Global

Global semiconductor stocks have returned 50% YTD in USD terms, and a whopping 200% since their September 2022 lows. However, they may have peaked back in July. Our Emerging Market strategists highlight a significant bifurcation between the revenues of…

The July Employment Situation report had already cemented the case for a September rate cut and Chairman Powell’s Jackson Hole comments dispelled any remaining doubt about an imminent monetary easing cycle. All the labor market data released since then…

BCA’s Global Leading Economic Indicator, a GDP-weighted average of the standardized leading indicators of 23 DM and EM economies, has had a good track record of predicting year-on-year changes in the IMF global real GDP growth series. The Global LEI has…

According to BCA Research’s Commodity & Energy Strategy service, central banks will continue to be a key source of gold demand. Central bank purchases in the first half of this year exceeded first-half purchases in every year they’ve been tracked going…

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

According to BCA Research’s Emerging Markets Strategy Service, China has been accumulating high-value memory semiconductors in anticipation of further US restrictions. Since October 2022, the US has been tightening rules that would limit China’s progress…

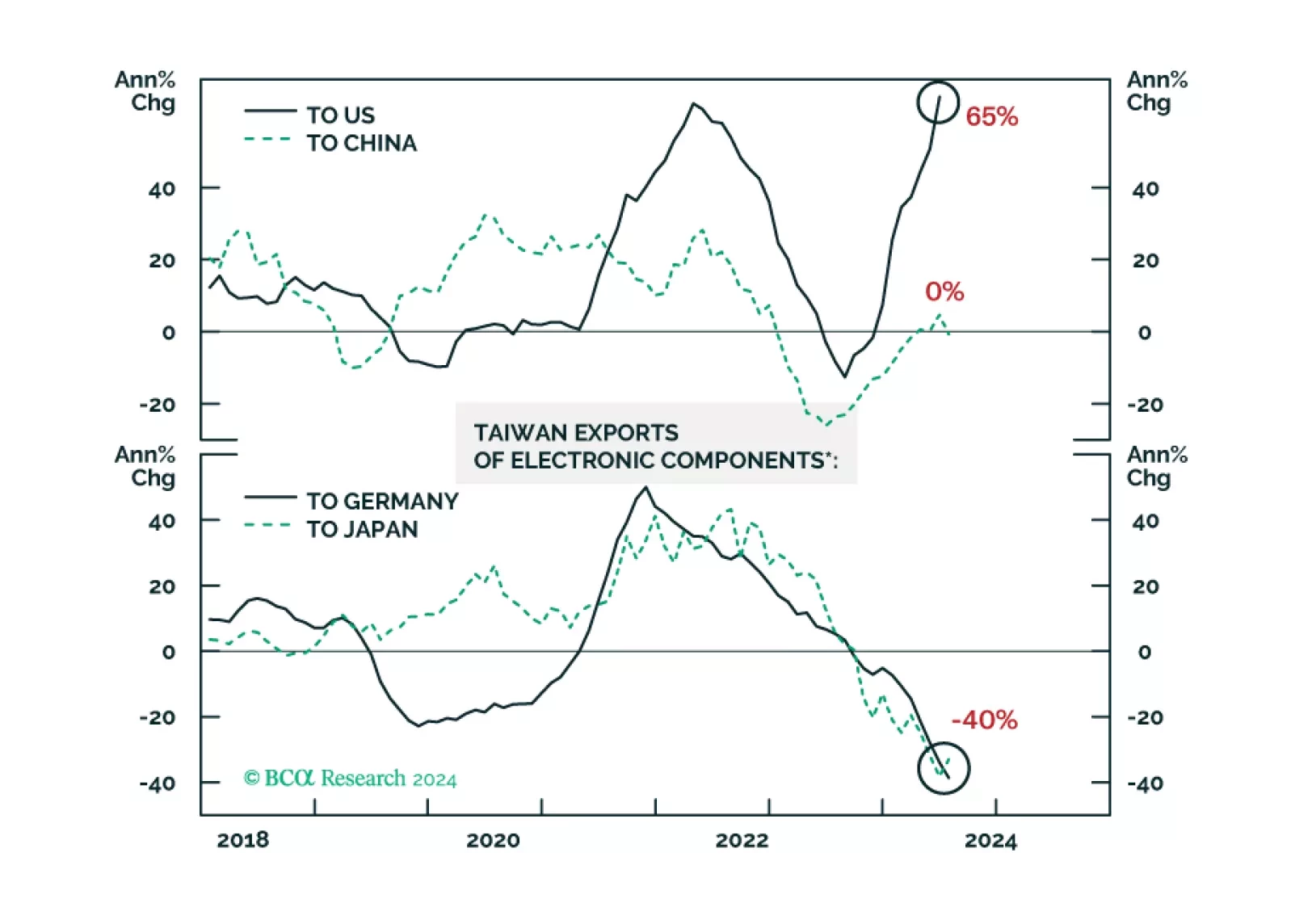

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

According to BCA Research’s GeoMacro Strategy service, there are two main pressure points that the US can utilize against China. First, the US consumer market is the largest in the world. Despite having diversified away from the US, it remains a very…

The risk-on soft-landing narrative dominated investors’ psyche last month and pro-cyclical assets topped the August return ranking. Asian currencies led the pack by a wide margin, while the dollar was the largest laggard. Markets pricing in an upcoming Fed…