Fixed Income

Our key US fixed income views for 2026.

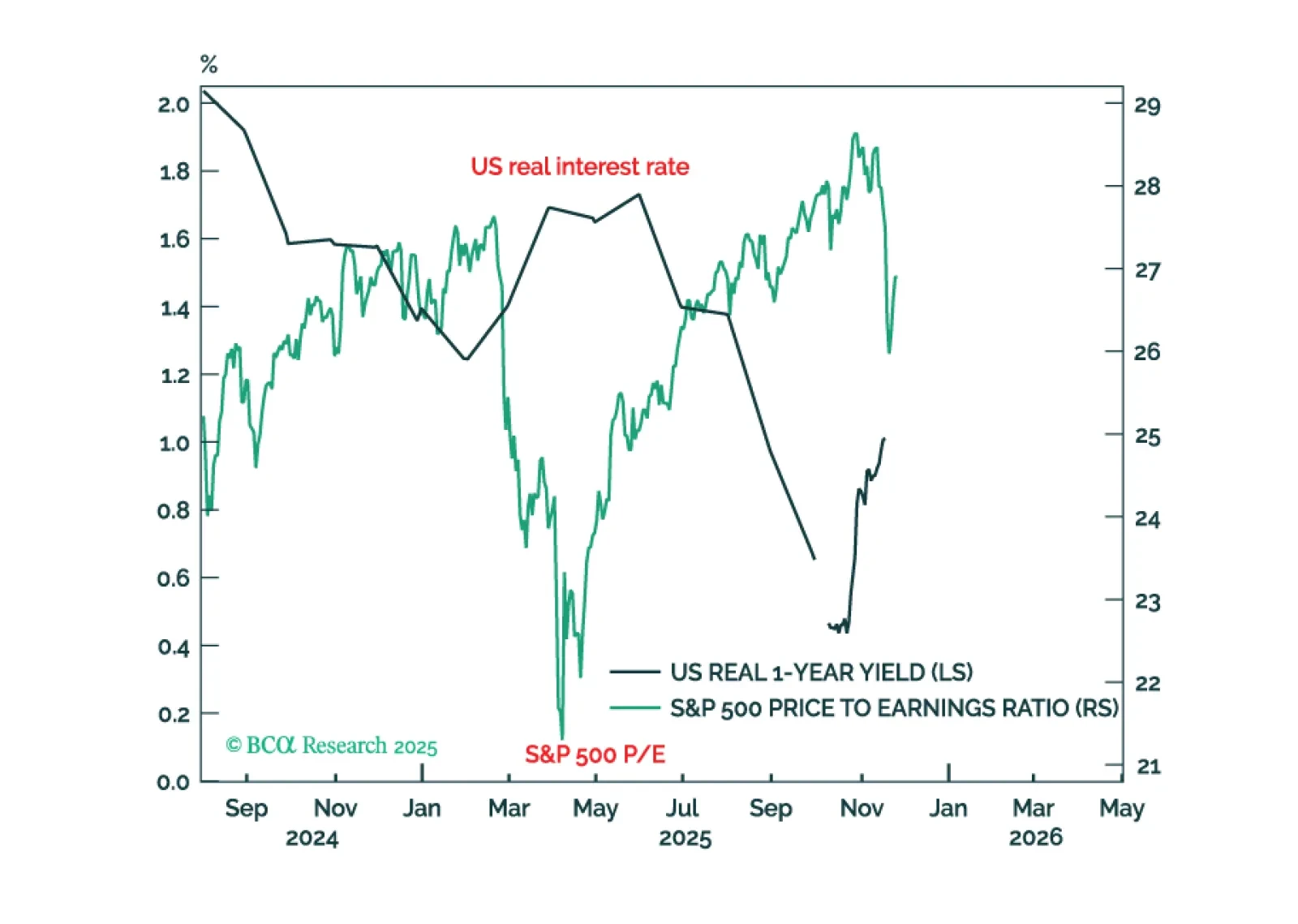

Stock market valuations are moving as a near-perfect mirror image of the US real interest rate, meaning that the Fed is underpinning the stock market. But if the market stopped believing in AI-driven profits growth, valuations would collapse, irrespective of the Fed’s efforts to underpin them. When might this happen? Plus, two new tactical trades are: long BTC versus gold; and overweight industrials.

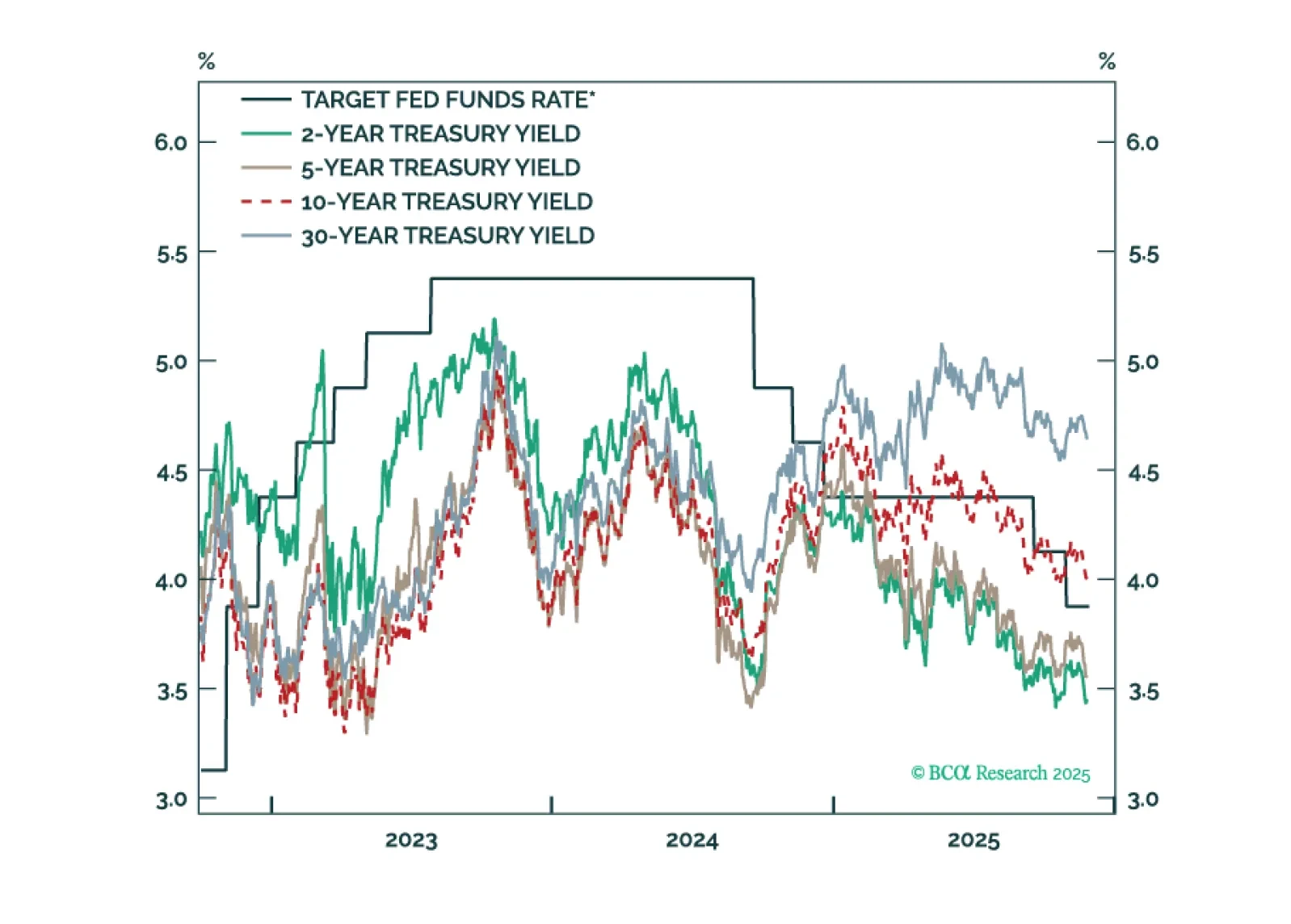

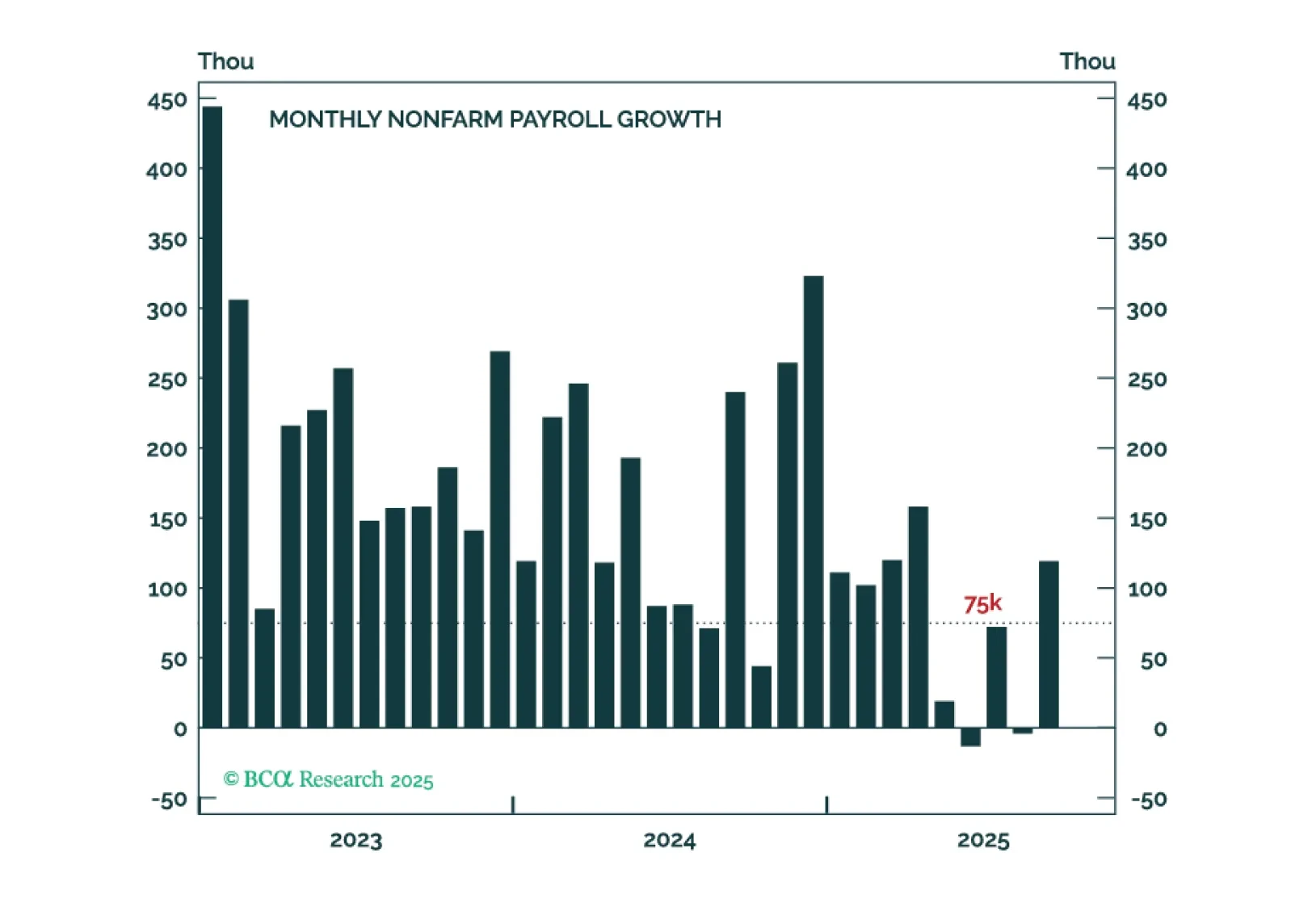

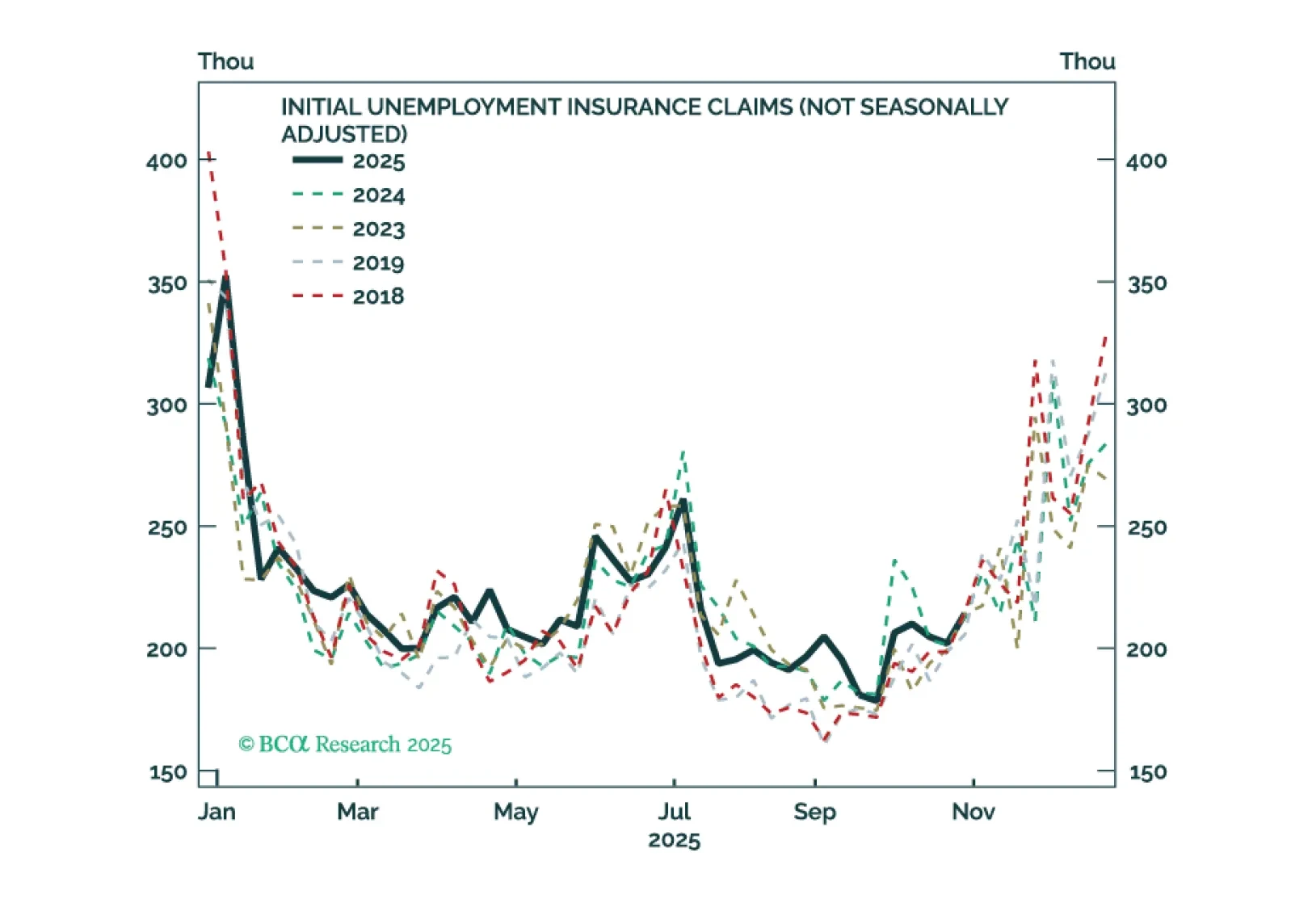

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

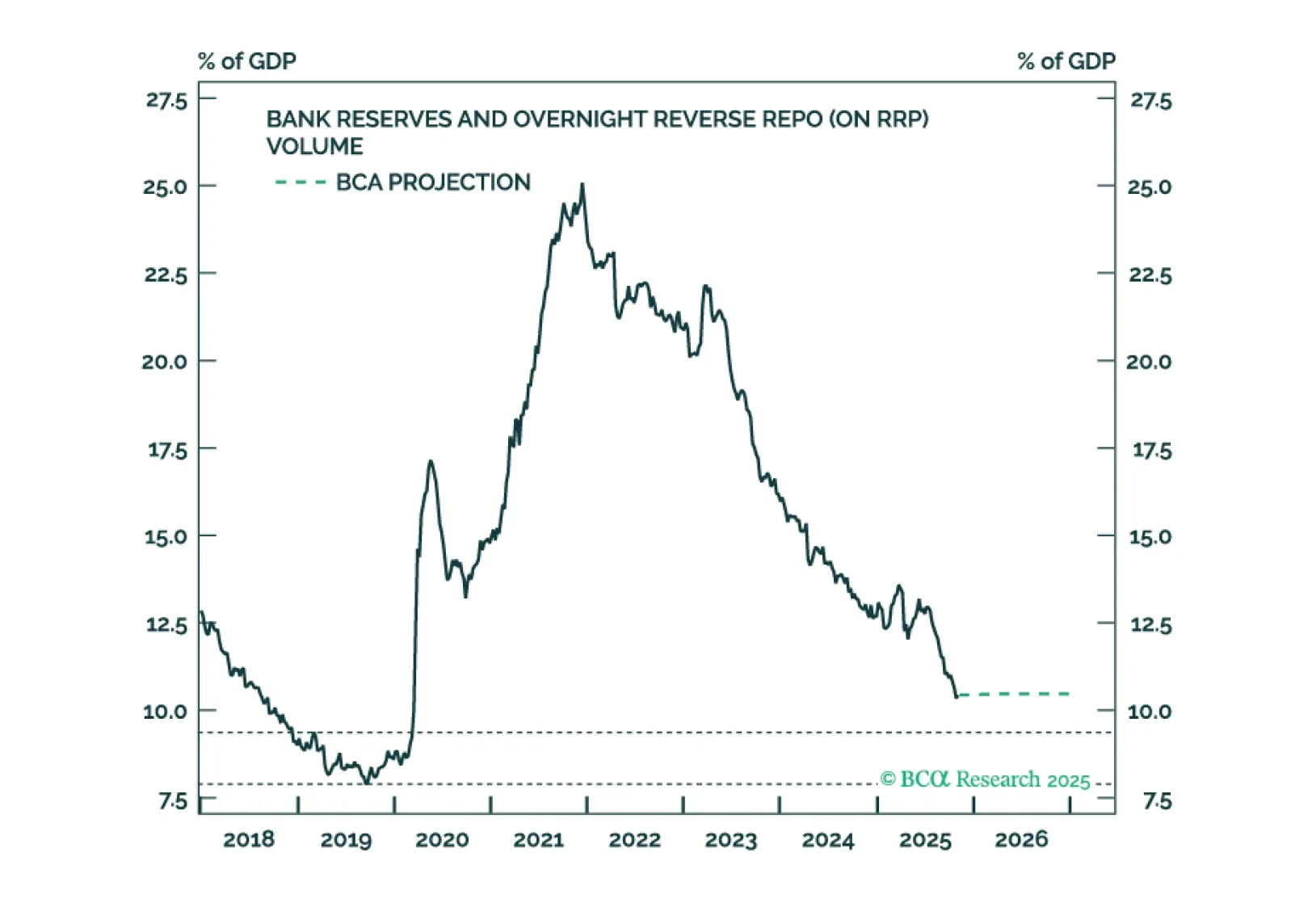

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

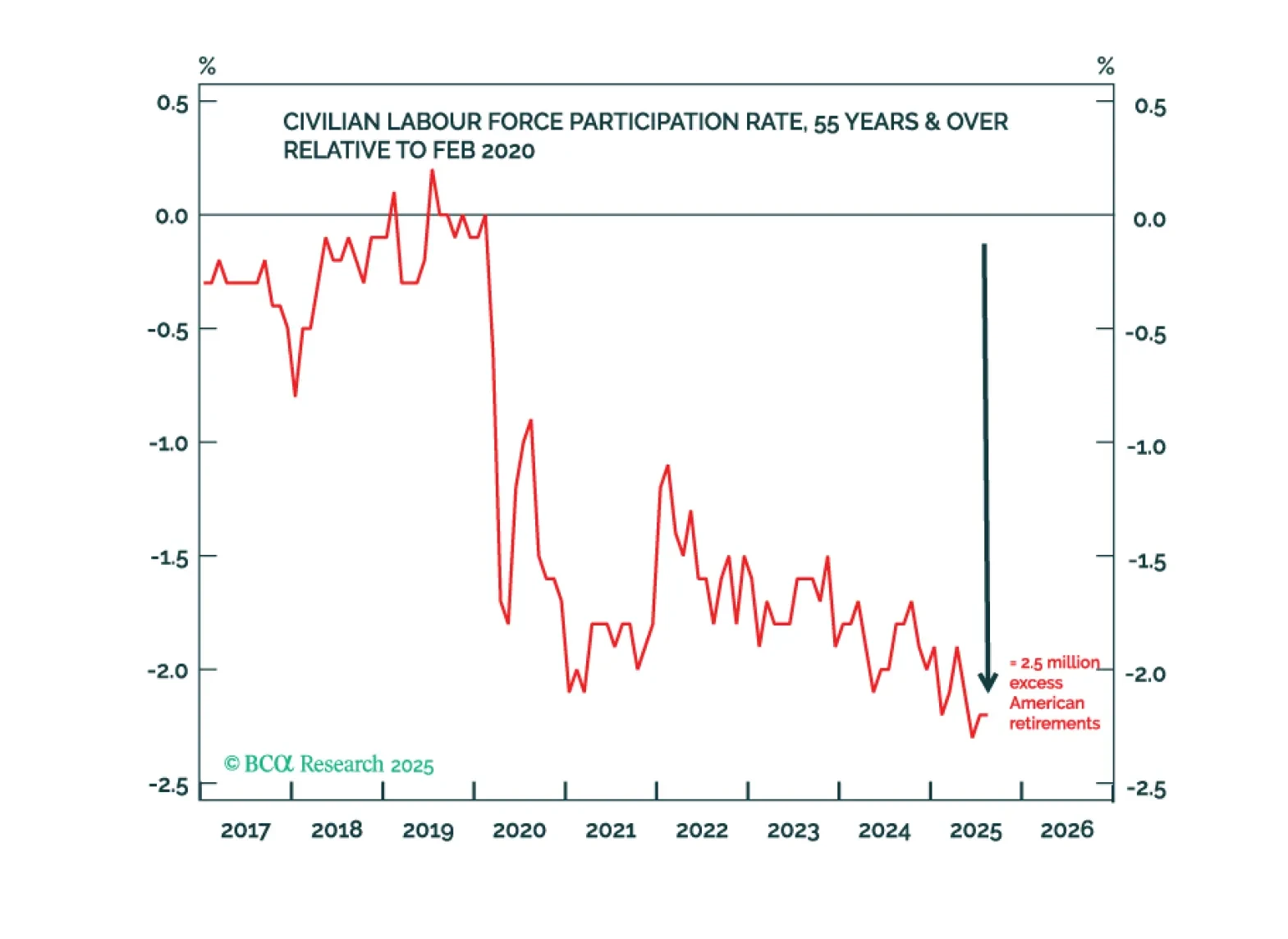

The greater risk to the world economy in 2026-27 is not that a recession triggers a market crash, but that a market crash triggers a recession. This is because a market crash will destroy the wealth that is funding the crucial marginal spending of 2.5 million excess American retirees. Plus, a new tactical trade is: Overweight Switzerland (SMI) versus UK (FTSE 100).

Our Portfolio Allocation Summary for November 2025.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

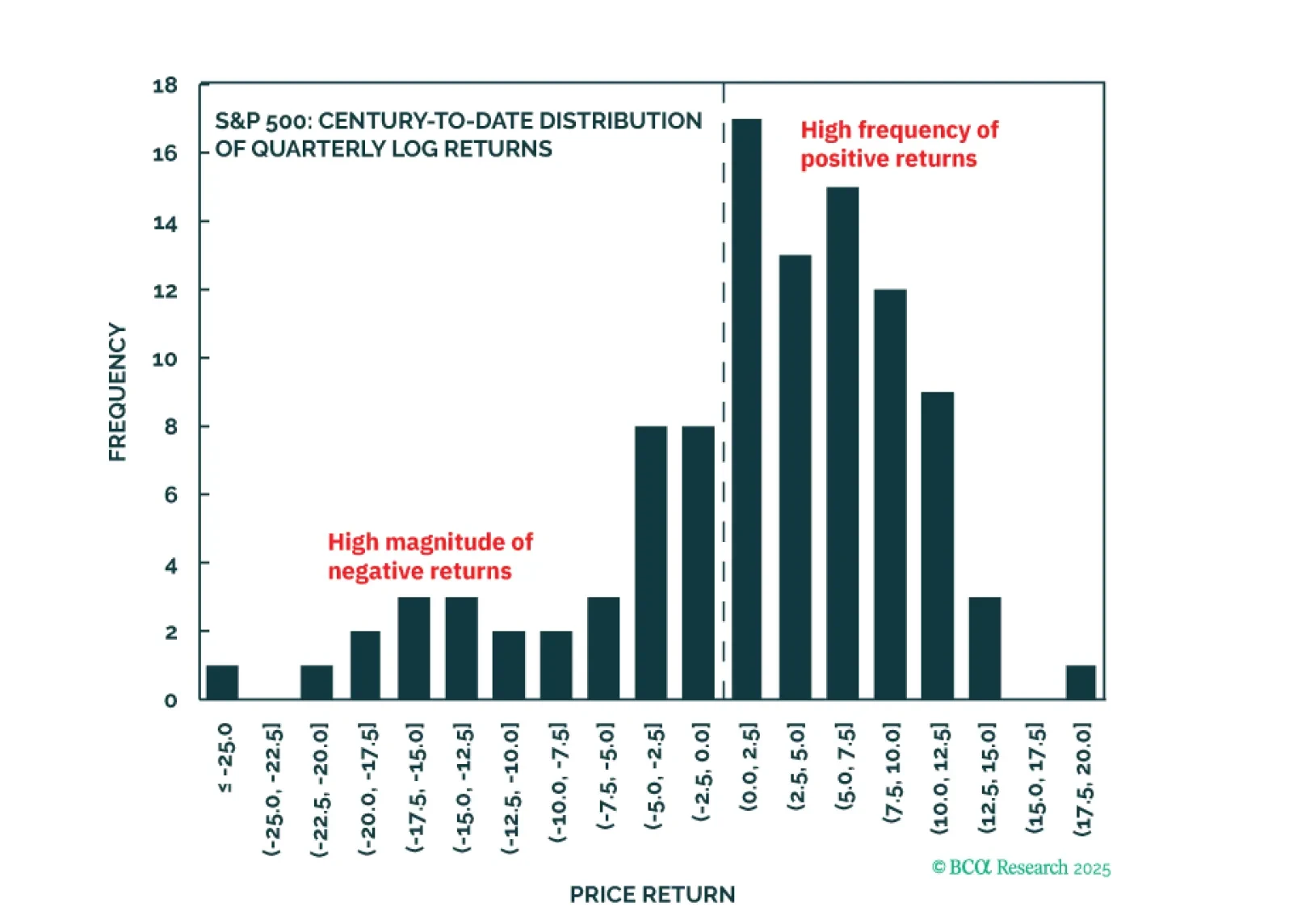

Asset allocators must pay attention not only to the magnitude of an asset’s expected returns but also to its shape, a concept technically known as skew. Adding skew into our analysis moves our equity allocation up to neutral while bonds remain at underweight. Plus: a new tactical trade is to buy sugar.