Fixed Income

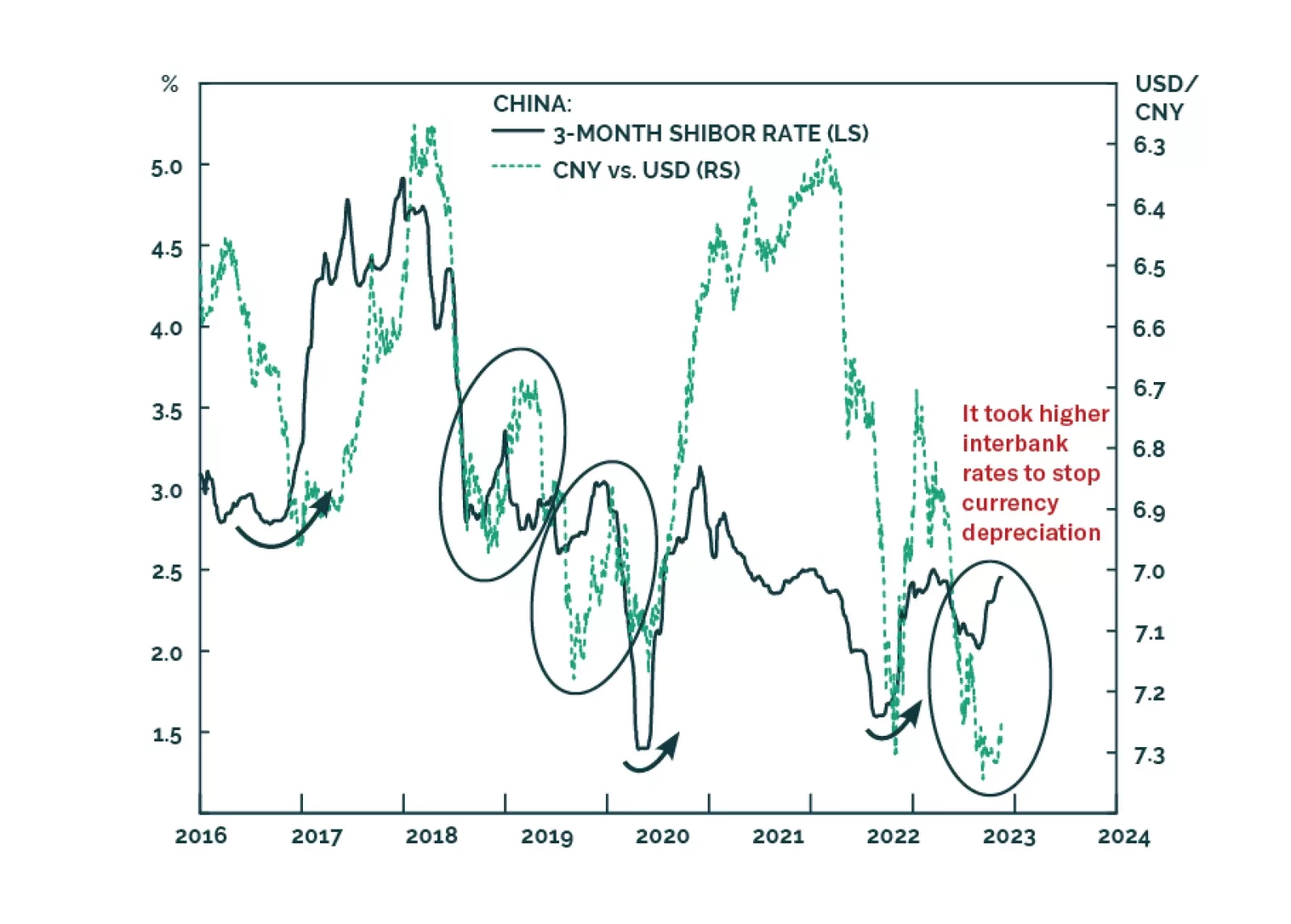

Many commentators have attributed the latest increase in Chinese interest rates to an improving economy, the large issuance of government bonds, the tax payments season, and other technical factors. Yet, these explanations are missing the key point: the PBoC has steered interbank rates higher to defend the currency. Higher borrowing costs are the last thing the mainland economy now needs.

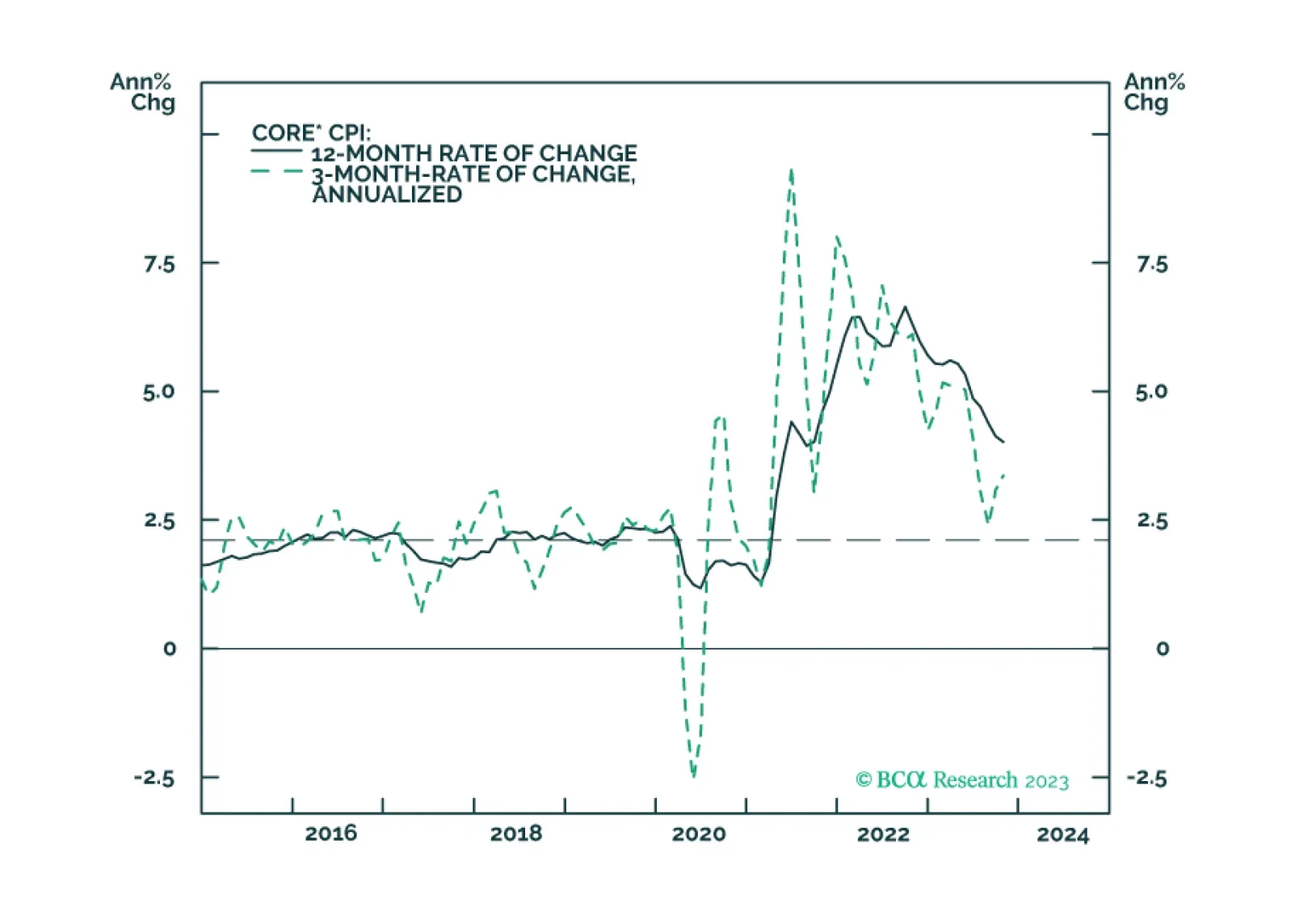

Our thoughts on this morning’s CPI print and the bond market’s reaction.

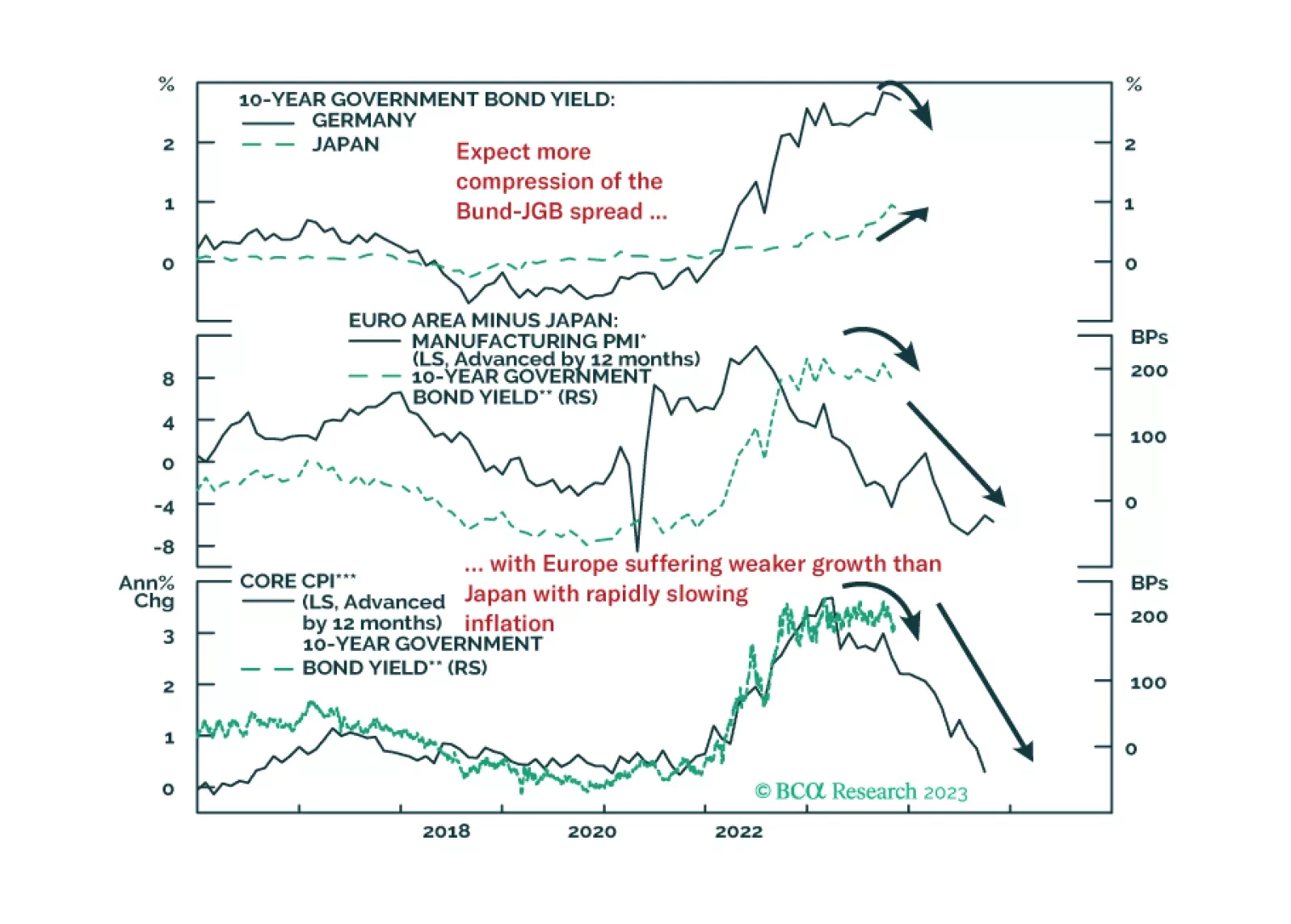

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.