Geopolitics

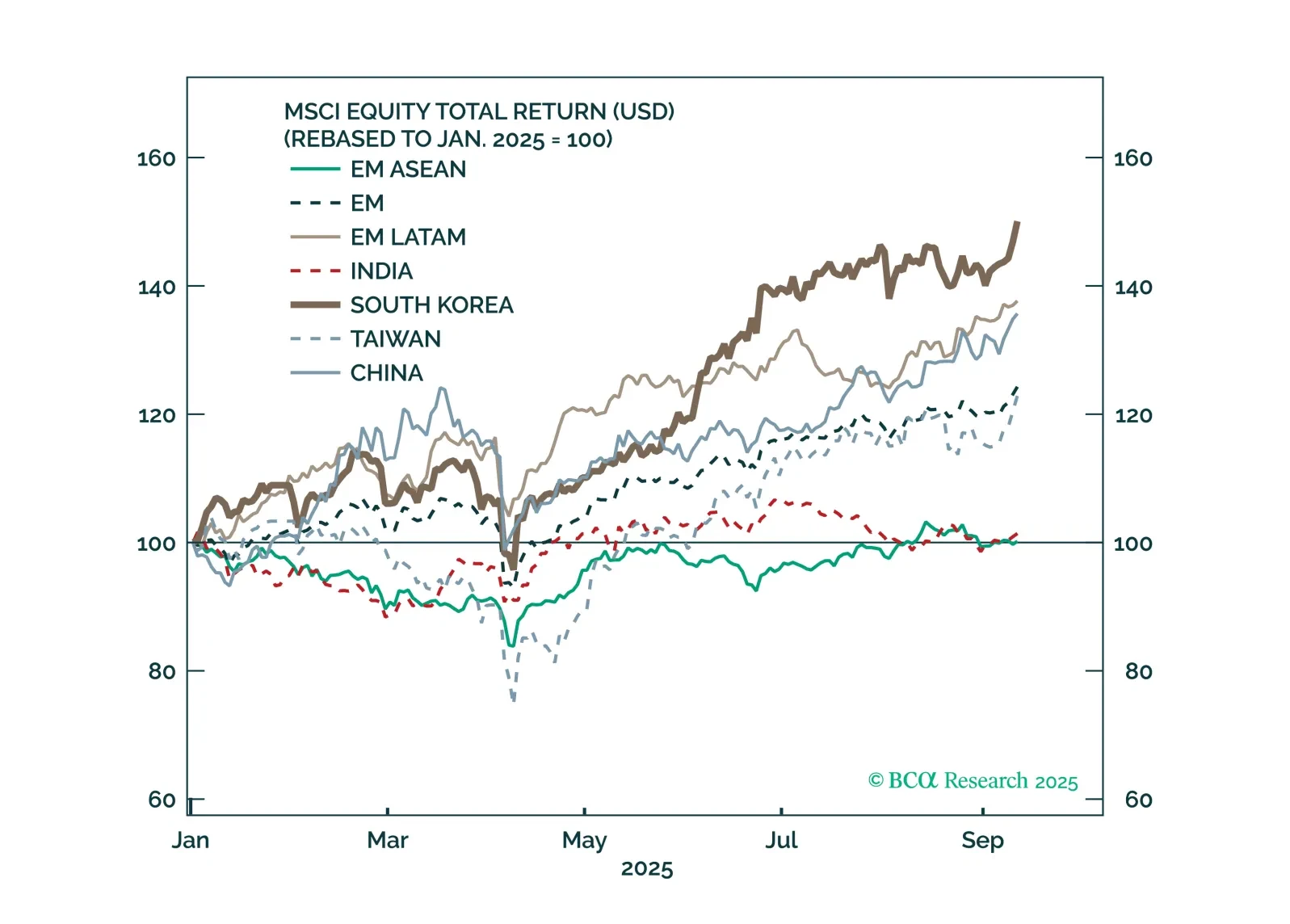

Political instability across Asia is colliding with the trade war fallout, forcing Southeast Asian economies to ease monetary and fiscal policy, while pushing the Bank of Japan in the opposite direction.

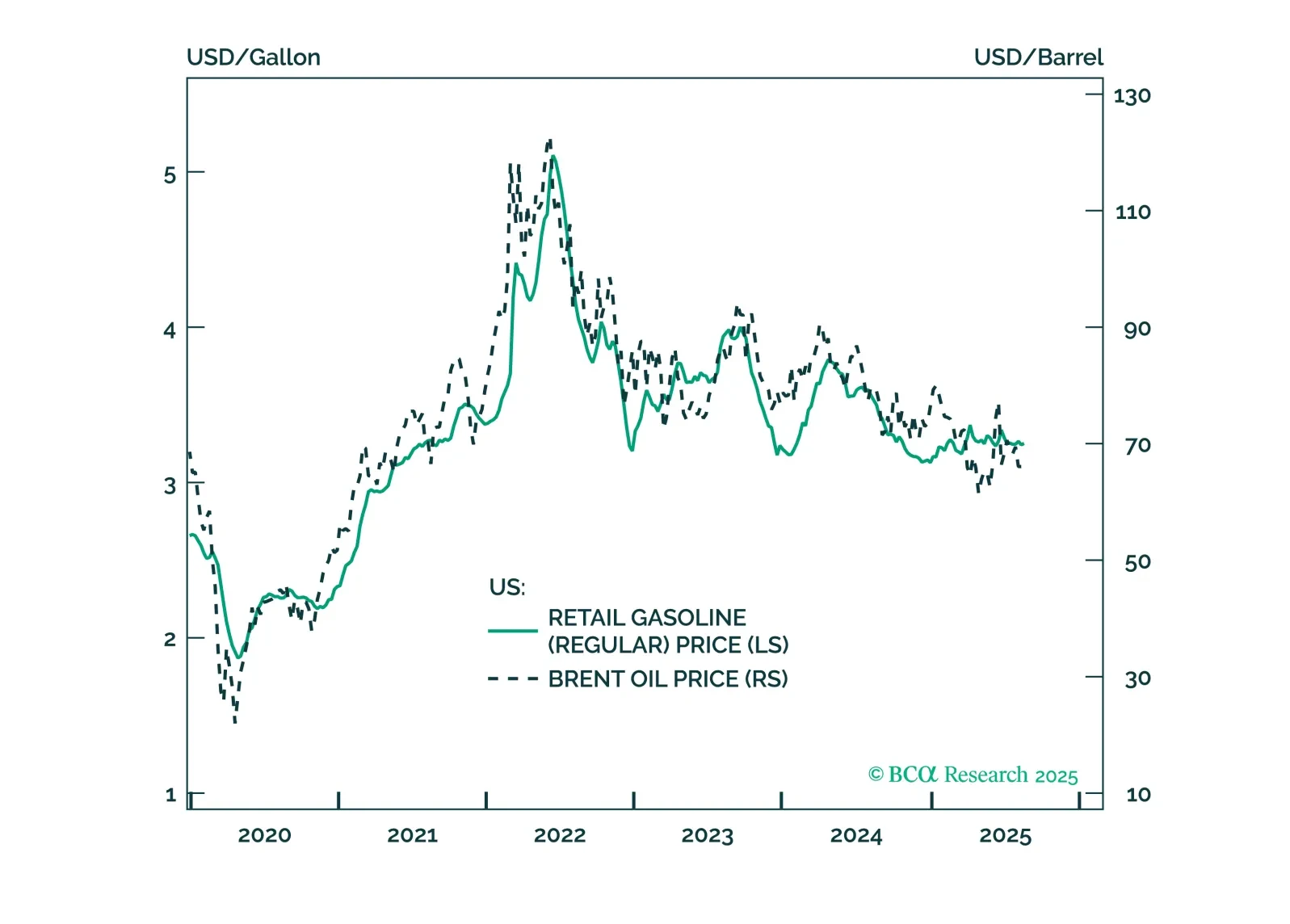

The media is missing the big picture: the war is already contained. The falling oil price confirms that. We fully expect cold feet and volatility incidents in the very near term but there is only a 5% chance of Russia triggering a larger war with NATO – and that is what really matters.

In our Beta report, we introduce a new framework for thinking about long-term investing in a multipolar world: The Garrison State. Investors need to shed their outdated view that geopolitical risks are... a risk. History teaches us that pressure makes diamonds. And geopolitical pressure makes Garrison States, which tend to outperform precisely because by definition, the bevy of risks that surrounds them is existential.