Geopolitics

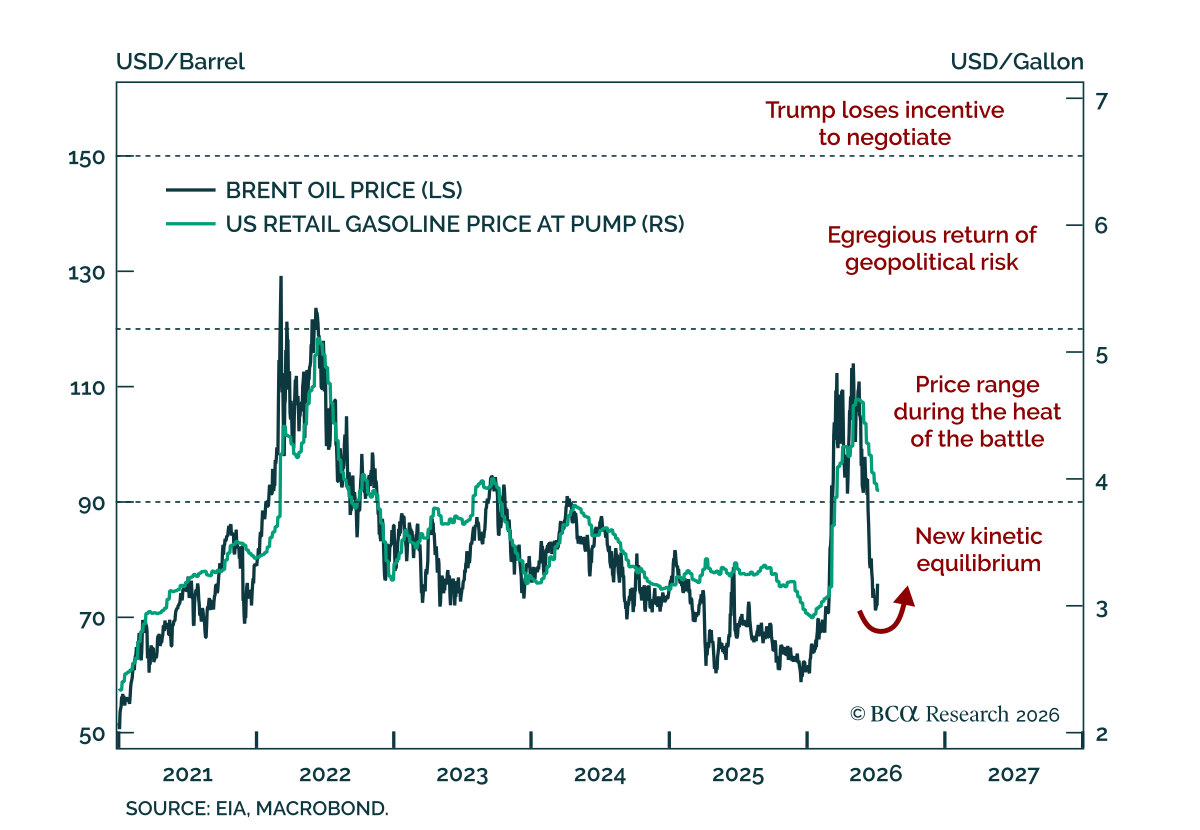

We stick to the view that geopolitical risk has peaked. The US and Iran tensions will increase oil prices, but below a level that will matter for the market. With global liquidity ample, private sector leverage low, and inflation peaking, bears are holding onto an epic collapse of the AI capex to short stocks. Eventually, the capex cycle will end in tears. That much history teaches us. But not yet.

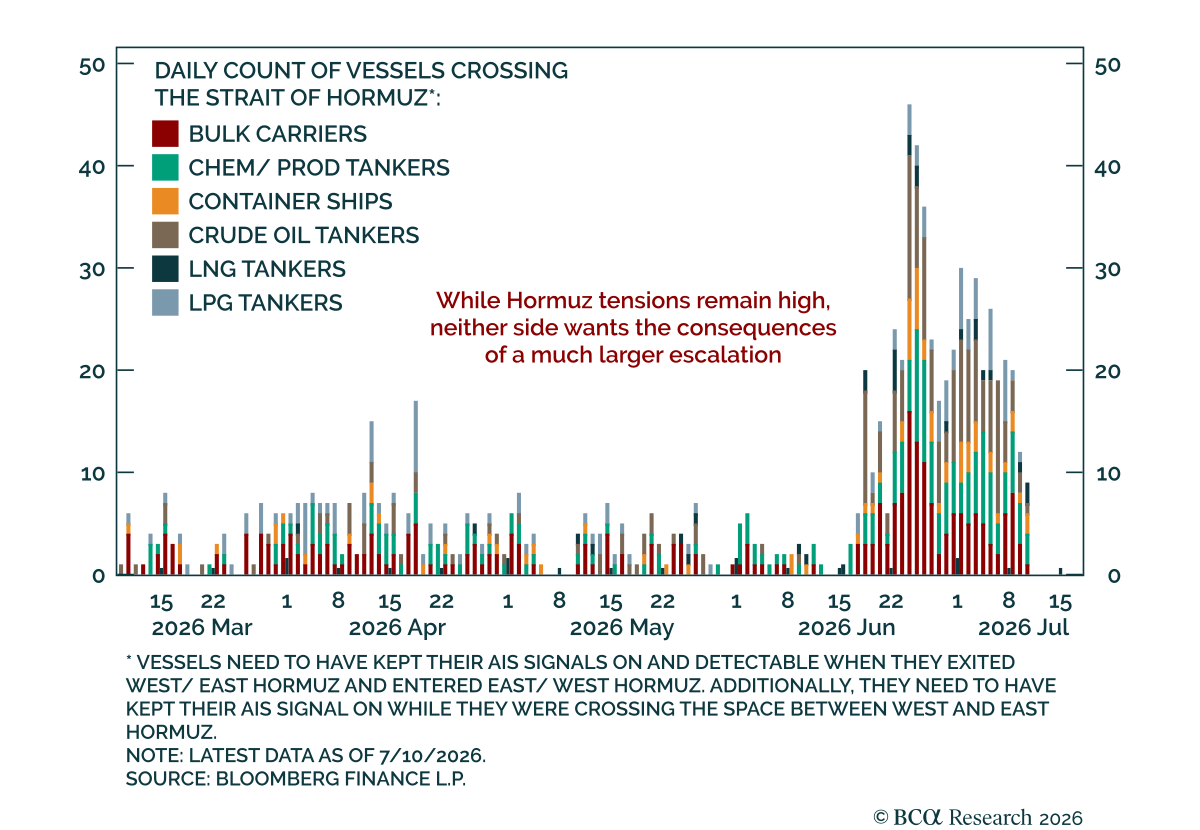

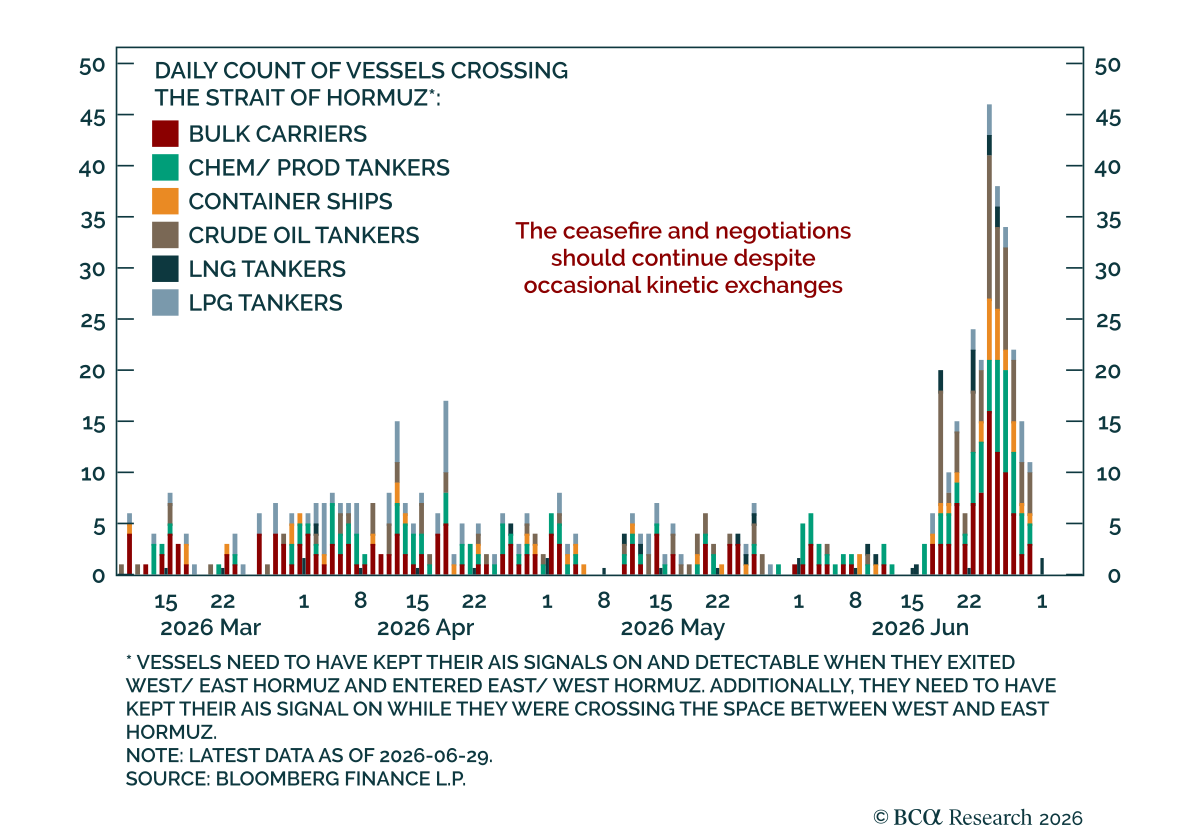

The US and Iran have engaged in a dramatic increase in kinetic activity over the past several days. It all appears to have started on July 6-7, when Iran allegedly attacked several ships in the Strait of Hormuz, vessels that were using the US-recommended route closer to Oman. Following US strikes against Iran in retaliation for that incident – with the US military claiming to have struck 140 sites – Iran has retaliated against US military facilities across the Gulf region. According to media reporting and Iranian government sources themselves, Iran attacked Bahrain, Kuwait, Jordan, Qatar and Oman on July 11-12.

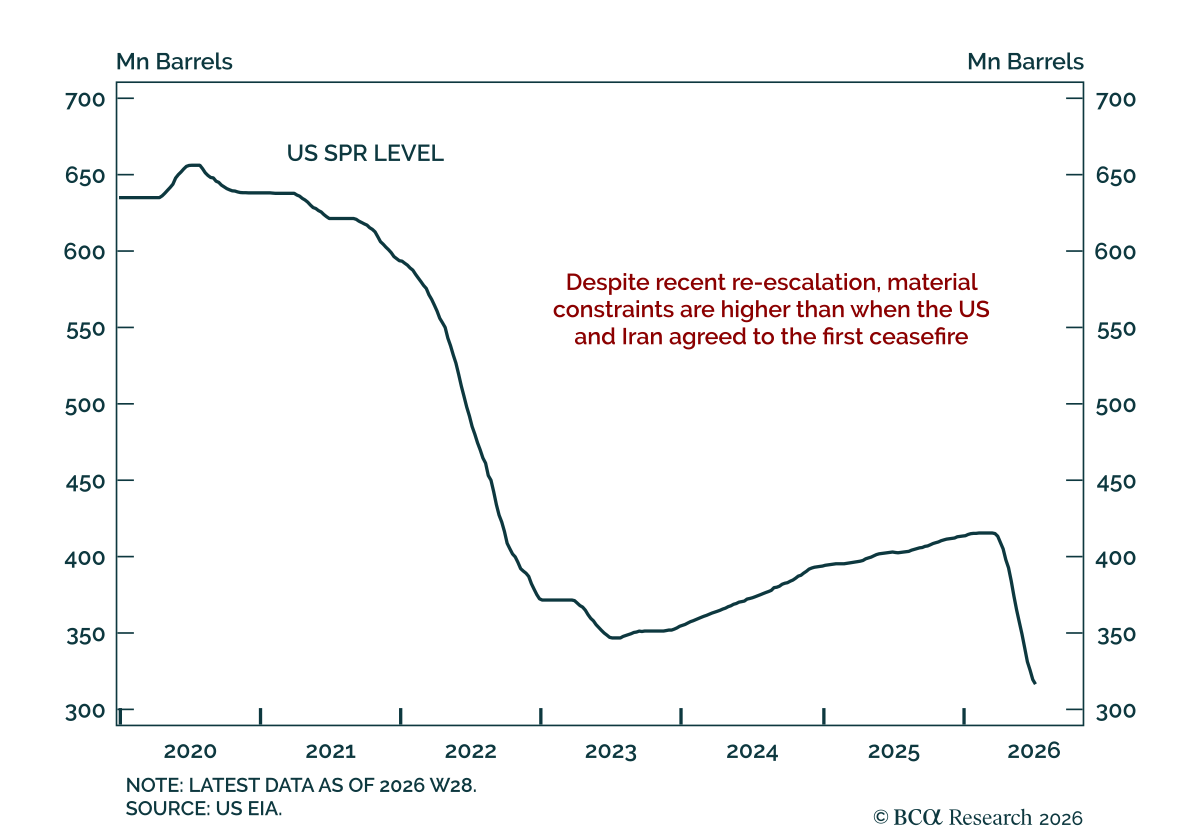

Just as we declared that geopolitical risk has peaked for the year – in yesterday’s Alpha report – President Trump has declared the ceasefire with Iran over after repeated violations via strikes against three tankers in the Strait of Hormuz. That is the life of an investment strategist. But the underlying dynamics continue to play out as we’ve described.

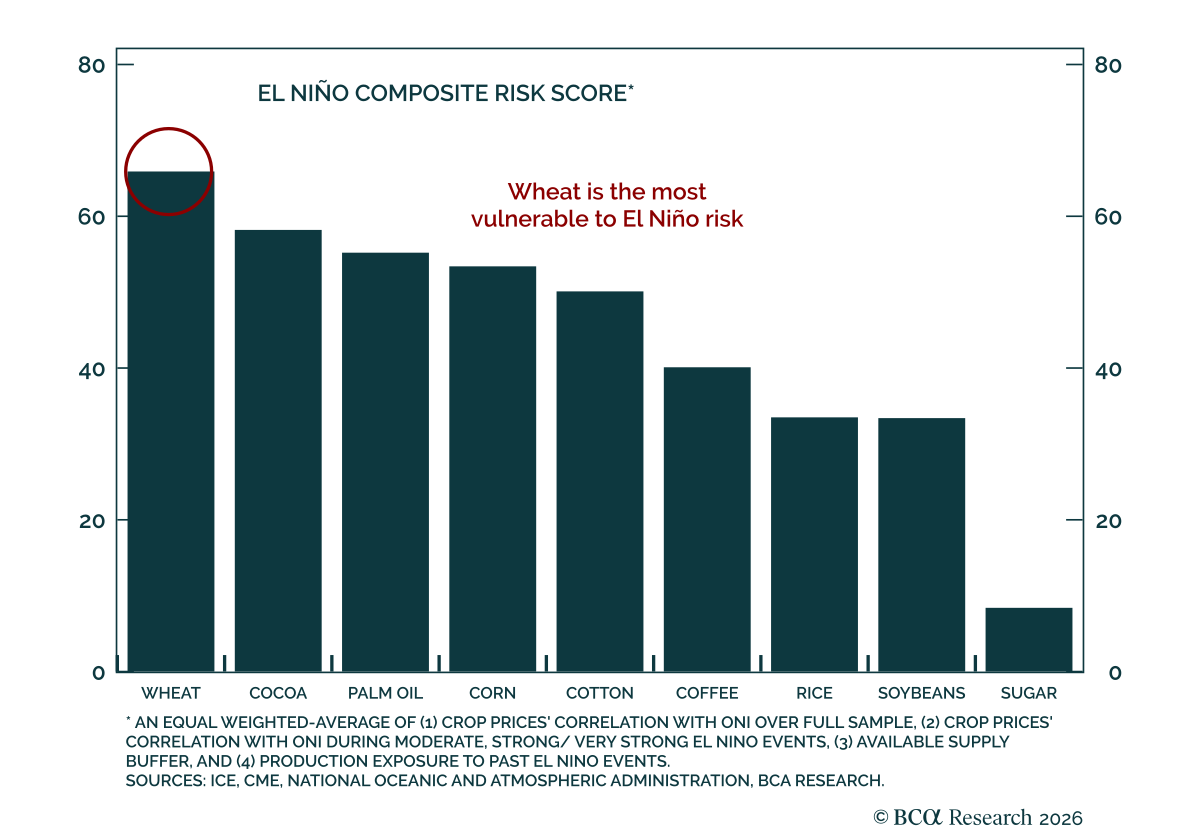

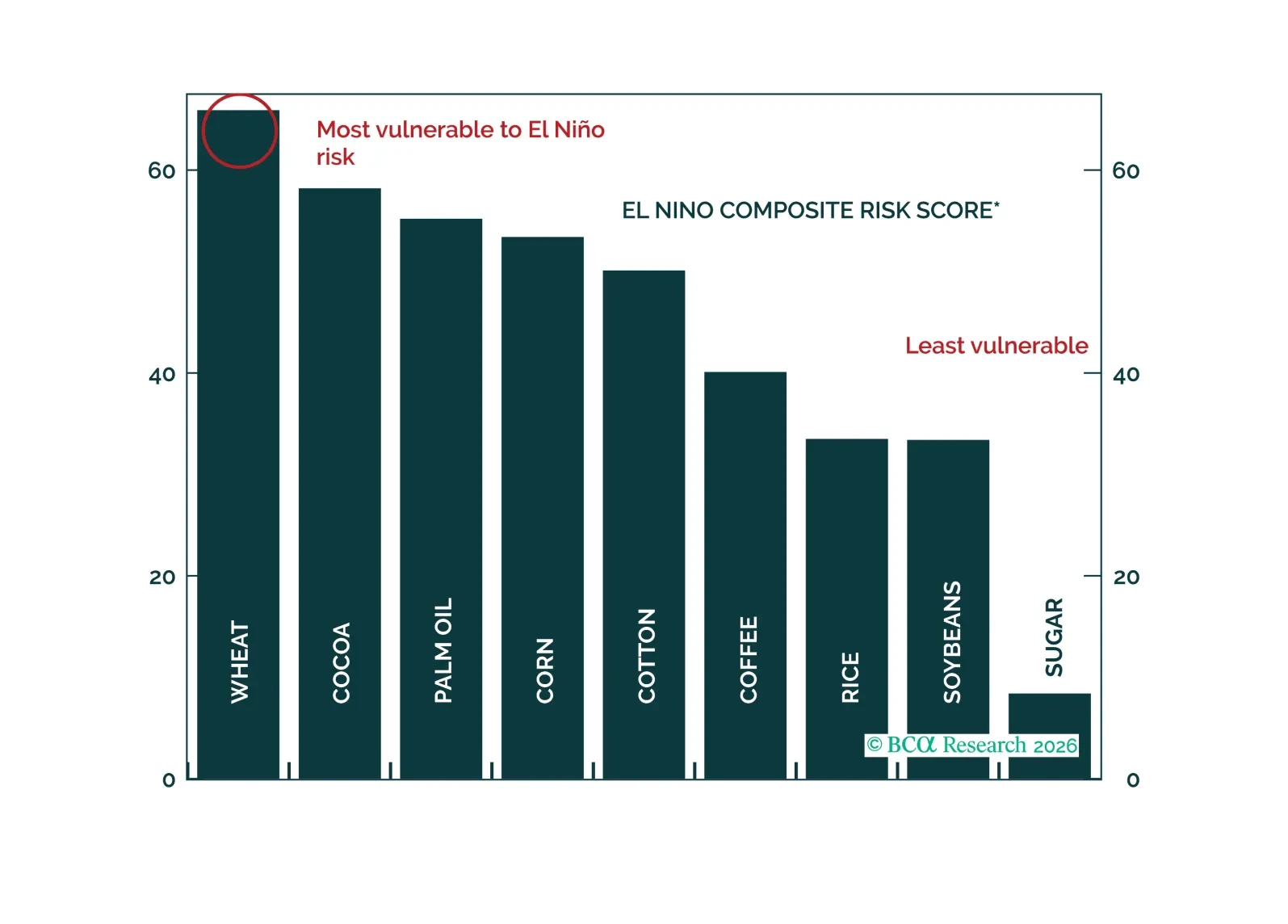

The risk of a “super El Niño” represents a meaningful threat to agricultural markets. Wheat, cocoa, and palm oil appear particularly vulnerable to El Niño-related supply disruptions.

A rise in food prices could also generate political — and potentially geopolitical — reverberations across frontier and emerging markets, where food prices are far more relevant than in developed economies.