Global

OPEC+ extended its production cuts for the third time, and lengthened the period over which it plans to bring spare capacity back online. Oil prices continue to trade near the bottom of their trading range despite the announcement. The decision aims to…

Our GeoMacro Strategy service published their 2025 outlook, and they see three peaks shaping the year: Peak fiscal, peak-deglobalization, and peak geopolitical risk. In 2024, our colleagues’ bullish economic outlook proved accurate in the first half, while…

Our Global Asset Allocation strategists published their monthly tactical asset allocation report and foresee a change of trend for 2025. “Thin is back in” for government budgets, growth, and valuations. The post-COVID recovery was marked by government…

South Korea is undergoing political turmoil, with President Yoon attempting to declare martial law. The situation is fluid and can change quickly, but there are a few investment takeaways. As we pointed a few weeks back, BCA expects geopolitical tensions…

November trading was centered around the US election and its aftermath. US assets led the way, with US equities significantly outperforming their global counterparts. The US dollar strengthened considerably against both DM and EM currencies. Investment-grade…

The November ISM Manufacturing index beat expectations, increasing to 48.4 from 46.5 in October. The improvement was partly driven by the new orders component, which increased to 50.4 from 47.1. Price pressures moderated. The underlying details of…

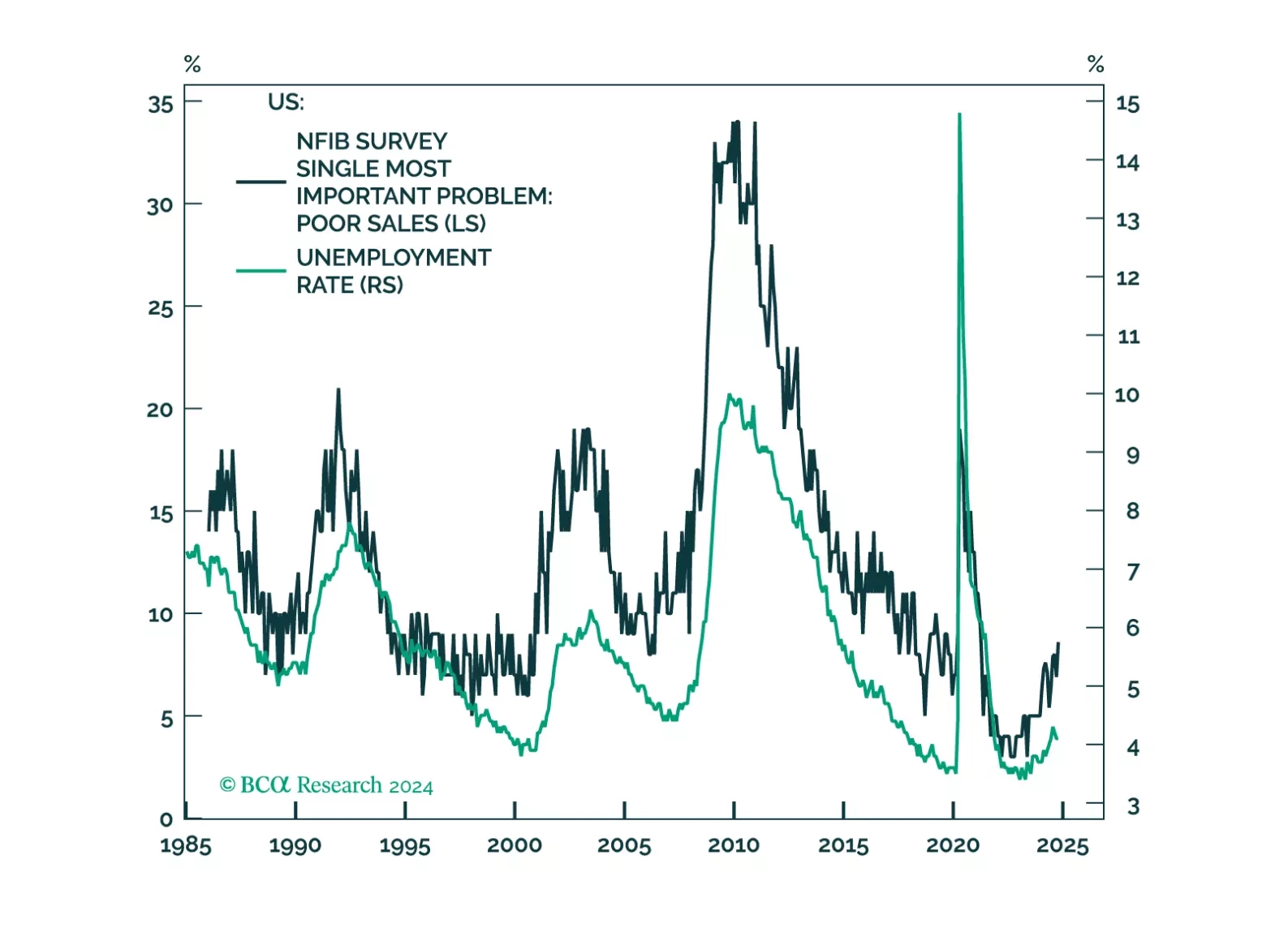

The post-COVID recovery has been one of excesses. Government deficits have ballooned, tight labor markets have led to a windfall of consumer spending, and equity valuations have soared on the back of lofty growth expectations. But these excesses will no longer be sustainable in 2025. Our theme for next year is Thin Is Back In. Government budgets, economic growth, and equity valuations will be leaner than investors expect. We discuss this the reasoning behind this macro view and the asset allocation implications that follow from it.

Our Commodity & Energy Strategy team evaluated the impact of president-elect Trump’s policies on commodity markets. Trump’s energy policies, while promoting increased domestic oil production, are unlikely to drive immediate growth in US crude output.…

Our Private Markets & Alternatives strategists have delved into the North American Buyouts market, concluding that the investment playbook needs rewriting. The performance of Middle Market Buyouts has been exceptional, leading many investors to stick…

President-elect Trump jolted markets Monday night by declaring that tariffs will be implemented on imports from Mexico, Canada, and China. The US dollar strengthened while stocks fell, as did Treasury yields. Equities, however, recovered on Tuesday, as a…