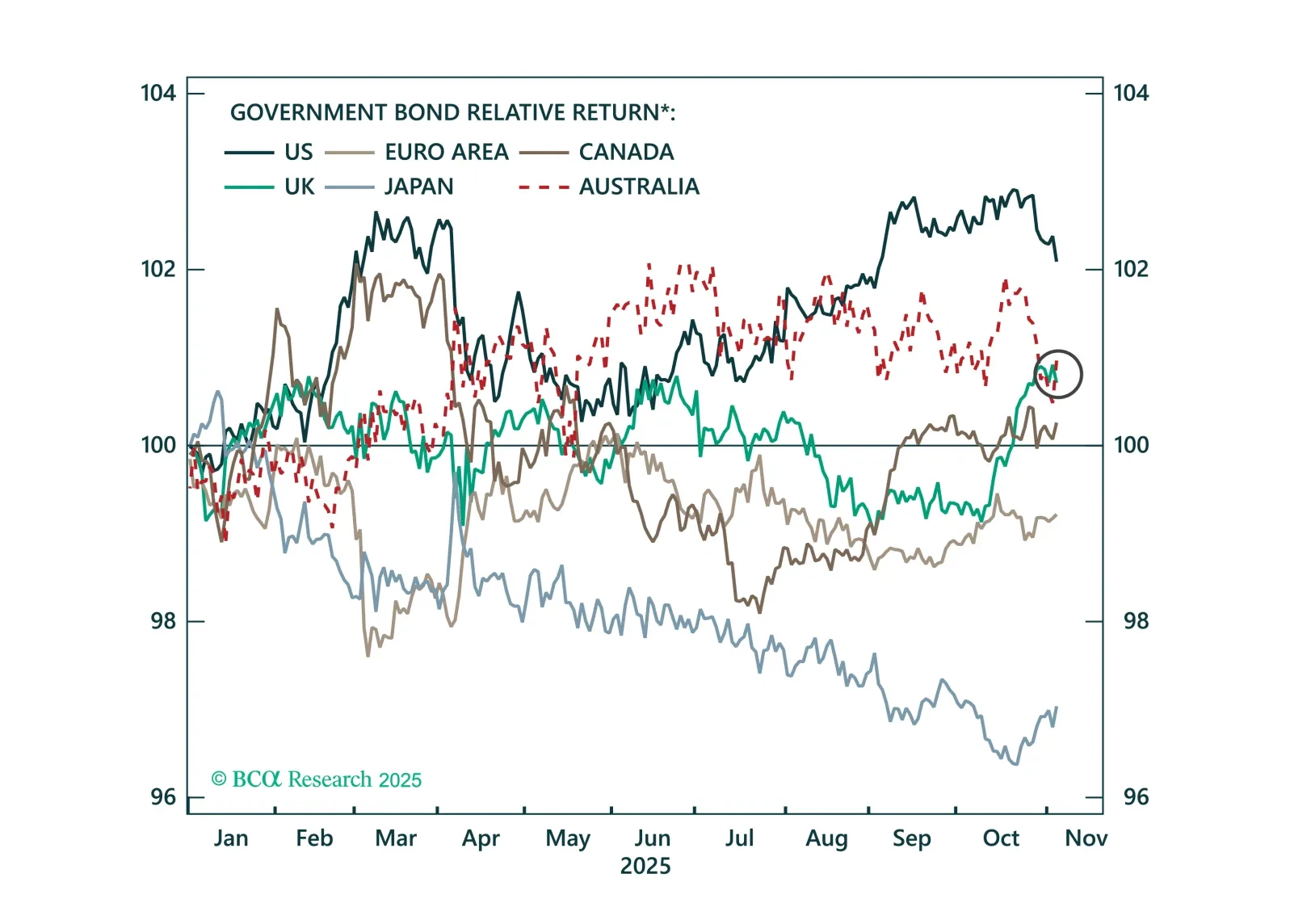

Gov Sovereigns/Treasurys

Our Portfolio Allocation Summary for December 2025.

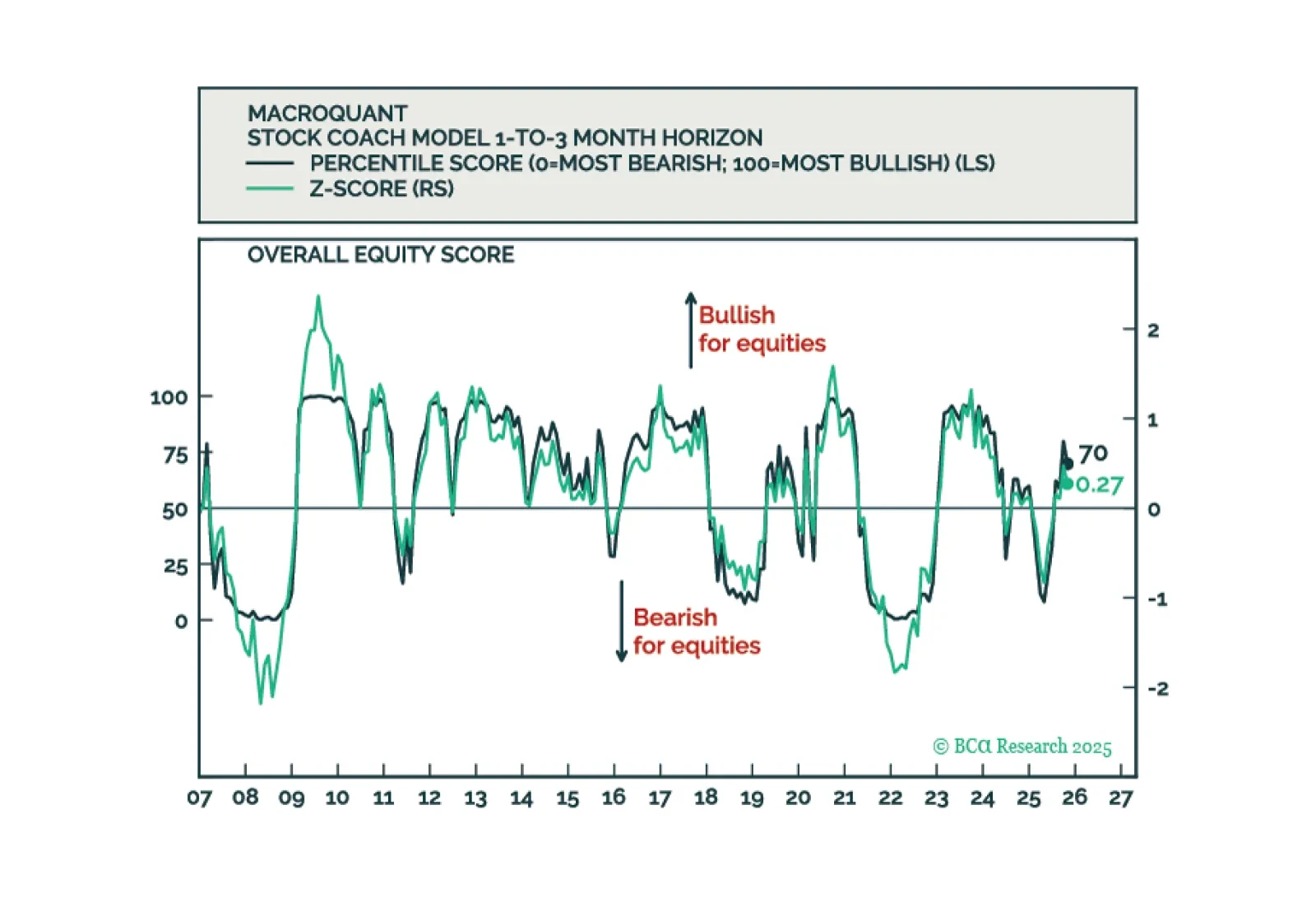

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

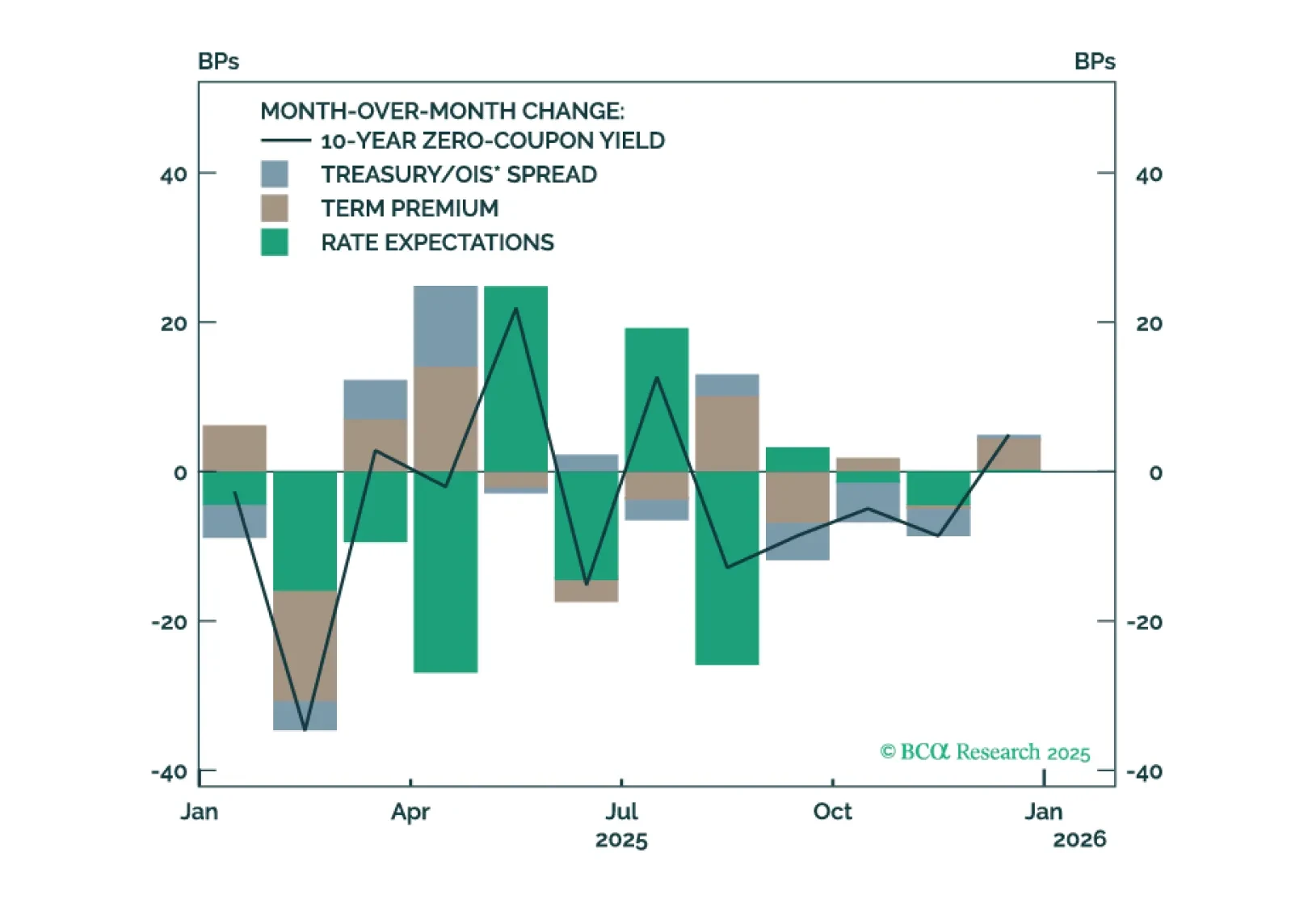

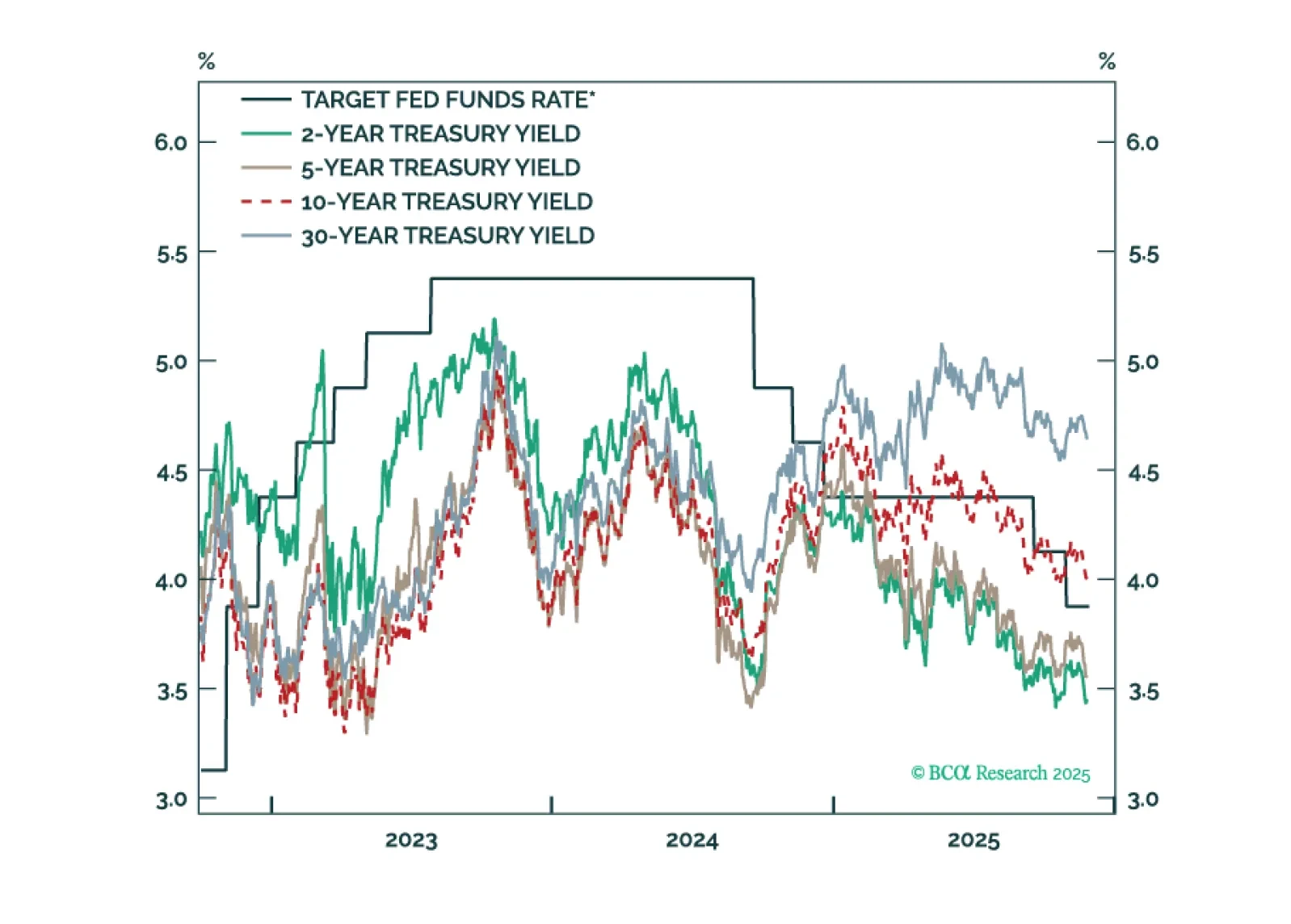

Our key US fixed income views for 2026.

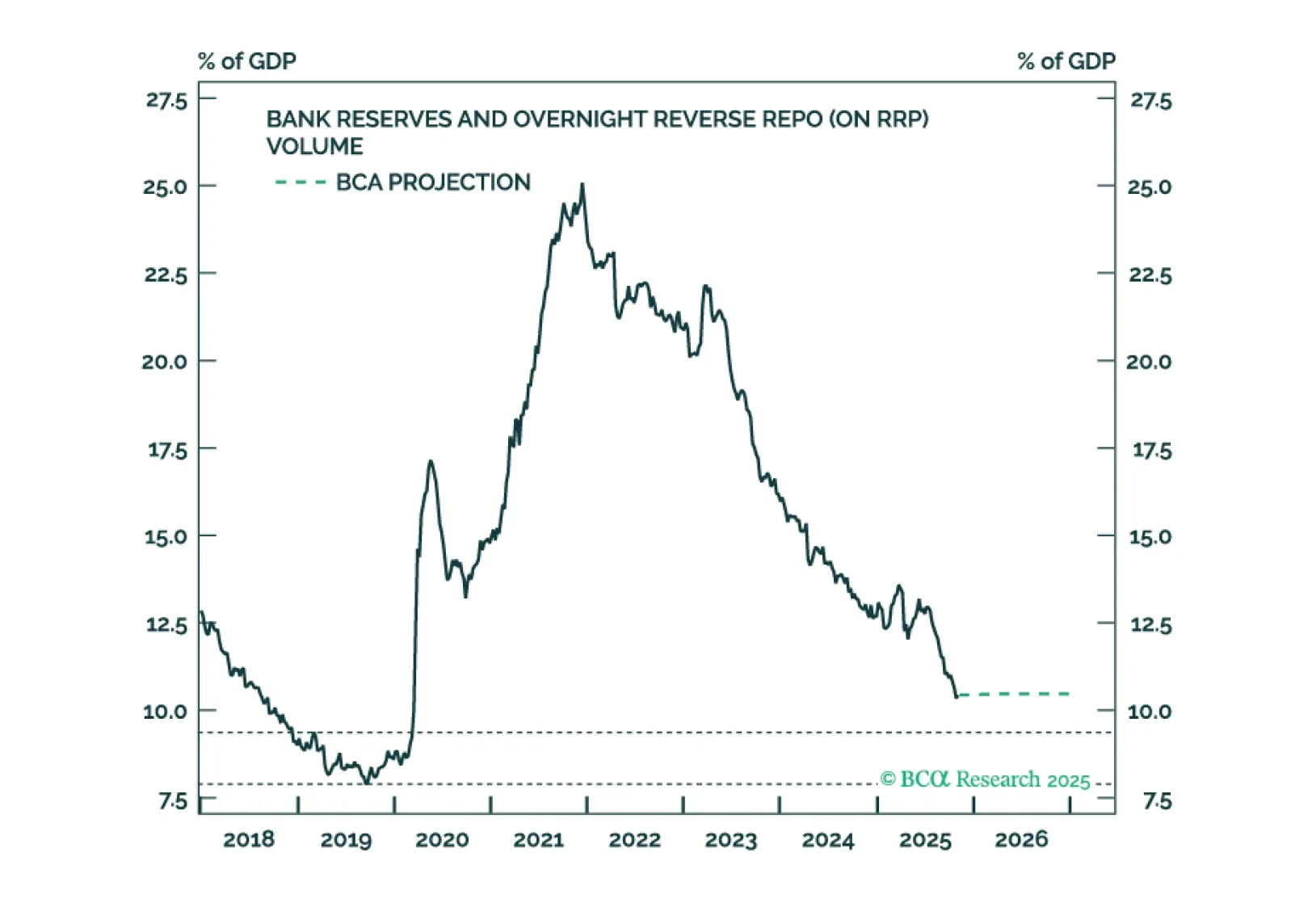

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

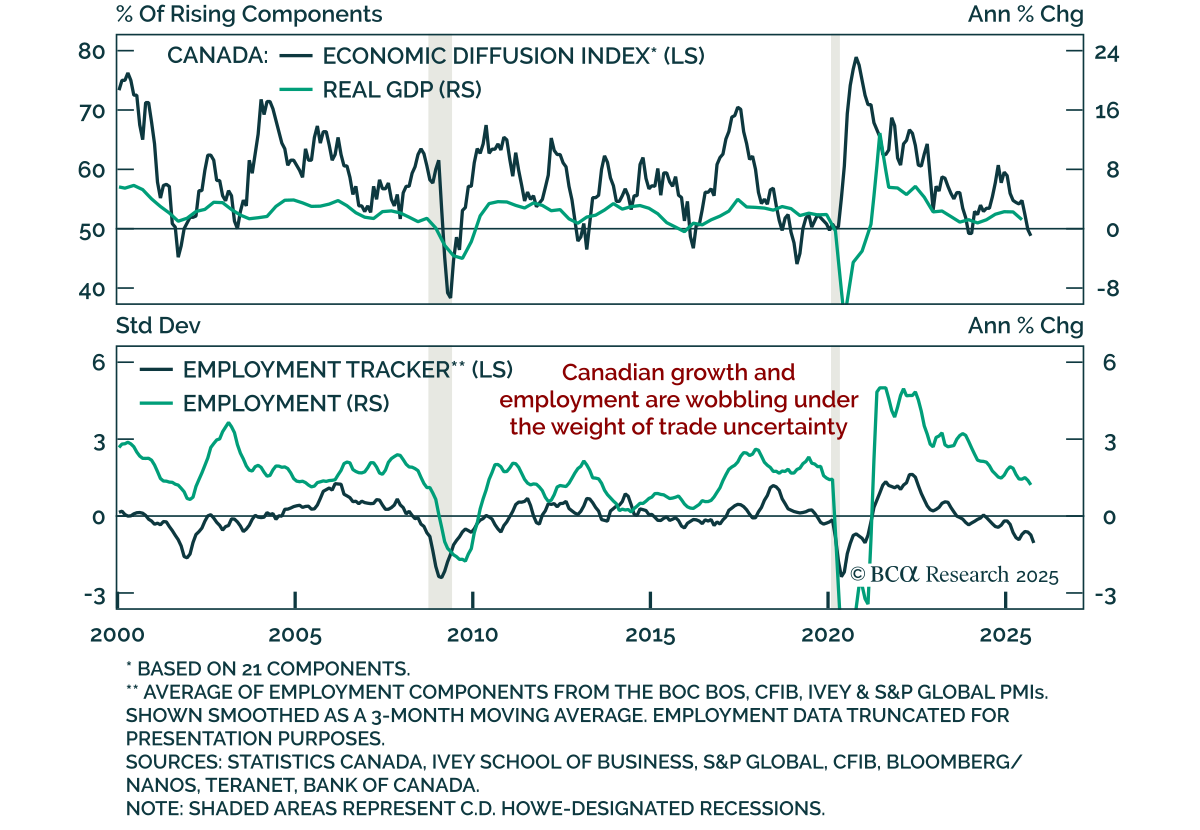

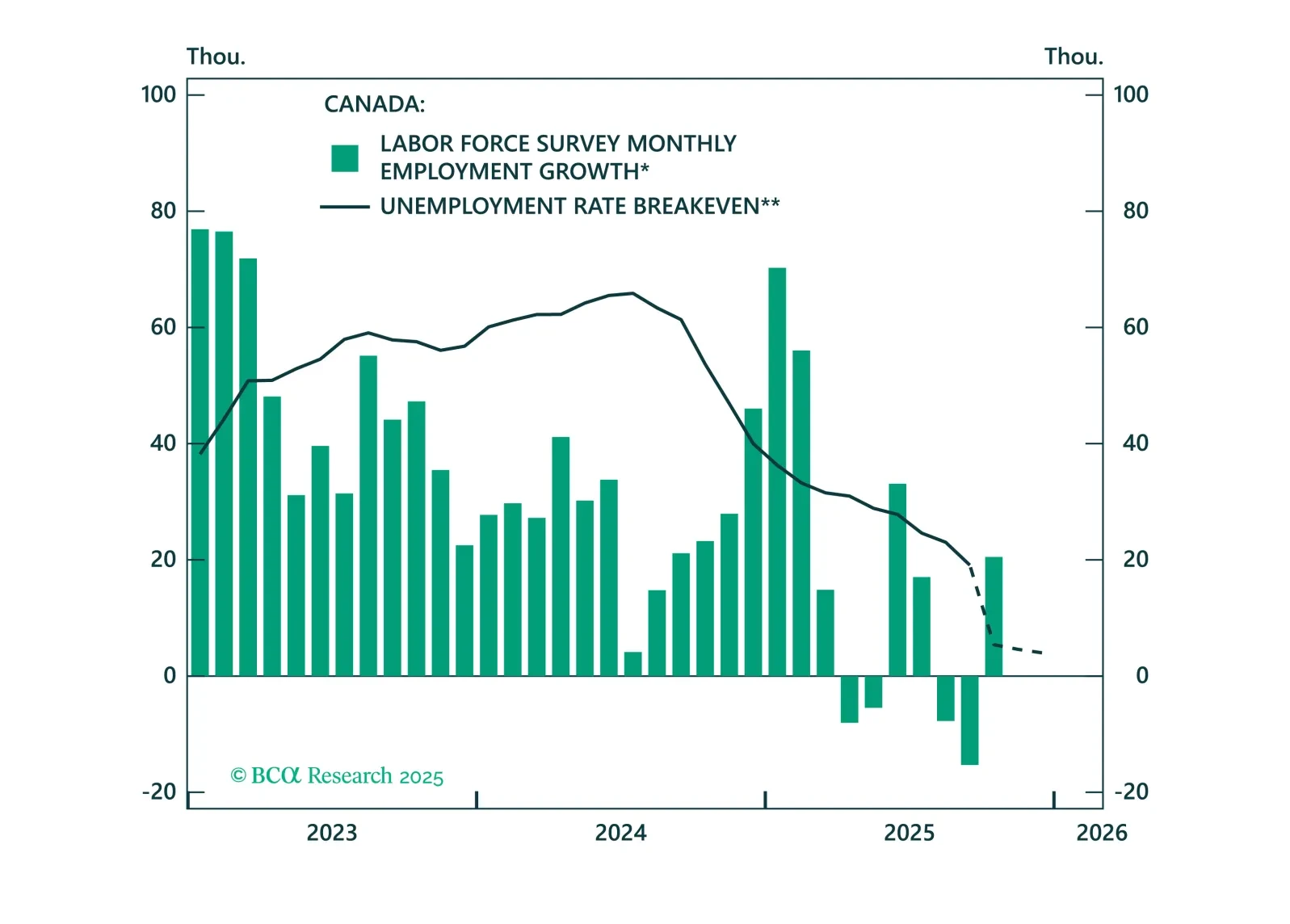

The trade war hit Canada’s economy hard, but the worst is over. In our latest update on Canada, we assess the aftermath of the trade shock, the new budget, and the effects of BoC easing. We outline what this means for duration, the Loonie, and Canadian stocks heading into 2026.

Our Portfolio Allocation Summary for November 2025.

The Bank of England will resume rate cuts in December after the autumn budget is passed. Today’s Strategy Insight discusses what this means for UK gilts and the pound.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.