Global

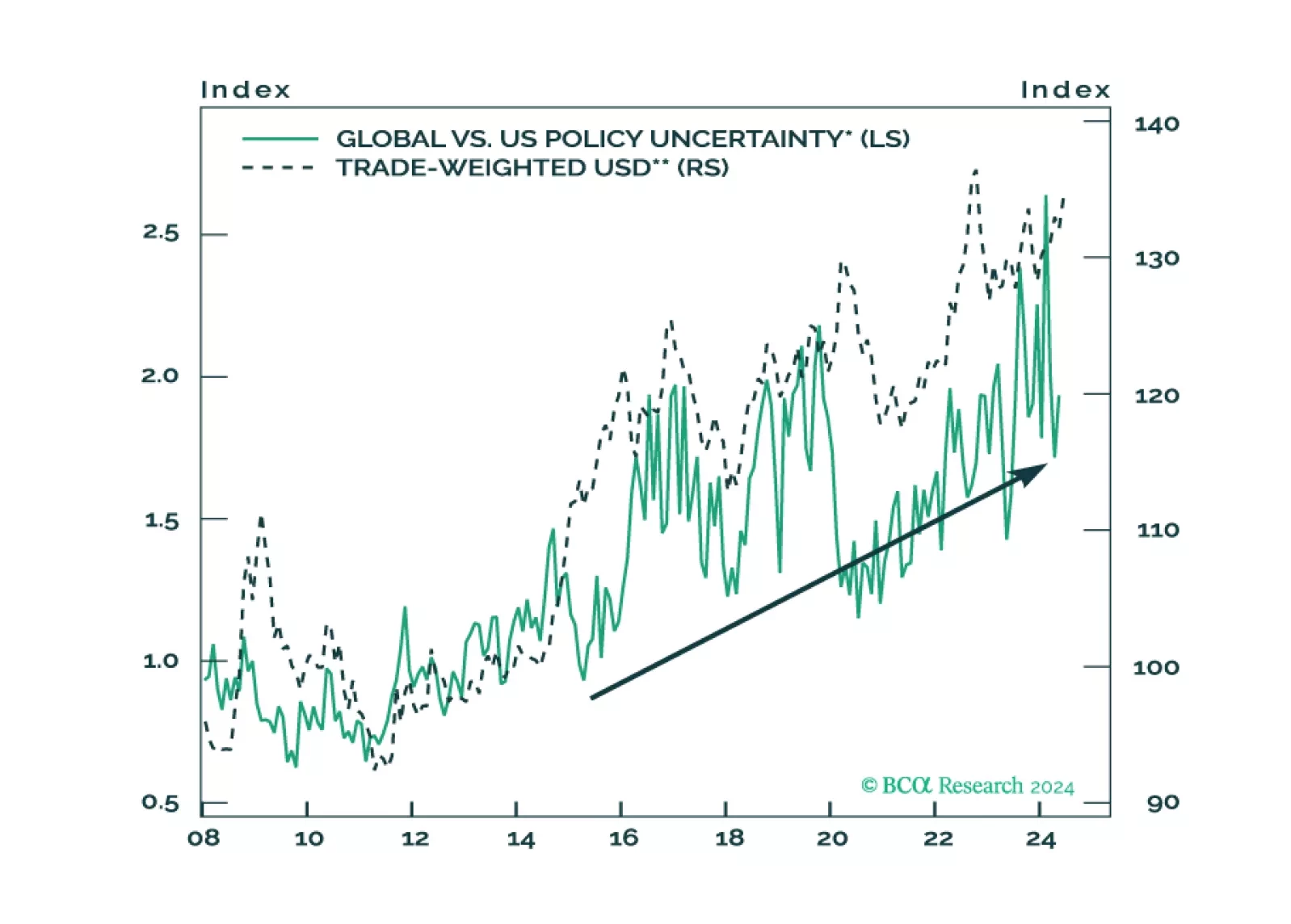

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

Outside of the US, forward earnings have grown at an underwhelming pace this year. Forward earnings for MSCI US have expanded by 7.3% in 2024YTD while MSCI EMU has remained flat and MSCI Japan has contracted by 4.9%. Against this backdrop, EMs stand out as…

The Euro Area economy broadly surprised to the upside in the first half of 2024. Cooling inflation lifted real wages and the global late cycle amelioration benefitted the pro-cyclical Euro Area economy, but these tailwinds are fading. First, monetary…

Investors greeted June’s mild CPI report with relief. 10-year Treasury yields declined a dozen basis points in the ensuing four sessions (with yesterday’s action fully reversing Monday’s backup on the increased probability of a Trump victory), the S&P 500…

Marko Papic, a pioneer in using geopolitics as an essential component of investment strategy, has returned to BCA, where he founded Geopolitical Strategy, the world’s first dedicated investment consultancy focused on political analysis. Geopolitical…

GeoMacro’s monthly Beta Report will typically perform deep dives into the most pressing macro topics of the moment. For its debut, however, it turns the microscope on its own process, explaining the team’s framework and how investors can best incorporate its…

US dollar liquidity has been shrinking, which has important ramifications for global asset prices, including currencies. In this report, we delve into the process of dollar liquidity creation and the outlook for currencies over the next six-to-twelve months.

After having peaked in mid-April, Citigroup’s global economic surprise index has been in negative territory for the past few weeks. The sub-zero reading indicates that economic data have been surprising to the downside and signals deteriorating economic…

An investor looking at the low unemployment rate and elevated job vacancy rate could reasonably conclude that the US expansion will continue. However history suggests that recessions often start seemingly out of the blue. Solid growth in the fourth quarter…

Copper has experienced a roller-coaster ride so far this year, with front-month futures on the Chicago Mercantile Exchange gaining nearly 40% from early February to late May, tumbling nearly 15% in just over five weeks, and bouncing around 7% over the last…