Germany

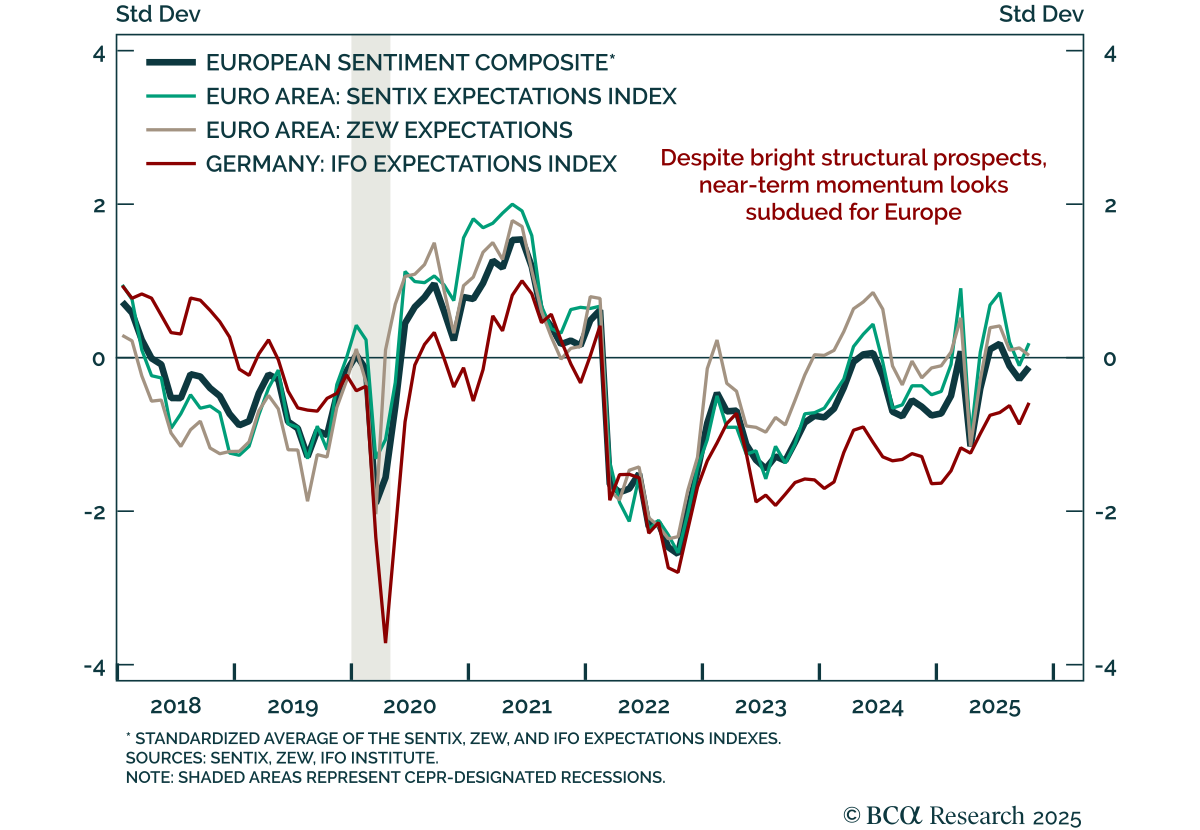

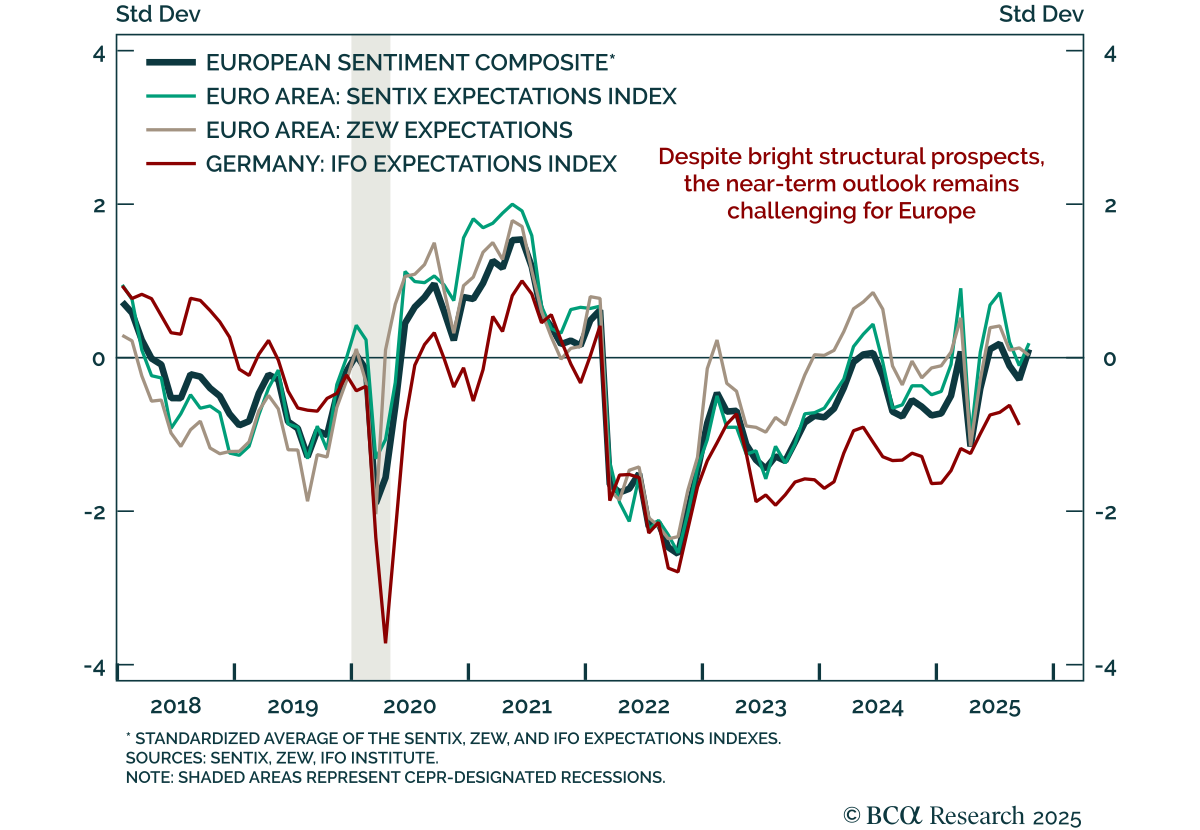

Germany’s economy is regaining momentum after nearly two years of recession. Despite the ongoing cyclical rebound and fiscal stimulus, political gridlock and deep-seated structural challenges threaten to limit the country’s long-term growth potential. Investors should be underweight German Bunds and favor Eurozone equities over German equities.

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

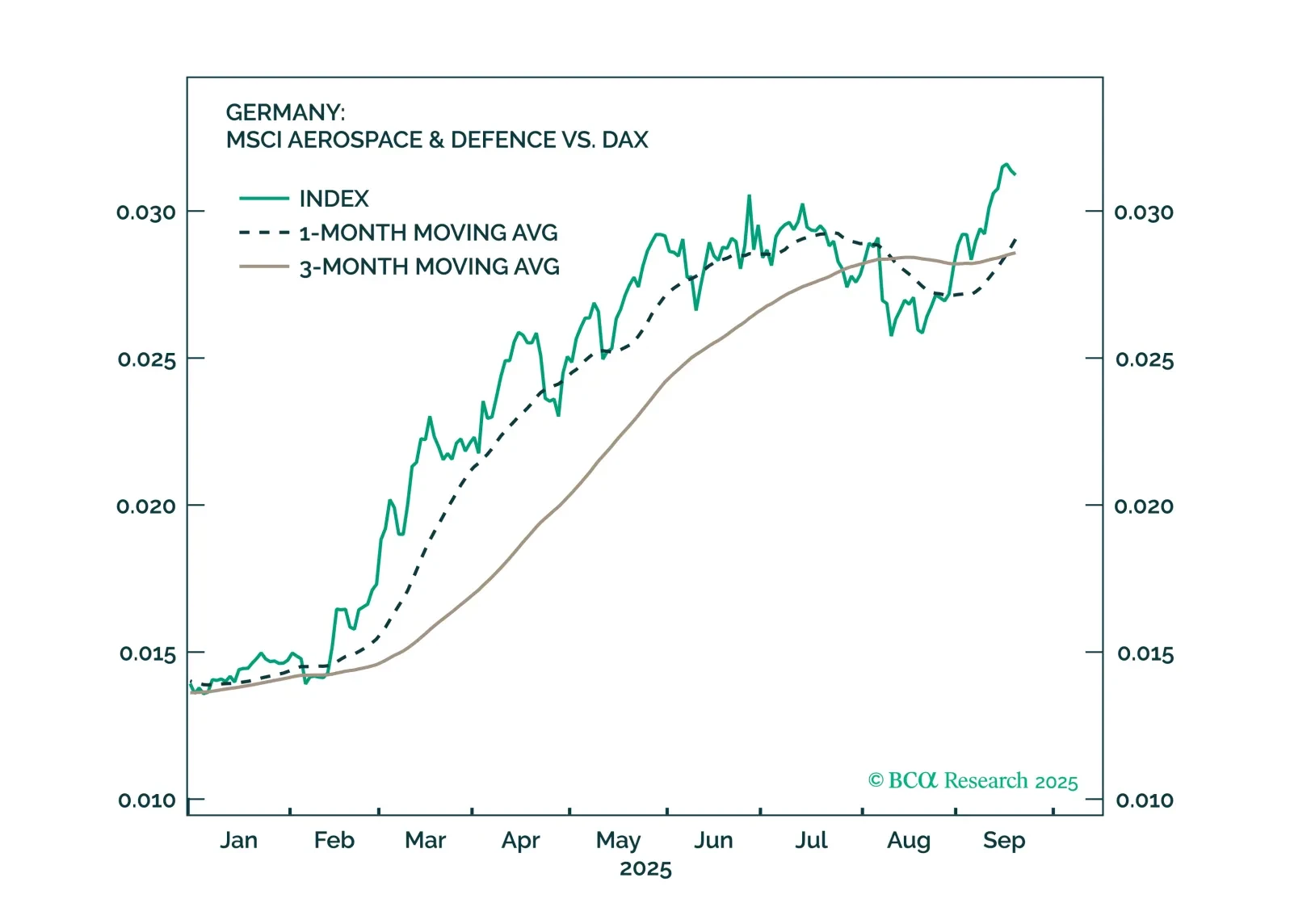

Germany is moving forward with implementing the large fiscal and defence spending announced earlier this year. Fiscal reforms are also positive, though they will fall short of expectations.

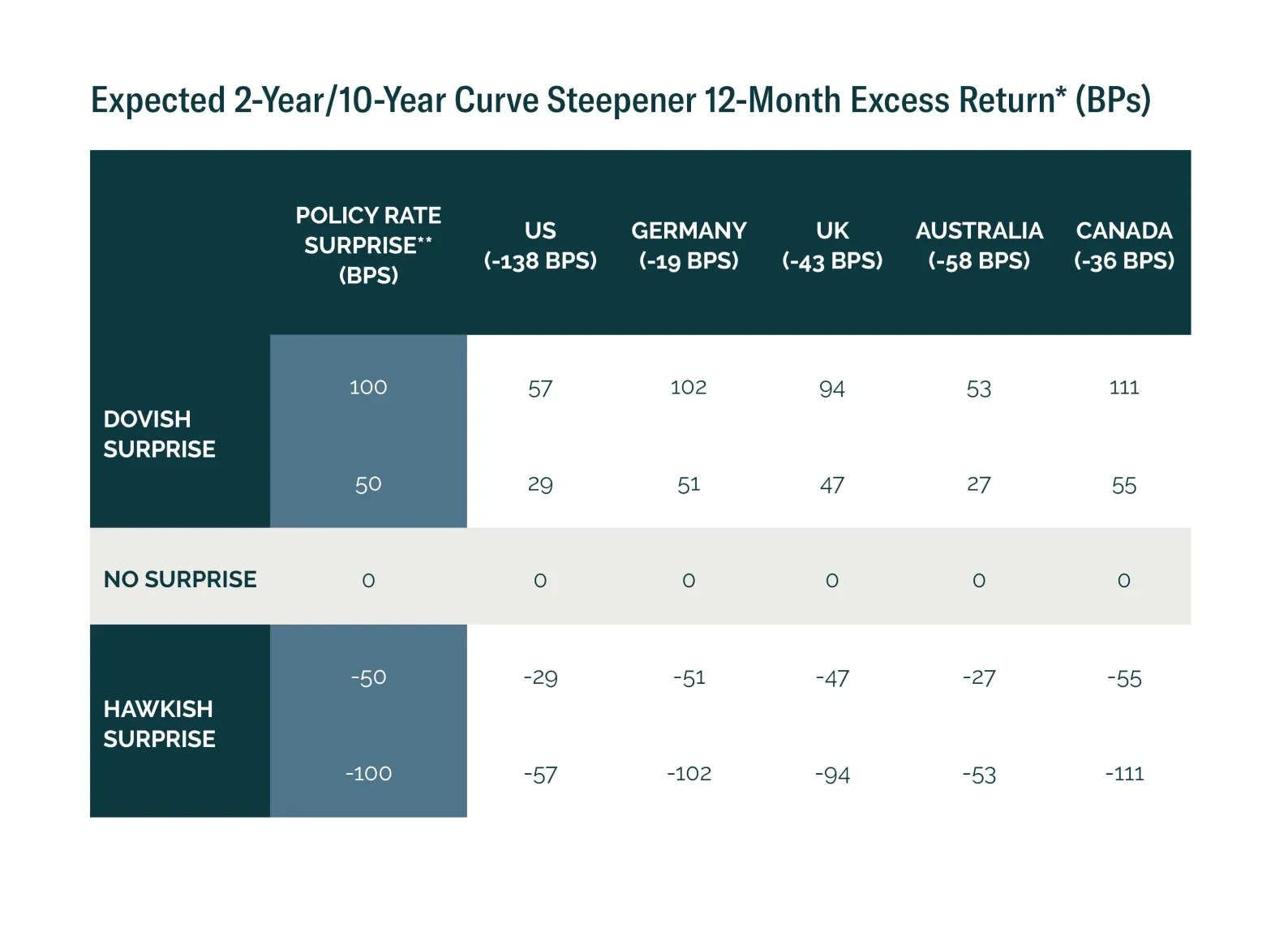

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.