Fixed Income

Deflation prevails in China’s economy. Marginal interest rate cuts will be insufficient to boost growth as the economy is experiencing debt deflation and might be entering a liquidity trap. There will likely be more economic disappointments in the coming months. Chinese stocks will continue to sell off. Government bond yields will fall to new lows, and the RMB will depreciate further against the US dollar.

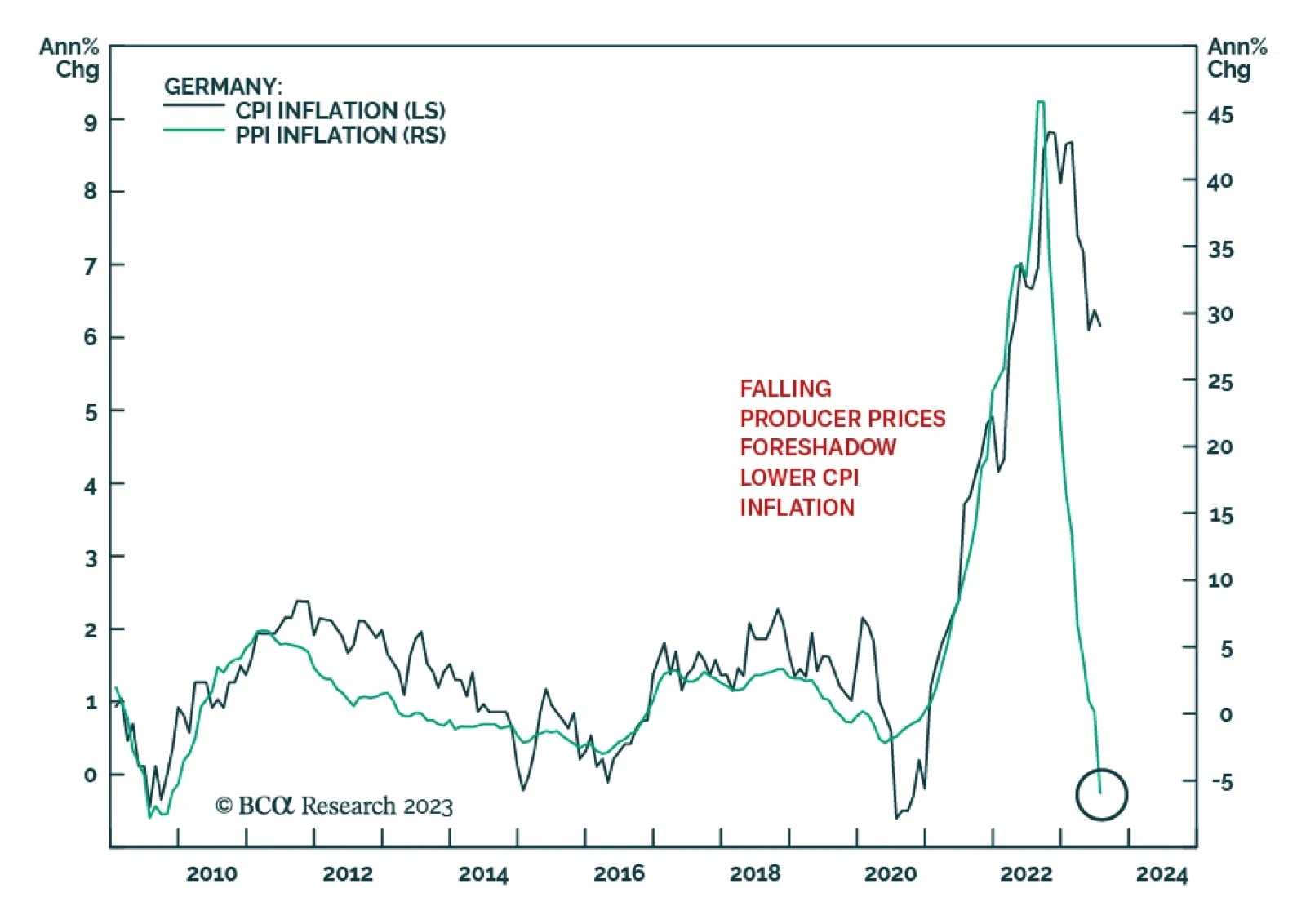

European yields are testing the upper end of their recent trading range. Is the European economic outlook consistent with an imminent breakout?

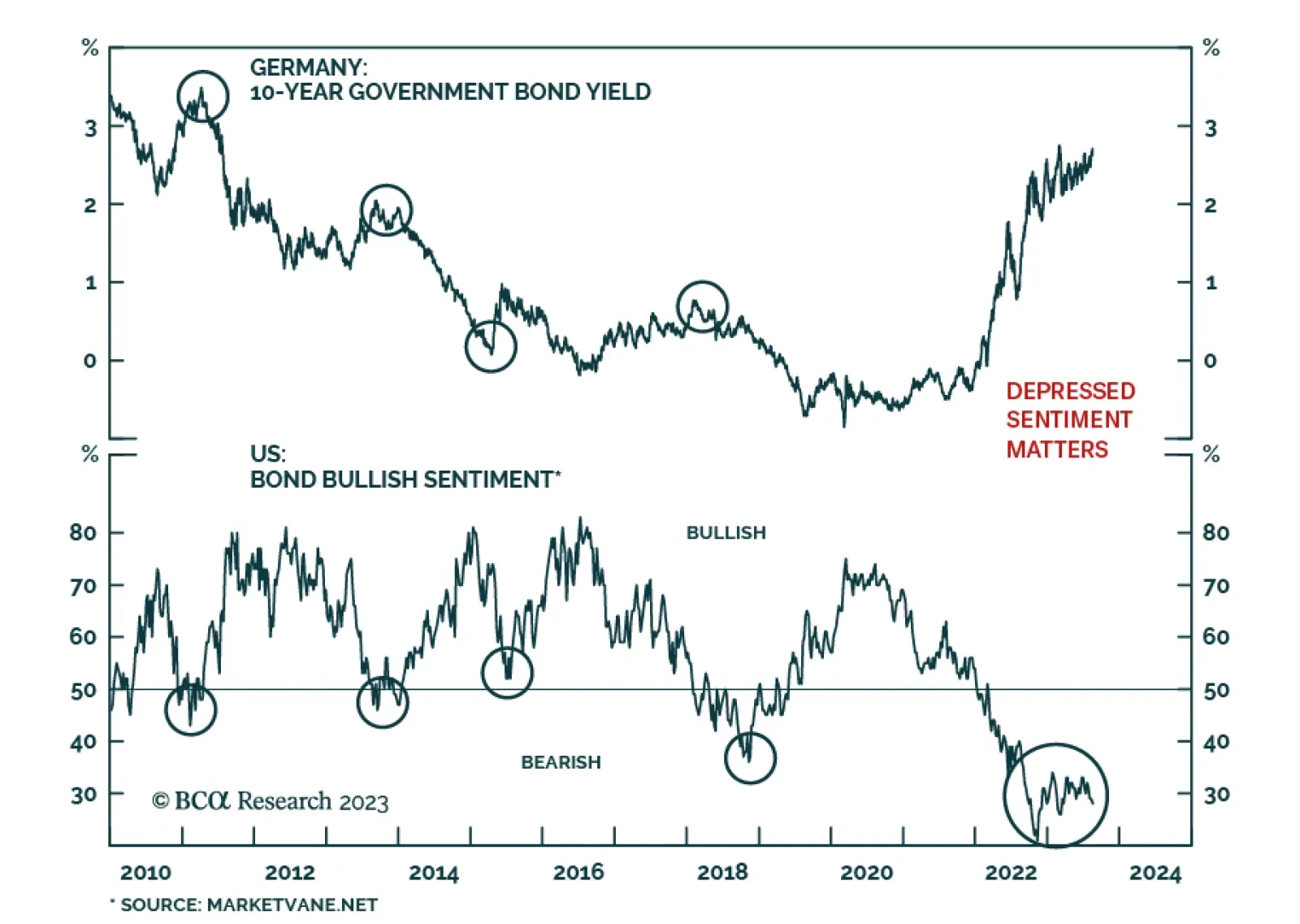

While the bearish bond trade currently has a lot of momentum, we continue to think that Treasury yields are close to a cyclical peak and will be lower on a 6-12 month horizon.

In this special report, we discuss whether the economic conditions necessary for a stronger yen (and higher JGB yields) will materialize over the next 12-to-18 months.

Commentators often use notions like debt deflation, balance sheet recession, and liquidity trap interchangeably. Yet, these are different concepts. This report develops a framework and provides a diagnosis of China’s economic malaise. A follow-up report will deal with what kind of treatment is needed for a recovery. As a trade, we recommend shorting the EM equity index.

In this special report, we discuss whether the economic conditions necessary for a stronger yen (and higher JGB yields) will materialize over the next 12-to-18 months.