Global

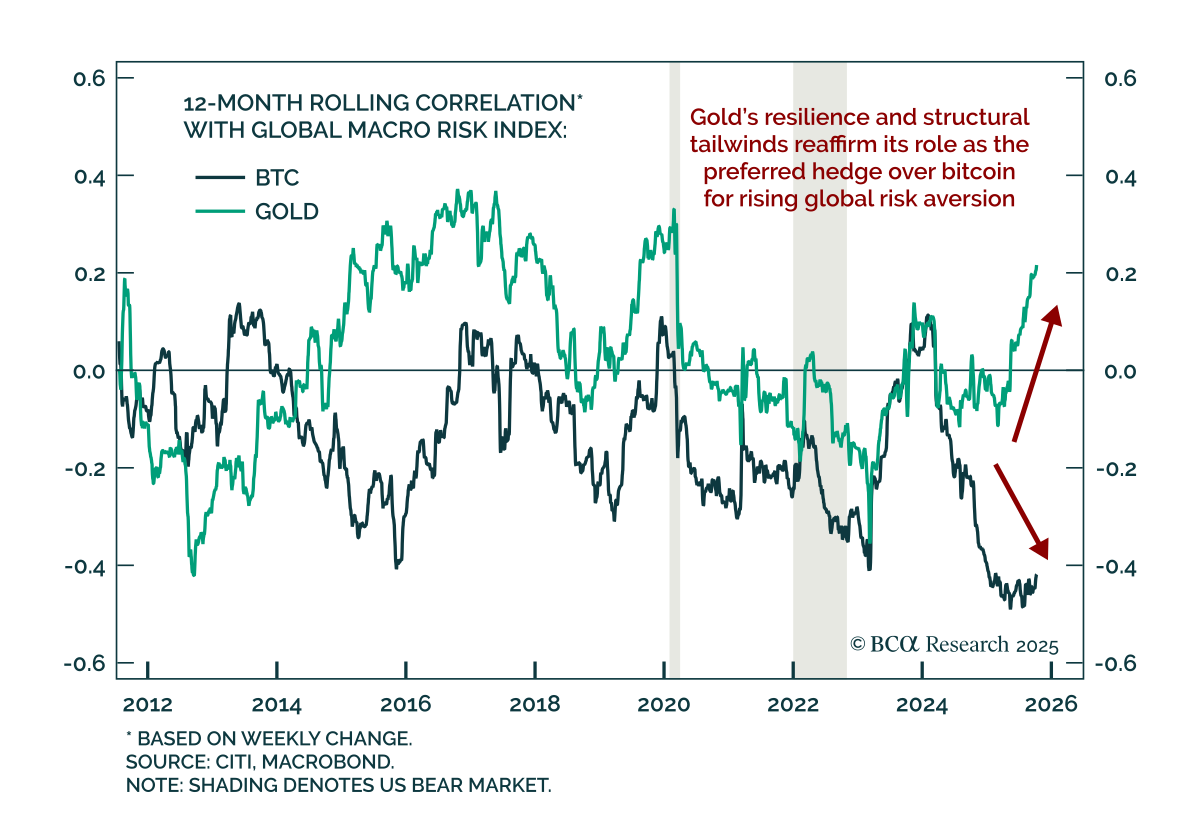

Gold remains a superior hedge asset to bitcoin during global risk-off periods. Both assets have rallied strongly this year, reaching new all-time highs as beneficiaries of the dubbed “debasement trade,” reflecting investor demand for alternatives to fiat…

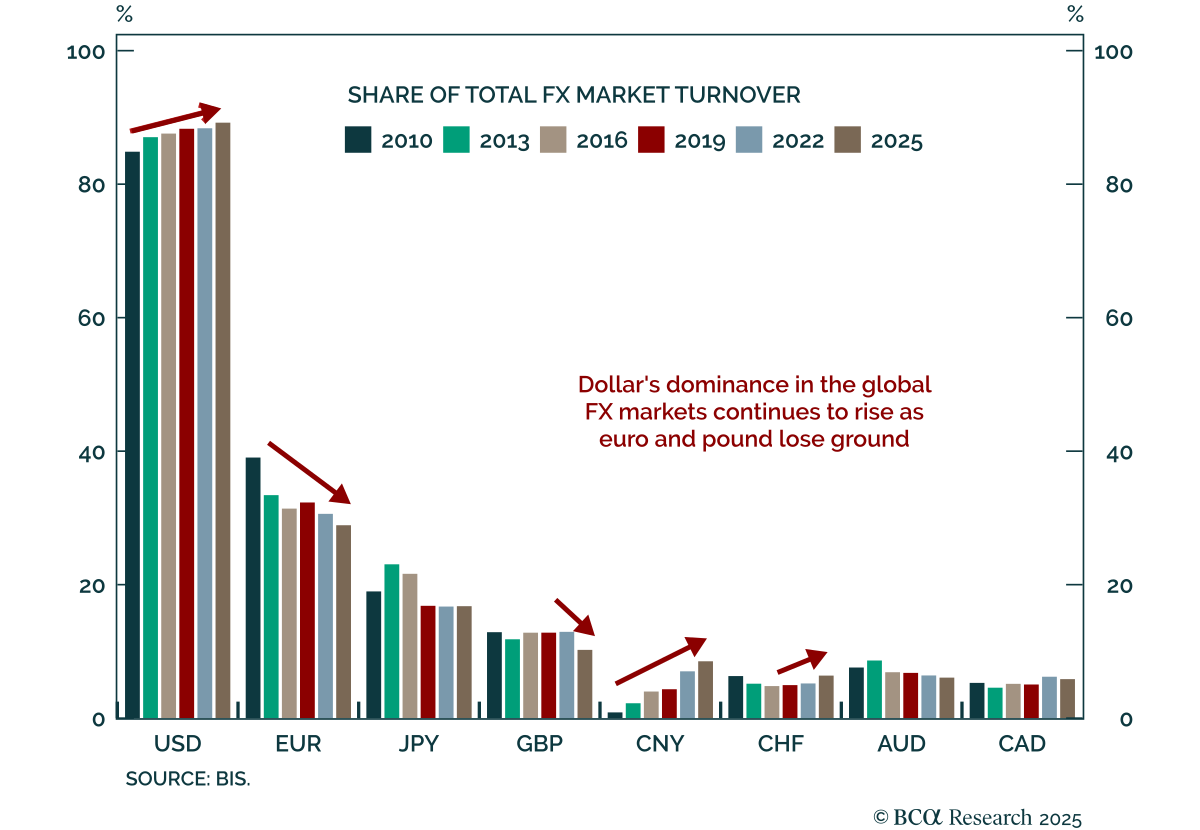

The latest BIS Triennial Central Bank Survey reaffirms the US dollar’s dominance in global FX markets, highlighting the structural challenges of truly moving away from the USD-centric financial system. The survey conducted in April 2025 reported total…

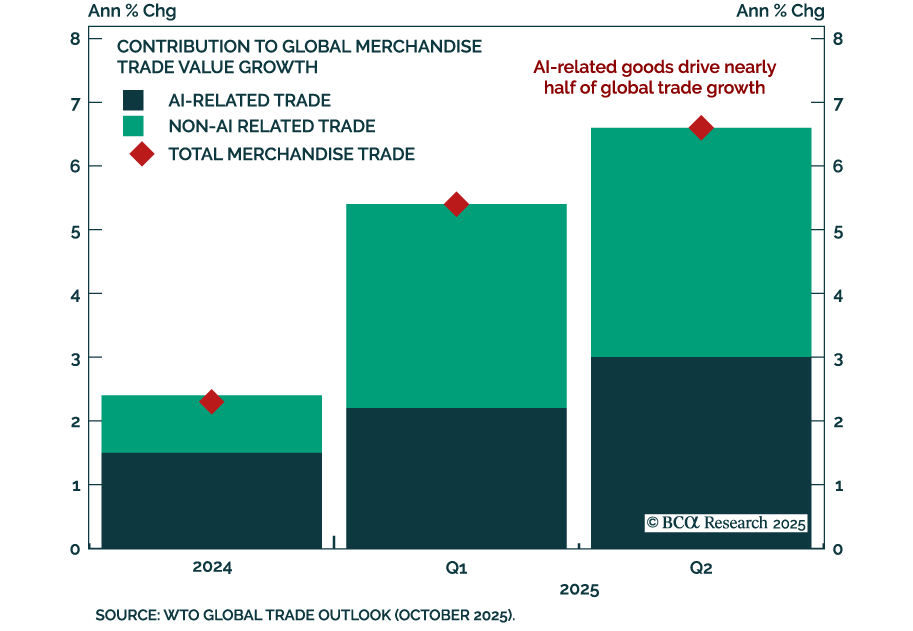

AI-related trade and frontloading lifted global trade growth in 2025 but also increased the risk of a slowdown next year, according to the WTO’s latest Global Trade Outlook. The organization sharply revised up its forecast for 2025 merchandise trade volume…

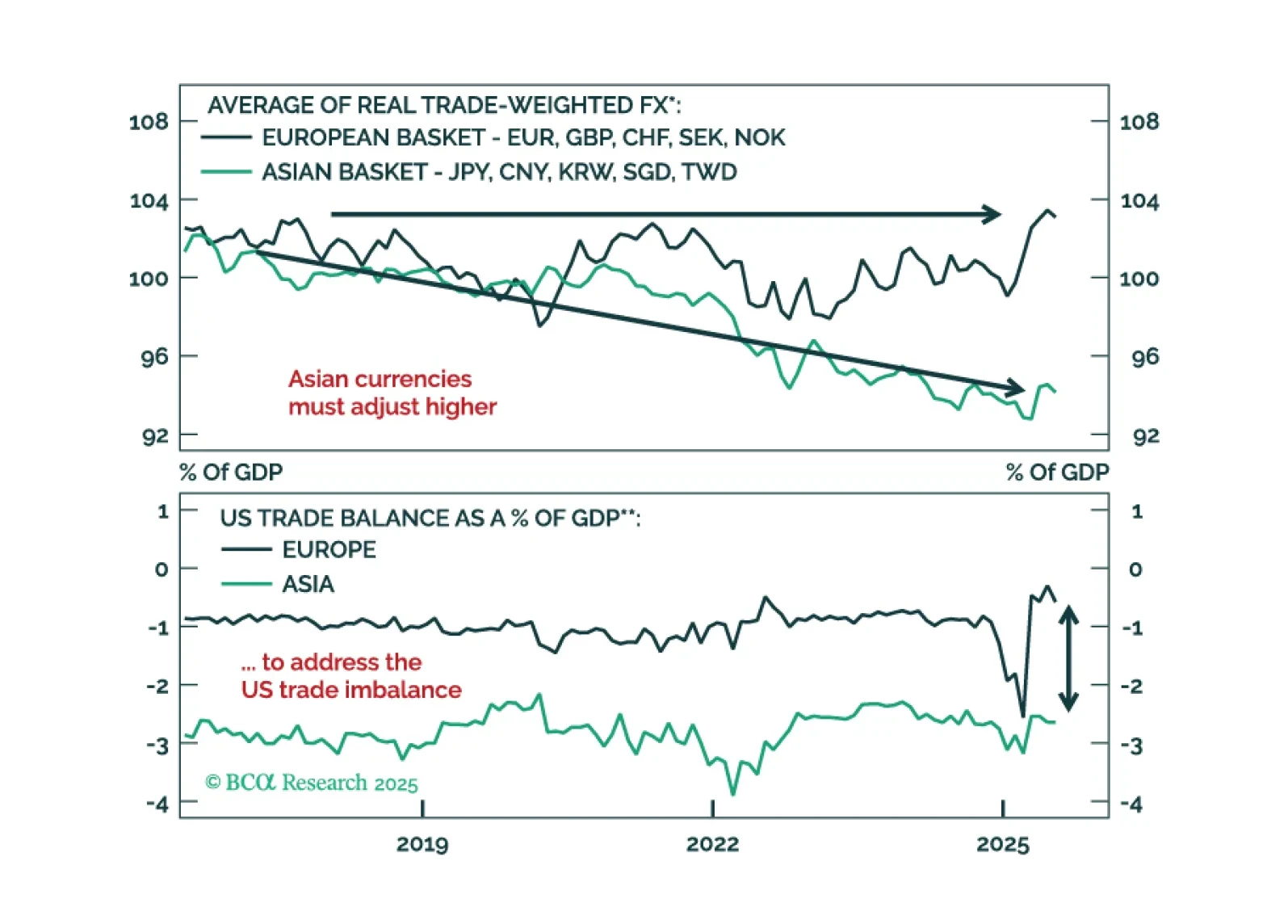

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

Momentum is building behind small-cap and value stocks, signaling a rare dual tailwind for cyclical styles. Our Chart Of The Week comes from Guy Russell, strategist for Equity Analyzer.While market attention remains focused on the Mag 7 and Tech, Equity…

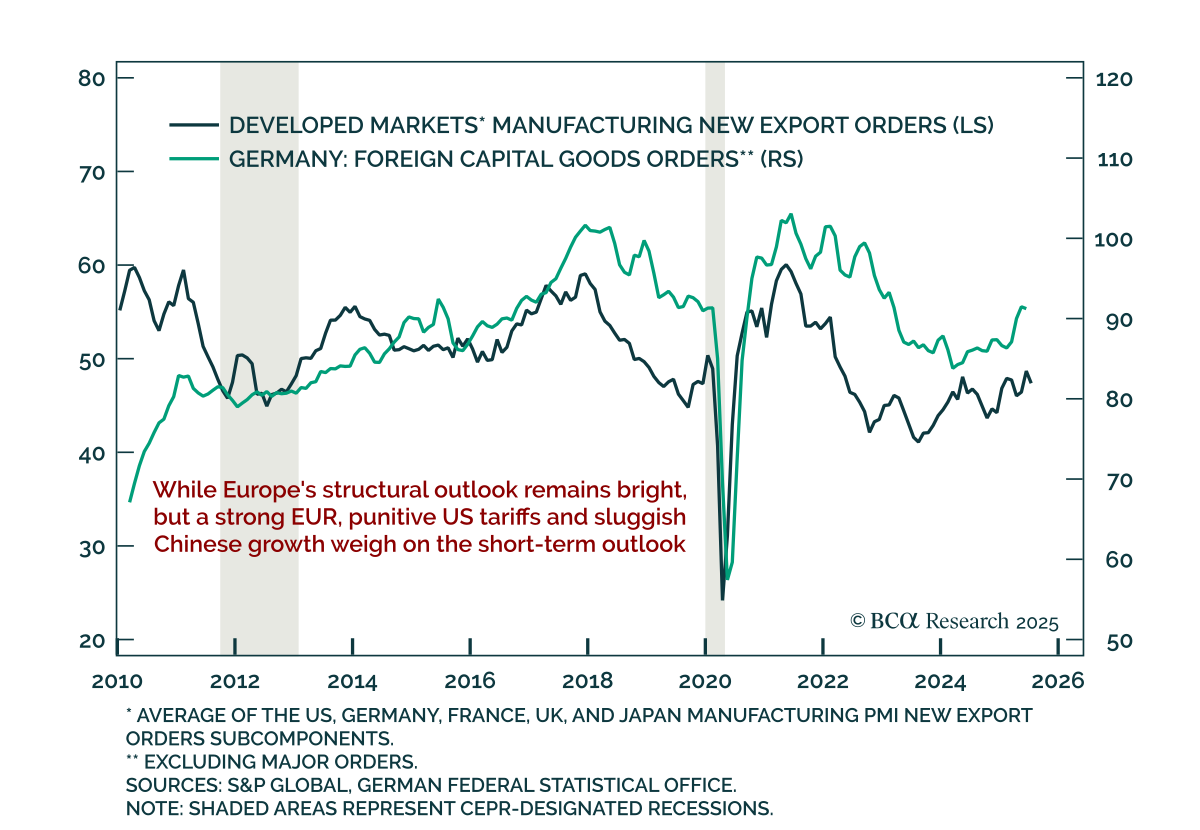

Germany’s June factory orders missed expectations, highlighting persistent headwinds reinforcing the case for a cautious tactical outlook on European assets. Orders fell 1.0% m/m, slowing to 0.8% y/y on a calendar-adjusted basis from 6.1% in May. The…

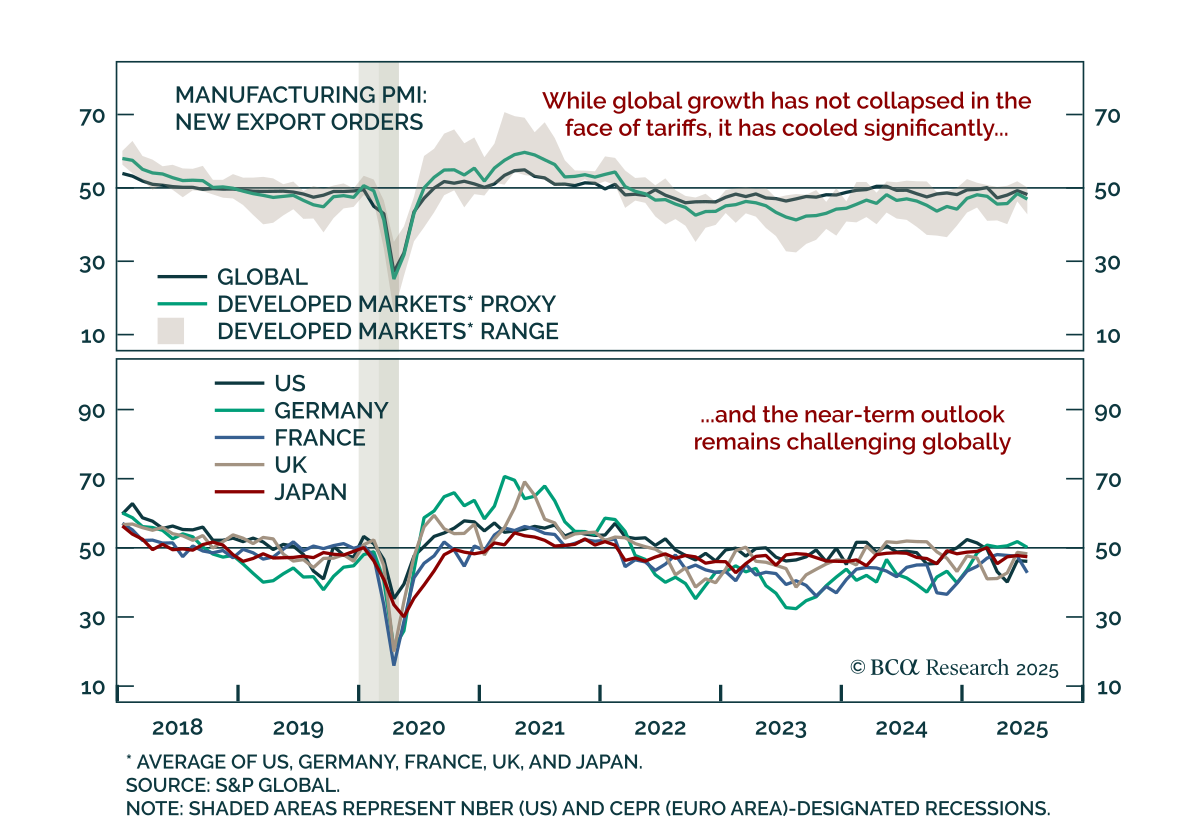

In response to trade uncertainty, global growth is cooling but not collapsing, supporting a cautious near-term view on risk assets. Trade disruption earlier this year raised fears of a global recession, but the data so far point to deceleration, not…

Our Commodity strategists recommend staying short LME copper outright and long gold/short LME copper on a cyclical basis. The unwind in copper, set off by the US tariff exemption on refined metal, is not yet complete. An inventory overhang in the US will…

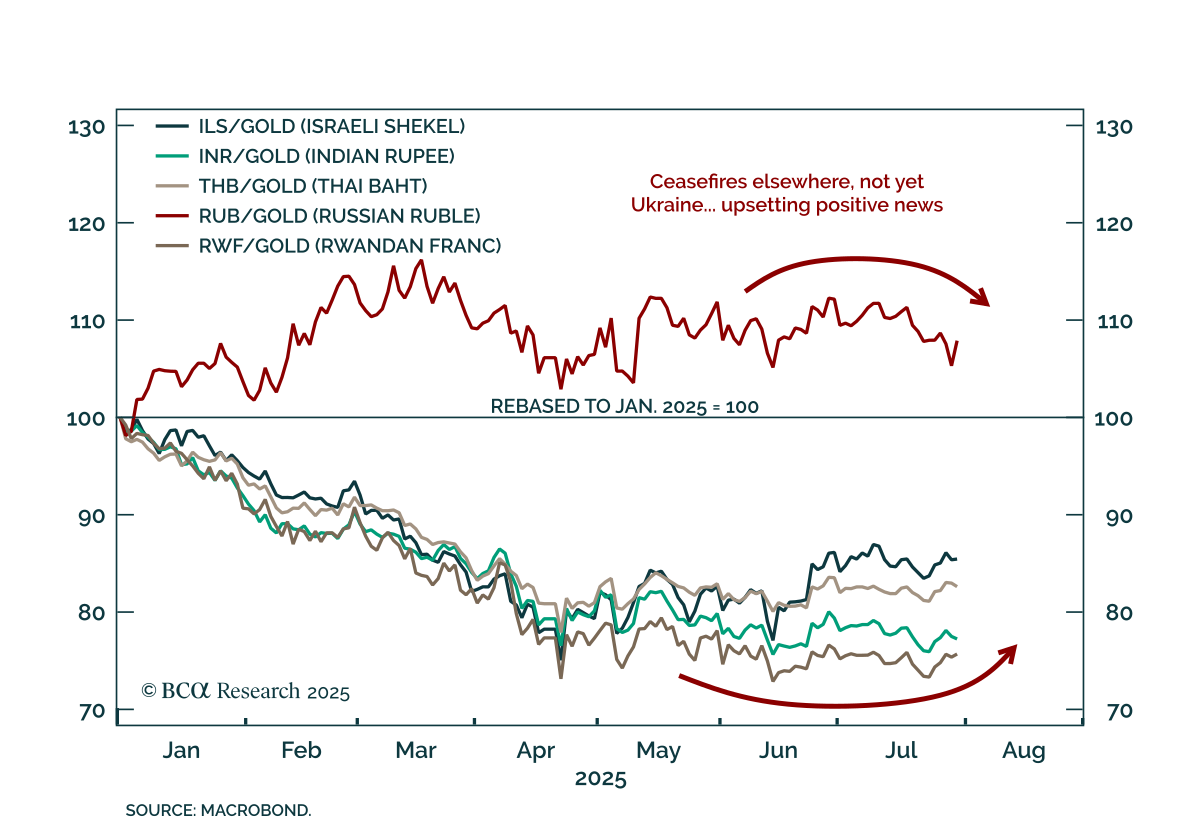

BCA’s US Political strategists warn that Russia presents an immediate market risk, with near-term pullbacks offering potential buying opportunities. President Trump is pivoting toward ceasefires and trade deals, supported by approval ratings and electoral…

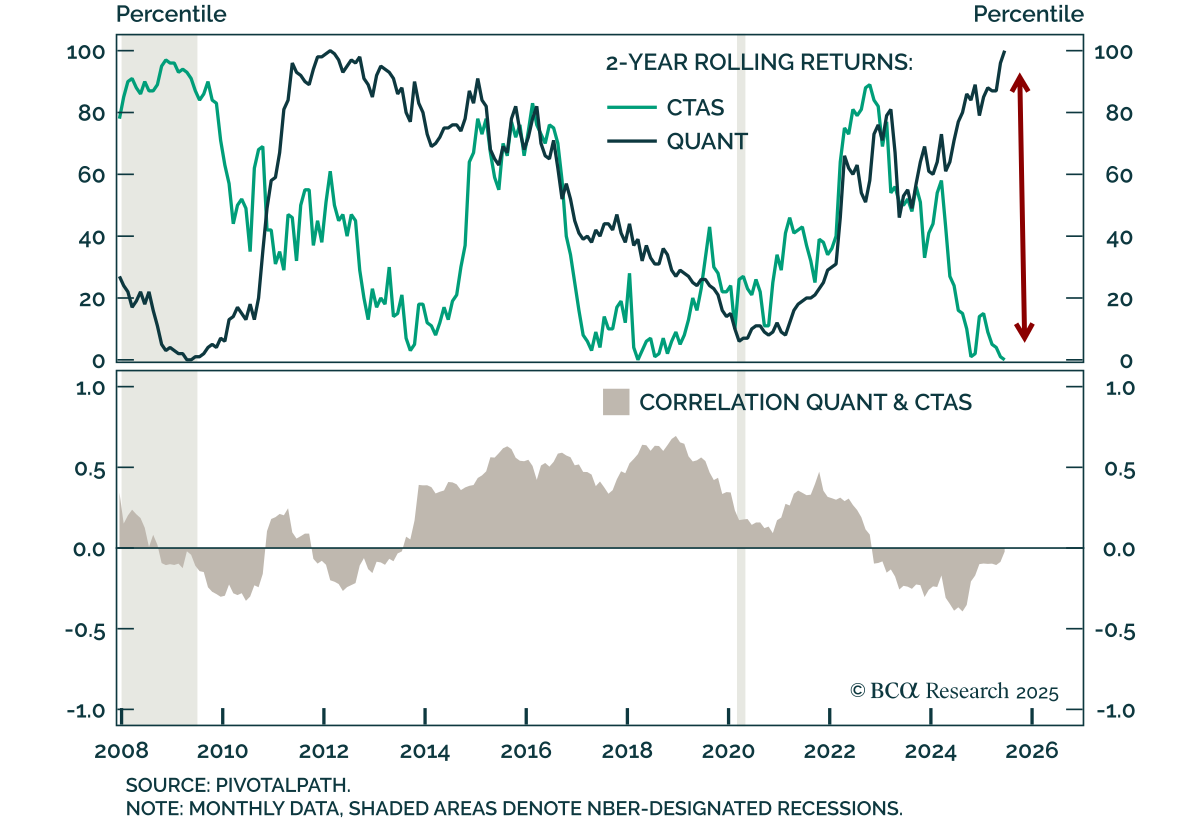

A historic divergence between systematic strategies is creating a compelling entry point into Managed Futures. Our Chart Of The Week comes from Brian Payne, Chief Strategist for our Private Markets & Alternatives team.In their…