Fixed Income

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The Chinese economy will not recover without significant “irrigation-style” stimulus. The latter is still unlikely for the time being. Dim economic fundamentals justify lower valuations of Chinese equities. Lingering deflationary pressures entail even lower interest rates, which is bearish for the RMB.

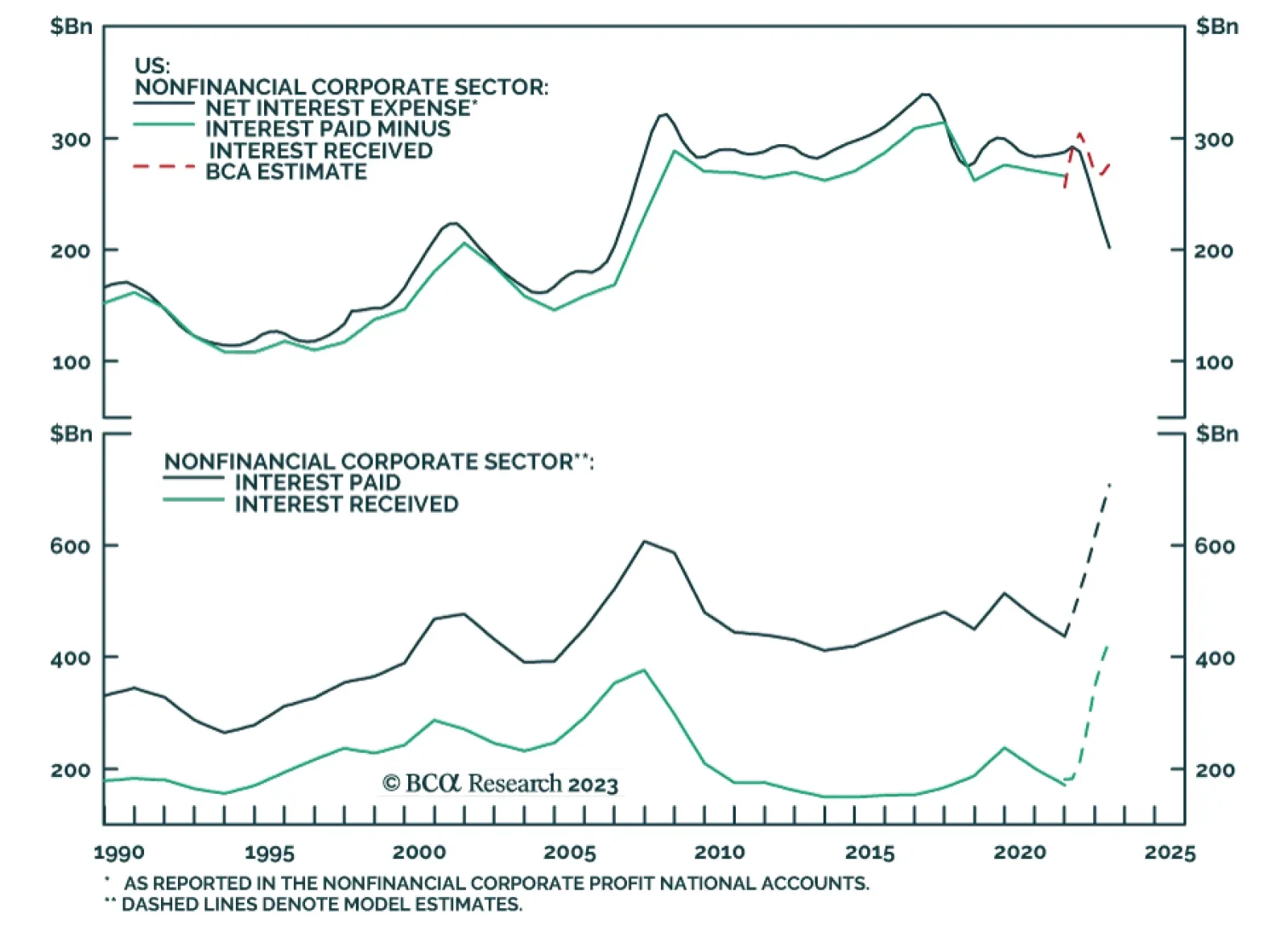

Top-down measures of nonfinancial corporate sector balance sheet health have been flattered in recent quarters by inaccurate data on interest expense. After correcting for the inaccurate data, we see that our best measures of corporate balance sheet health show a persistent steady deterioration.

The ECB is done lifting interest rate for the cycle and its next move will be a cut next year. Yet, European rates will climb even higher in the second half of the decade.

While we are sympathetic to the view that the Fed could temporarily achieve a soft landing, we are skeptical that it could stick that landing for very long. Stocks could strengthen into year-end, with small caps potentially leading the charge. But the rally will fizzle out next year as the global economy begins to sink into recession.

The implications of this morning’s CPI report for Fed policy, Treasuries and TIPS.

In this report, we review our European fixed income strategy recommendations ahead of tomorrow’s critical ECB meeting