Gov Sovereigns/Treasurys

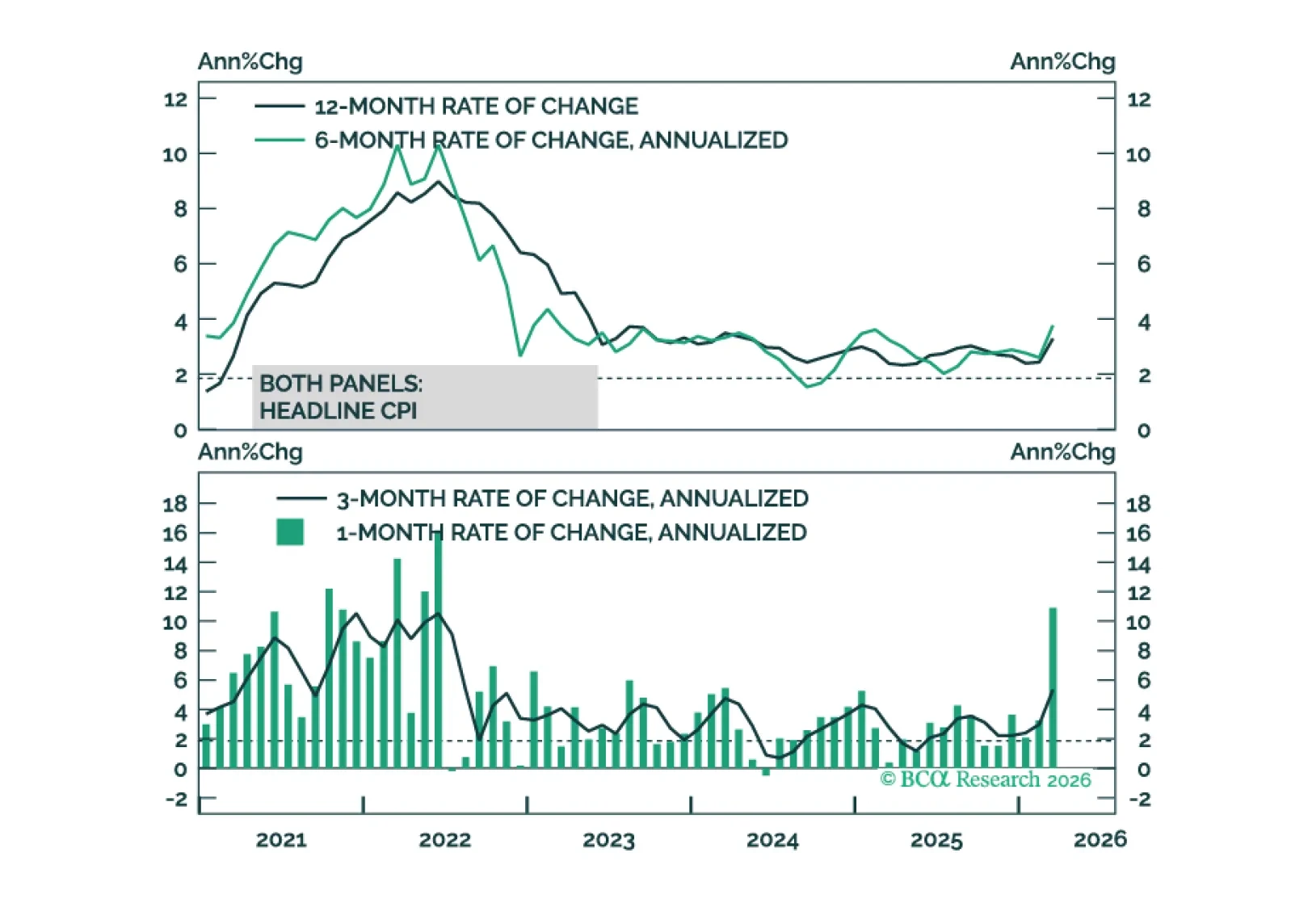

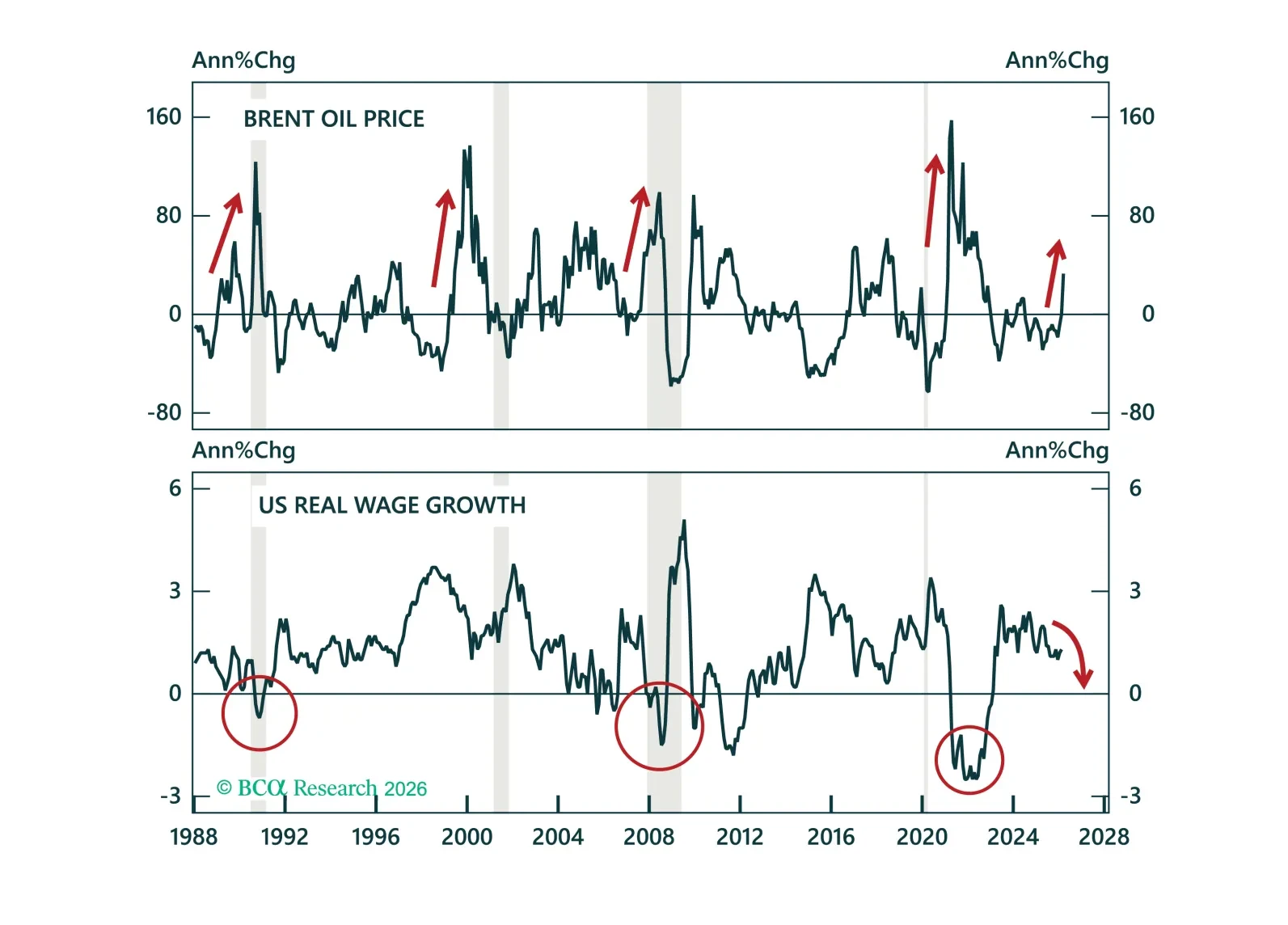

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

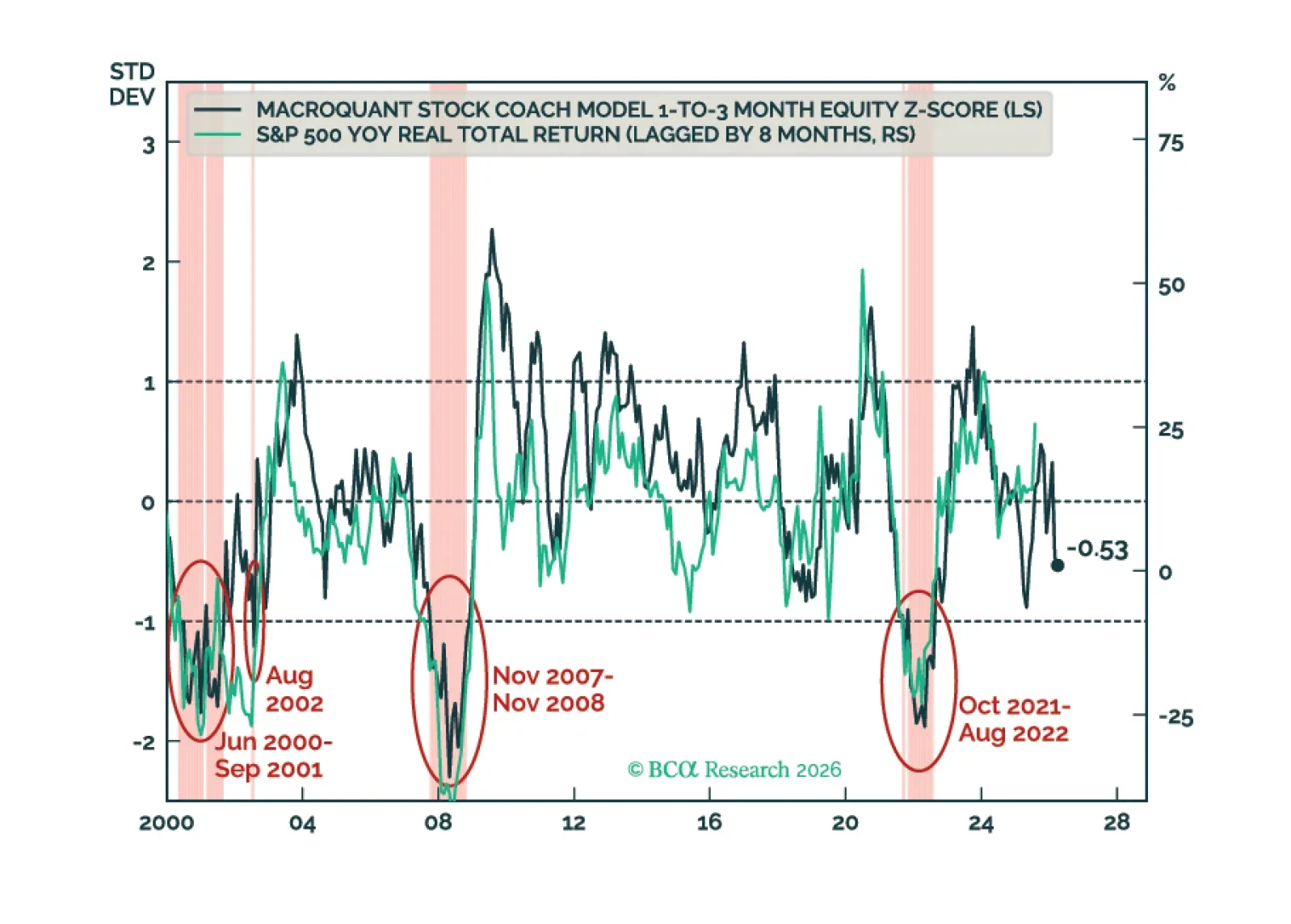

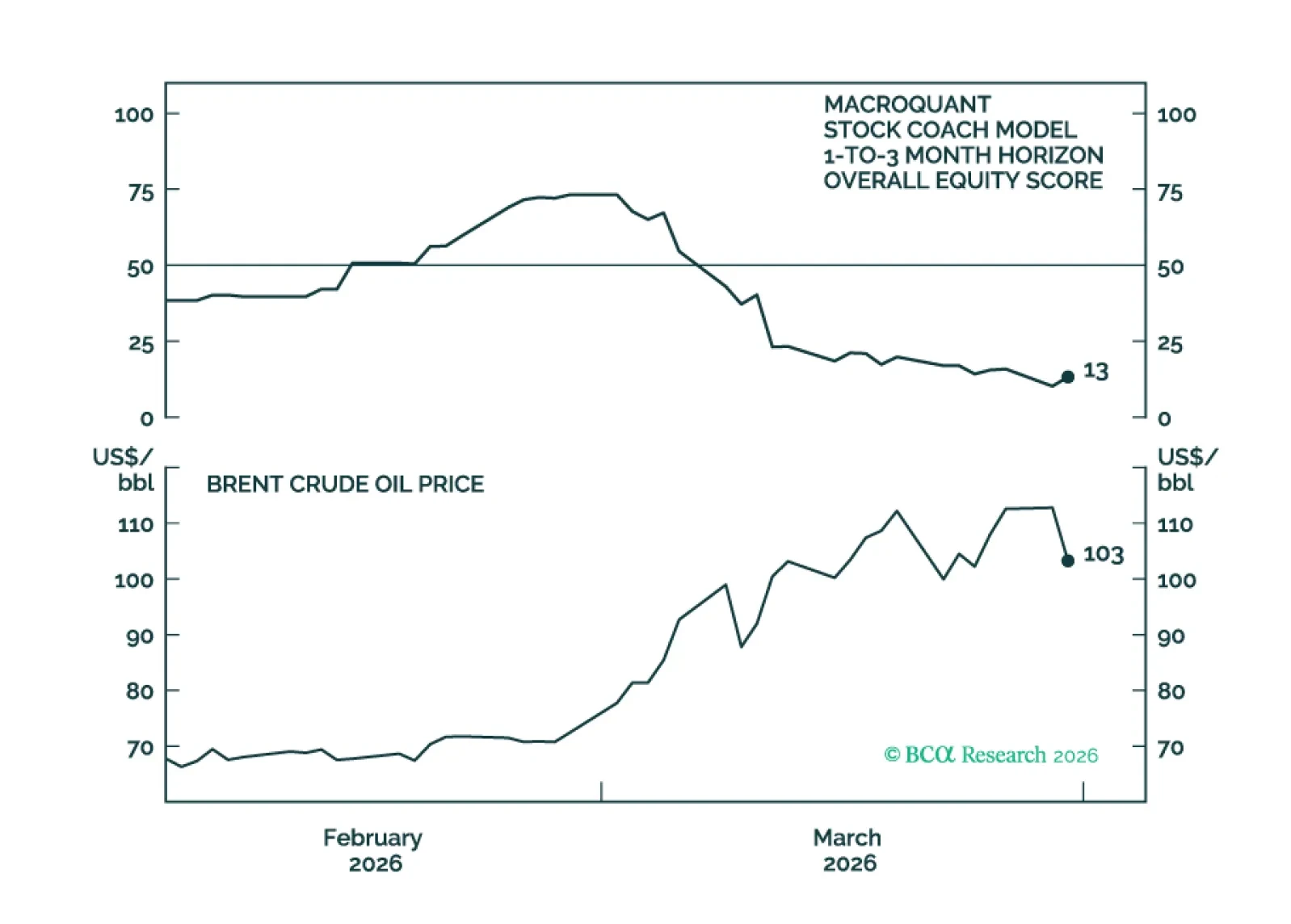

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

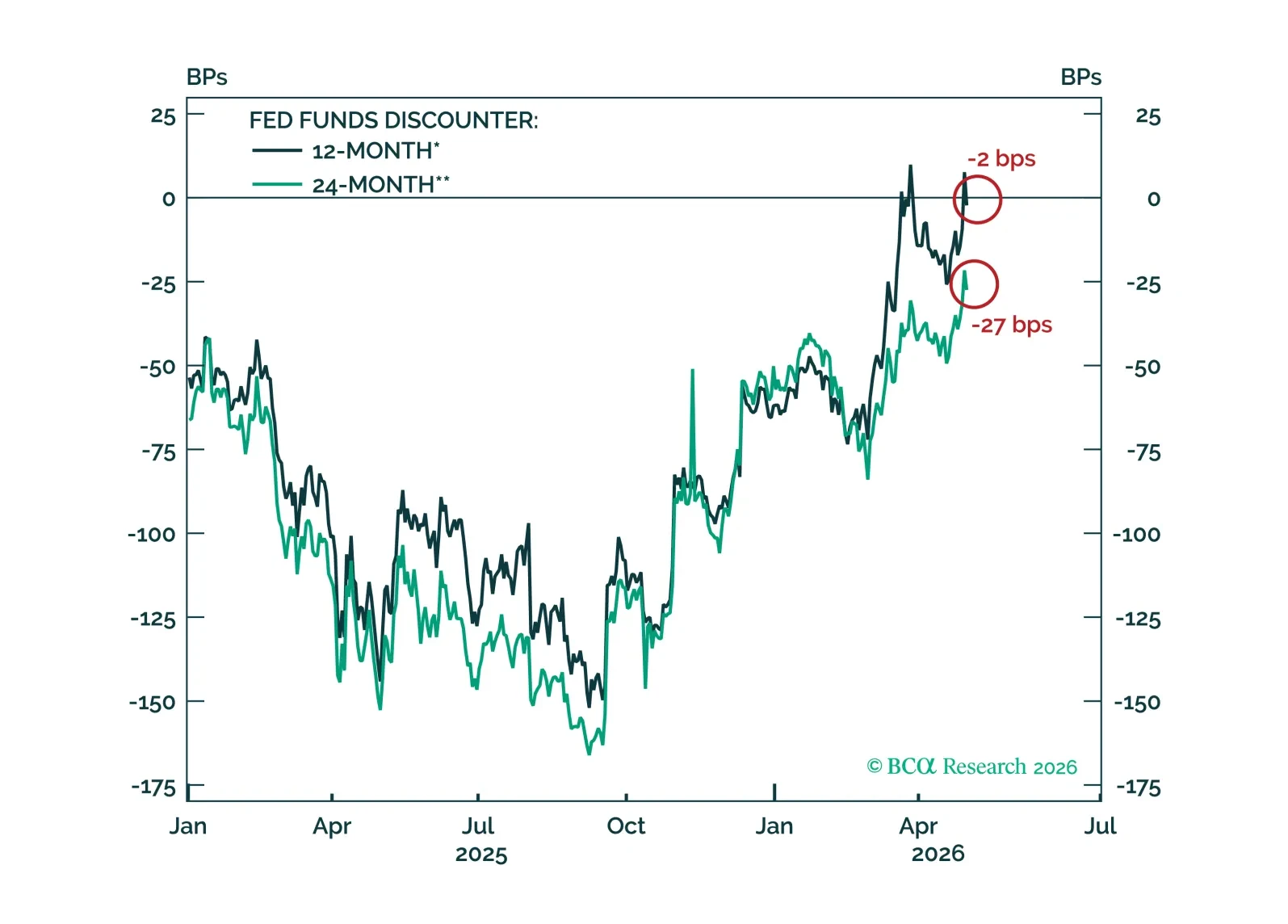

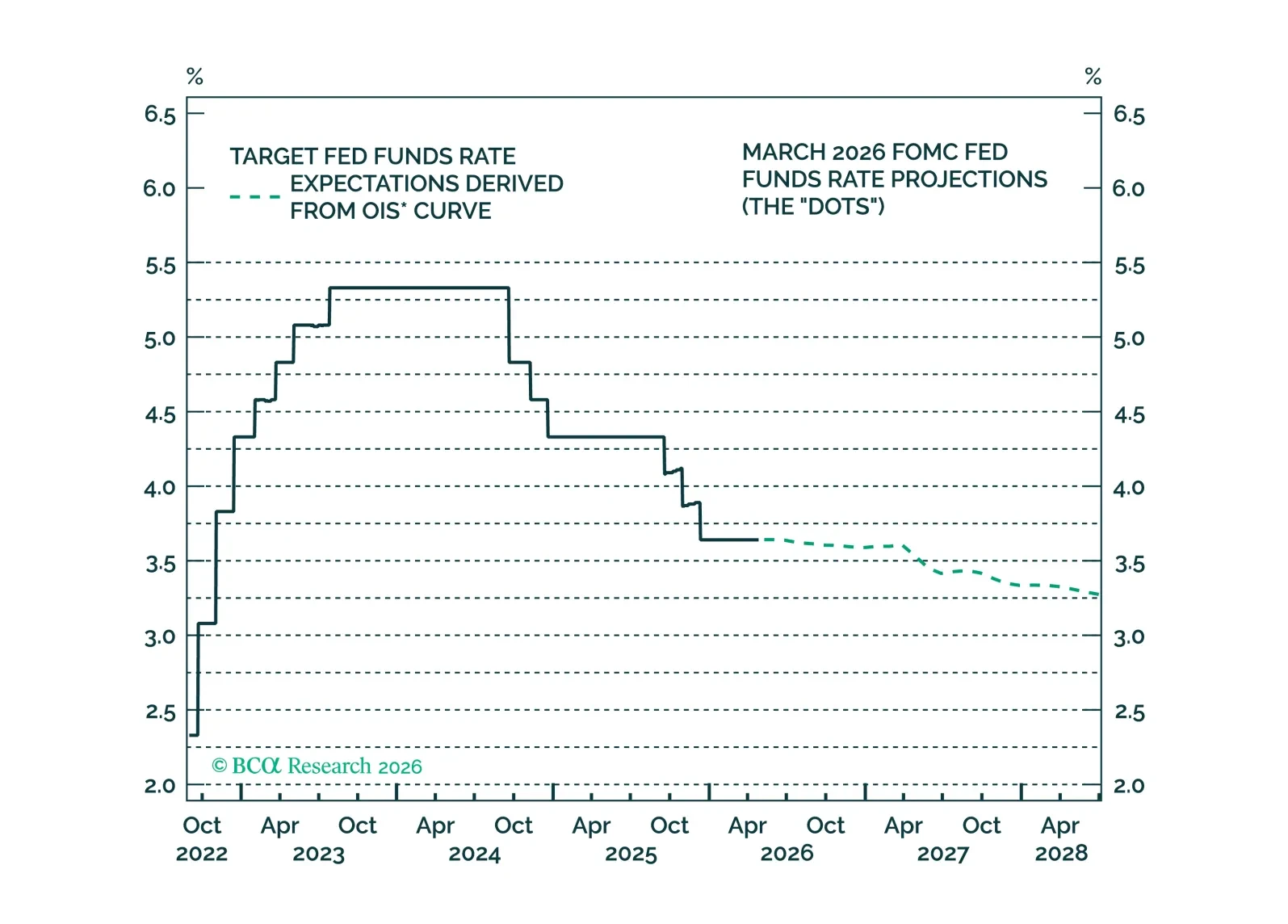

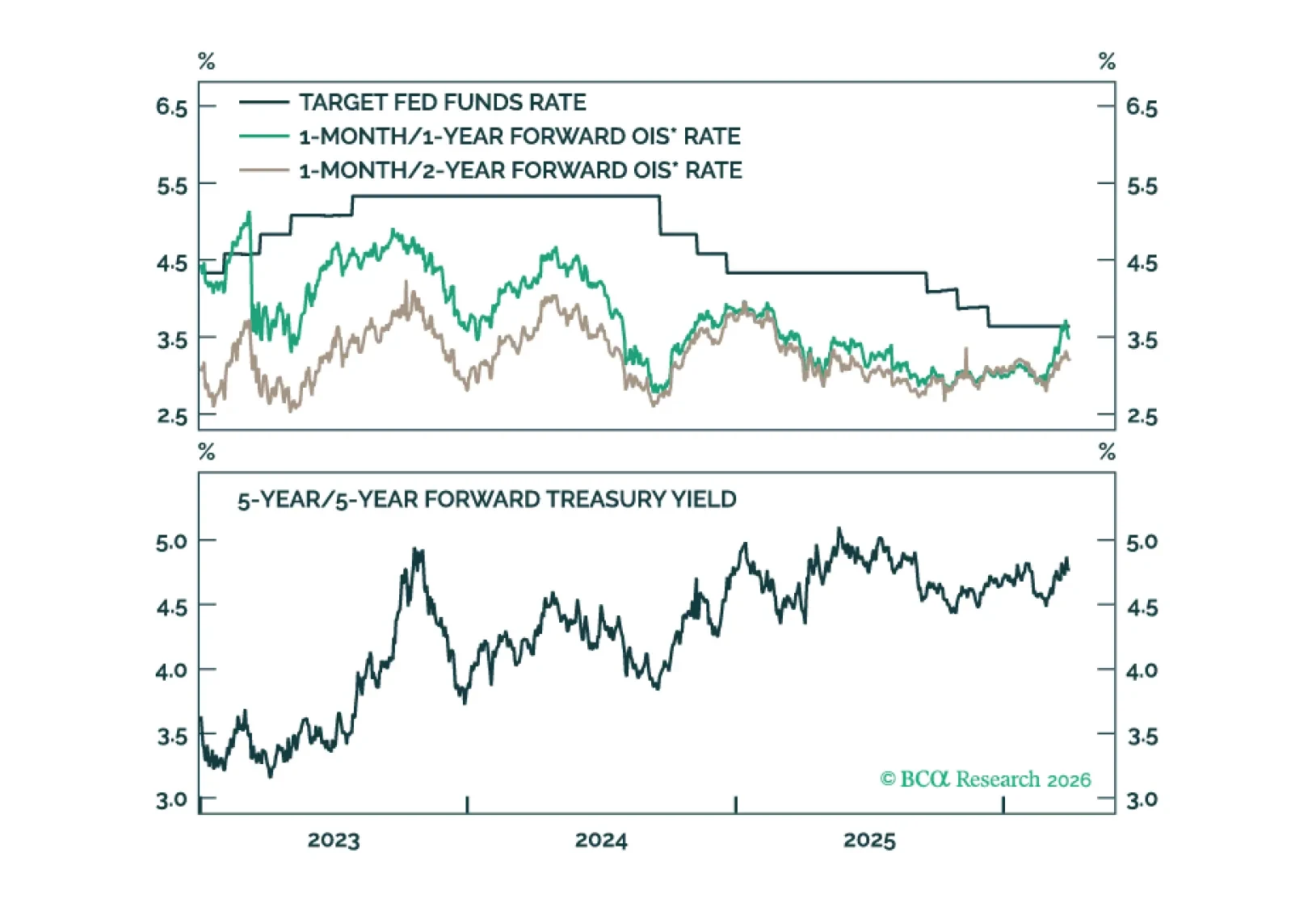

FOMC participants are coalescing around the idea that the funds rate will stay on hold for some time, an outcome that is now well priced in the bond market and that will not materially change under a new Fed Chair.

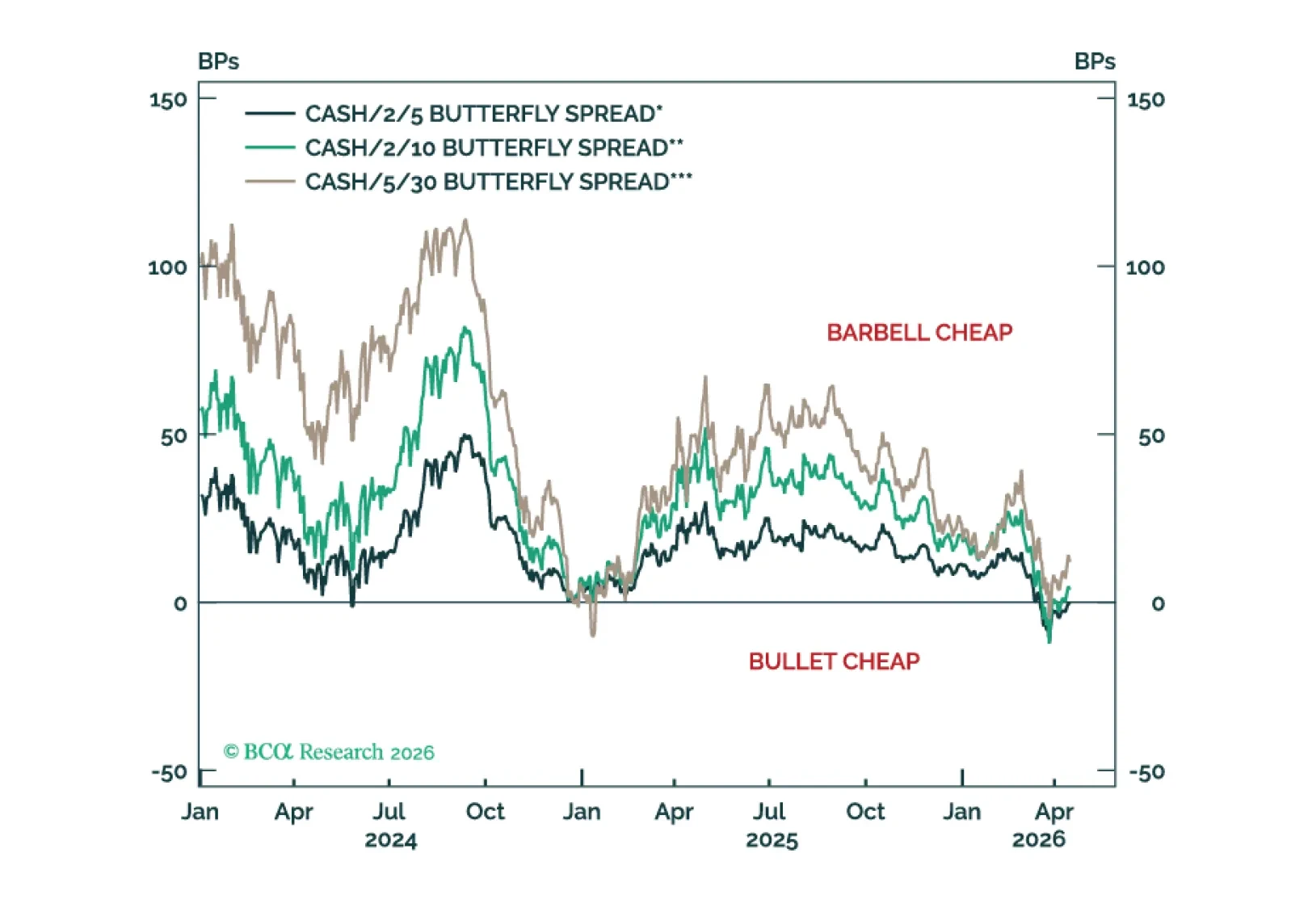

The rates market is moving back into a low vol regime, but with yields at a higher level. This argues for maximizing carry across the Treasury curve.

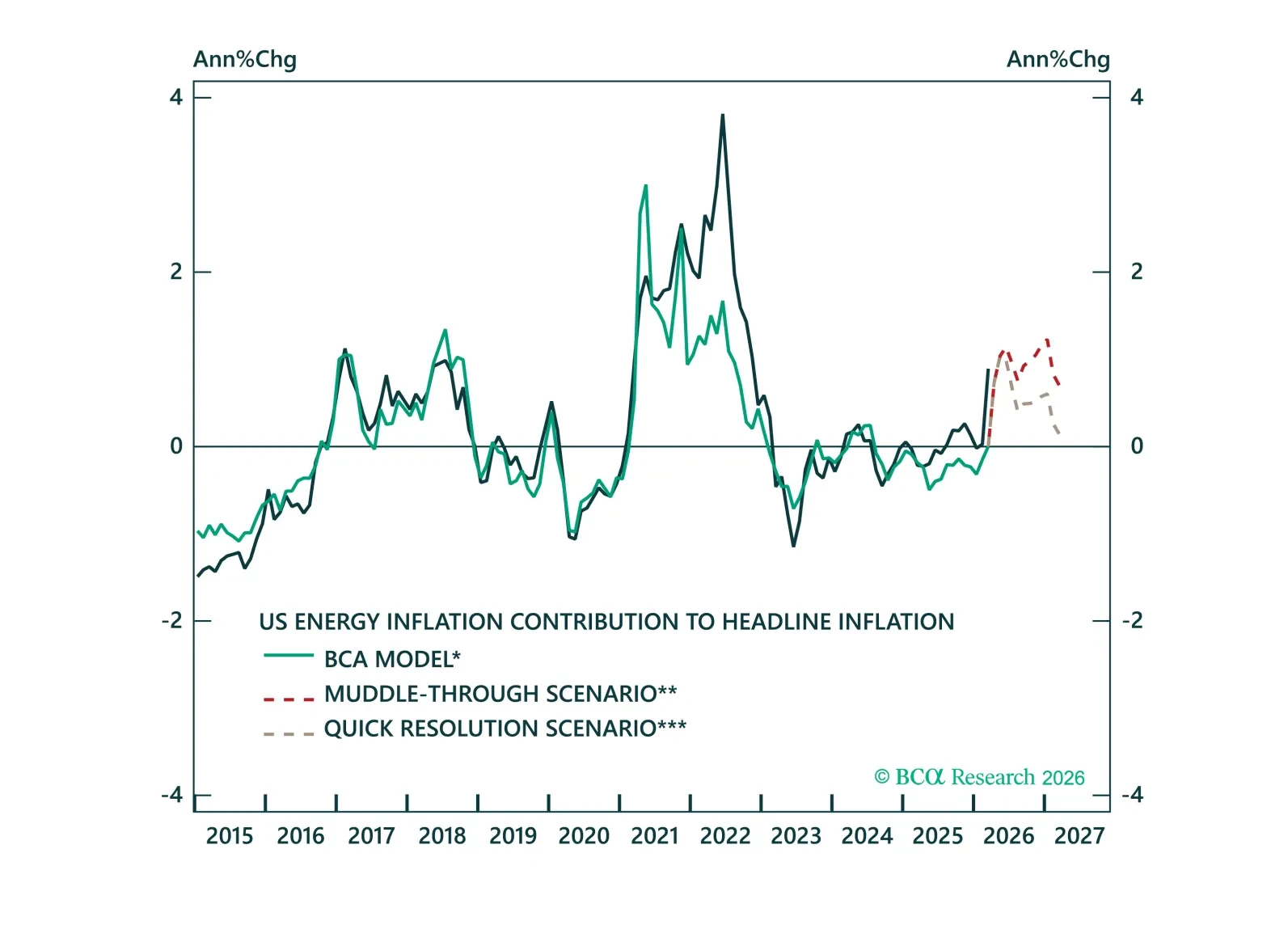

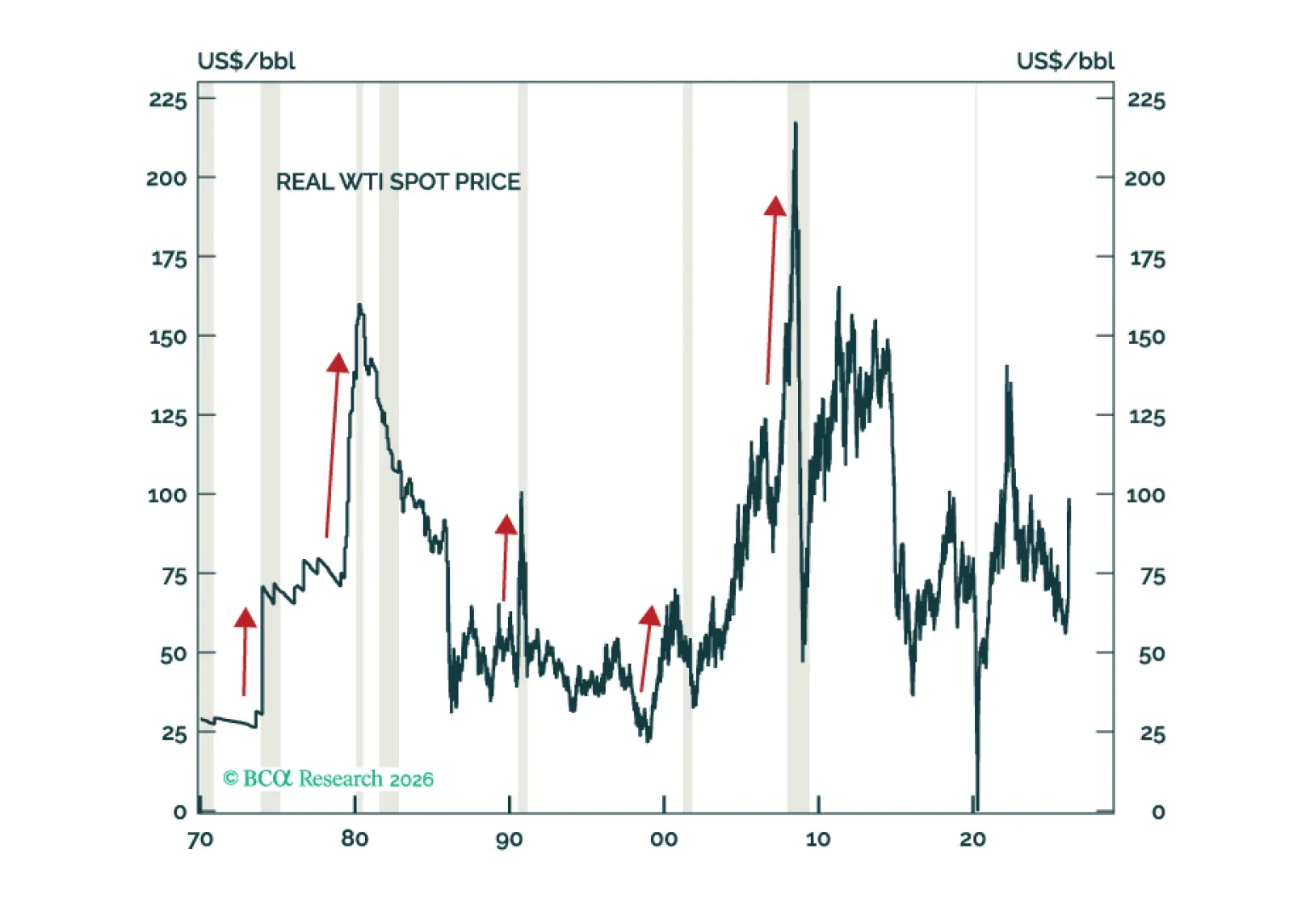

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

Inflation’s underlying trend was headed lower prior to the Iran war. This makes the recent back-up in bond yields look like an attractive buying opportunity.

Our Portfolio Allocation Summary for April 2026.

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

In today’s Strategy Insight, we show why both a quick resolution and a prolonged crisis ultimately point to lower yields.