Fixed Income

Credit spreads continue to price in a Goldilocks scenario. US investment grade and high-yield OAS have tightened 41 and 137 bps from their October peaks, resulting in handsome outperformance by both sectors relative to duration-equivalent Treasuries. …

US headline CPI inflation decelerated to a softer-than-expected 0.3% m/m (3.4% y/y) in April, from 0.4% m/m (3.5% y/y). Core CPI eased from 0.4% m/m (3.5% y/y) to 0.3% m/m (3.4% y/y). Declines in new (-0.4% m/m) and used vehicles (-1.4% m/m) prices largely…

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.

Despite historically high interest rates and the fact that variable-rate mortgage issuances dominate the mortgage market landscape, Australian home prices continue to climb at a close to double-digit annual rate. The Core Logic House Price index is now…

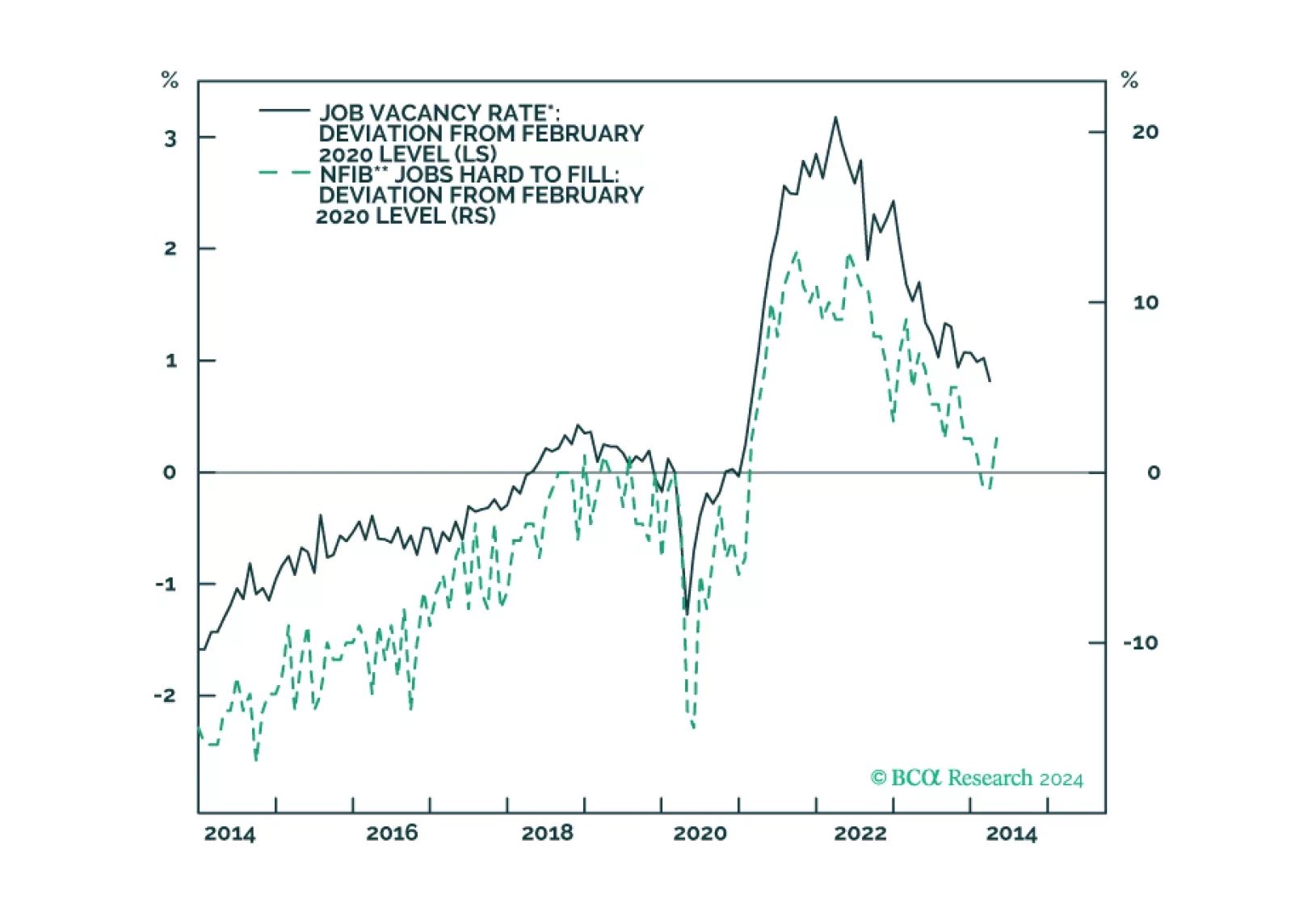

The US Citi Economic Surprise Index has recently dipped below zero, indicating that US economic data releases have been disappointing expectations. Most notably, the ISM Services PMI started contracting in April against anticipation of a faster pace of…

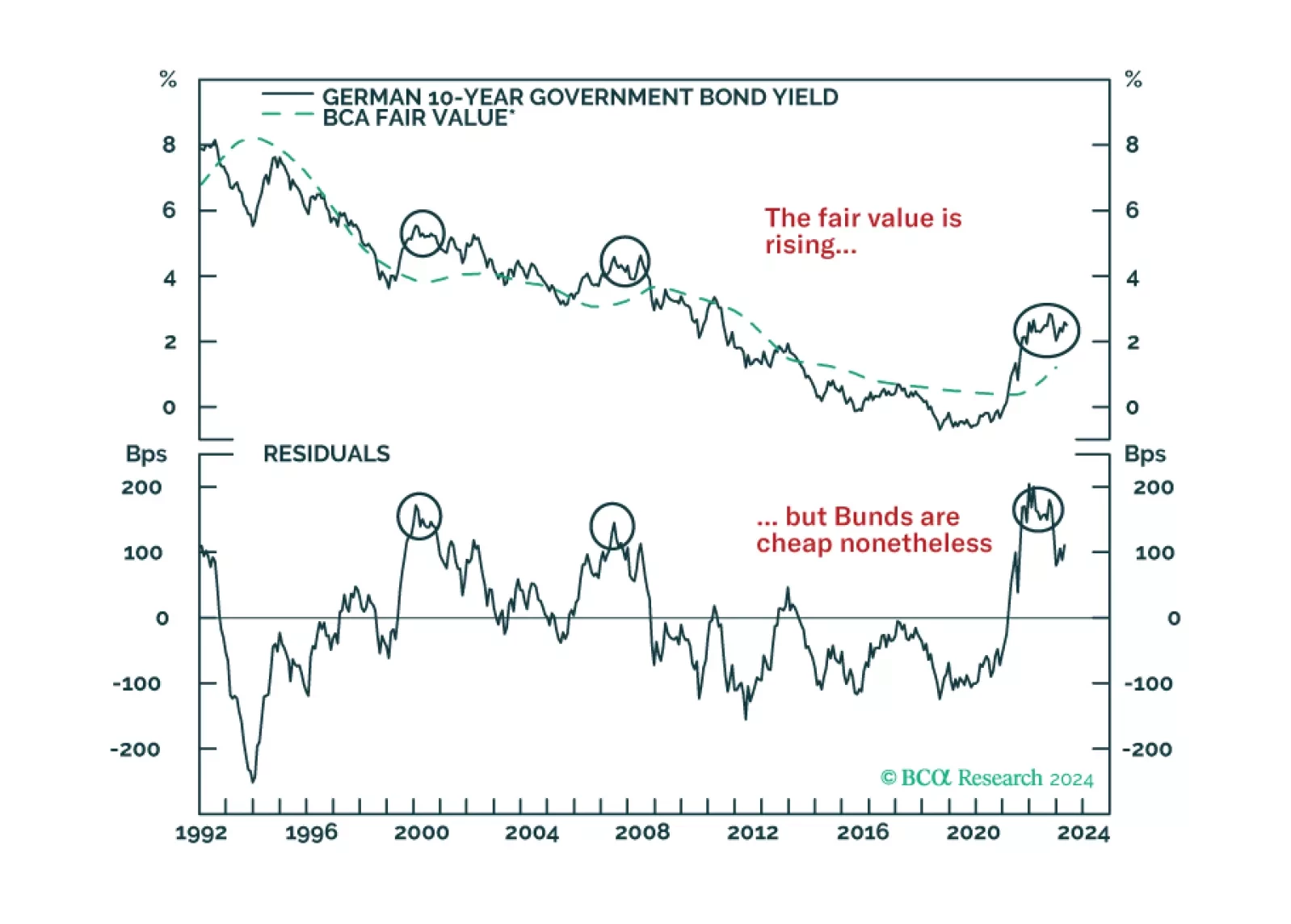

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

The Canadian economy added 90.4 thousand jobs in April, up from a new loss of 2.2 thousand jobs in March. The April reading beat expectations of a more moderate increase of 20 thousand. The services sector entirely explains April’s employment growth; services…

Preliminary GDP estimates suggest that the UK economy started growing again in Q1, thus exiting a technical recession in the past two quarters. Q1 growth came in at 0.6%, improving from a 0.3% contraction last quarter, surpassing expectations of 0.4%. On a…

The idea that rising interest rates benefit value at the expense of growth has become consensus amongst market participants. The rationale is simple: Most of the cashflow that shareholders will receive from growth stocks are farther into the future than…

In this report, we review our trade recommendations based on incoming data in the last month.