Gov Sovereigns/Treasurys

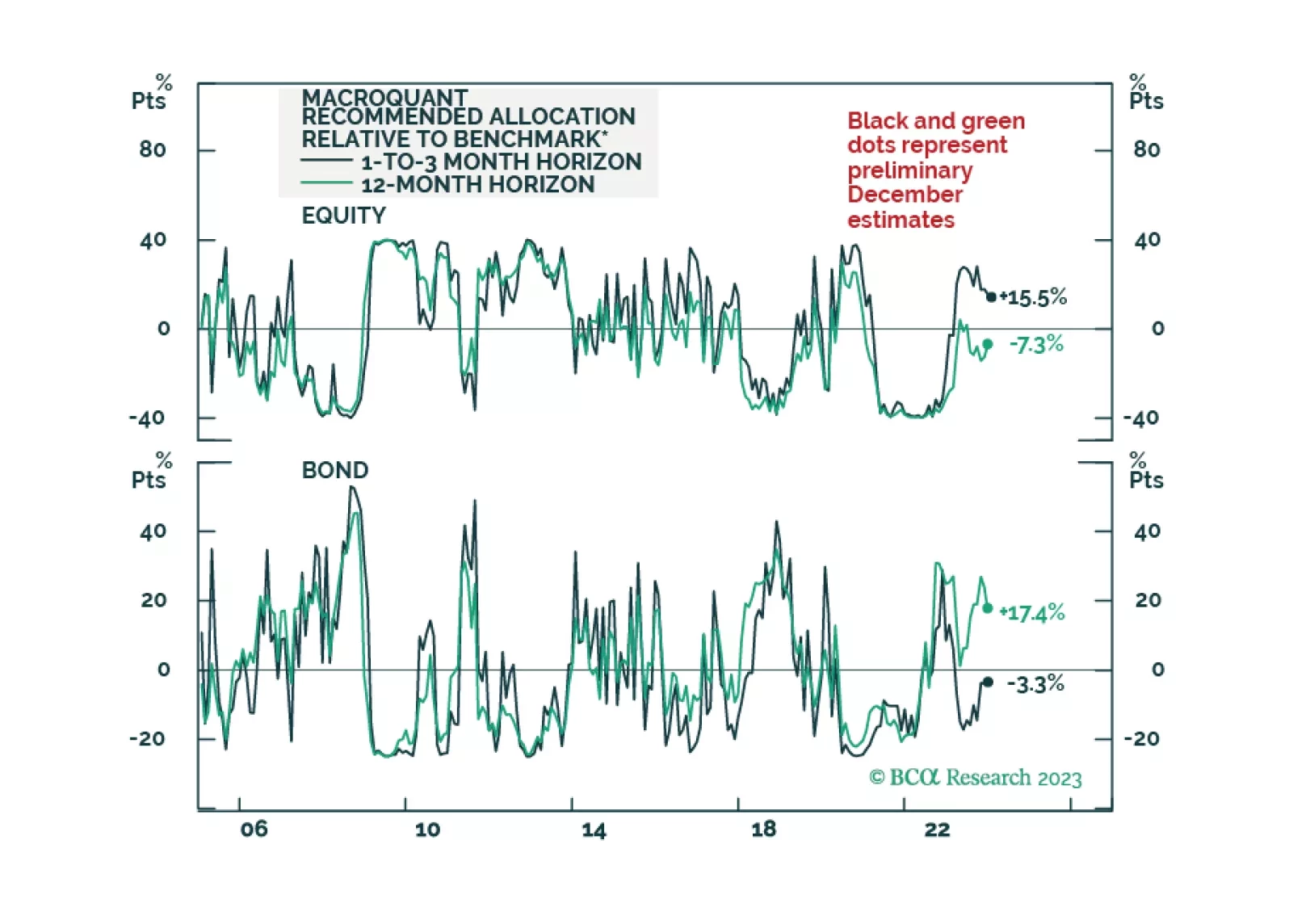

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

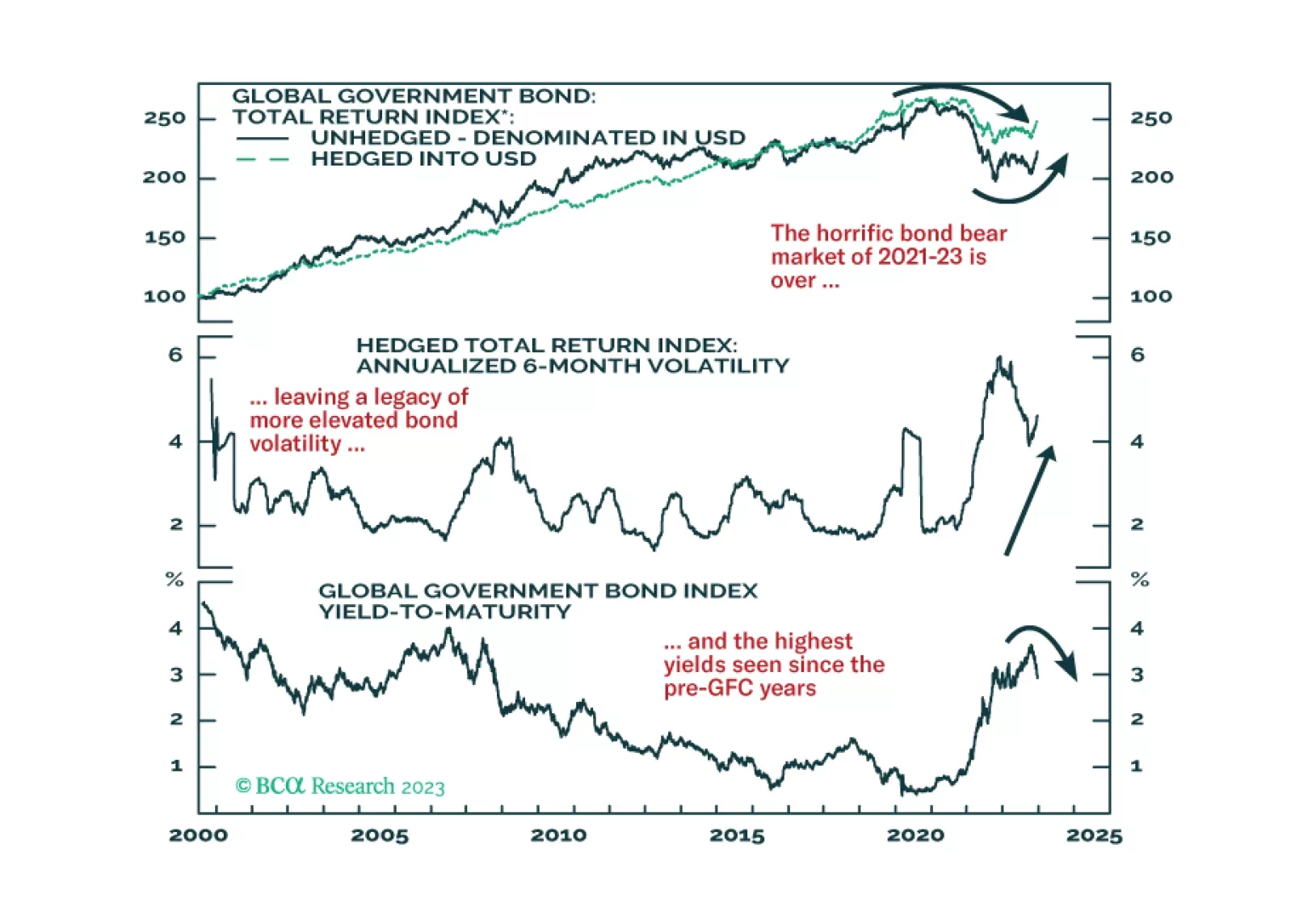

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

Explore the eight main themes that will drive the returns of European assets in 2024.

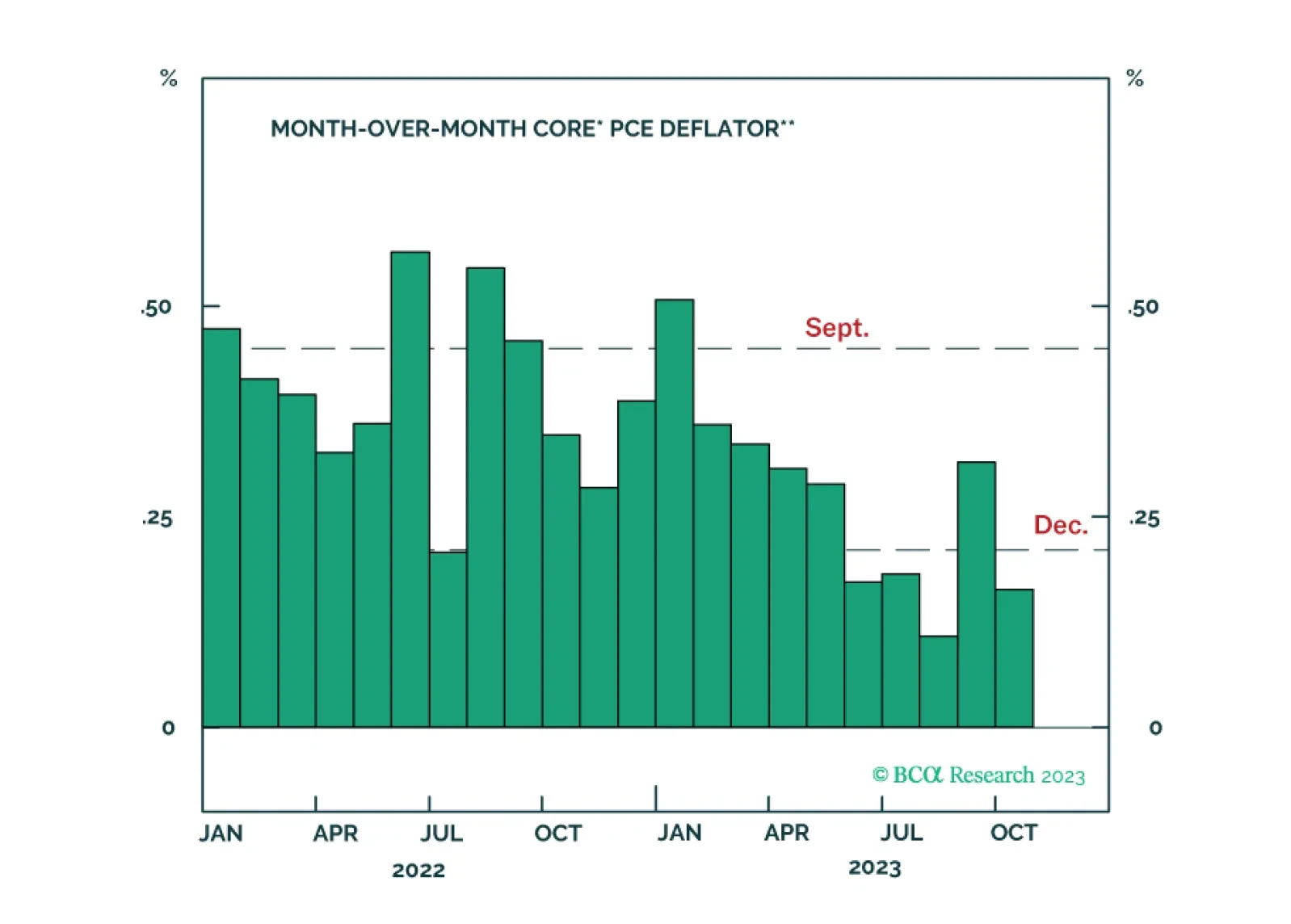

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

Our US fixed income team’s key investment views for 2024.

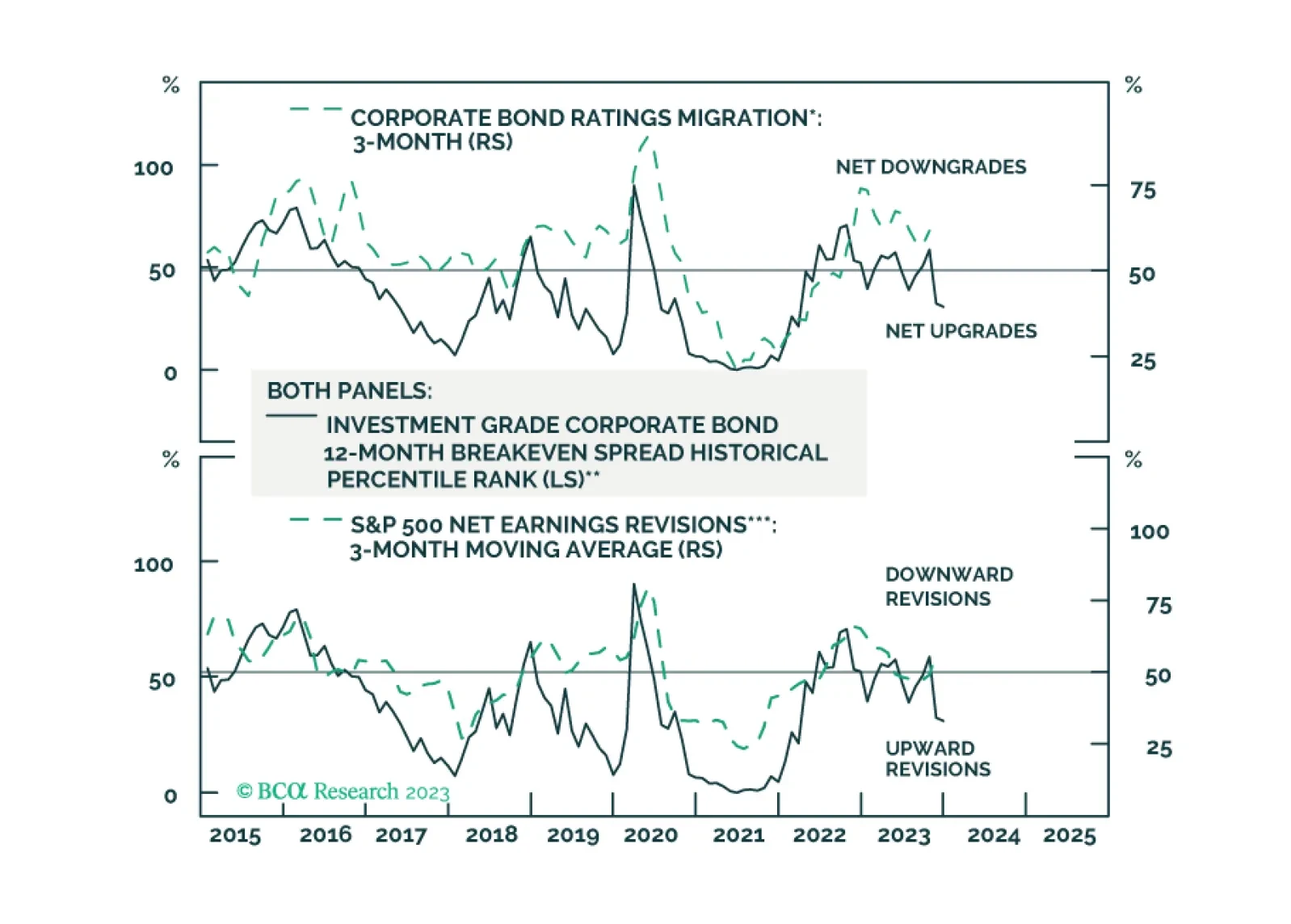

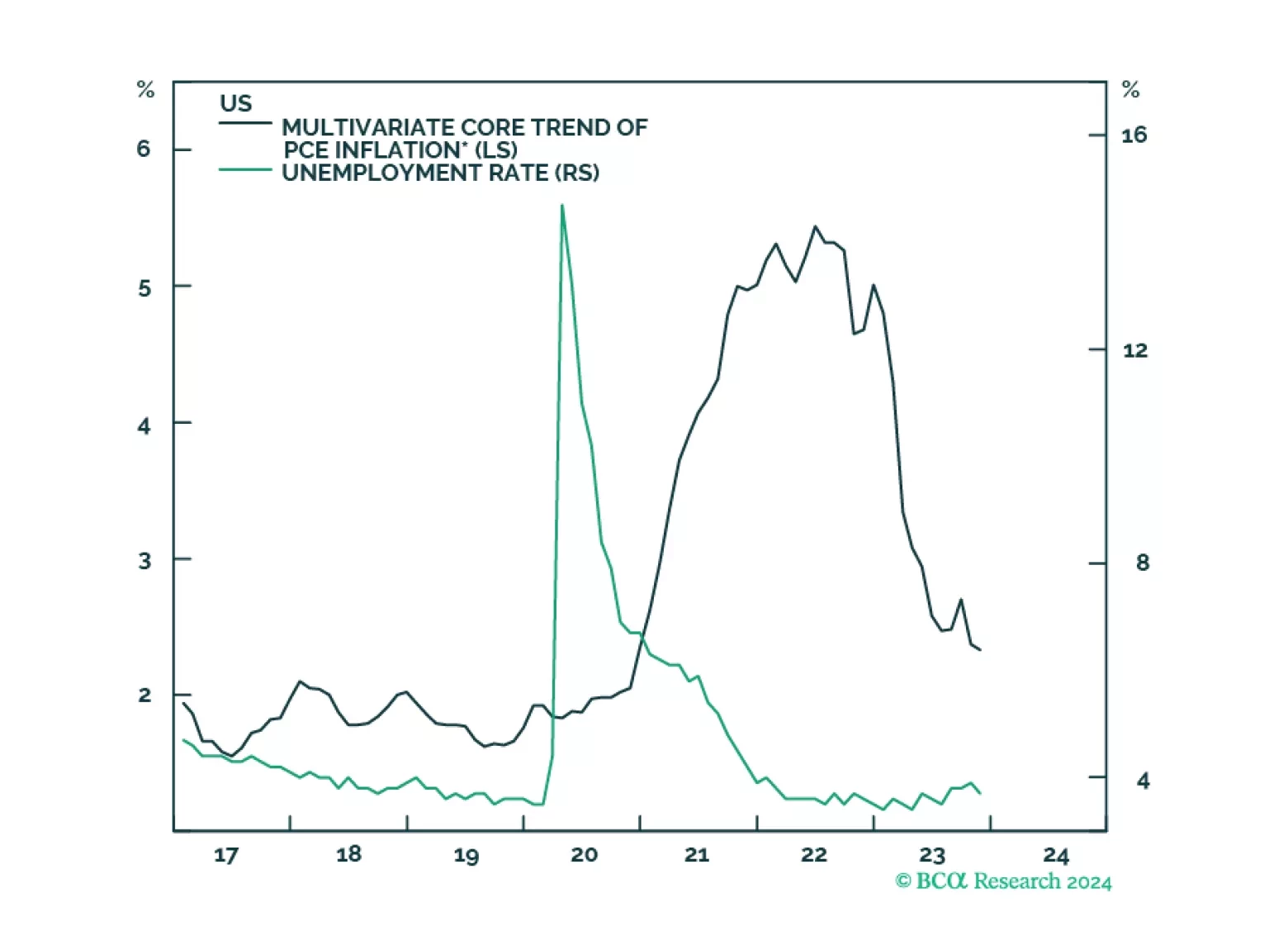

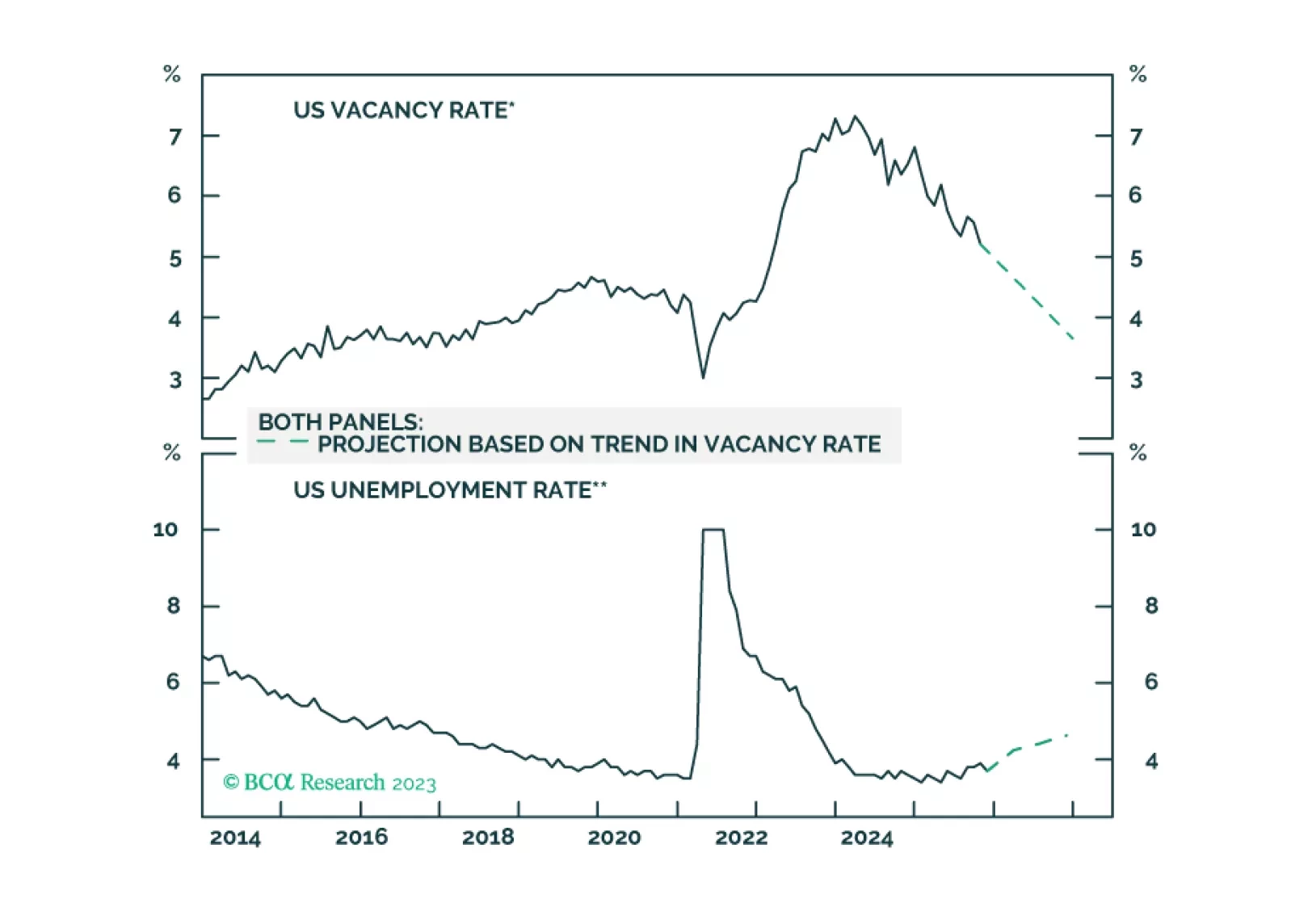

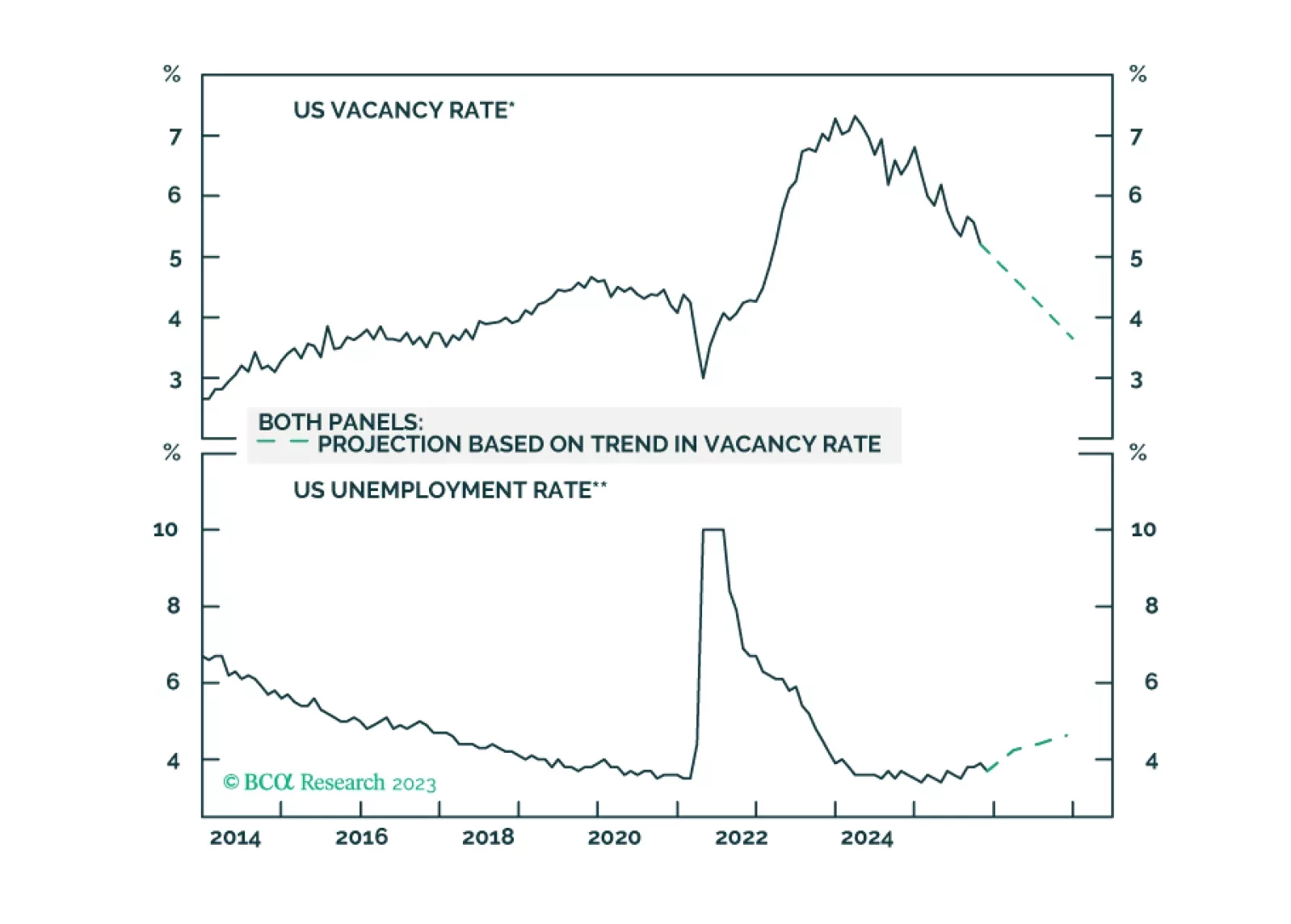

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

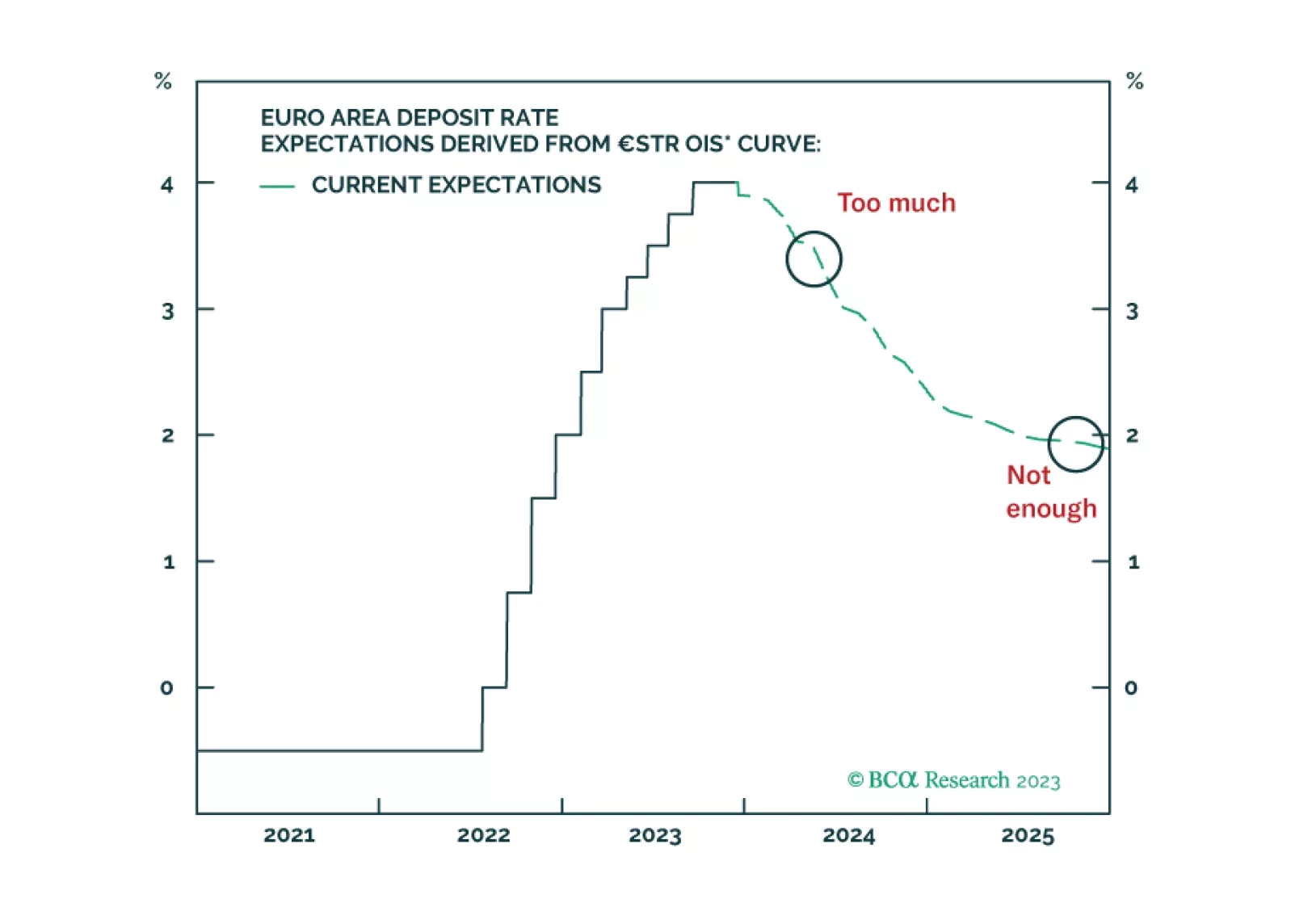

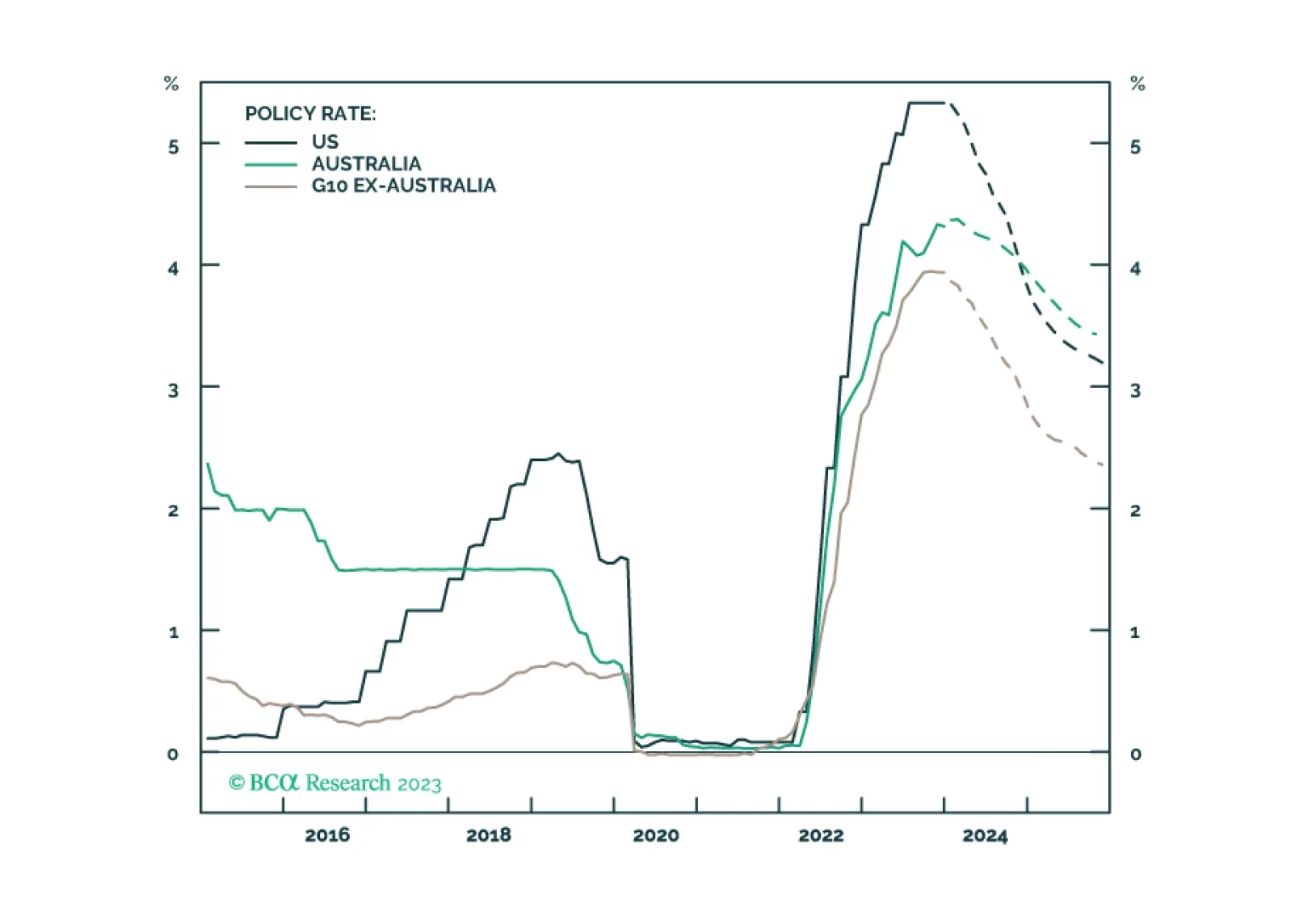

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.