Germany

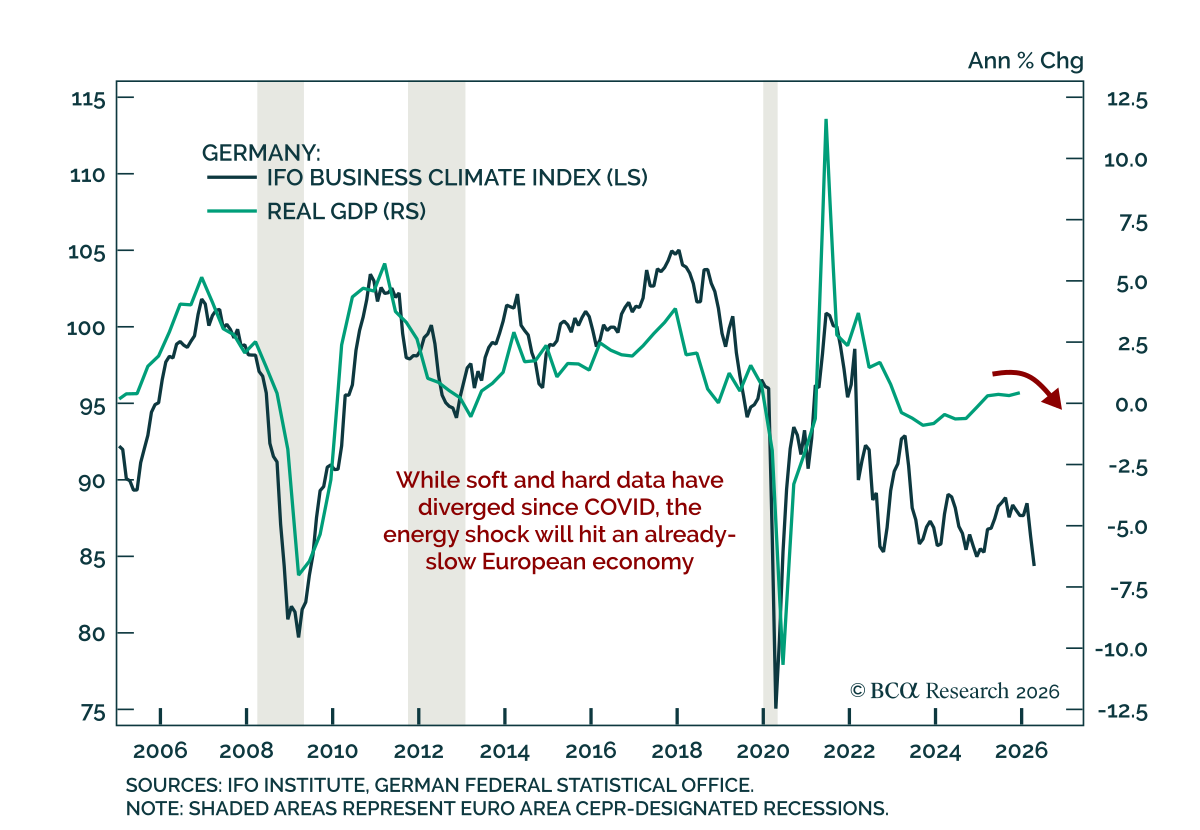

German data continue to deteriorate, reinforcing Europe’s vulnerability to a prolonged energy shock. The May GfK German Consumer Climate indicator fell to -33.3 from -28.1, a level not seen since the 2022 energy shock and near all-time lows for the series.…

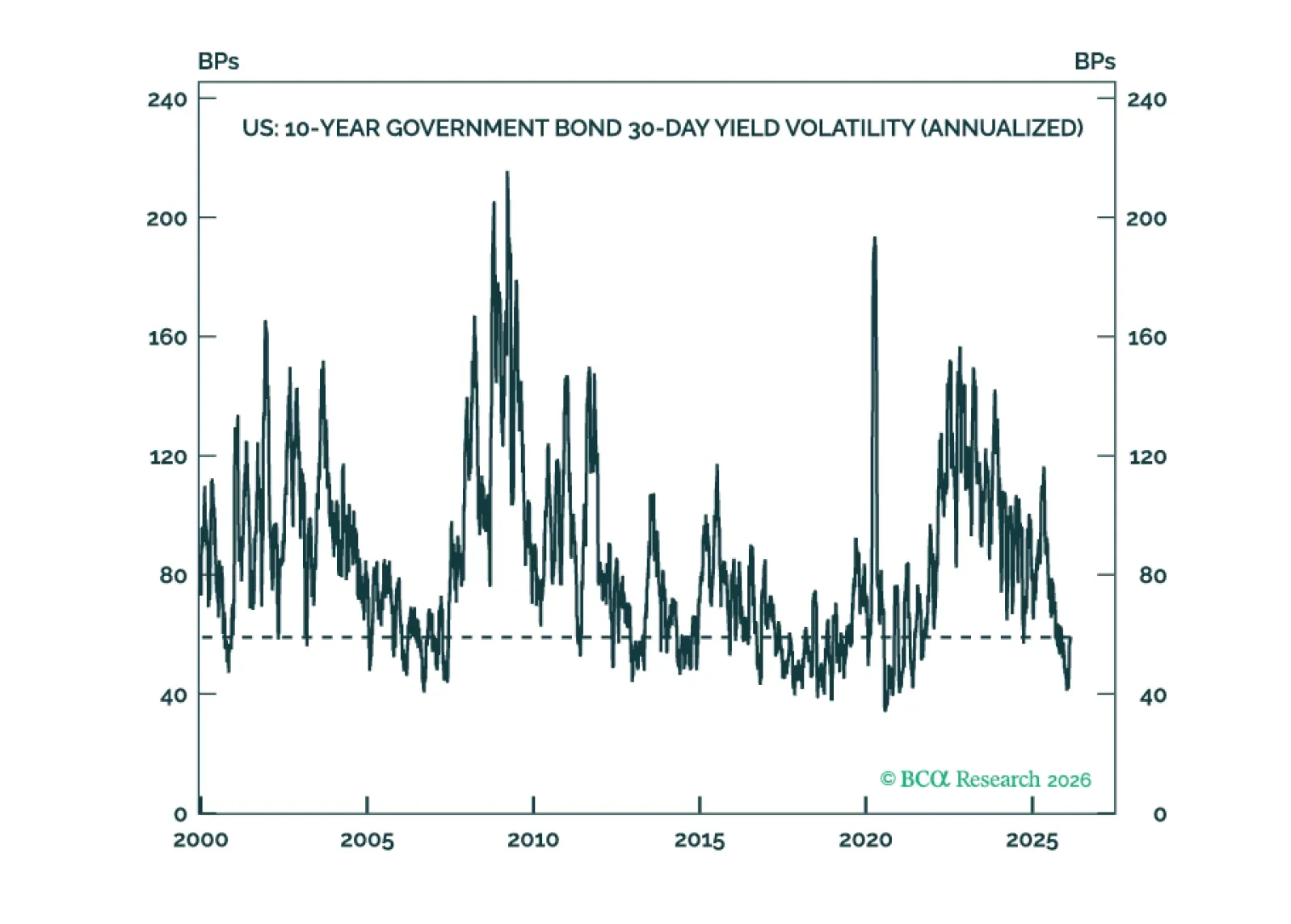

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

The February Germany Ifo survey improved, but broader European momentum remains weak. The Ifo headline and expectations components rose for the first time since October, and firms’ assessment of current conditions also improved, continuing the trend seen…

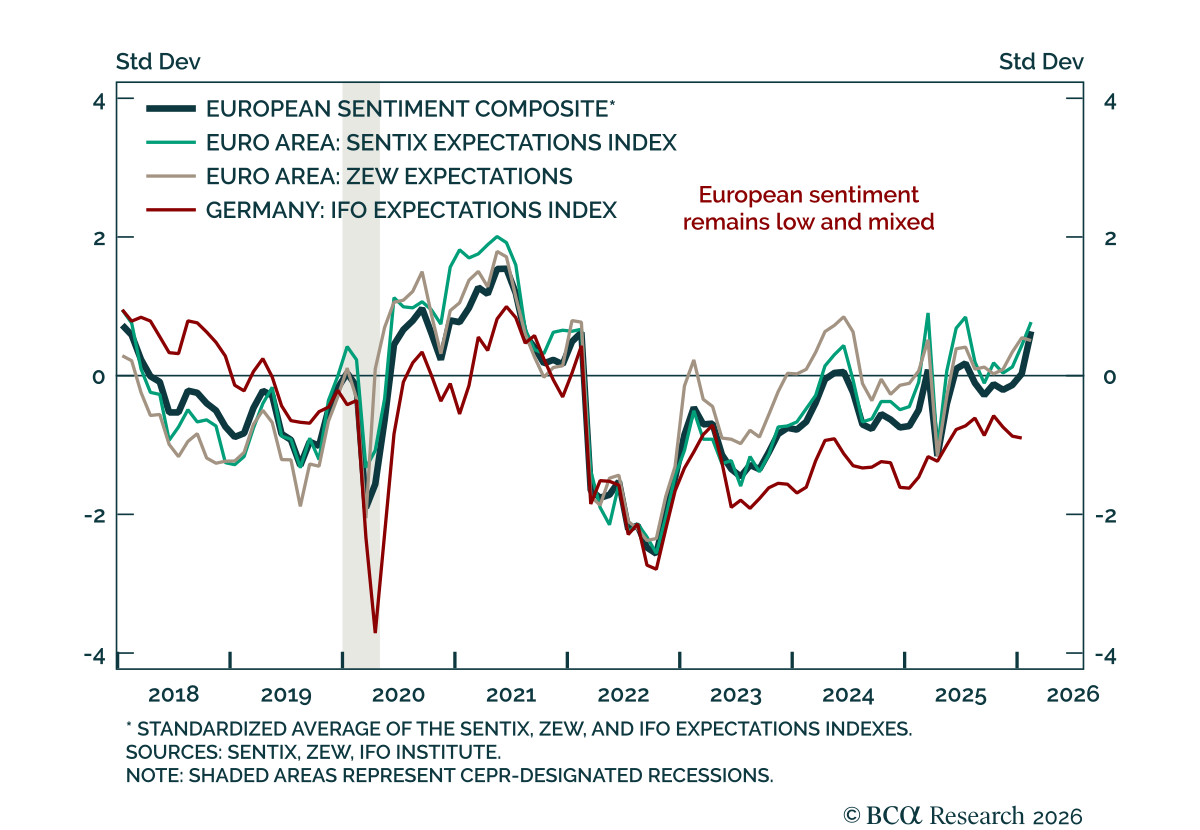

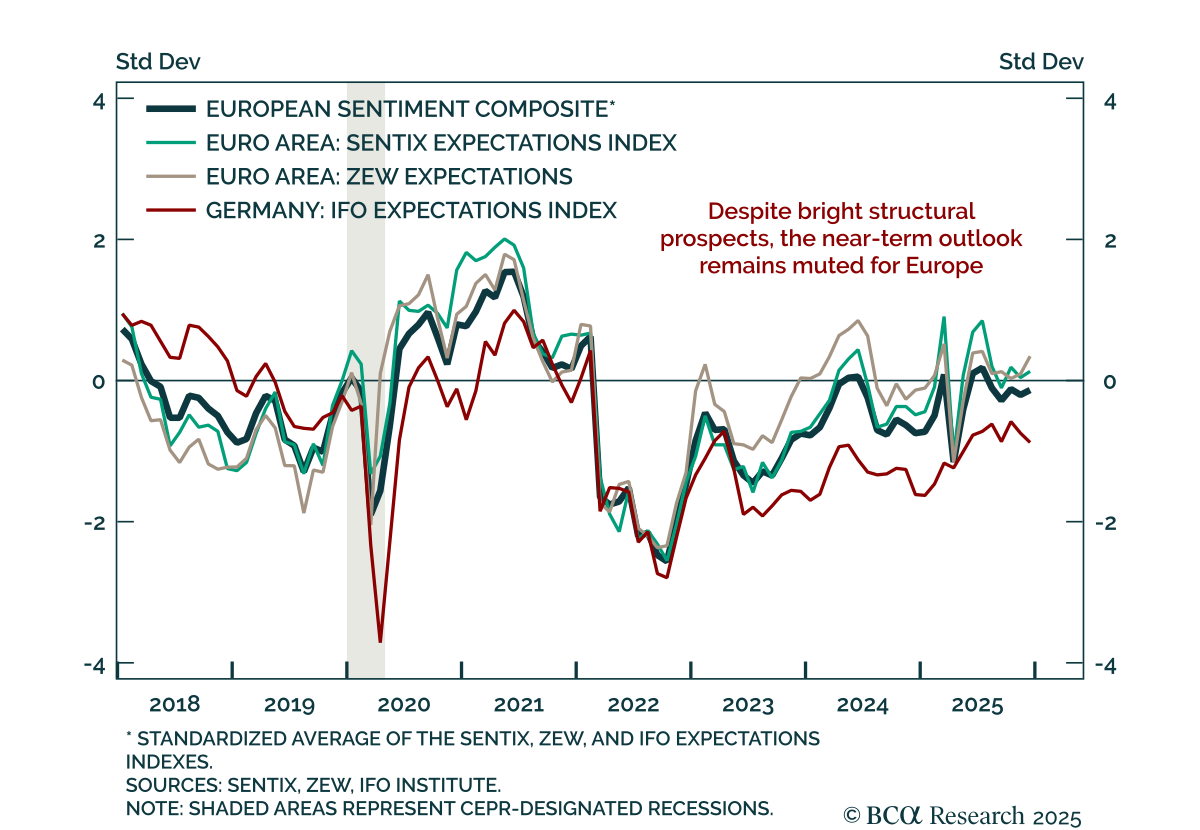

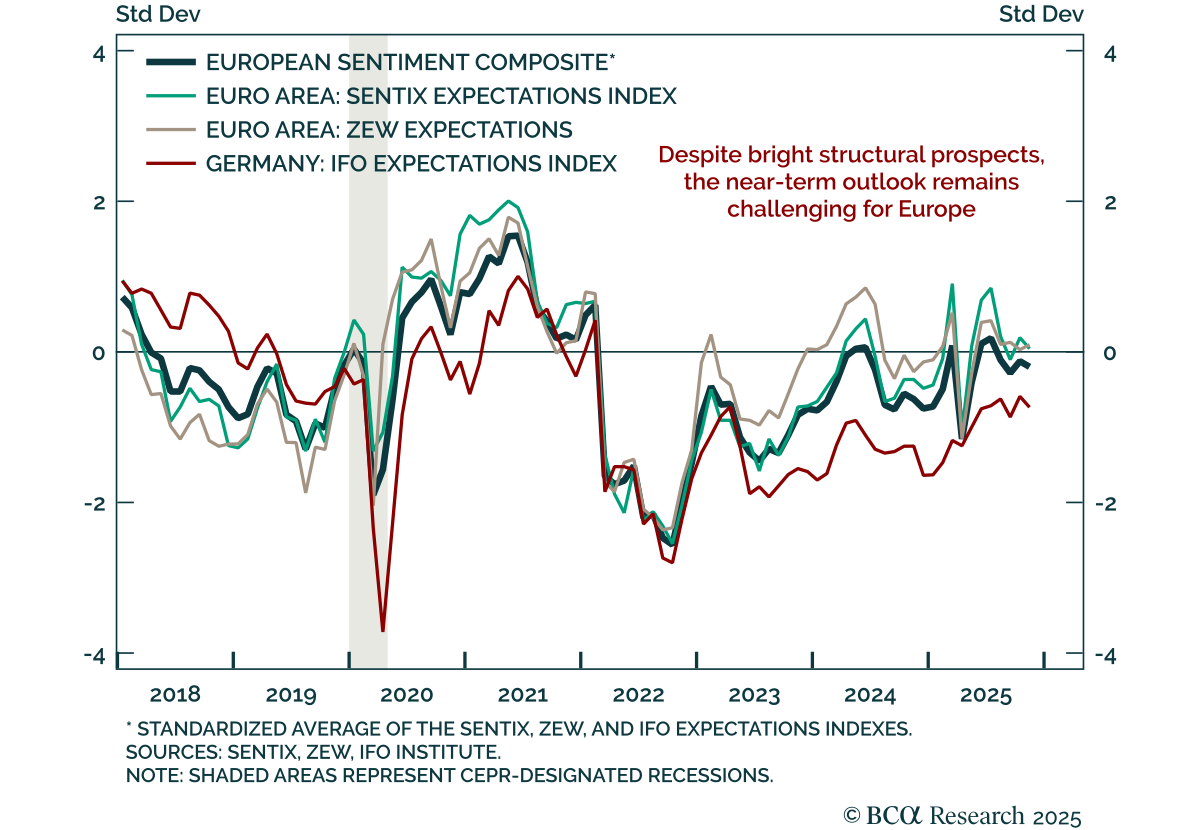

European sentiment has yet to reach escape velocity, with growth momentum still limited. The February ZEW showed expectations declining to 39.4 from 40.8 at the Euro Area level. In Germany, expectations fell to 58.3 from 59.6, missing expectations, while…

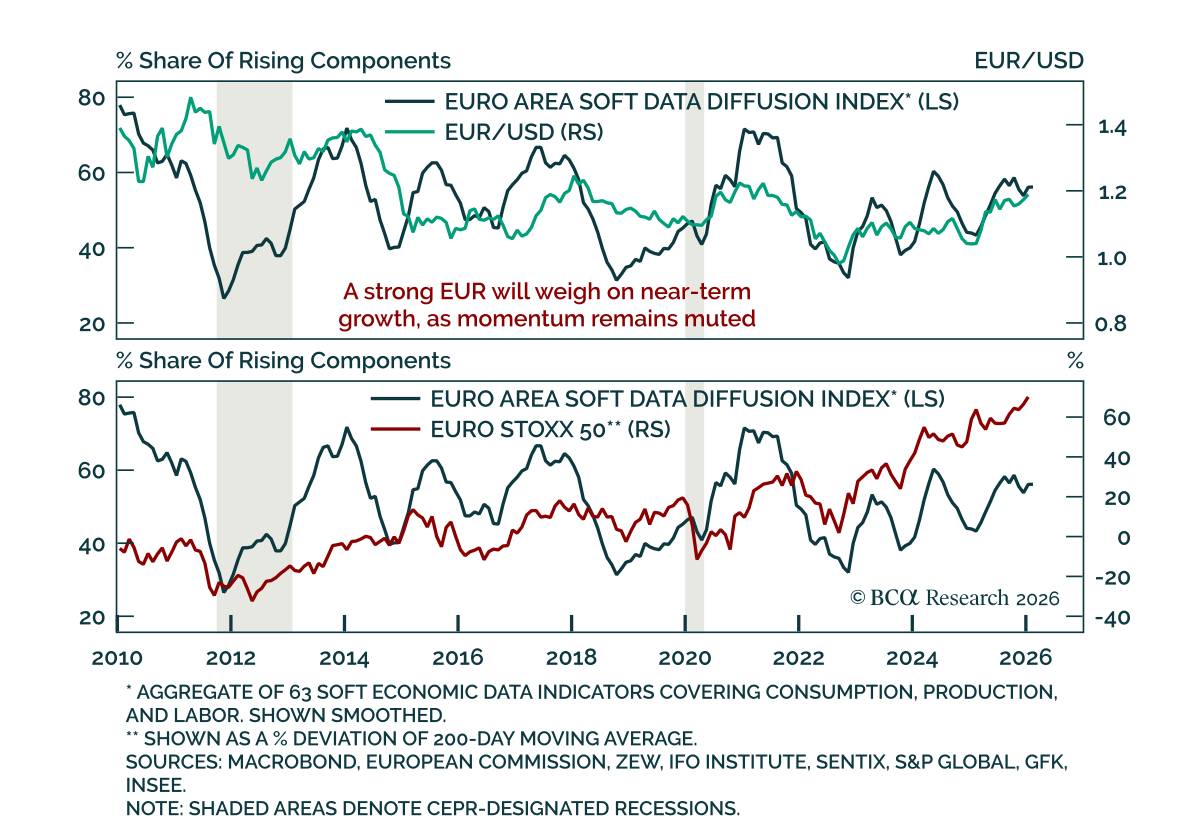

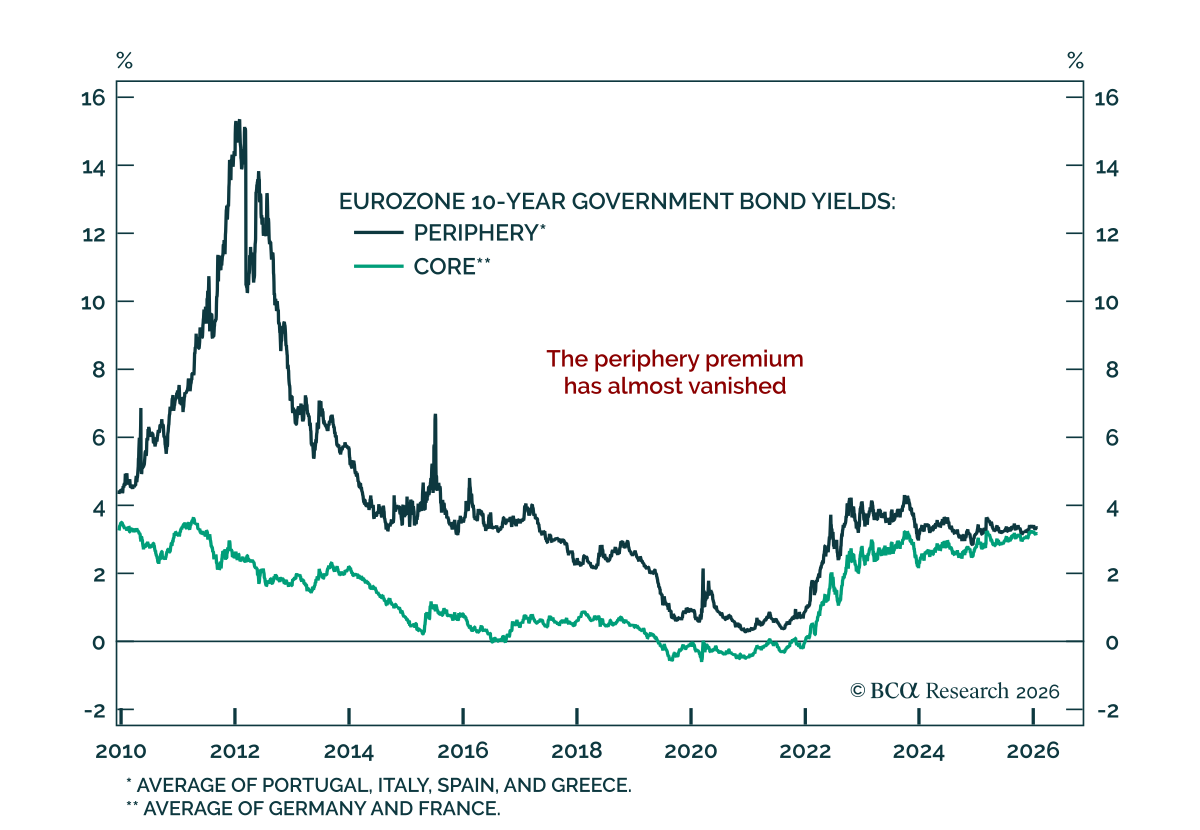

Peripheral Europe is driving the region’s resilience, and finally closing the gap with the core. Our Chart Of The Week comes from Jeremie Peloso, Chief European Investment Strategist. The resilience of the European economy and strong equity performance in…

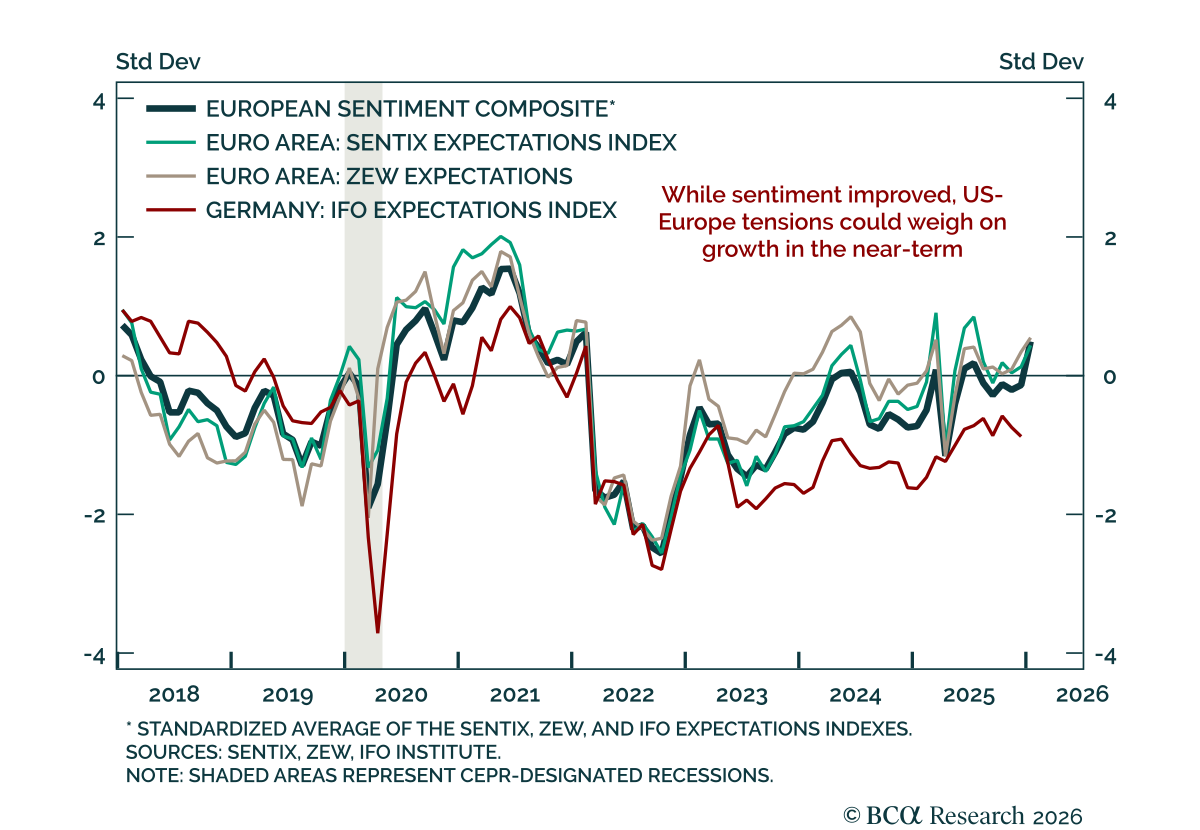

January Euro area sentiment improved, but growth momentum remains limited as tensions with the US rise and reflationary ECB cuts remain possible. January sentiment brightened in the Euro area. The ZEW survey beat expectations for Germany, with both current…

Cold inflation prints and weak momentum support reflationary ECB cuts. Preliminary December national inflation readings came in colder than expected. German CPI was flat at 0.0 % m/m (1.8 % y/y), while France printed at 0.1 % m/m (0.8 % y/y), pointing to a…

Remain tactically cautious on European assets as sentiment stays mixed and leading indicators show no acceleration. Euro area sentiment data for December continued to send conflicting signals. The Sentix index slightly beat expectations, improving to -6.2…

The November Ifo survey disappointed, highlighting weakening expectations for Germany and limited near-term upside for European growth. The Business Climate Index fell to 88.1 from 88.4, driven by expectations dropping to 90.6 from 91.6, while current…

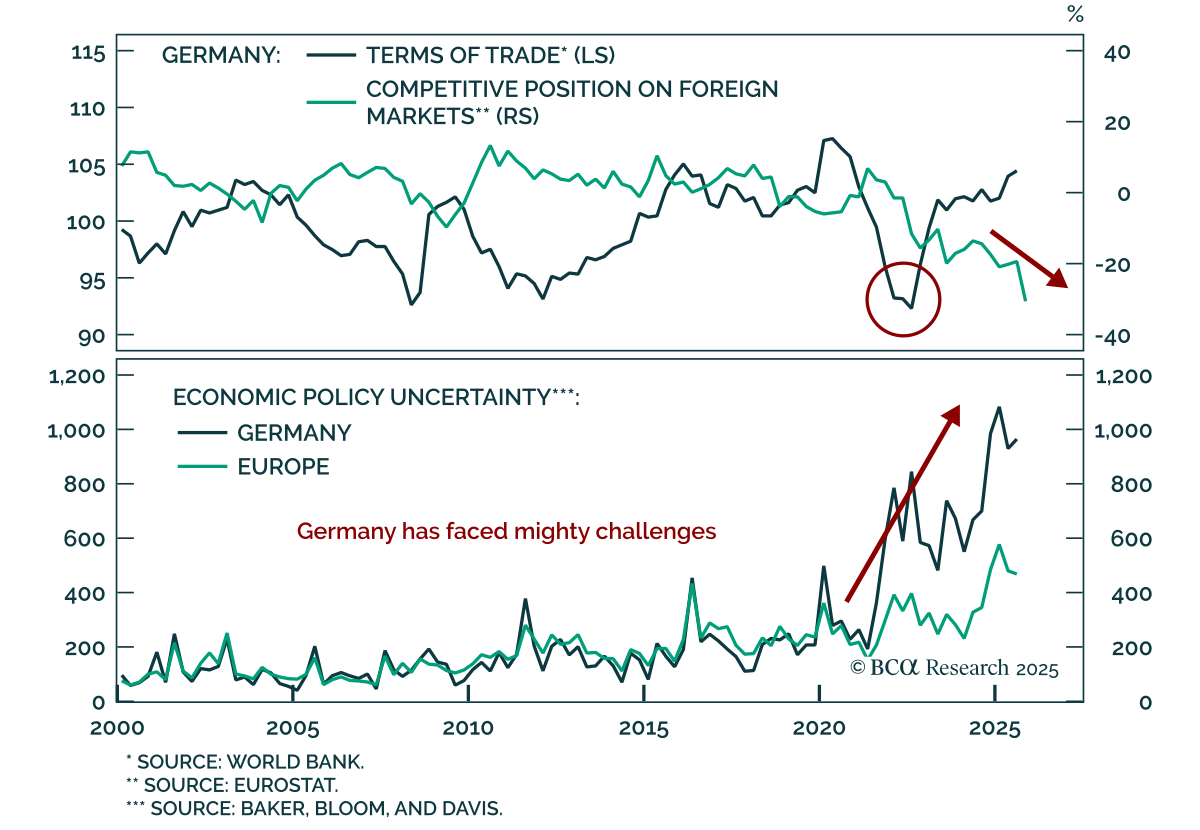

Our European Investment strategists recommend underweighting German Bunds and favoring Eurozone equities over German equities, as Germany’s cyclical rebound is offset by structural and political headwinds. After nearly two years of recession, the economy is…