Global

The dollar is now far more dependent on foreign equity inflows than it was in the late Bretton Woods era, leaving it vulnerable if capital inflows weaken. Our Chart Of The Week comes from Arthur Budaghyan, Chief EM/China Strategist. Arthur draws a…

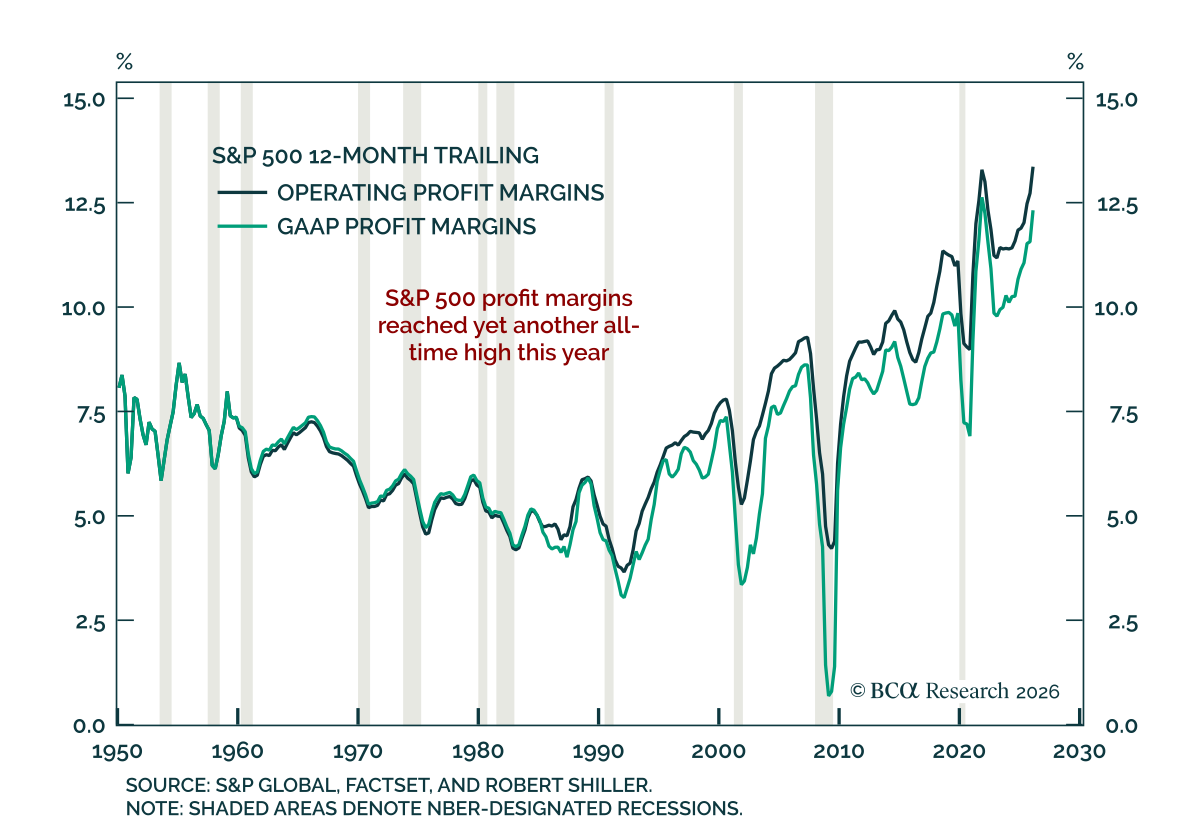

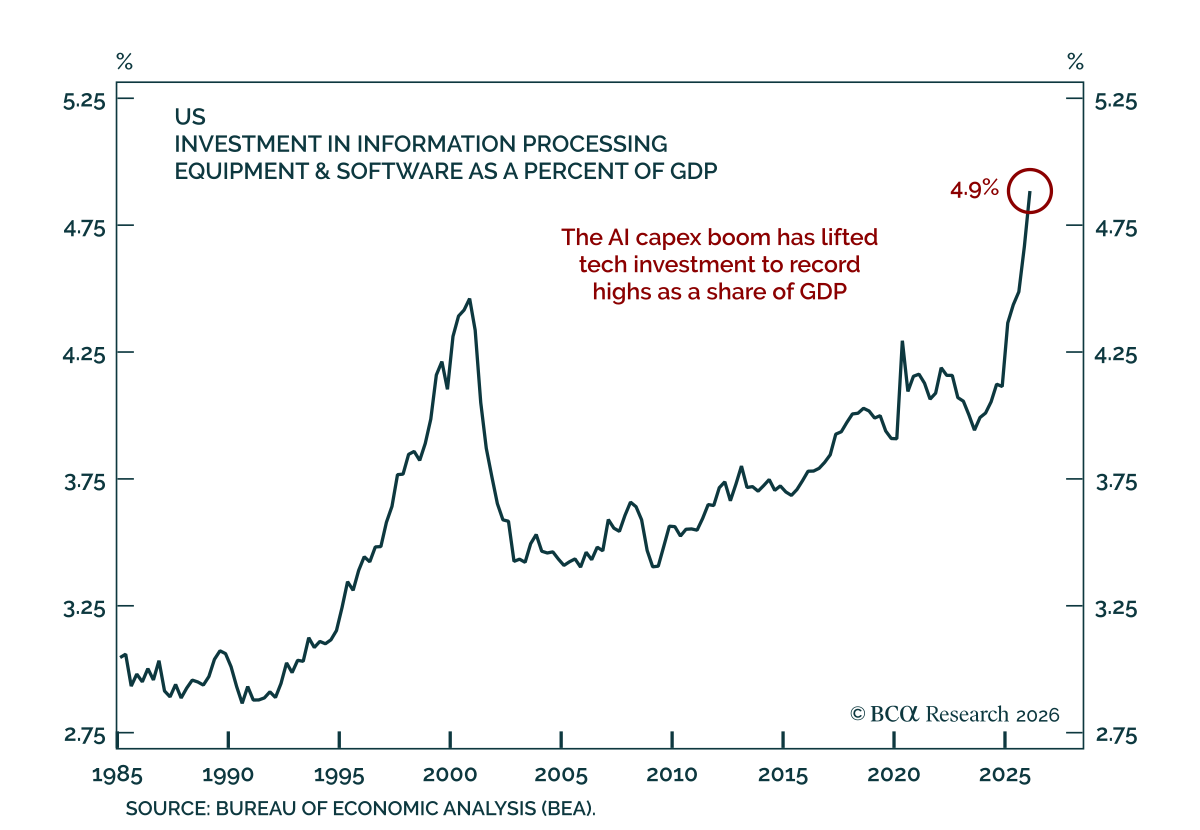

Our Global Investment strategists see US profit margins deteriorating next year. They expect margins to stay elevated through the rest of 2026, helped by robust business sales, muted real wage gains, and the AI capex boom. Beyond that, the picture dims. A…

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.

Our Global Investment strategists see the equity bull market entering its late stages and expect bonds to do well once growth slows. Lower oil prices and heavy AI capital spending should support the global economy through the rest of 2026, but our colleagues…

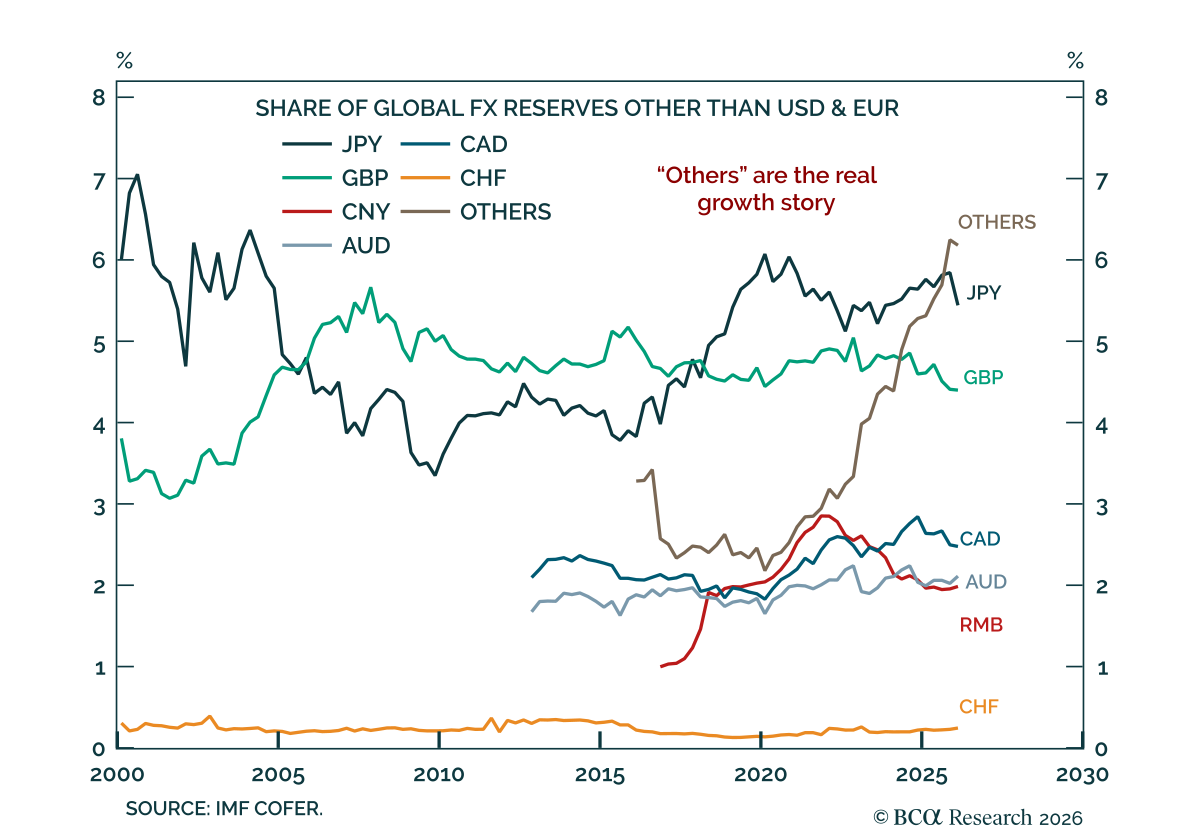

Our FX strategists expect the global reserve system to grow less dollar-centric. This will benefit a widening set of smaller fiat currencies rather than any single successor to the USD. The dollar's share of global reserves has fallen more than five…

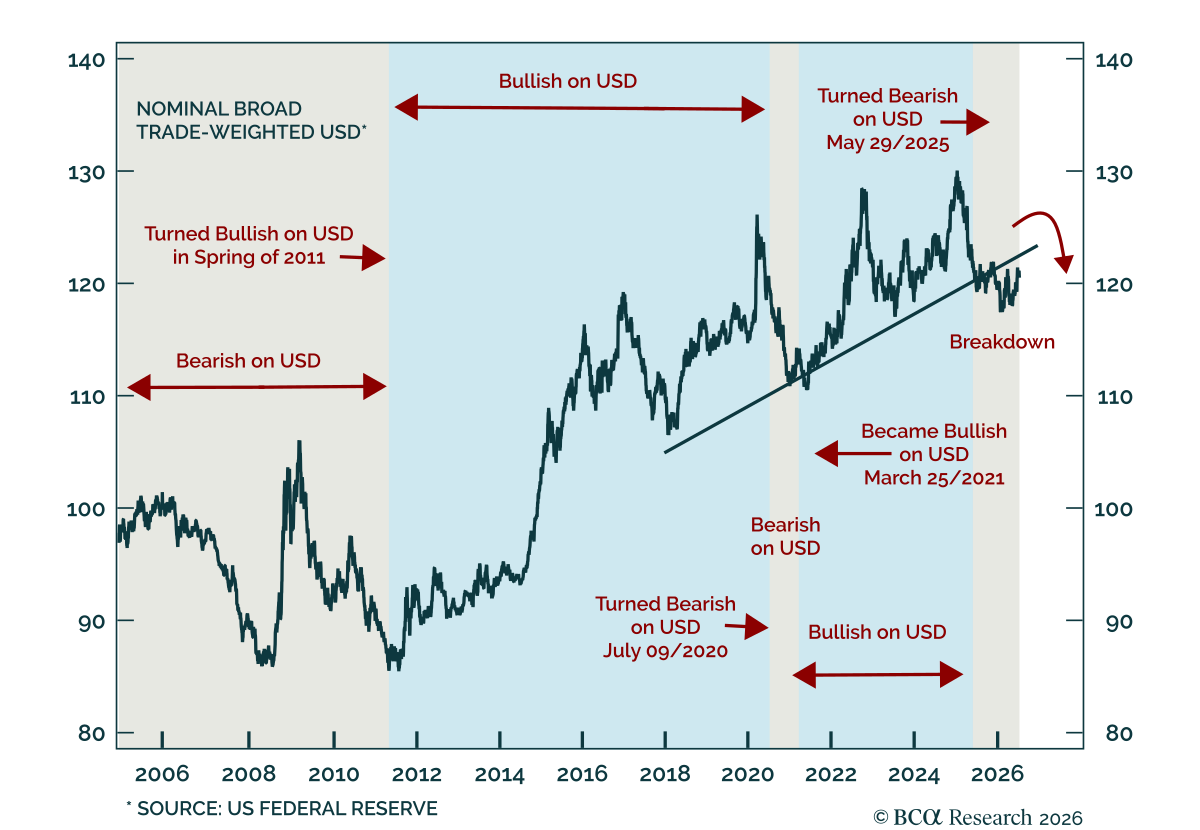

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

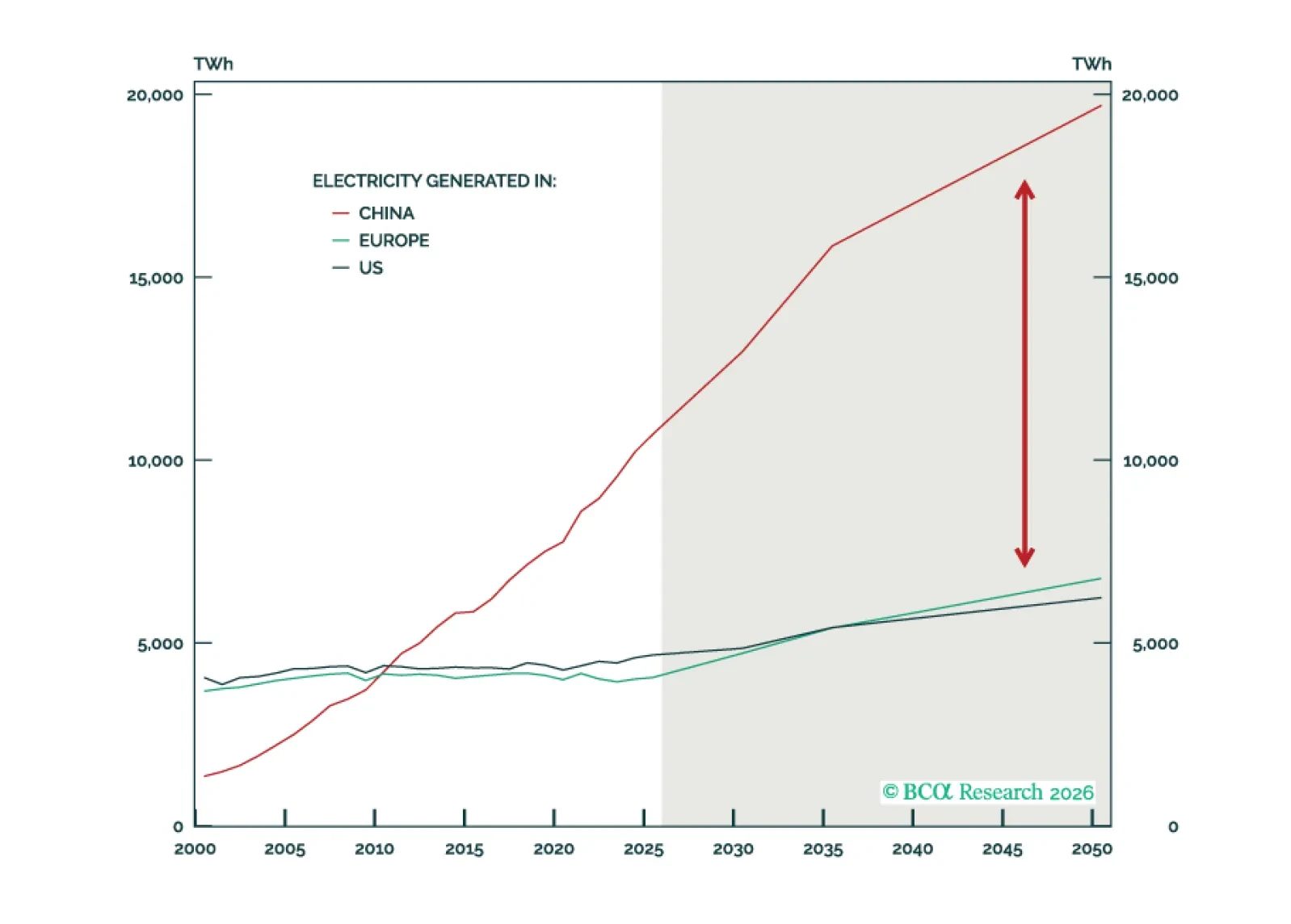

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

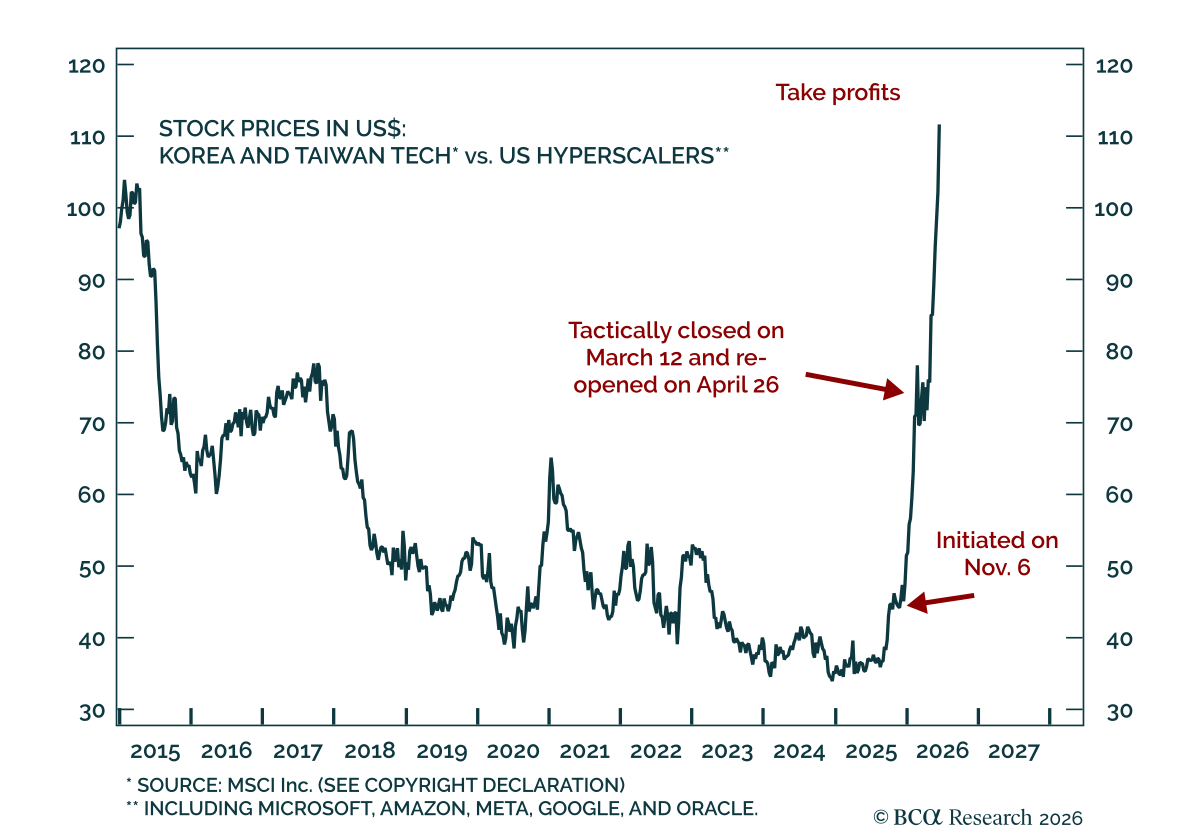

Our EM strategists view Korea’s equity tantrum as a warning for global risk assets and recommend taking profits and downgrading Korean stocks. Korea has become the most extreme expression of the global equity rally, driven by semiconductor momentum, high-beta…

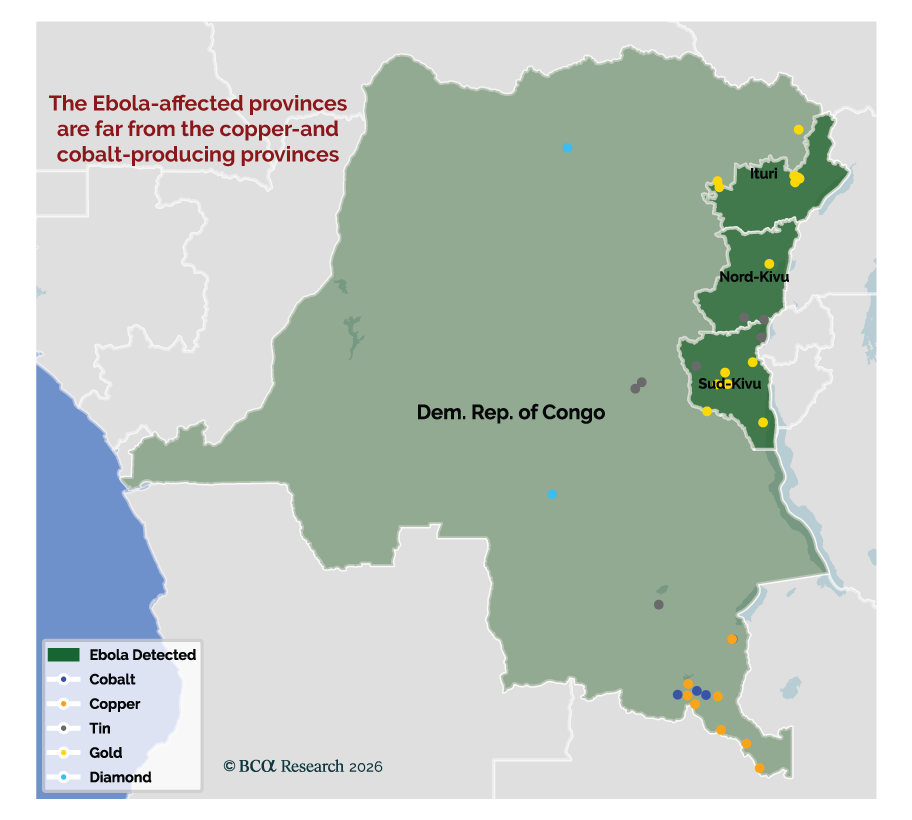

Our Geopolitical strategists see the DRC Ebola outbreak as a low-probability but high-consequence supply-chain risk. The country holds a critical position in global copper and, especially, cobalt production. Our colleagues expect the outbreak to stay…

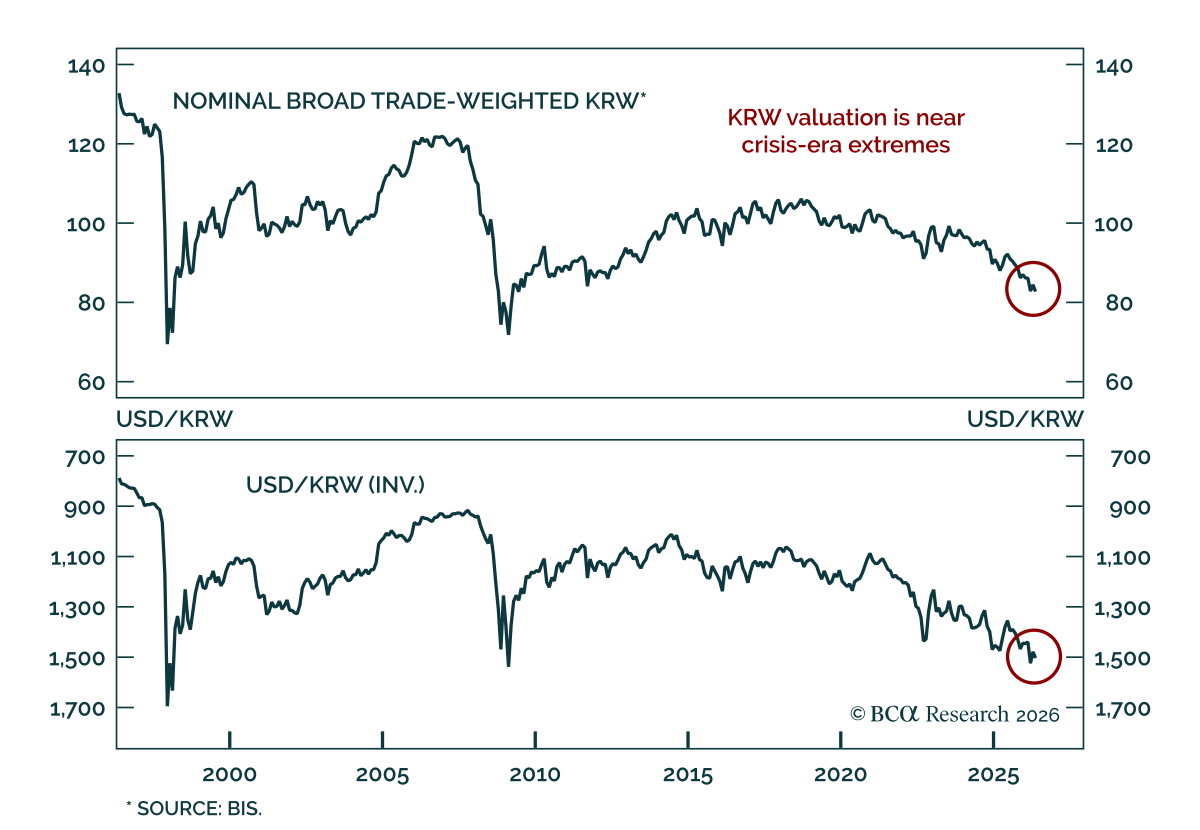

Our FX and EM strategists see the Korean won as increasingly mispriced, and recommend positioning for appreciation. KRW weakness is driven by unfavorable portfolio flows, not by any deterioration in Korea's growth or external position. Flow-driven weakness of…