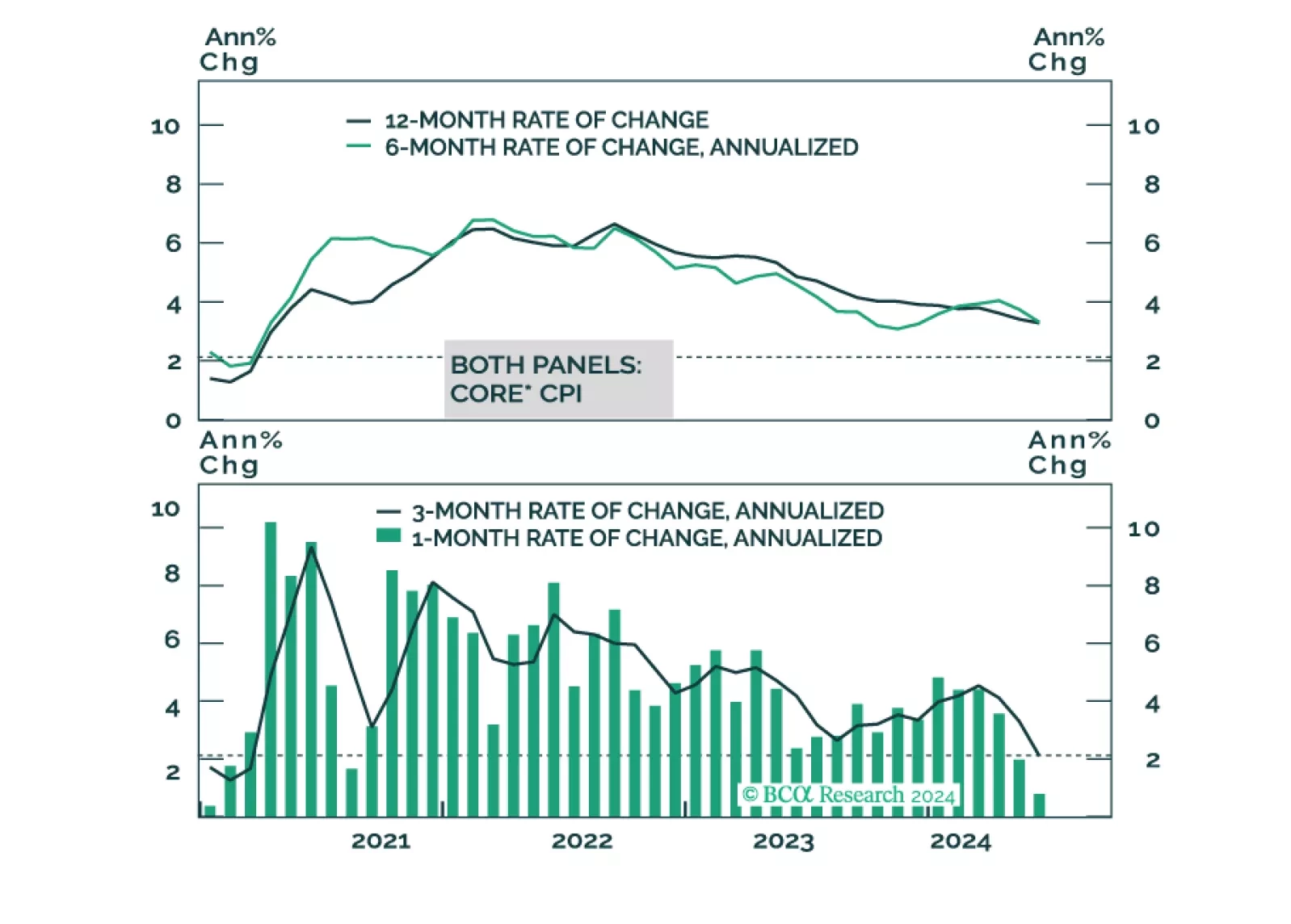

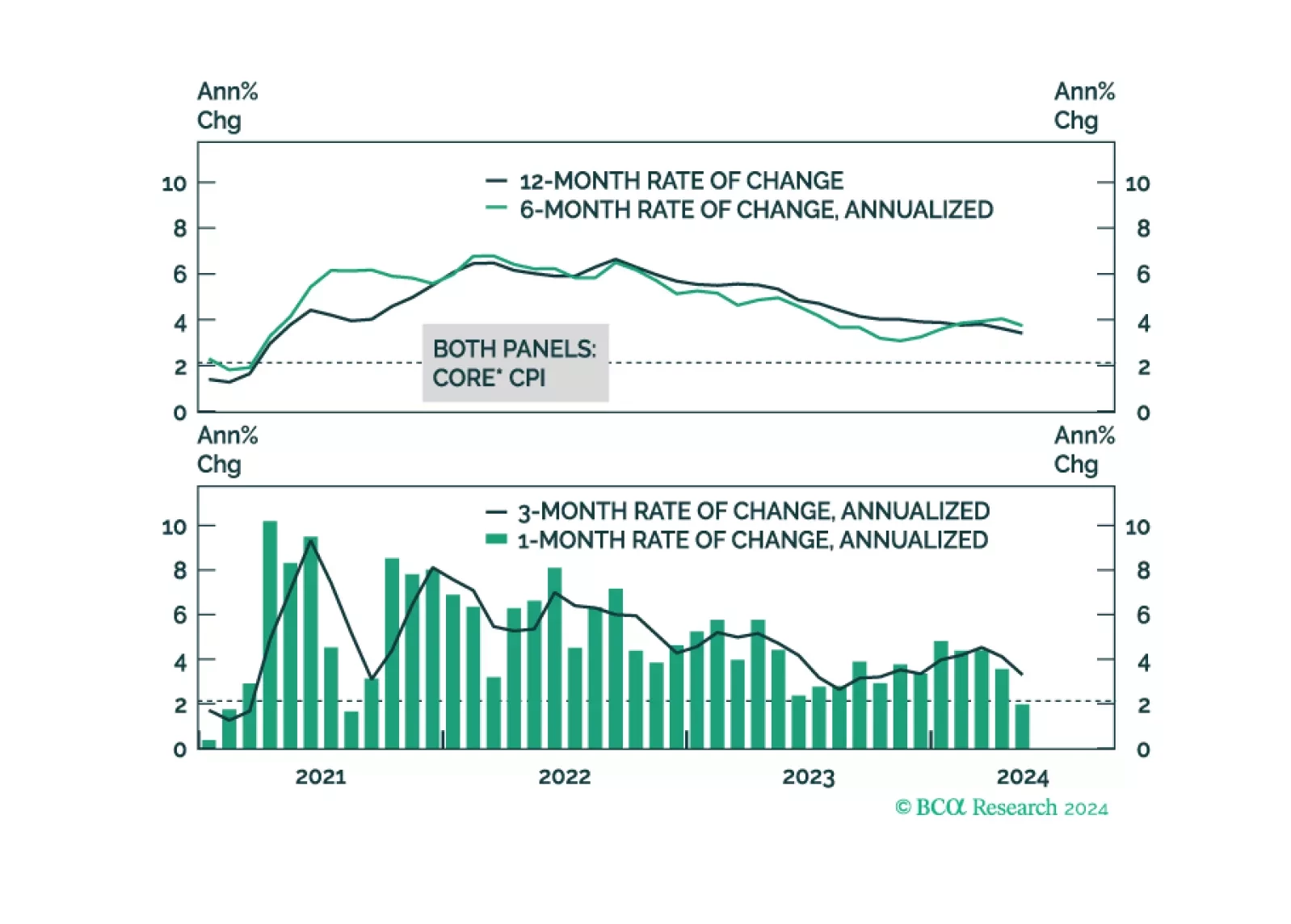

We consider the outlook for CPI inflation over the next 12 months. Our baseline forecast calls for core CPI to hit 2.40% during this timeframe and for headline CPI to fall between 1.74% and 2.49%.

Although we ticked a second box on our checklist, the incoming data still do not indicate that a recession is imminent. We remain tactically equal weight equities with a strong bias to underweight them, but we’re not exiting the party just yet.

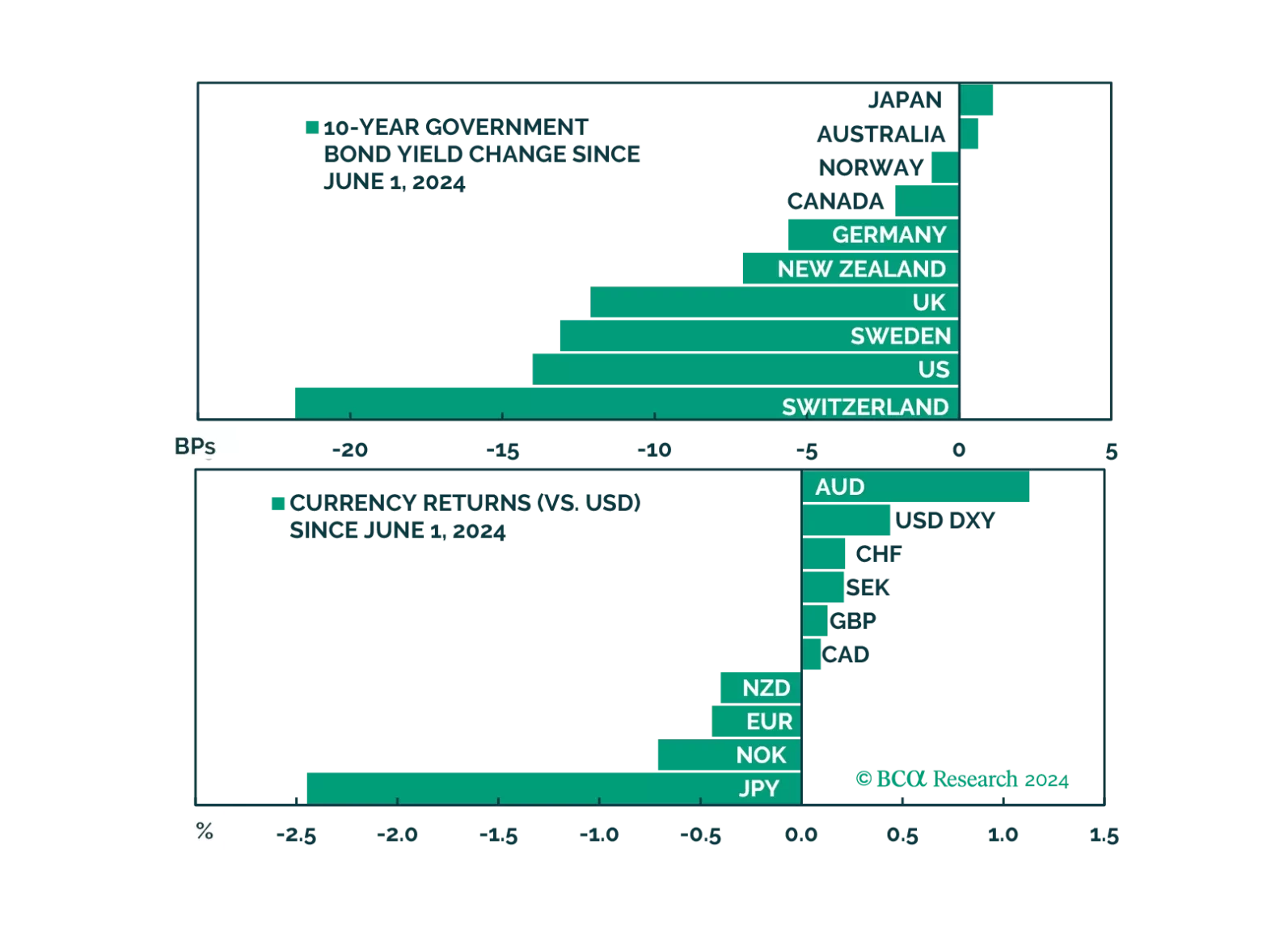

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.