Global

China’s National Development and Reform Commission (NDRC) provided no insights Tuesday on the size or nature of the fiscal stimulus Beijing promised in late September. The key takeaway of the authorities' first briefing following a weeklong national holiday…

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

German factory orders contracted by a larger-than-anticipated 5.8% m/m (3.9% y/y) in August, from a 3.9% expansion (4.6% y/y). Domestically, Germany is constitutionally bound to maintain a balanced budget. The emergency pandemic funds disbursed in 2020 are…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the upside in September coming in at 105.5 against expectations of 101.0. The August reading was also significantly revised higher, from 101.6 to 105.0. …

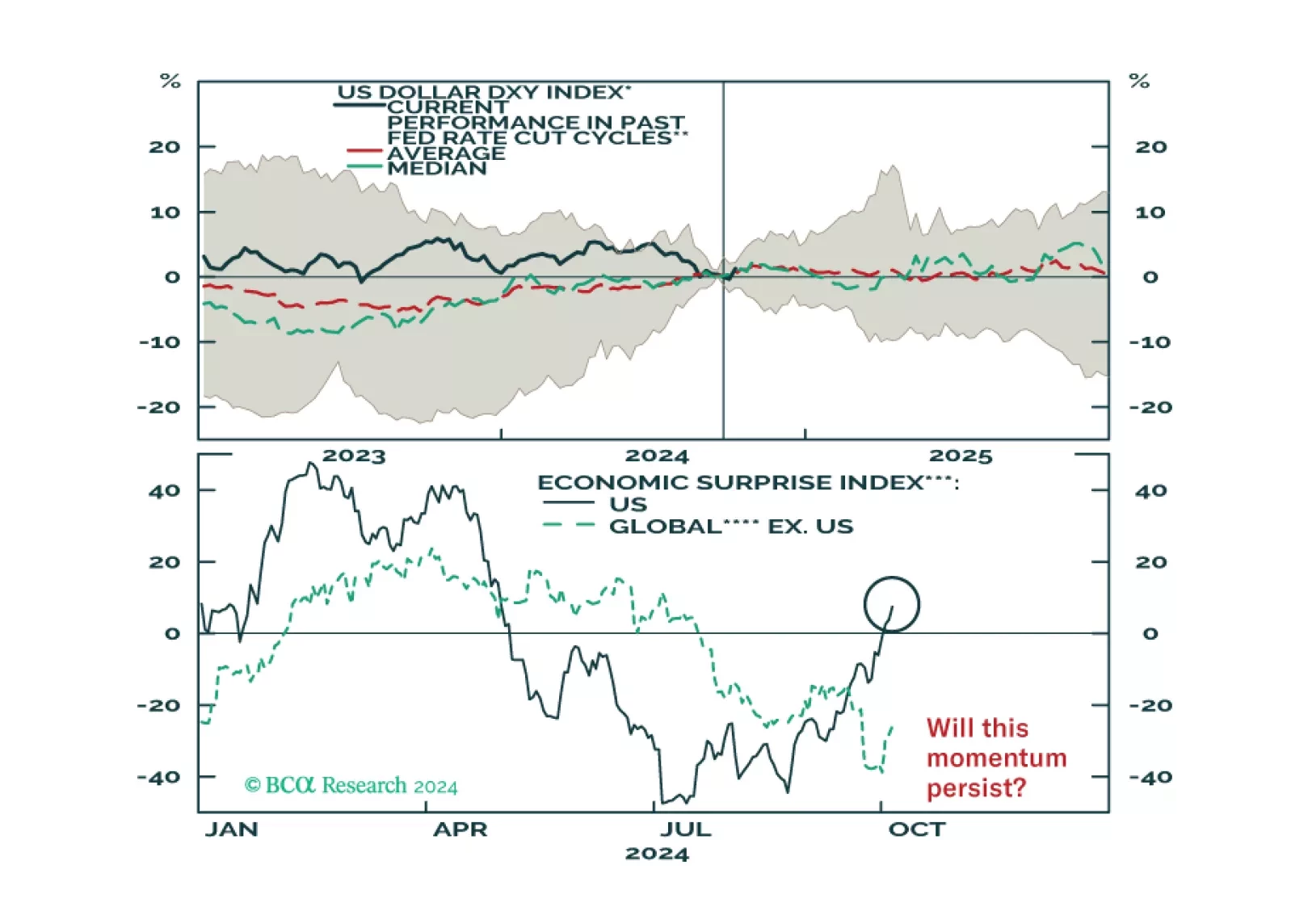

The dollar had erased all of its 2024 gains going into the fall, as markets prepared for Fed rate cuts. After a nearly 6% drawdown over the spring and summer, last week’s DXY rally brought the dollar back into the black YTD. Can these gains continue now…

According to BCA Research’s Private Markets & Alternatives service, intra-market repricing will offer investors a unique opportunity to enter the industrial real estate space in the next two years. In the short term, Mexico will be a big winner…

This report looks at the likely path for the dollar and bond yields over the next 6-to-12 months.

The European Commission voted to impose tariffs of up to 45% on imports of Chinese electric vehicles (EVs). The announcement follows previous tariffs imposed on Chinese EV imports back in June. This new round of economic sanctions will only have a minor…

According to BCA Research’s Bank Credit Analyst service, CAPEX does not appear to be especially broad-based even among the largest companies in the US. The enclosed chart presents a bottom-up estimate of CAPEX as a percent of sales for the S&P…