Global

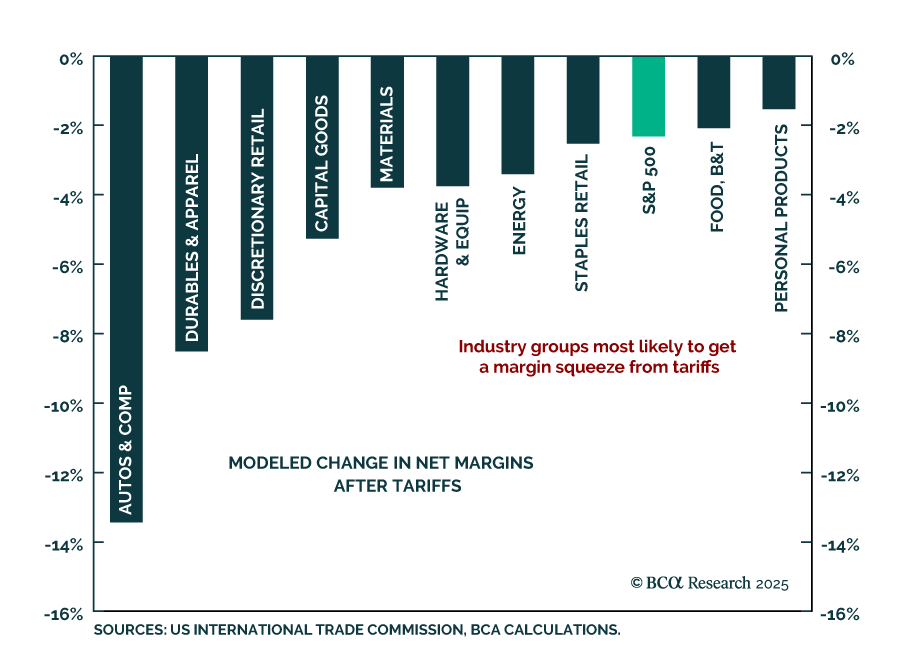

Our US Equity strategists warn that tariffs will meaningfully compress S&P 500 margins, with little pricing power to offset rising input costs. A two-point hit to net margins and falling multiples will drive earnings downgrades and negative forward…

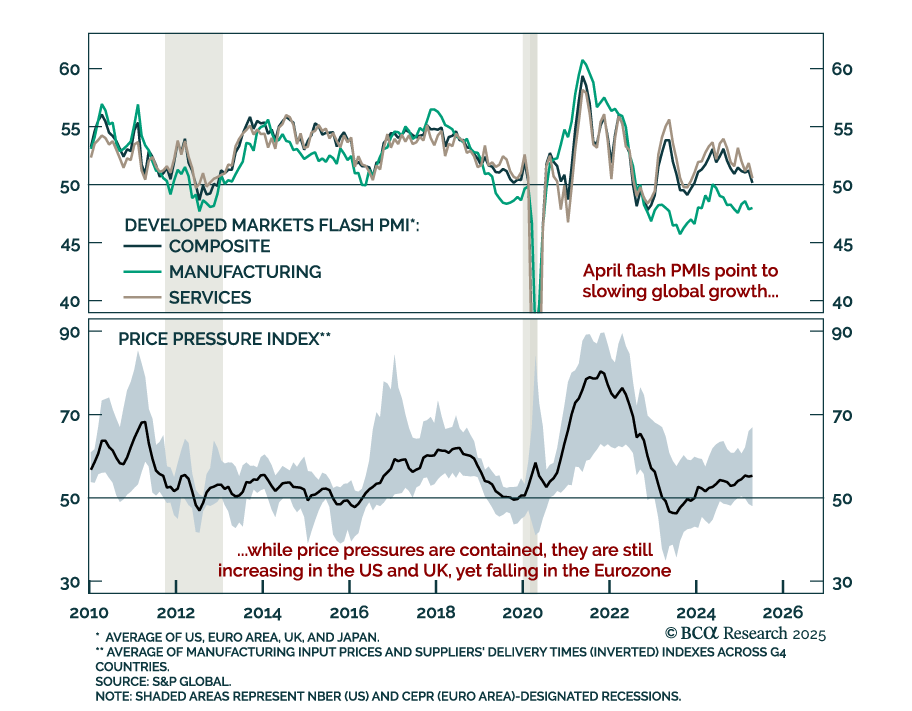

April PMIs confirm global growth is stalling, reinforcing our overweight in government bonds and underweight in risk assets. Services witnessed the worst deterioration, but manufacturing is still contracting even if broadly stable. This mirrors recent US…

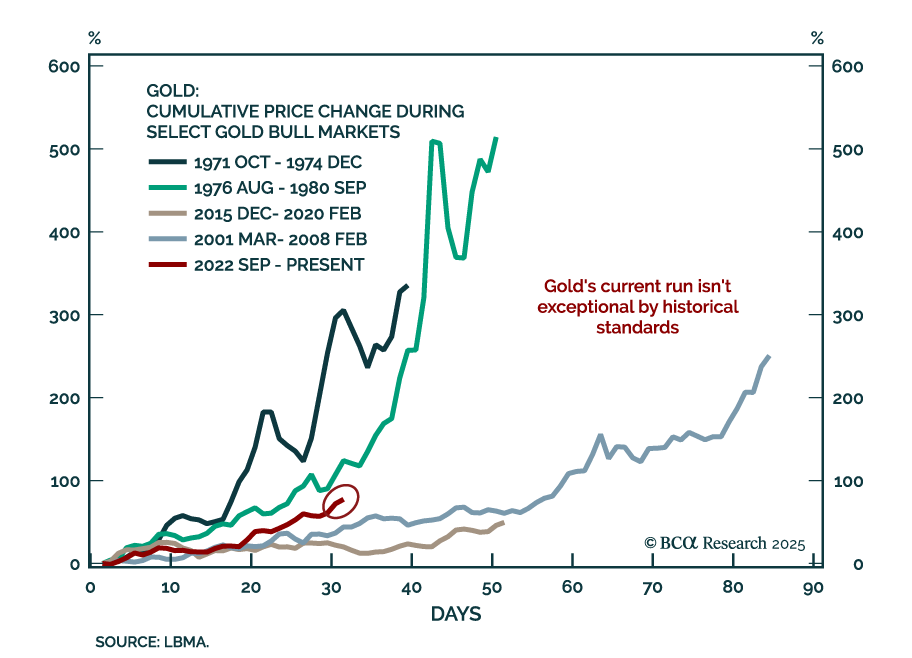

Our Commodity strategists remain defensive as both demand- and supply risks abound. Stay long gold and underweight oil and copper as increasing OPEC+ supply and tariff-driven demand risks will hurt energy and industrial metals prices. The motivations…

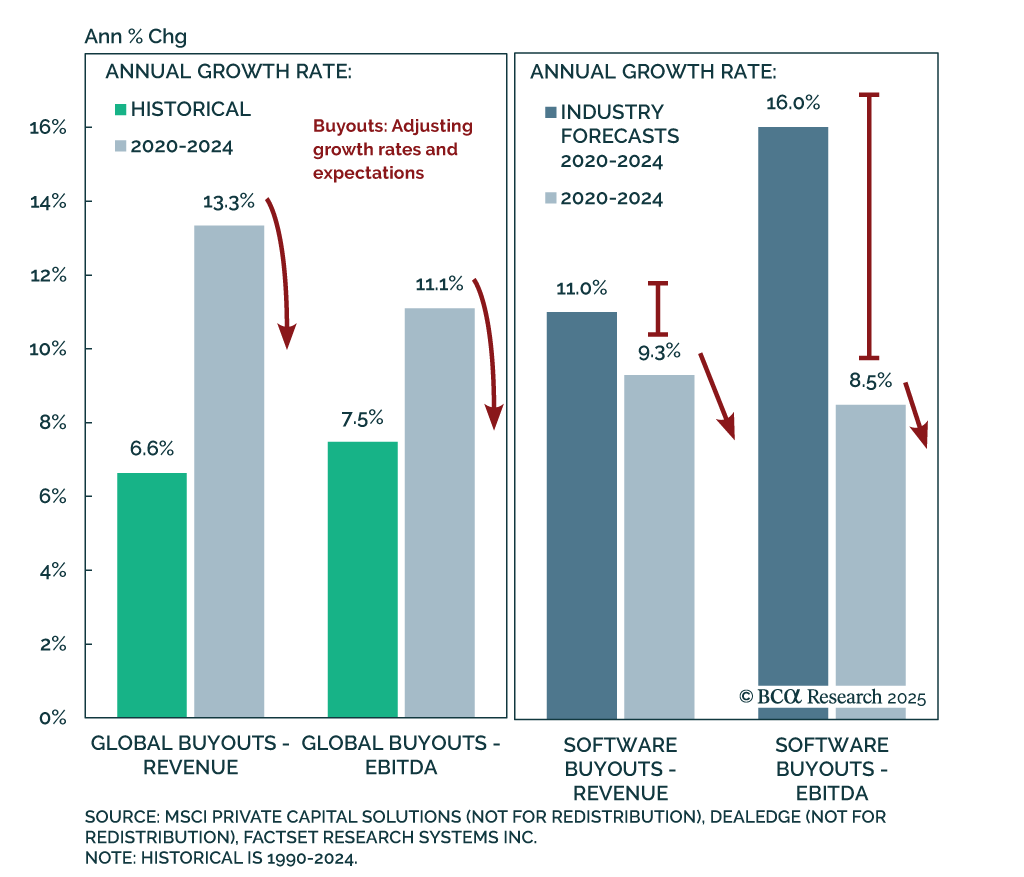

Our Private Markets & Alternatives strategists remain positioned for a downturn. Private Equity is most threatened as tariffs intensify existing recession risks. Buyout strategies face stress from record-low distributions and rising LP-GP friction.…

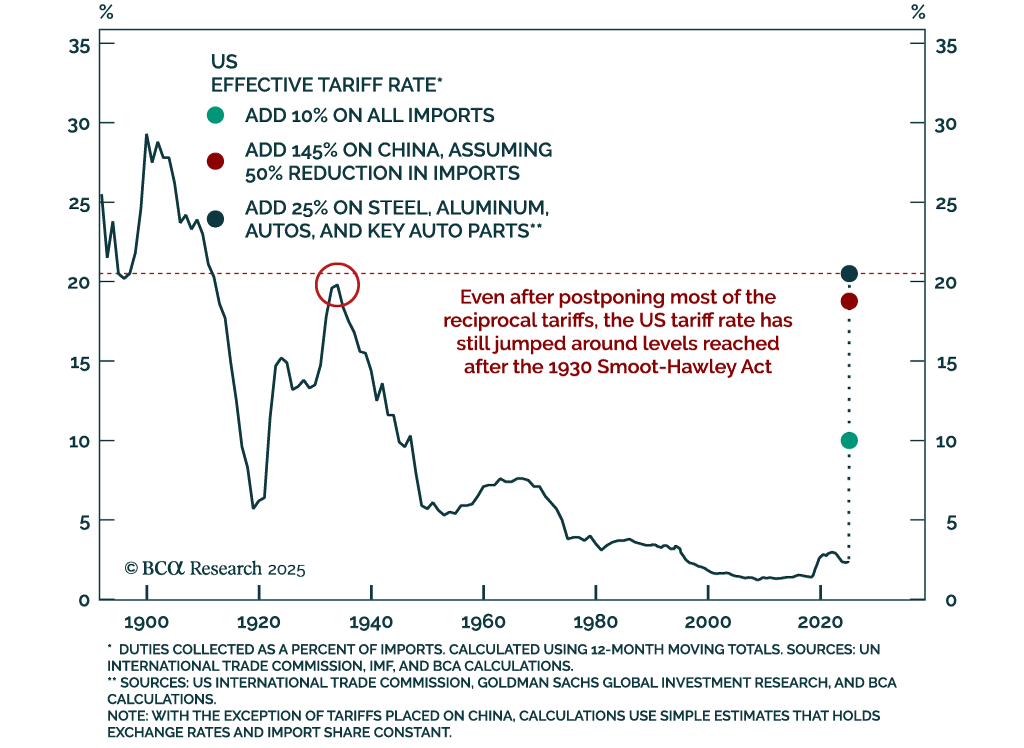

Our Global Investment Strategists remain defensive, expecting a global recession in the coming months unless the trade war de-escalates meaningfully. They maintain a year-end S&P 500 target of 4450, with downside risk to 4200.While reciprocal tariffs were…

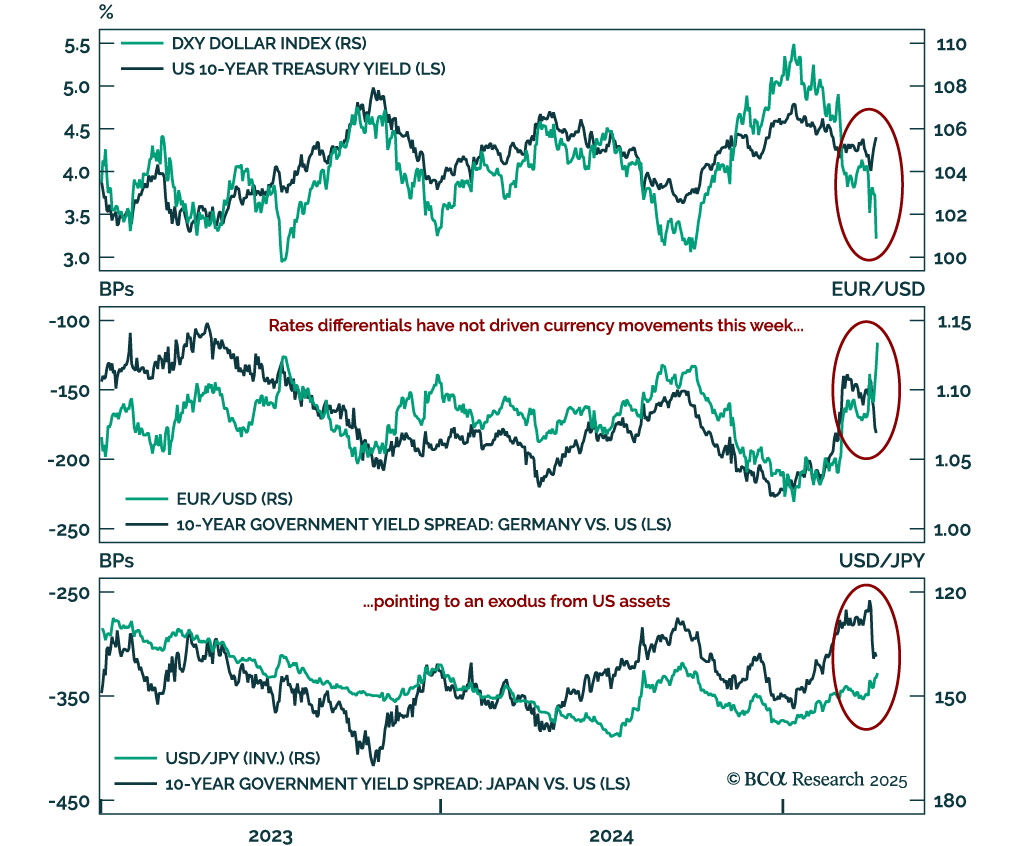

The recent breakdown in cross-asset correlations highlights mounting risk premia on US assets. Last week, the long-standing correlations underpinning our understanding of global markets violently broke down. The Treasury market turmoil had already broken the…

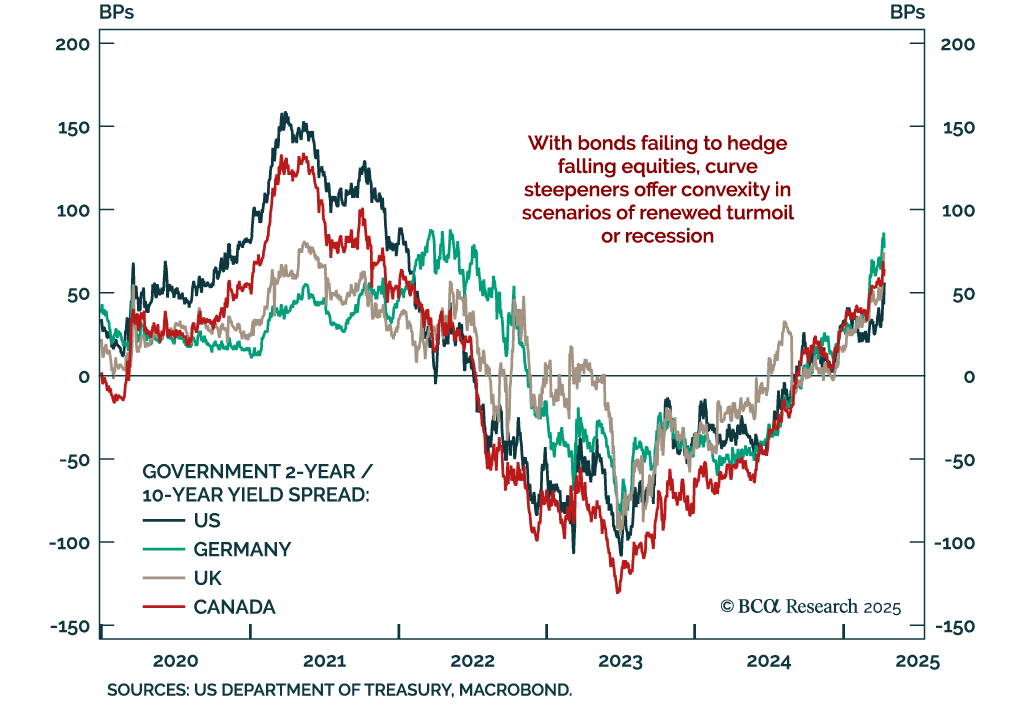

Bonds are failing to deliver defensive convexity; asset allocators should look to tactical curve steepeners for protection. Despite rising growth fears, Treasury yields have risen sharply at the long end. This is a clear break from the typical recession…

The US dollar’s reserve status is not done, but its foundations are starting to crack. Our Chart Of The Week comes from Juan Correa, Chief Global Asset Allocation Strategist. Most defensive currencies, like the yen and the Swiss franc, benefit from a positive…

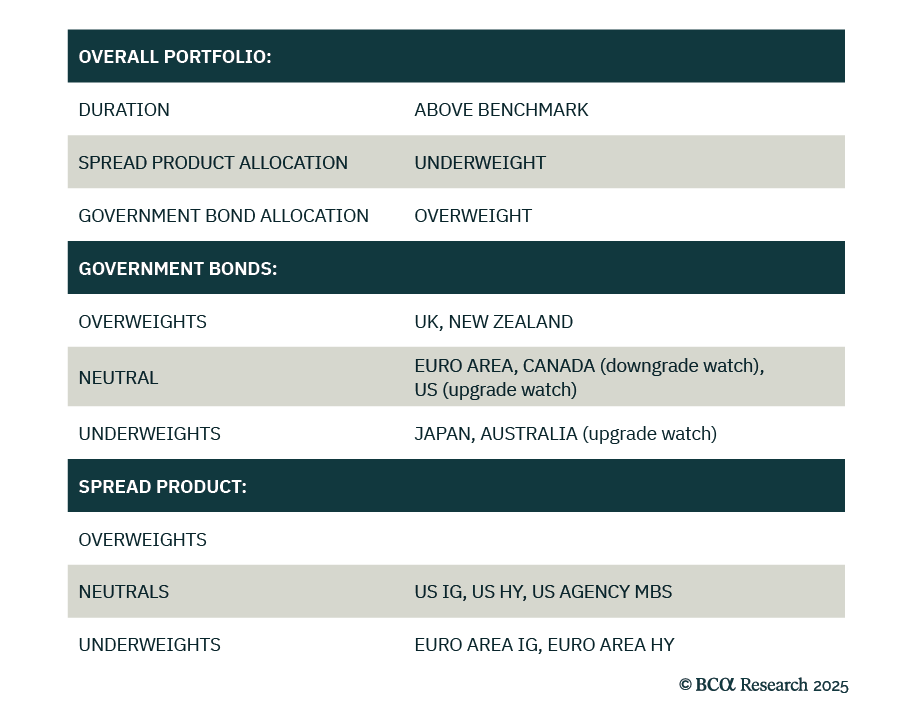

Our Global Fixed Income strategists continue to recommend long duration exposure, curve steepeners, and an underweight in corporate bonds relative to government bonds, as global recession risks rise. The trade war has increased the odds of a downturn, but the…

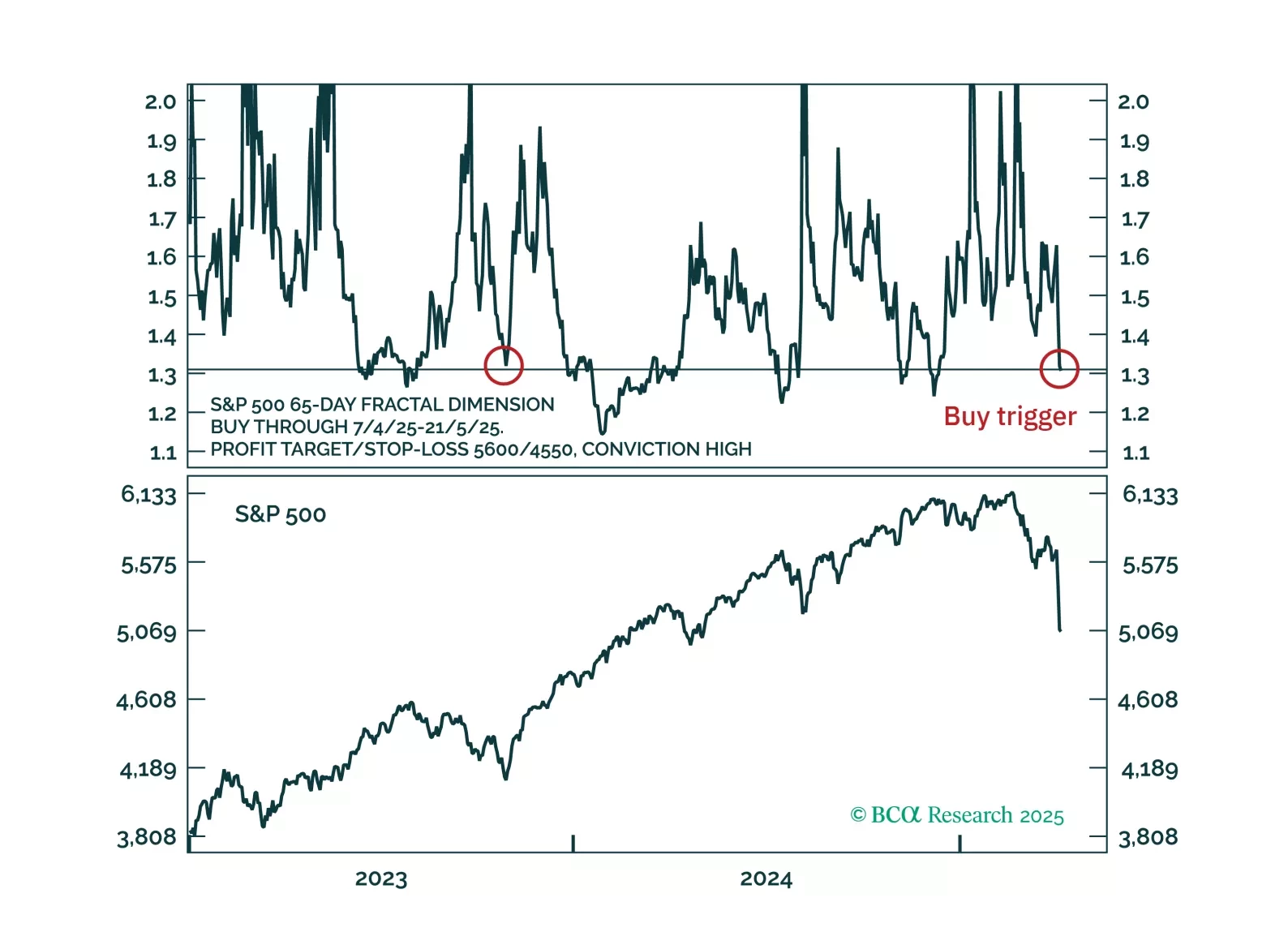

Countertrend buy triggers have been activated for the S&P 500, Nasdaq and Nasdaq versus 30-year T-bond.