Global

This week, we review our currency positions, based on the latest data from G10 economies.

According to BCA Research's Commodity & Energy Strategy service, Qatar will be the winner as it takes advantage of the global energy transition towards renewables and the world fragments under economic and military competition. Qatar recently…

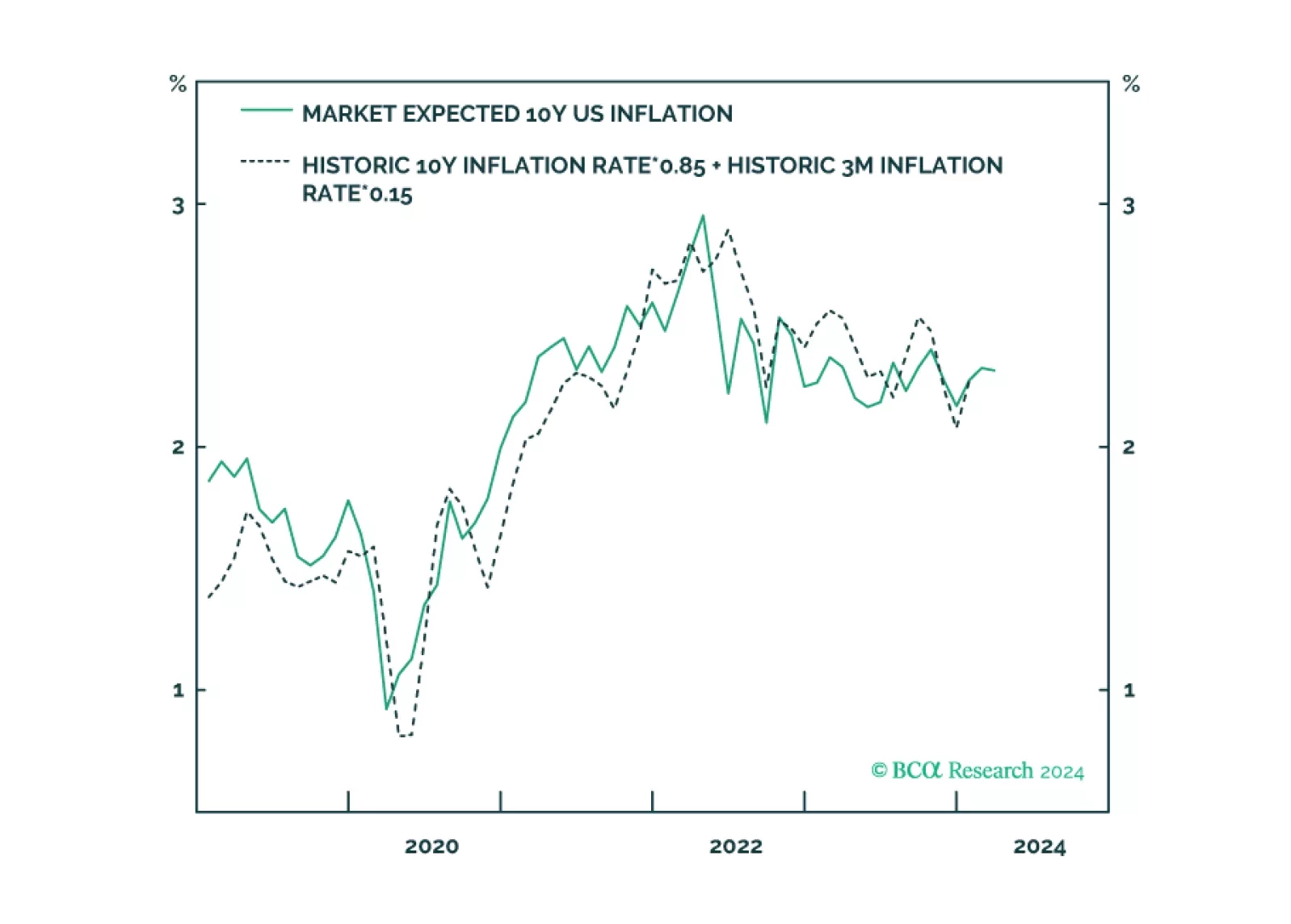

Expected inflation has surged to its highest level in a year. This has surprised many people, but expected inflation is behaving just as expected. Expected inflation is not a prophecy, it is just a mathematical function of delivered inflation. We discuss what this means for central banks in the US, UK, euro area, and Japan. Plus: bitcoin’s structural uptrend to $100,000+ is still intact.

The stock market of the Eurozone’s largest economy keeps grinding higher with the DAX 40 closing at new highs last week. Since its October low, the index of German blue-chip companies advanced by 20%. Does this rally have legs? On a relative basis,…

The JPM Global Manufacturing PMI improved from 50.0 to 50.3 in February, indicating that global manufacturing activity is growing again after having contracted for 18 months. Notably, new orders expanded from previously contracting levels (from 49.8 to…

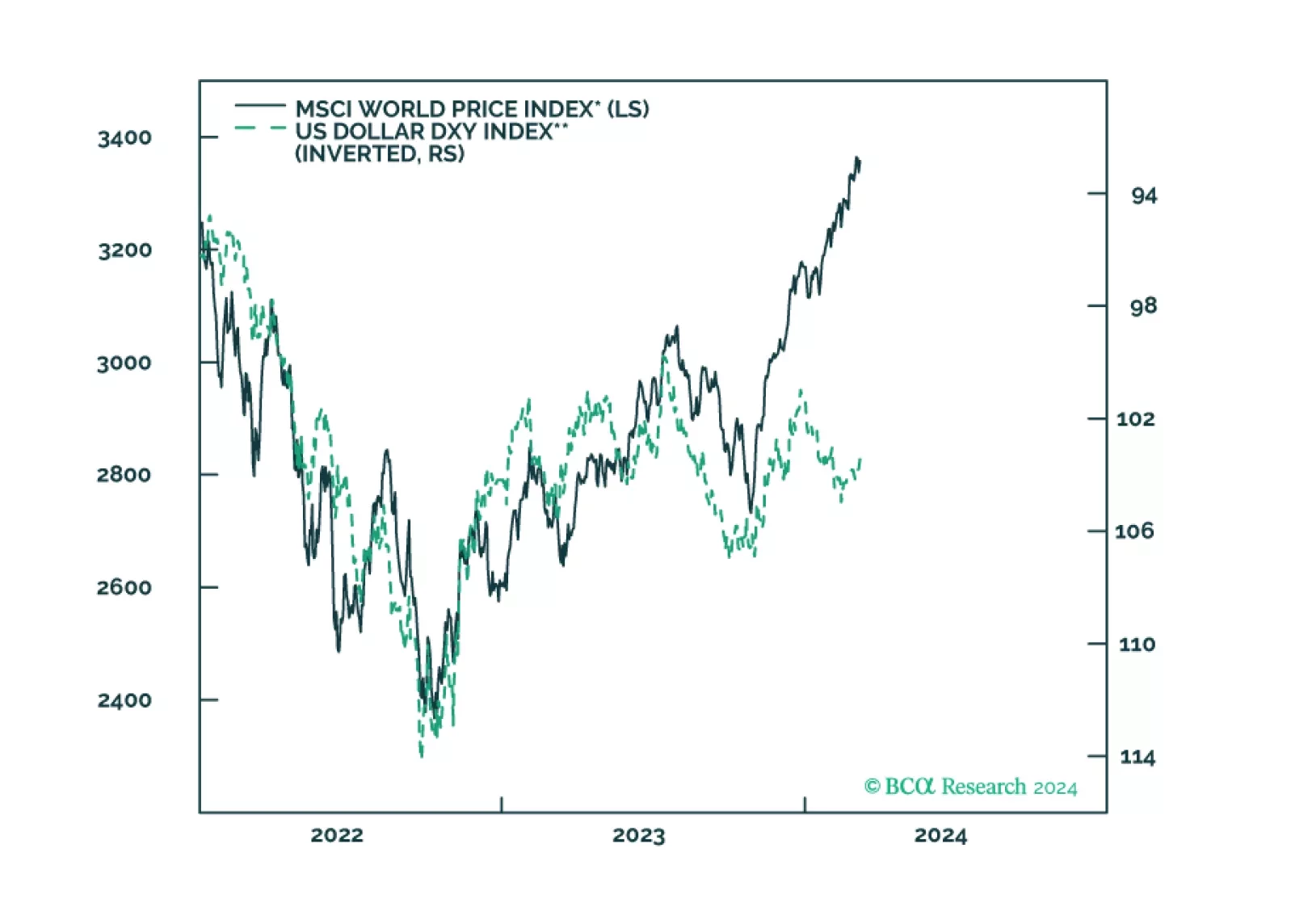

The global equity rally – which fizzled at the start of the year – picked up steam again in February with nearly all major regions posting above average returns. After having underperformed last year, Chinese stocks led their global counterparts in terms of…

According to BCA Research’s Geopolitical Strategy and The Bank Credit Analyst services, trade policy under a second Trump presidency represents the greatest cyclical risk to investors. In 2018, the Trump administration’s trade war with China and several…

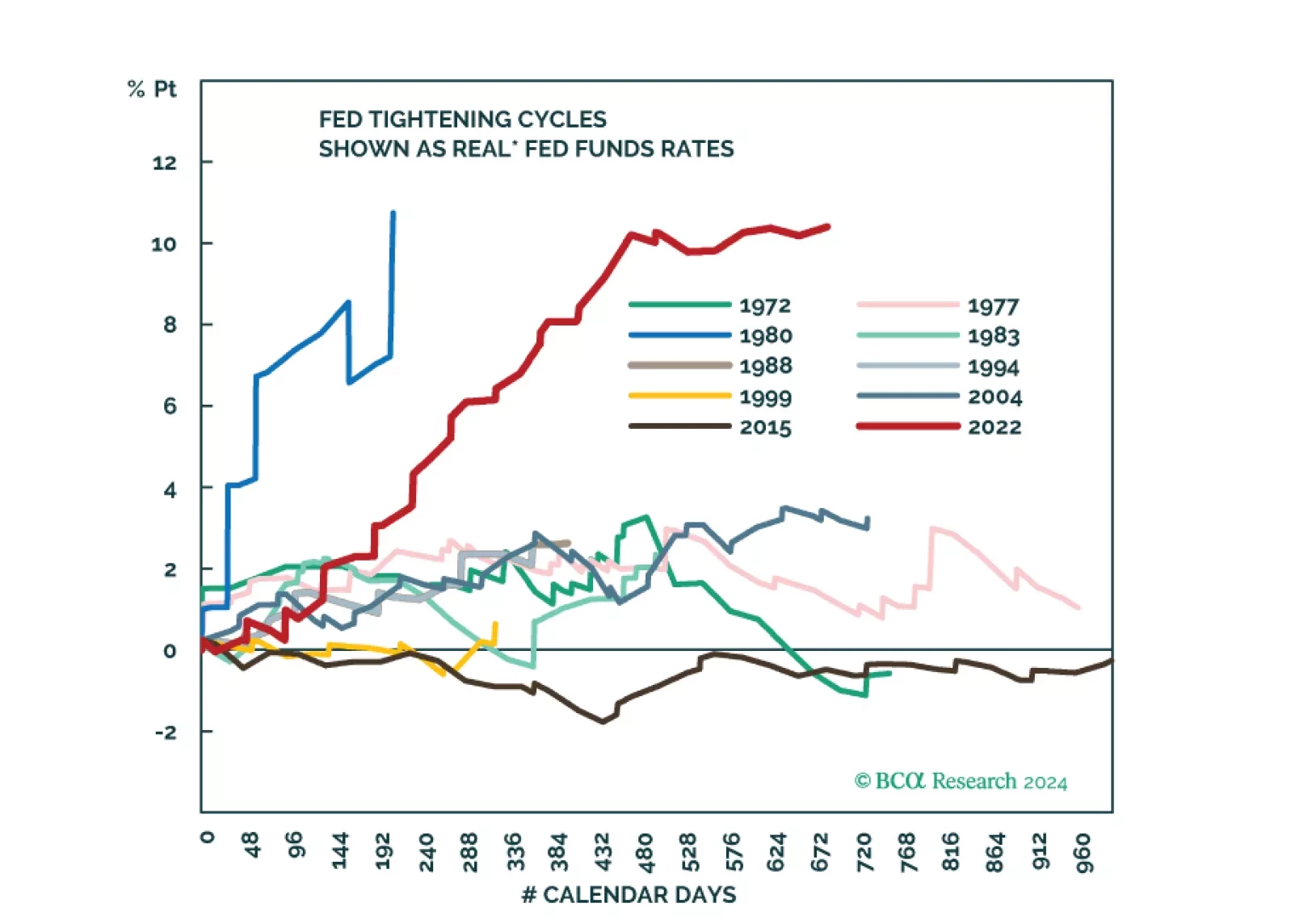

Amid patchy global growth, the US economy remains resilient. However, tight monetary policy will eventually trigger a recession in the US too. The stock market rally has been very narrow. Stay underweight risk assets.

The MSCI ACW Growth index continues to strengthen vis-à-vis the Value index, outperforming the latter by 4.7 percentage points year-to-date, following 23.3 percentage points in 2023. Given that the IT, Consumer Discretionary, and Communication Services…

On the surface, the latest Taiwanese export orders release delivered a positive signal on the global trade cycle. The 1.9% y/y expansion in January marks a significant improvement from the 16.0% contraction in December. Moreover, a 28% surge in orders from…