Global

The commodity complex performed exceptionally poorly last year. Industrial metals and crude oil were among the few major financial assets we track that posted negative z-scores in 2023. Indeed, the 12% drop in the Golman Sachs Commodity Index in 2023 follows…

Following a strong rally in the prior two years, the performance of the US dollar was significantly weaker in 2023. The DXY index ended last year down 0.9%, after gaining 3.3% and 6.4% in 2021 and 2022, respectively. Importantly, the USD weakness was…

The dollar has kicked off 2024 on a tear. The closely followed DXY index bottomed on Thursday December 28th, and has since risen almost 2%. Year-to-date, the only major currency that has held up against the dollar is the Mexican peso, with the yen continuing…

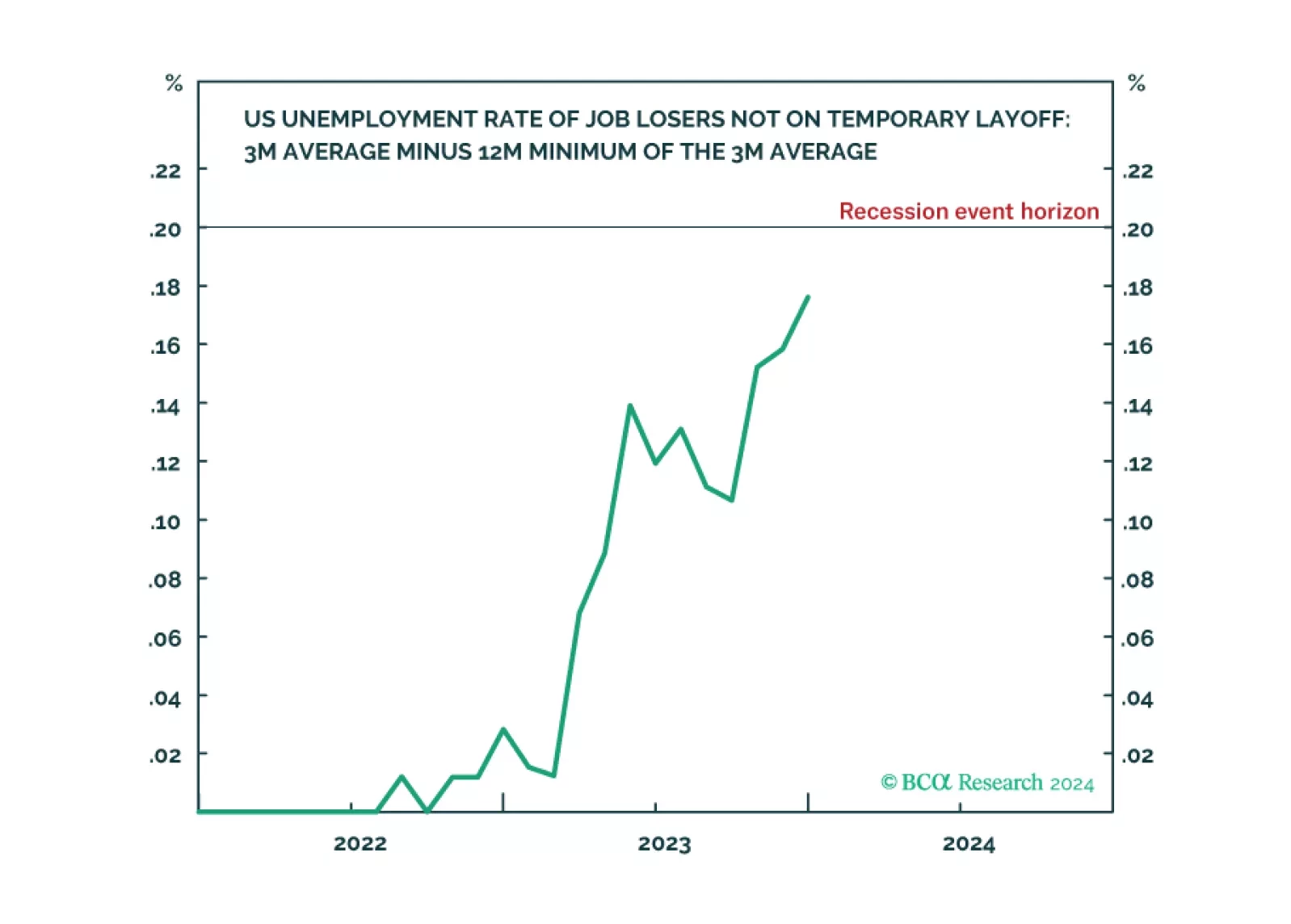

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

China’s equity market stands out as a major underperformer vis-à-vis its global peers in 2023. The 13% drawdown in China’s investable stock price contrasts with the 20% rally in the MSCI ACW Index. It reflects the country’s disappointing recovery as…

The AI craze was the dominant force driving difference in equity sector returns in 2023. Broadly-defined technology sectors were the top three outperformers last year with IT, Communication Services, and Consumer Discretionary soaring by 50%, 36%, and 28%,…

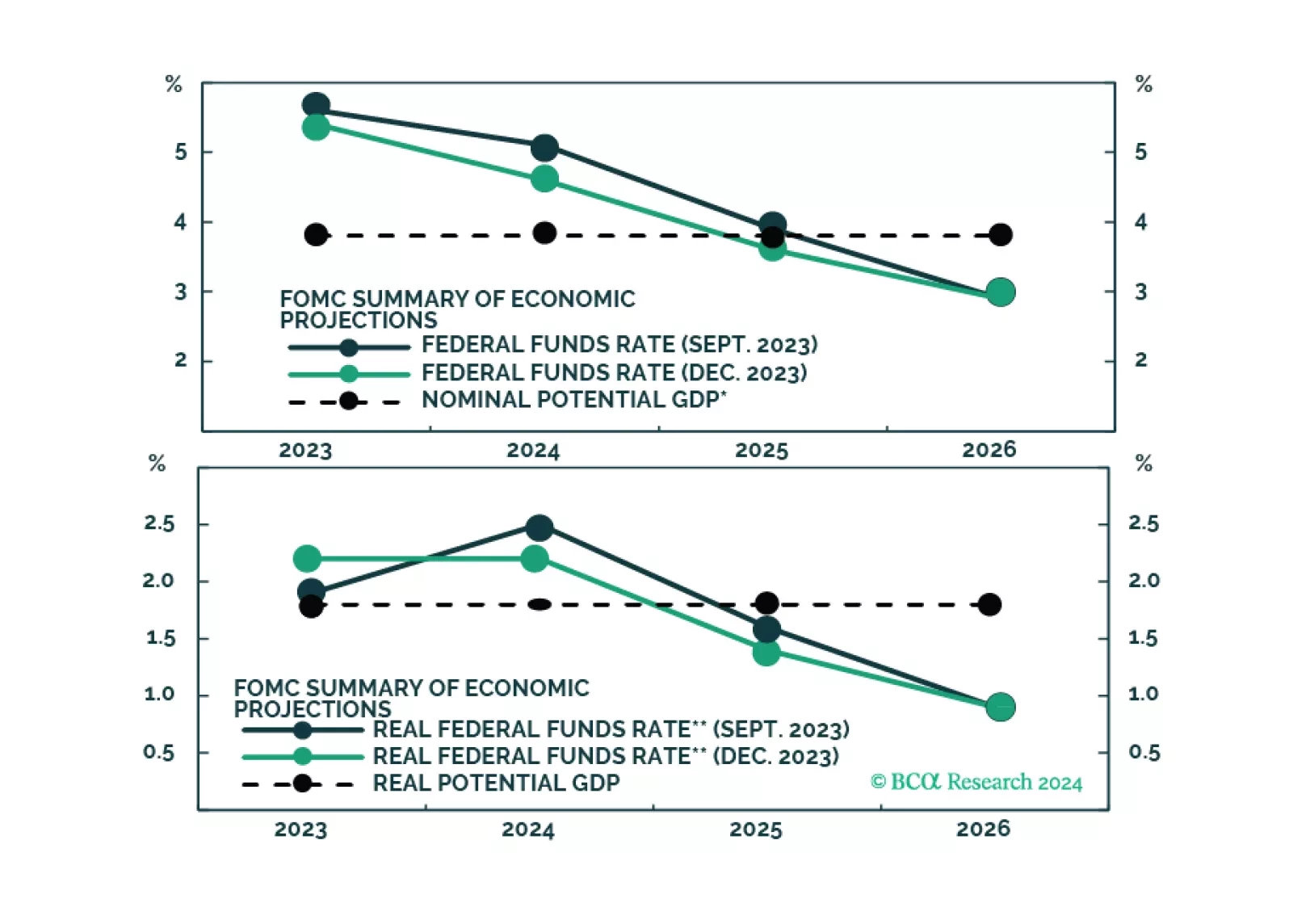

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

December PMIs indicate that the global manufacturing sector is not experiencing a meaningful rebound. The Global Manufacturing PMI declined from 49.3 to 49.0 in December, marking the sixteenth consecutive month of a sub-50 reading. The output, new orders,…

2023 was an unexpectedly good year for global financial markets. Most of the major financial assets we track generated positive abnormal gains. Although US stocks outperformed their global counterparts, Eurozone, Japanese, and EM ex-China equities led in…

Global financial markets ended 2023 on a positive note, delivering a second consecutive month of exceptional gains in December. Fixed income once again led in terms of abnormally large returns on the back of increased expectations of Fed rate cuts in 2024.…