Gov Sovereigns/Treasurys

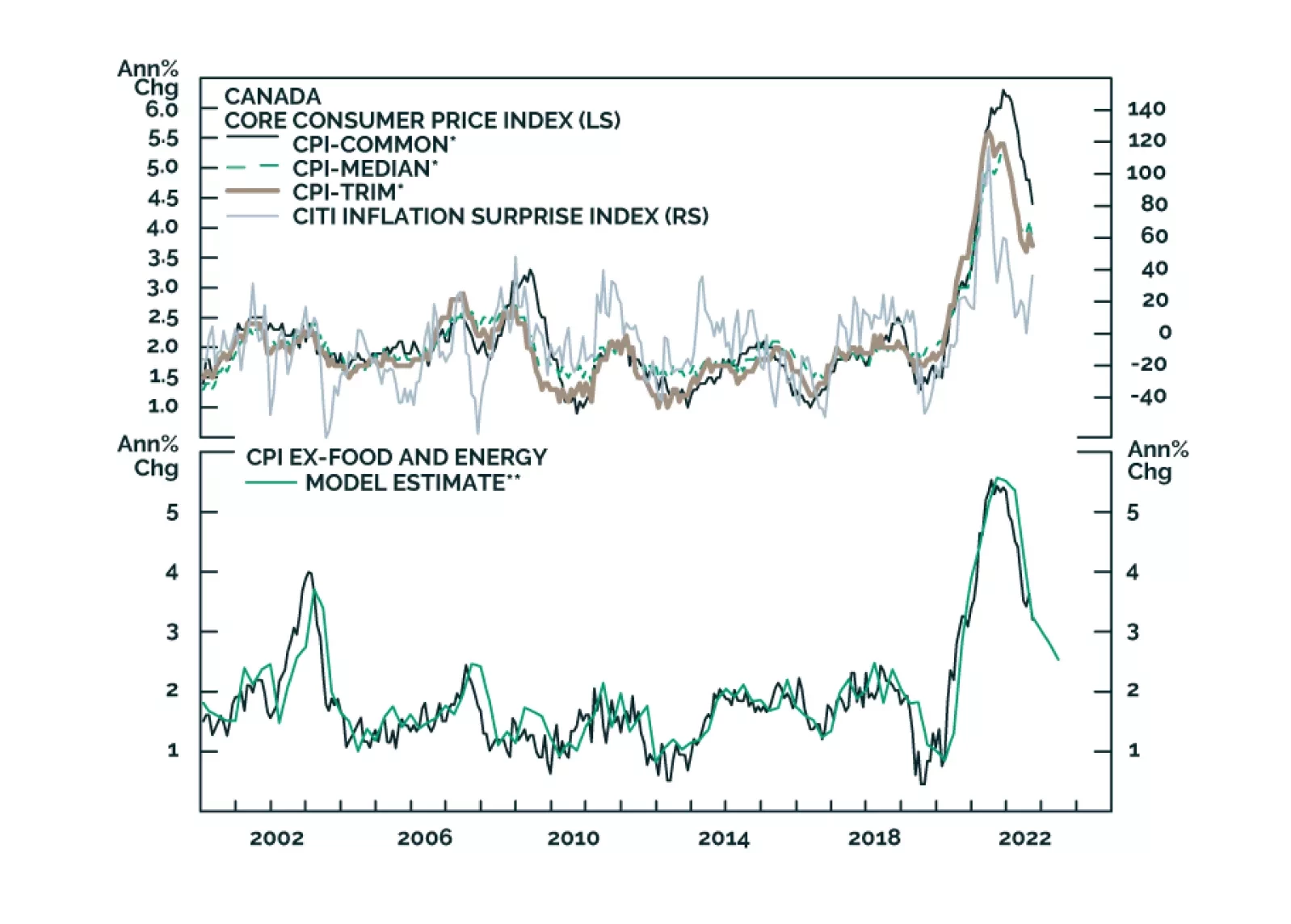

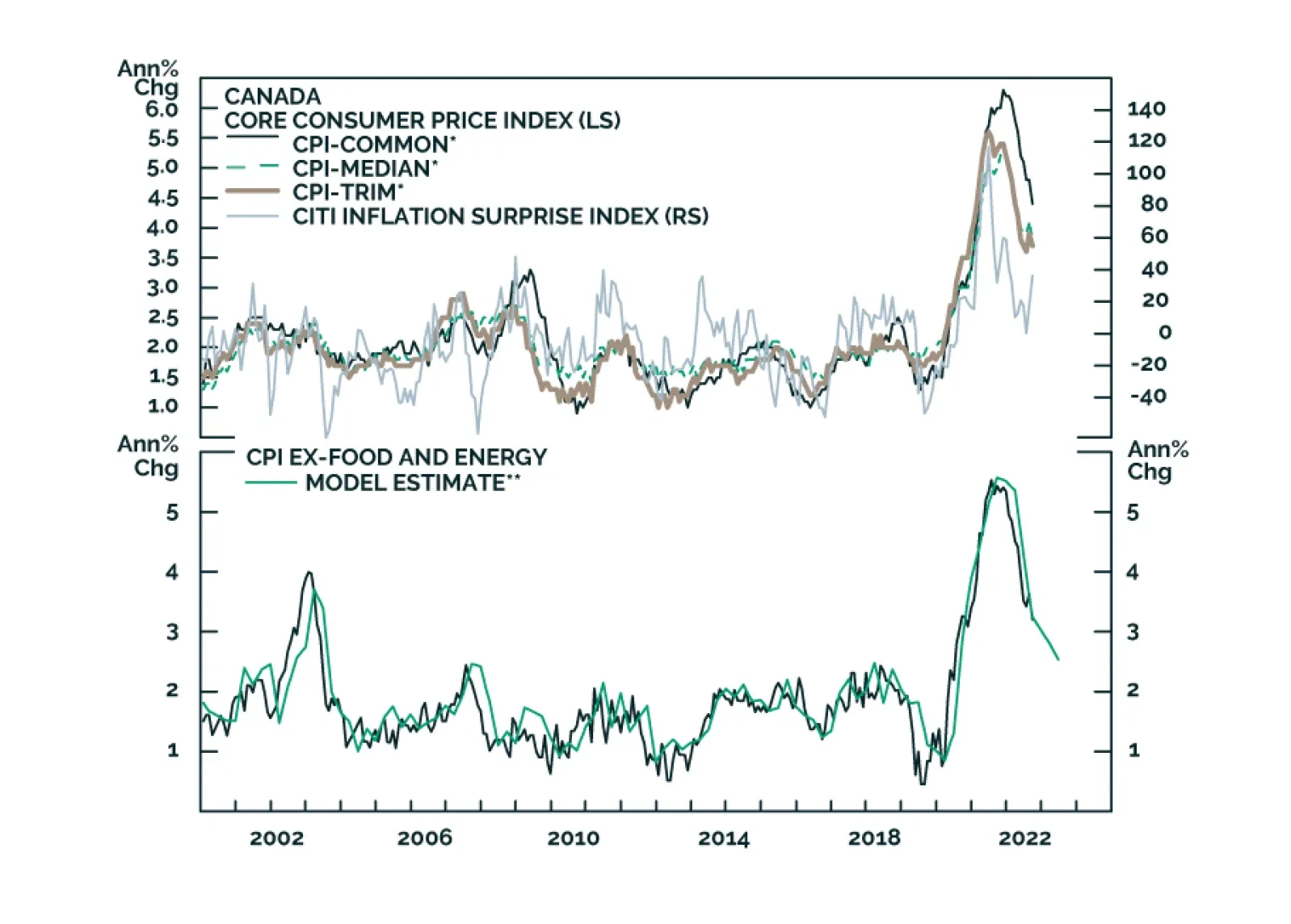

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.

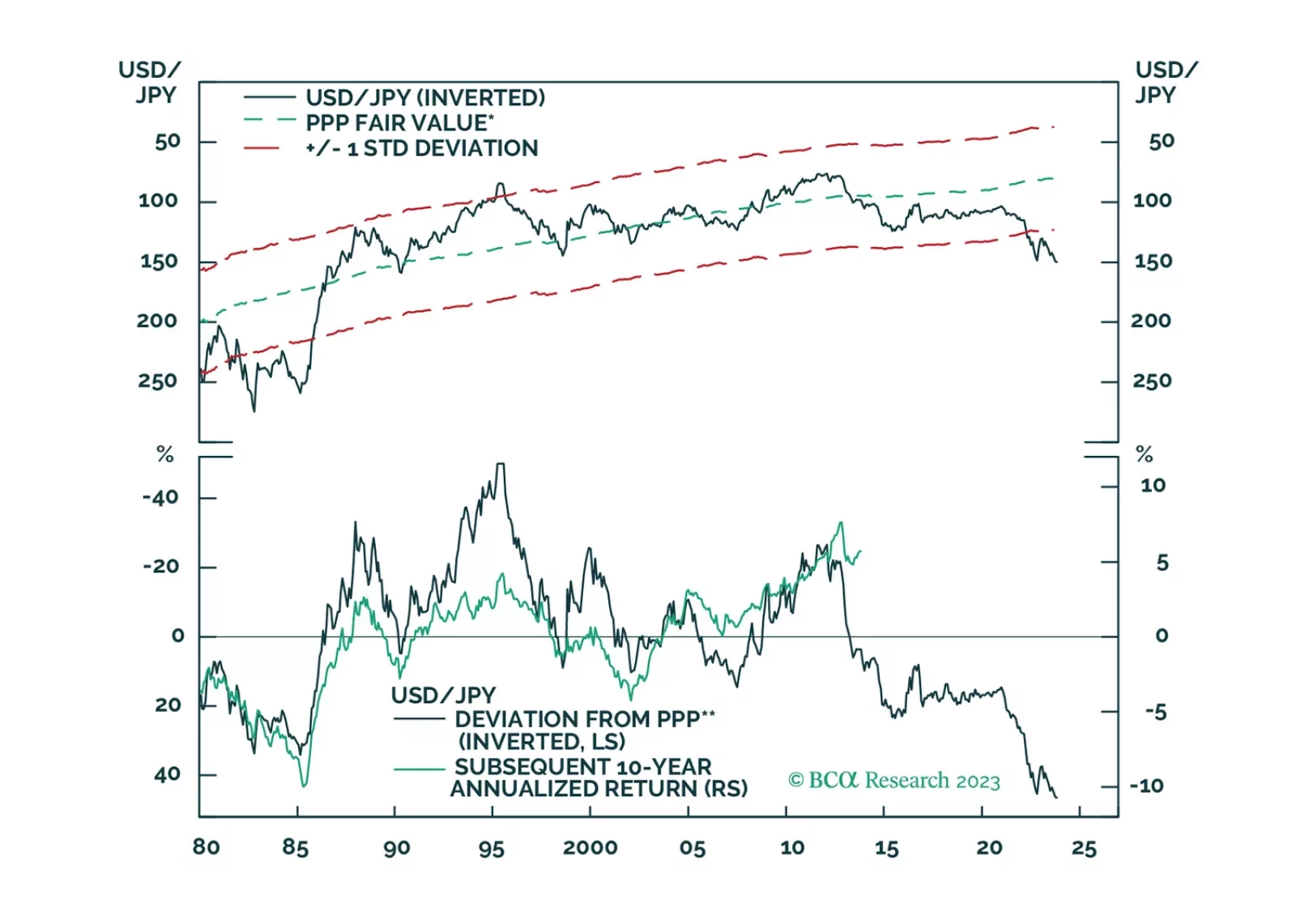

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

The recent bear-steepening of the US Treasury curve has been driven by the combination of stronger-than-expected economic growth and stable Fed rate expectations. Historically, such periods do not last very long, and we see the current bear-steepening episode ending soon. We also highlight an opportunity in Agency MBS.

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

Comments on recent Fedspeak, bond market moves and this morning’s CPI report.

An update to our US bond strategy following this morning’s employment report.

There is a connection between the bond market meltdown and Republican Party’s meltdown. Investors should expect more short-term financial market volatility as a result of the triple whammy of high bond yields, high oil prices, and a strong dollar.