Global

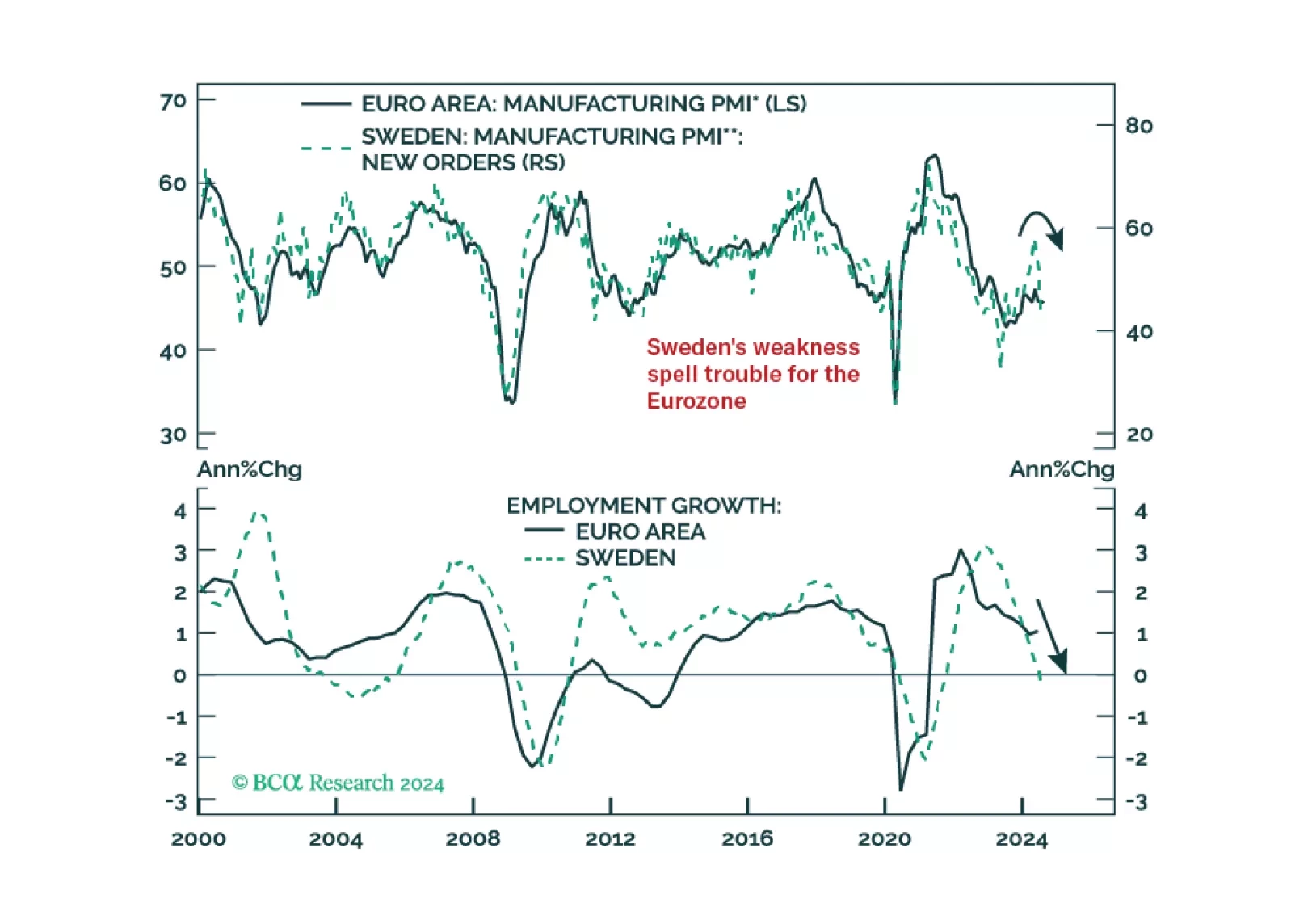

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

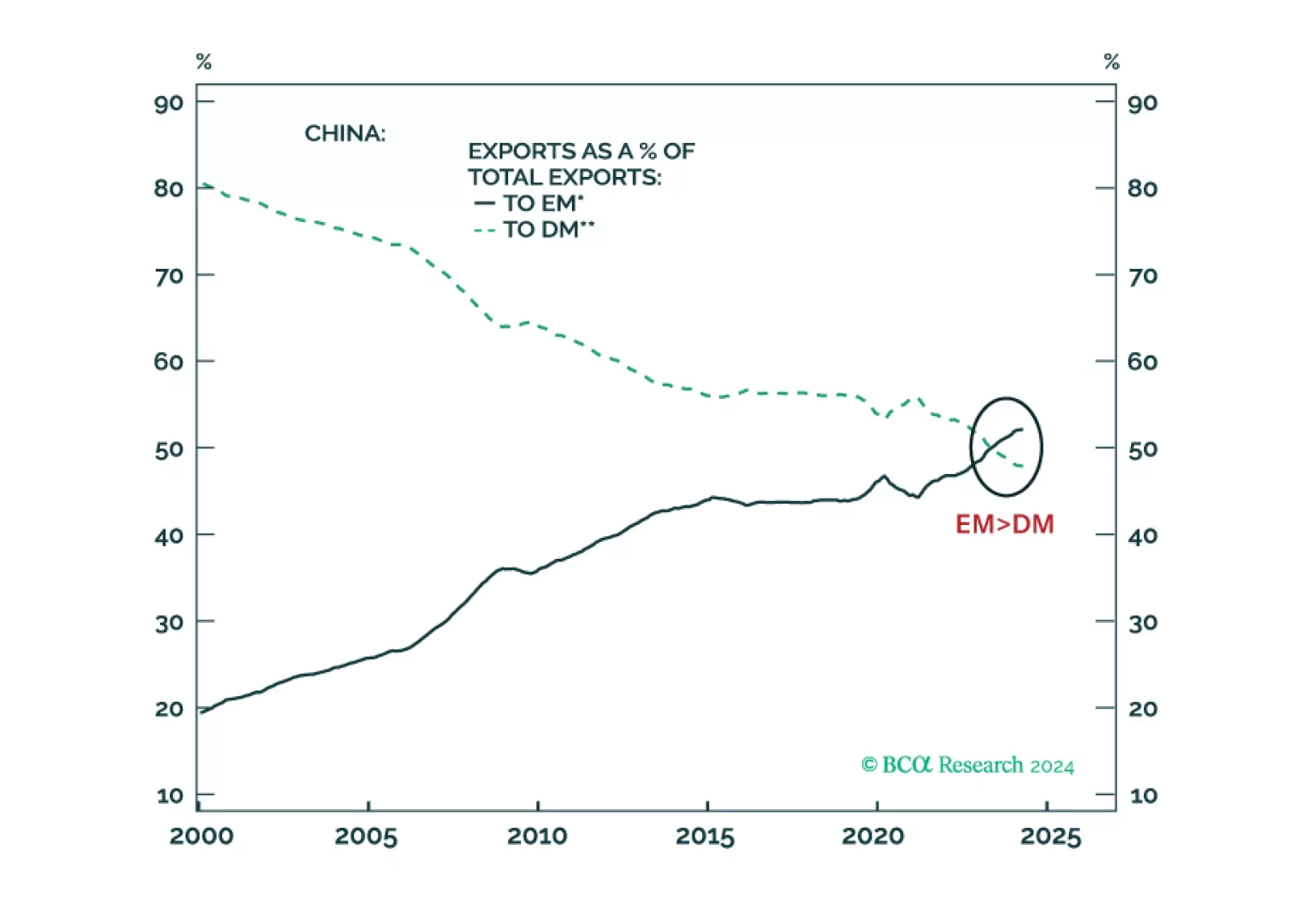

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

Gold reached new all-time highs earlier this week. The yellow metal has returned a whopping 20.2% YTD, with the rally reaccelerating over the past month. Gold prices are inversely correlated with the dollar, and the expectations for US interest rate cuts have…

According to BCA Research’s Geopolitical Strategy service, the logic of pursuing one’s interest against US interests in the final hours of the election mostly applies to states that will suffer a significant loss to their strategic security if the…

According to Goldman Sachs’ Financial Conditions Index (FCI) financial conditions have become considerably more supportive since the fall of 2023. More recently, the index ticked noticeably lower from 99.4 earlier in August to 98.8. US equities have indeed…

In a widely expected move, the Riksbank lowered its policy rate from 3.75% to 3.5% in August. It had kept rates on hold in June, after having led many other major DM central banks in easing policy in May. The Riksbank also signaled it could cut as many as…

Back in May, our Commodity and Energy strategists argued that OPEC, EIA, and IEA oil demand forecasts were likely too optimistic. Indeed, while all three major oil price forecasters projected a moderation in demand this year, none of them anticipated weak…

EM equities have dramatically underperformed their US and Eurozone peers in USD terms over the past 15 years. The inability of EM and EM Asia companies to grow their EPS largely explains EM equities “lost decade” (and a half). Since 2010, US EPS have grown…

According to BCA Research’s Commodity and Energy Strategy service, soft oil demand growth raises the likelihood that OPEC+ will back down from its plan to begin unwinding some of its production cuts later this year. However, investors should not read this as…