Fixed Income

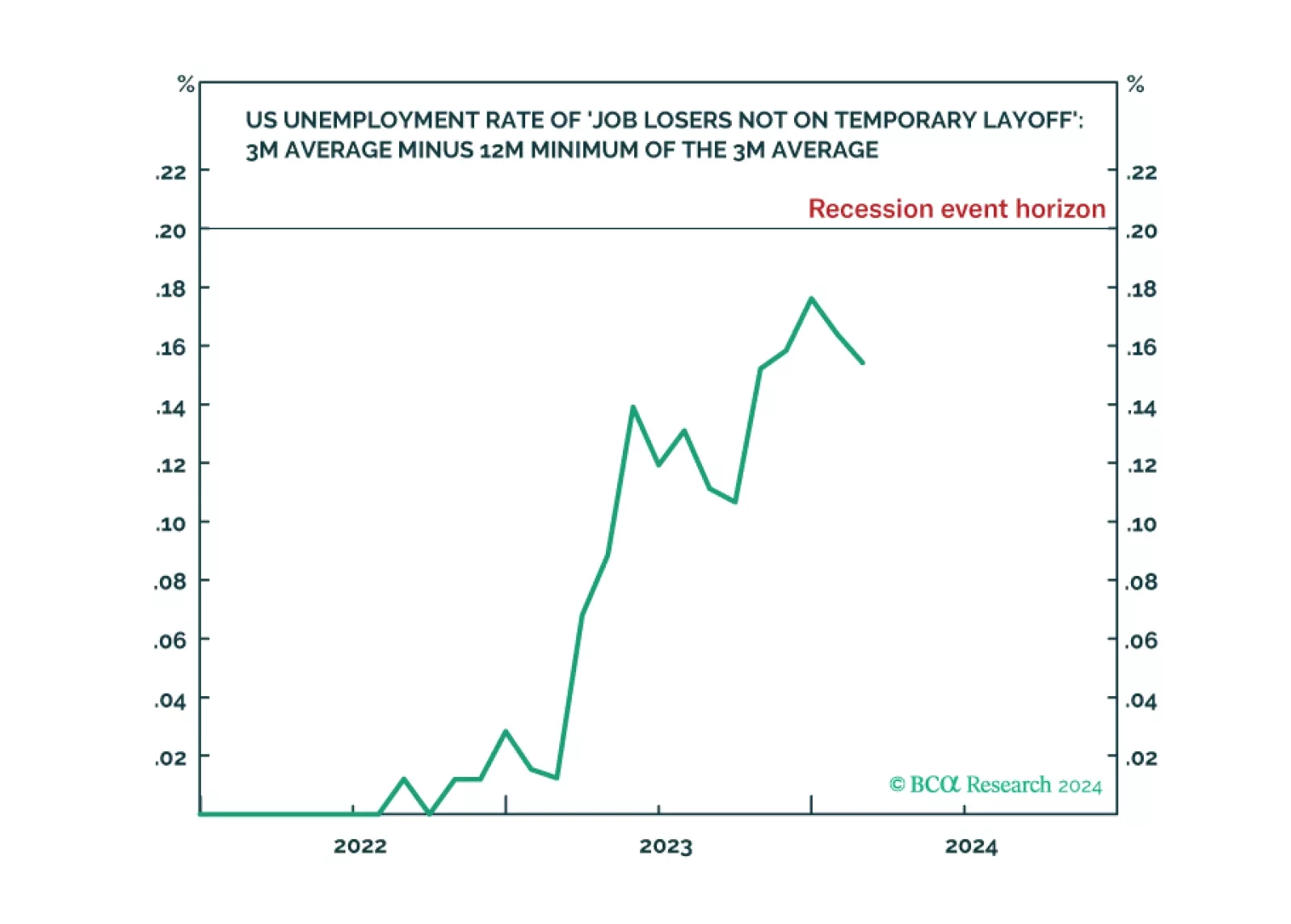

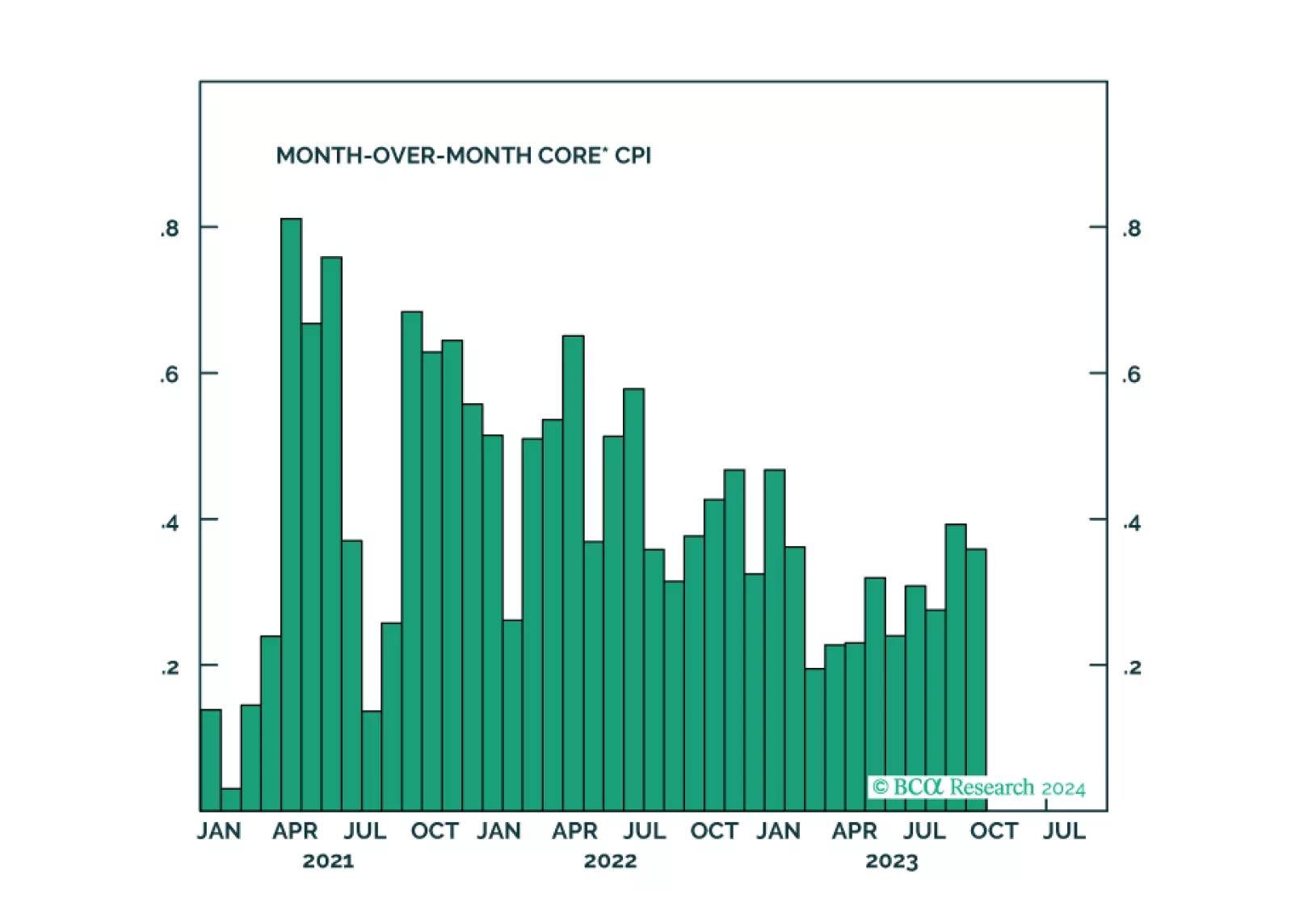

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

Our Portfolio Allocation Summary for March 2024.

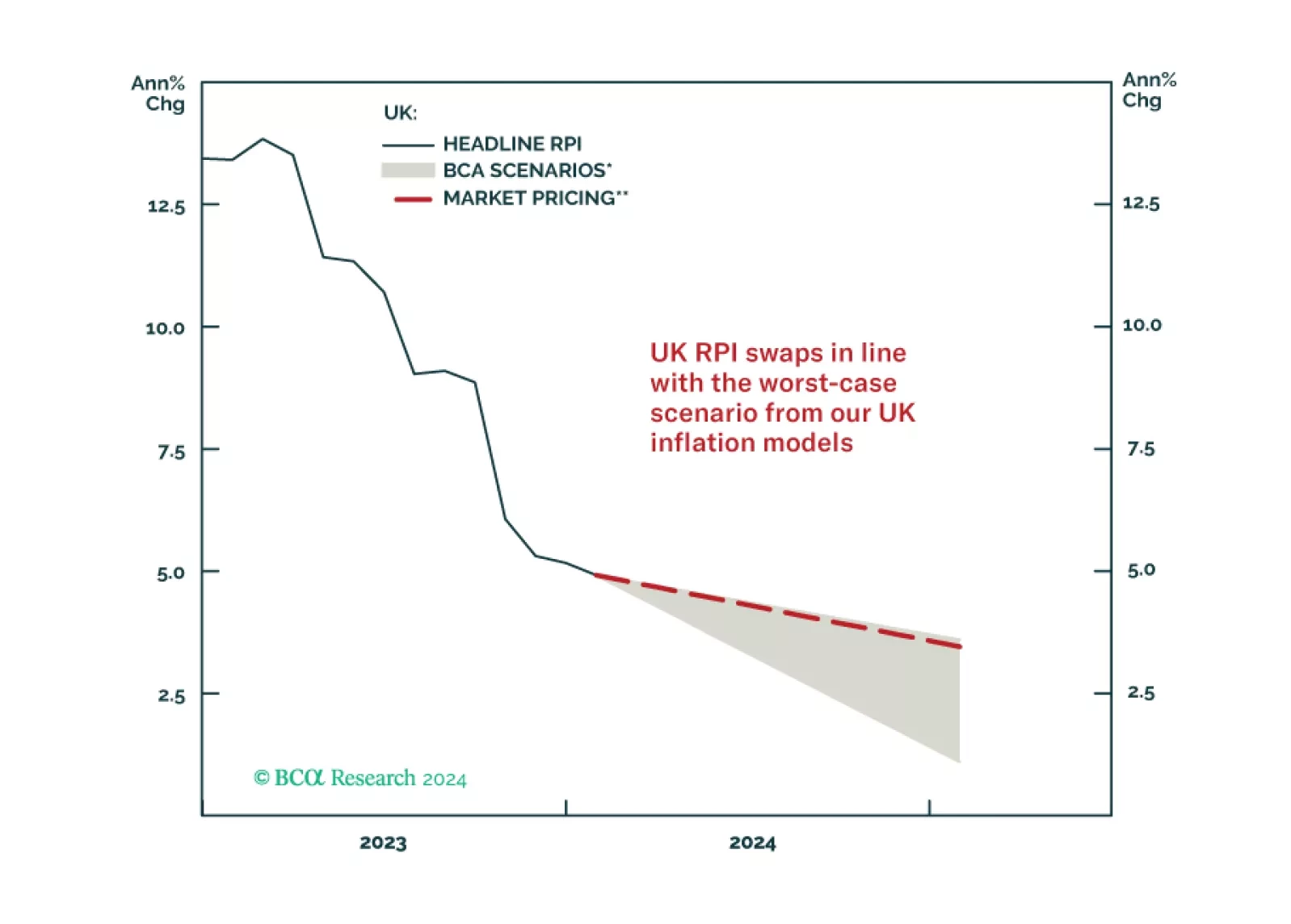

In this Special Report, we introduce our UK Linkers Golden Rule – a framework to profitably trade and invest in UK inflation-linked bonds versus nominal UK gilts. The Rule is currently signaling that nominal Gilts should outperform UK linkers over the next year as UK inflation slows.