Fixed Income

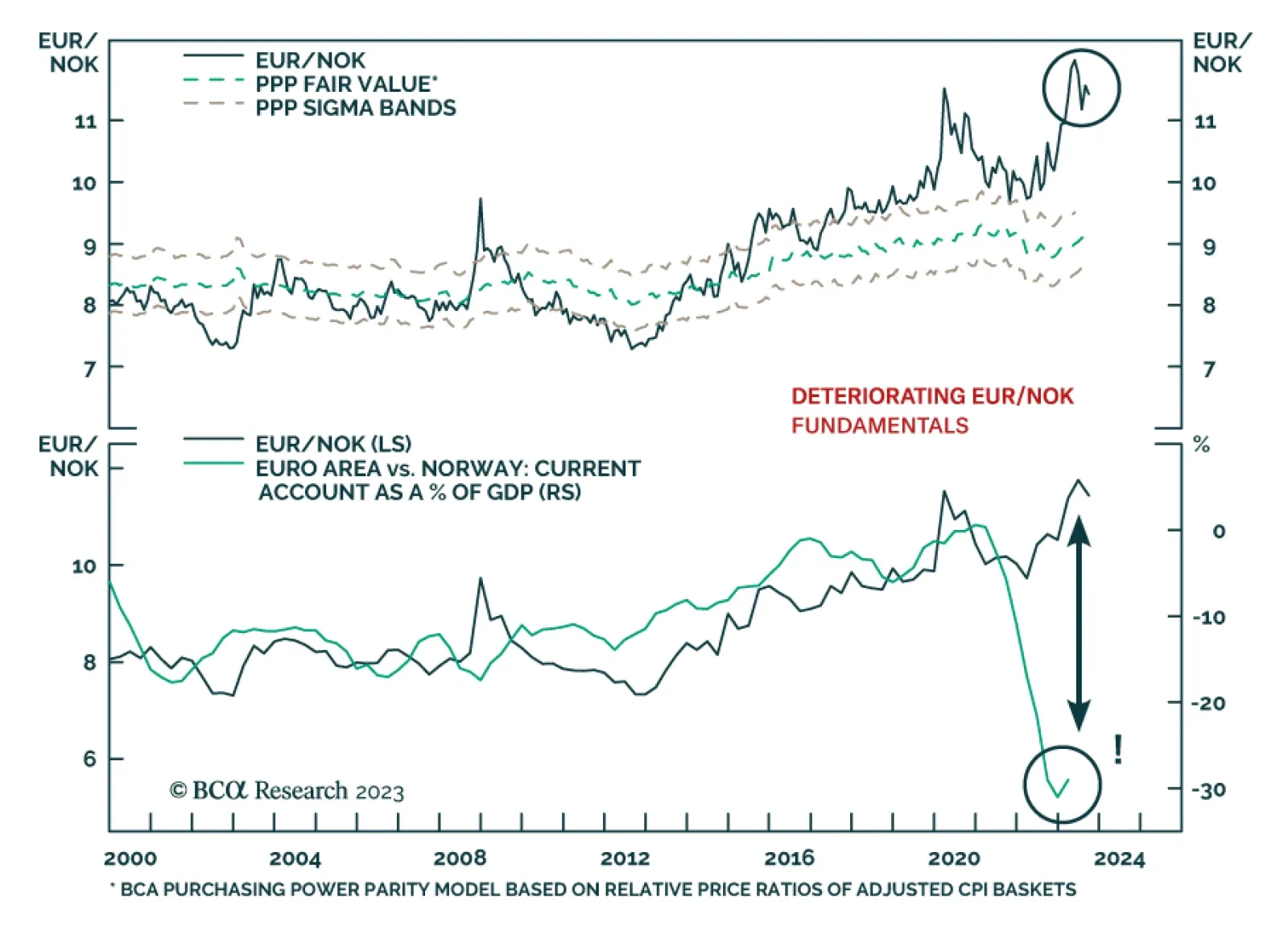

Real wages are set to rise in CE3 economies with implications for their asset markets and currencies. Of the three, Polish assets and the zloty are the most vulnerable.

Our Portfolio Allocation Summary for September 2023.

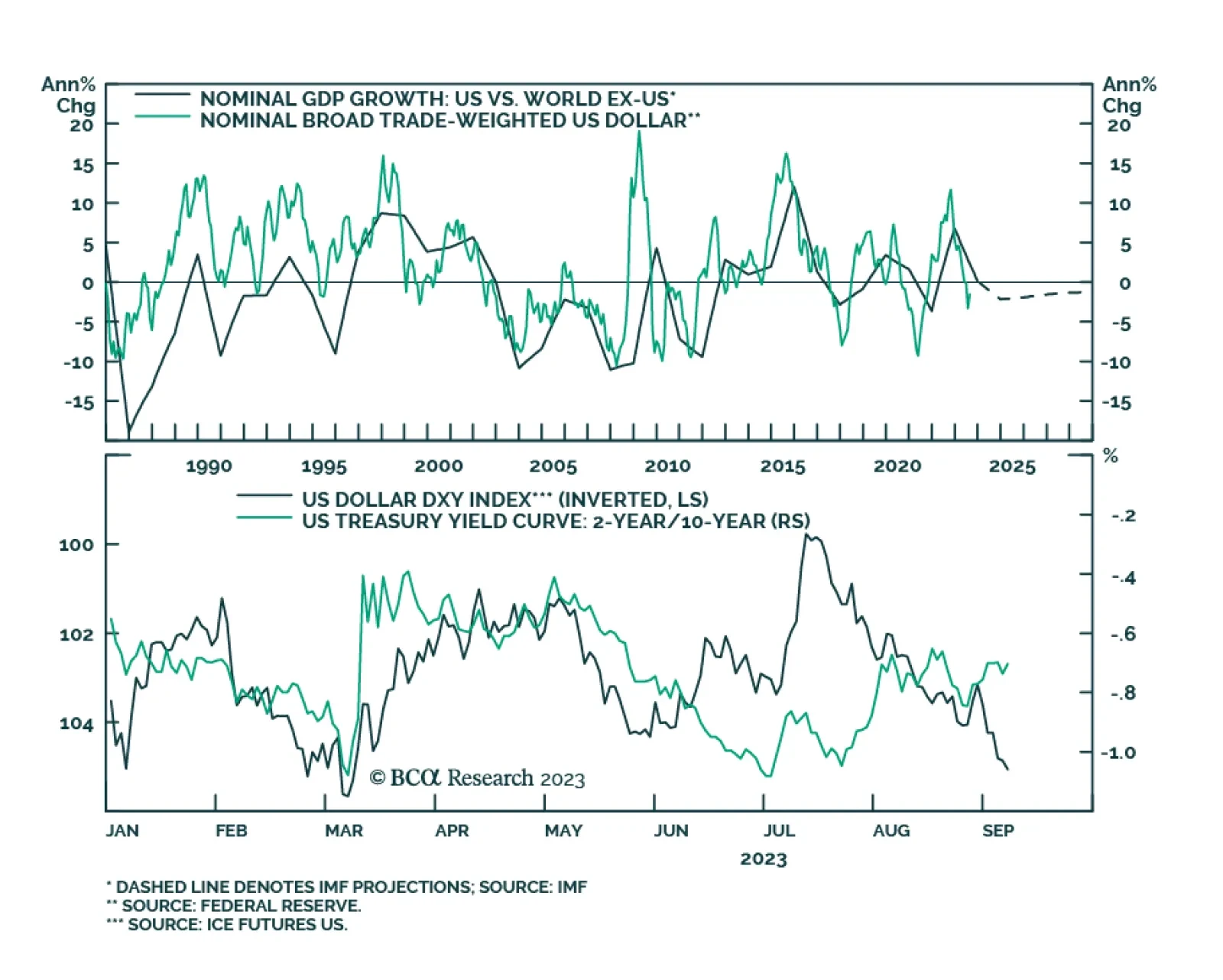

If we look at global growth as an aircraft, the plane is experiencing failing engines and will lose more altitude in the coming months. Yet, neither Chinese authorities, nor the Fed or the ECB will be quick to come to the rescue as global growth downshifts. These dynamics herald a stronger US dollar and lower EM risk asset prices.

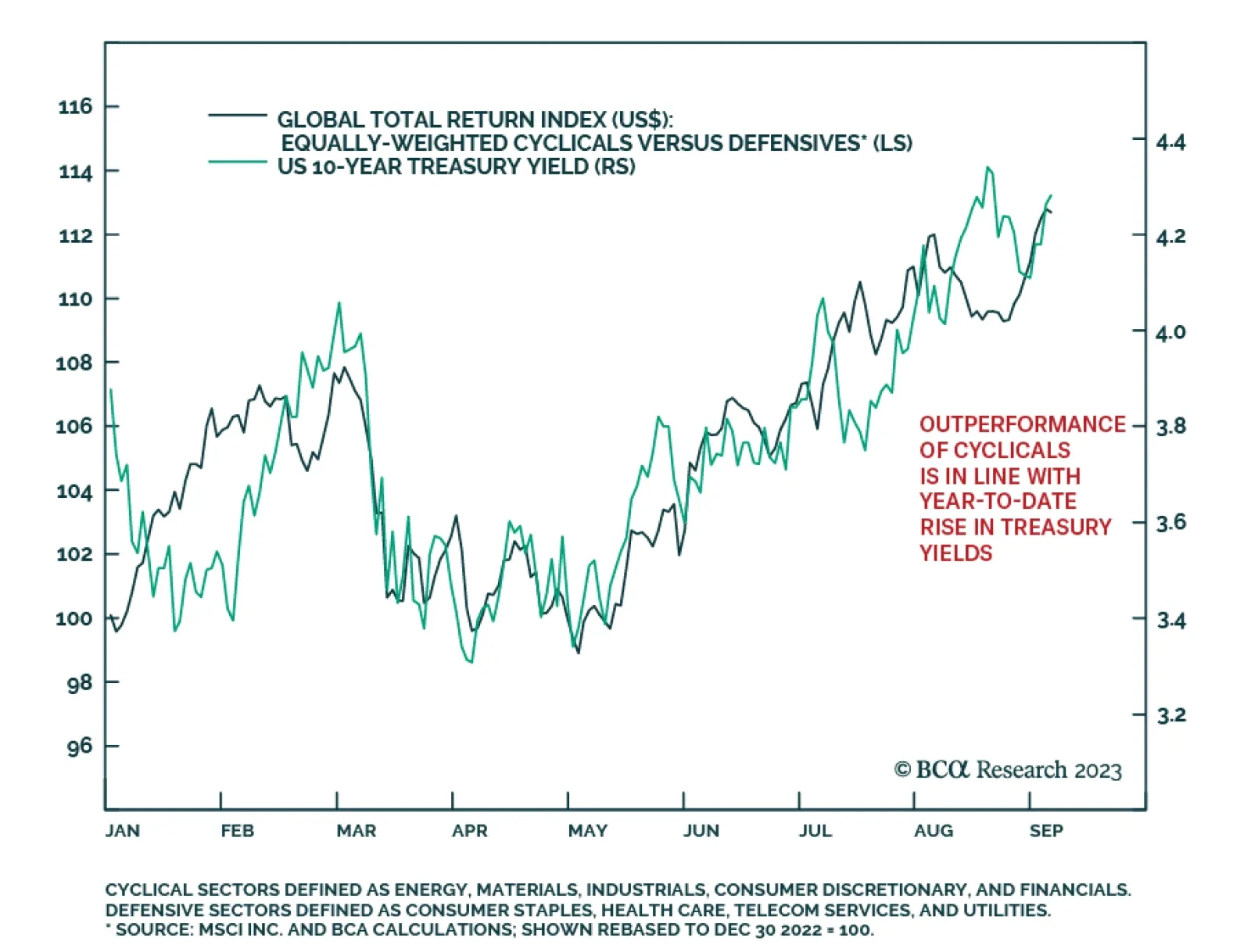

The broader rally that started in June is premised on a Goldilocks narrative that will prove to be a fairy tale. Either by stubborn inflation. Or, by higher unemployment that shows that the war on inflation is far from costless. Or, by both. We discuss the implications for stocks and bonds. And we reveal our new top long dollar cross.