Global

Sweden is a small export-oriented economy and its high sensitivity to global trade makes it a good bellwether of global growth developments. The headwinds from high borrowing costs are relatively more pronounced in Sweden where a large share of households…

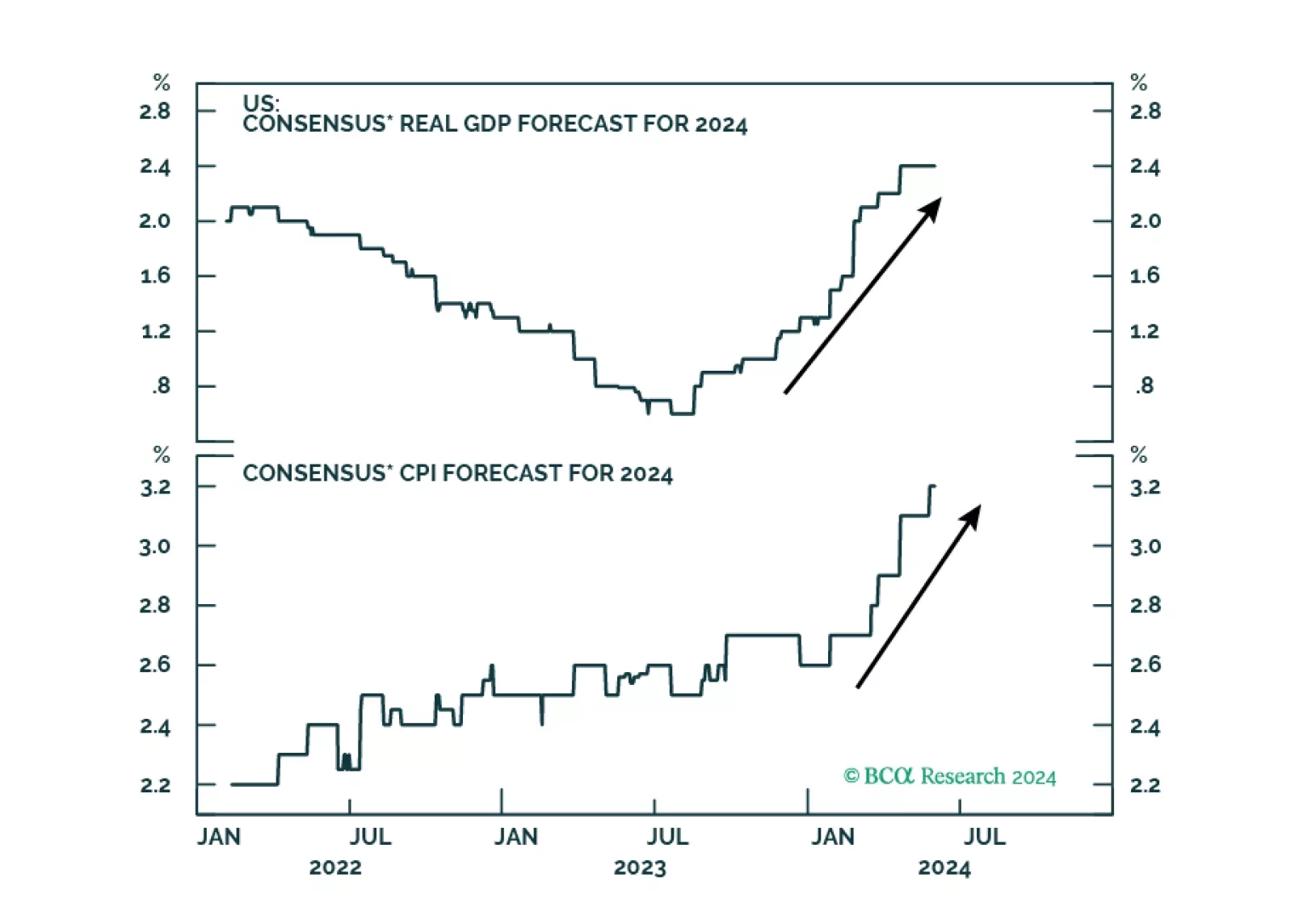

Global growth expectations for 2024 have been revised higher. Investors now forecasts 2024 GDP growth to clock in at 3%, up from 2.6% at the beginning of this year. A 1.1% upward revision in US growth expectations since January is driving the increased…

BCA’s Global Leading Economic Indicator has had a good track record of predicting year-on-year changes in the IMF global real GDP growth series. This GDP-weighted average of the standardized leading indicators of 23 DM and EM economies bottomed in early 2023,…

The ISM Services PMI largely surpassed expectations in May. The headline index grew by 4.4 ppt to 53.8, returning to expansion following April’s one-month contraction. Double-digit jumps in new export orders (13.9 ppt) and business activity (+10.3 ppts) drove…

The silver-to-gold ratio has surged close to 10% this year on the back of silver prices catching up to gold. Silver has returned 22% on a YTD basis, against 12% for gold, 13% for industrial metals and 5% for the broad commodity complex, making the white metal…

Utilities have had a stellar run since February with the MSCI ACW Utilities index outperforming the MSCI ACW by nearly nine percentage points. Despite being a defensive sector, Utilities’ performance this year has been comparable to that of top performing…

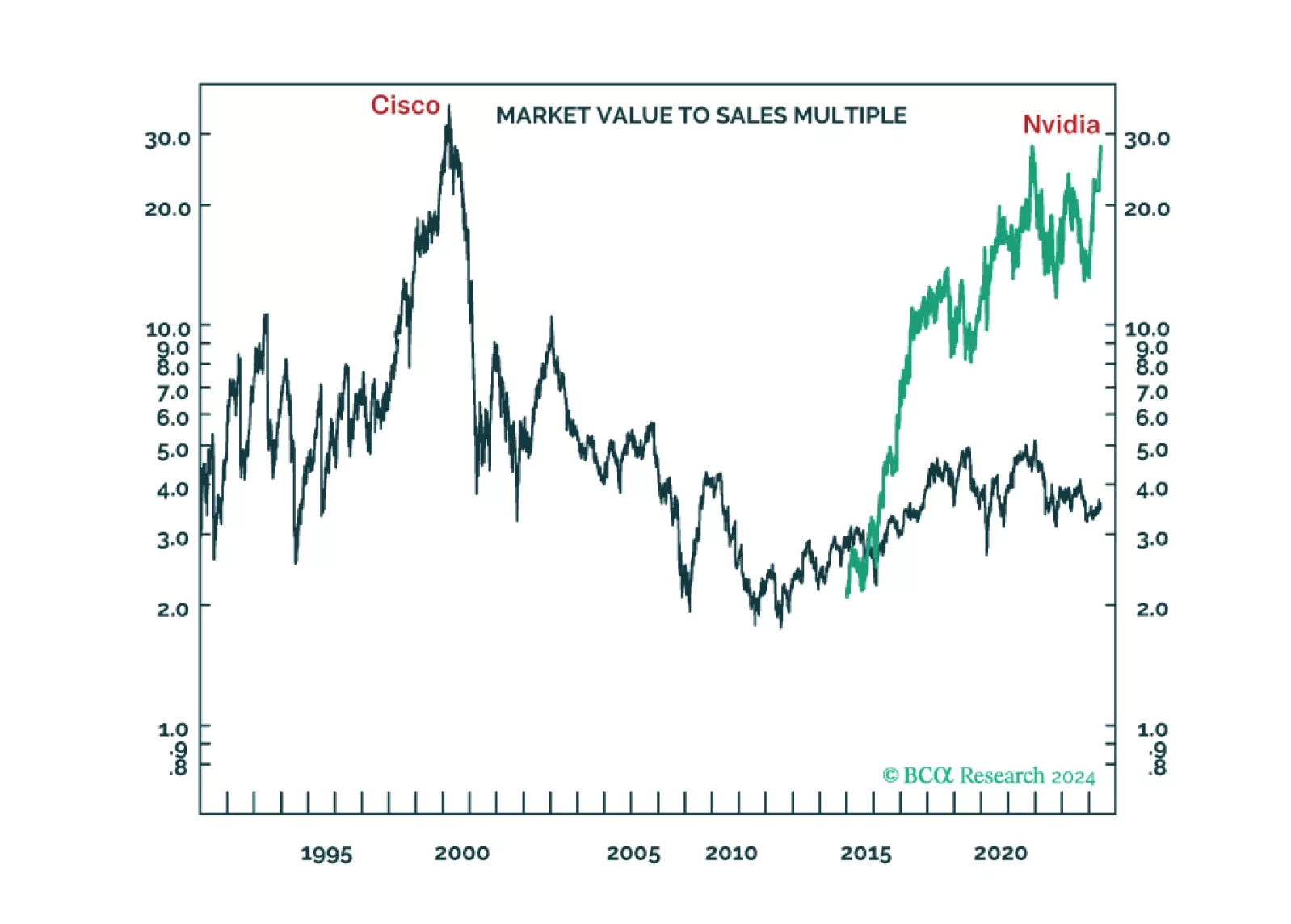

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

The risk-on soft-landing narrative dominated markets in May, with both equities and bonds rallying throughout the month. Meanwhile, the counter-cyclical US dollar slumped, and the cyclical euro appreciated against the greenback. Regionally, US assets…

According to BCA Research’s Commodity & Energy Strategy service, the oil demand forecasts from the IEA, EIA, and OPEC are too optimistic. The IEA, EIA, and OPEC all anticipate oil demand growth to slow this year following a robust post-pandemic…

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.