Gov Sovereigns/Treasurys

Highlights Chart 1The 2003 SARS Roadmap

The 2003 SARS Roadmap

The 2003 SARS Roadmap

The bond market impact from the coronavirus has already been substantial. The 10-year Treasury yield has fallen back to 1.51%, below the fed funds rate. Meanwhile, the investment grade corporate bond index spread is back above 100 bps, from a January low of 93 bps. The 2003 SARS crisis is the best roadmap we can apply to the current situation. Back then, Treasury yields also fell sharply but then rebounded just as quickly when the number of SARS cases peaked (Chart 1). The impact on corporate bond excess returns was more short-lived (Chart 1, bottom panel). Like in 2003, we expect that bond yields will rise once the number of coronavirus cases peaks, but it is difficult to put a timeframe on how long that will take. The economic impact from the virus could also weigh on global PMI surveys during the next few months, delaying the move higher in Treasury yields we anticipated earlier this year. In short, we continue to expect higher bond yields and tighter credit spreads in 2020, but those moves will be delayed until markets are confident that the virus has stopped spreading. Feature Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 80 basis points in January. The sector actually outpaced the Treasury benchmark by 7 bps until January 21 when the impact of the coronavirus started to push spreads wider. As stated on page 1, we expect the impact of the coronavirus on corporate spreads to be short lived. Beyond that, low inflation expectations will keep monetary conditions accommodative. This in turn will encourage banks to ease credit supply, keeping defaults at bay and providing a strong tailwind for corporate bond returns.1 Yesterday’s Fed Senior Loan Officer survey showed a slight easing of C&I lending standards in Q4 2019, reversing the tightening that occurred in the third quarter (Chart 2). We expect that accommodative Fed policy will lead to continued easing of C&I lending standards for the remainder of the year. Despite the positive tailwind from accommodative Fed policy and easing bank lending standards, investment grade corporate bond spreads are quite expensive. Spreads for all credit tiers are below our targets (panels 2 & 3).2 As a result, we advise only a neutral allocation to investment grade corporate bonds. We also recommend increasing exposure to Agency MBS in place of corporate bonds rated A or higher (see page 7). Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Contagion

Contagion

Table 3BCorporate Sector Risk Vs. Reward*

Contagion

Contagion

High-Yield Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield underperformed the duration-equivalent Treasury index by 111 basis points in January. Junk outperformed the Treasury benchmark by 30 bps until January 21 when the coronavirus outbreak sent spreads sharply wider. Once the negative impact of the coronavirus passes, junk spreads will have plenty of room to tighten in 2020. In fact, the junk index spread is now at 390 bps, 154 bps above our target (Chart 3).3 While spreads for all junk credit tiers are currently above our targets, Caa-rated bonds look particularly cheap. We analyzed the divergence between Caa and the rest of the junk index in a recent report and came to two conclusions.4 First, the historical data show that 12-month periods of overall junk bond outperformance are more likely to be followed by underperformance if Caa is the worst performing credit tier. Second, we can identify several reasons for 2019’s Caa spread widening that make us inclined to downplay any negative signal. Specifically, we note that the Caa credit tier’s exposure to the shale oil sector is responsible for the bulk of 2019’s underperformance (bottom panel). Absent significant further declines in the oil price, this sector now has room to recover. MBS: Overweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 53 basis points in January. The sector was only lagging the Treasury benchmark by 7 bps as of January 21, when the coronavirus outbreak sent spreads wider. The conventional 30-year zero-volatility spread widened 8 bps in January, driven by a 7 bps widening of the option-adjusted spread (OAS) and a 1 bp increase in expected prepayment losses (aka option cost). The fact that expected prepayment losses only rose by a single basis point even though the 30-year mortgage rate fell by 23 bps is notable. It speaks to the high level of refi burnout in the mortgage market, which is a key reason why we prefer mortgage-backed securities over investment grade corporate bonds in our portfolio. Essentially, most homeowners have already had at least one opportunity to refinance during the past few years, so prepayment risk is low even if rates fall further. Competitive expected compensation is another reason to move into Agency MBS. The conventional 30-year MBS OAS is 49 bps, only 7 bps below the spread offered by Aa-rated corporate bonds (Chart 4). Also, spreads for all investment grade corporate bond credit tiers are below our cyclical targets. Risk-adjusted compensation favors MBS even more strongly. The Excess Return Bond Map in Appendix C shows that Agency MBS plot well to the right of investment grade corporates. This means that the sector is less likely to see losses versus Treasuries on a 12-month horizon. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index underperformed the duration-equivalent Treasury index by 14 basis points in January. The index was up 2 bps versus the Treasury benchmark until January 21, when the coronavirus outbreak hit. Sovereign debt underperformed duration-equivalent Treasuries by 99 bps on the month, and Foreign Agencies underperformed by 28 bps. Local Authorities, however, bested the Treasury benchmark by 60 bps. Domestic Agency bonds underperformed Treasuries by 2 bps in January, while Supranationals outperformed by 2 bps. We continue to recommend an underweight allocation to USD-denominated sovereign bonds, given that spreads remain expensive compared to US corporate credit (Chart 5). However, we noted in a recent report that Mexican and Saudi Arabian sovereigns look attractive on a risk/reward basis.5 This is also true for Local Authorities and Foreign Agencies, as shown in the Bond Map in Appendix C. Our Emerging Markets Strategy service also thinks that worries about Mexico’s fiscal position are overblown, and that bond yields embed too high of a risk premium (bottom panel).6 Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 33 basis points in January (before adjusting for the tax advantage). They were up 39 bps versus the Treasury index before the coronavirus outbreak hit on January 21. The average Aaa-rated Municipal / Treasury (M/T) yield ratio swung around during the month, but settled close to where it began at 77% (Chart 6). We upgraded municipal bonds in early October, as yield ratios had become significantly more attractive, especially at the long-end of the Aaa curve (panel 2).7 Yield ratios have tightened a lot since then, but value remains at long maturities. Specifically, the 2-year, 5-year and 10-year M/T yield ratios are all below average pre-crisis levels at 62%, 65% and 78%, respectively. But 20-year and 30-year yield ratios stand at 89% and 93%, respectively, above average pre-crisis levels. Fundamentally, state and local balance sheets remain solid. Our Municipal Health Monitor is in “improving health” territory and state & local government interest coverage has improved considerably in recent quarters (bottom panel). Both of these trends are consistent with muni ratings upgrades continuing to outpace downgrades going forward. Treasury Curve: Maintain A Barbell Curve Positioning Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bull-flattened dramatically in January. Treasury yields declined across the curve, and the 2/10 slope flattened from 34 bps to 18 bps. The 5/30 slope flattened from 70 bps to 67 bps. Despite the significant flattening, the 2/10 slope remains near the middle of our target 0 – 50 bps range for 2020, and we anticipate some bear-steepening once the coronavirus is contained.8 The front-end of the curve also moved in January to price-in 57 bps of Fed rate cuts during the next 12 months (Chart 7). At the beginning of the year the curve was priced for only 14 bps of rate cuts. We expect that the Fed would respond with rate cuts if the coronavirus epidemic worsens, leading to inversion of the 2/10 yield curve. However, for the time being the safer bet is that the virus will be contained relatively quickly and the Fed will remain on hold for all of 2020. Based on this view, we continue to recommend holding a barbelled Treasury portfolio. Specifically, we favor holding a 2/30 barbell versus the 5-year bullet, in duration-matched terms. The position offers positive carry and looks attractive on our yield curve models (see Appendix B).9 TIPS: Overweight Chart 8Inflation Compensation

Inflation Compensation

Inflation Compensation

TIPS underperformed the duration-equivalent Treasury index by 75 basis points in January. The 10-year TIPS breakeven inflation rate fell 12 bps on the month and currently sits at 1.66%. The 5-year/5-year forward TIPS breakeven inflation rate fell 16 bps on the month and currently sits at 1.71%. Both rates remain well below the 2.3%-2.5% range consistent with the Fed’s target. The divergence between the actual inflation data and inflation expectations remains stark. Trimmed mean PCE inflation has been fluctuating around the Fed’s target since mid-2018 (Chart 8). However, long-maturity TIPS breakeven inflation rates remain stubbornly low. It takes time for expectations to adapt to a changing macro environment, but even accounting for those long lags, our Adaptive Expectations Model pegs the 10-year TIPS breakeven inflation rate as 31 bps too low (panel 4).10 It is highly likely that the Fed will have to tolerate some overshoot of its 2% inflation target in order to re-anchor long-term inflation expectations. As a result, the actual inflation data will lead expectations higher, causing the TIPS breakeven inflation curve to flatten.11 ABS: Underweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 32 basis points in January. The index option-adjusted spread for Aaa-rated ABS tightened 14 bps on the month. It currently sits at 26 bps, below its minimum pre-crisis level (Chart 9). Our Excess Return Bond Map (see Appendix C) shows that Aaa-rated consumer ABS ranks among the most defensive US spread products. This explains why the sector performed so well in January when other spread sectors struggled. ABS also offer higher expected returns than other low-risk sectors such as Domestic Agency bonds and Supranationals. However, we remain wary of allocating too much to consumer ABS because credit trends are slowly shifting in the wrong direction. The consumer credit delinquency rate remains low, but has put in a clear bottom. This is also true for the household interest expense ratio (panel 3). Senior Loan Officers also continue to tighten lending standards for both credit cards and auto loans. Tighter lending standards usually coincide with rising delinquencies (bottom panel). Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 43 basis points in January. The index option-adjusted spread for non-agency CMBS tightened 6 bps on the month. It currently sits at 67 bps, below its average pre-crisis level (Chart 10). In last week’s Special Report, we explored how low interest rates have boosted commercial real estate (CRE) prices this cycle, and concluded that a sharp drawdown in CRE prices is likely only when inflation starts to pick up steam.12 In that report we also mentioned that non-agency Aaa-rated CMBS spreads look attractive relative to US corporate bonds from a risk/reward perspective (see our Excess Return Bond Map in Appendix C), and that the macro environment is only slightly unfavorable for CMBS spreads. Specifically, CRE bank lending standards are just in “net tightening” territory. But both lending standards and loan demand are very close to neutral (bottom 2 panels). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 34 basis points in January. The index option-adjusted spread tightened 4 bps on the month to reach 54 bps. The Excess Return Bond Map in Appendix C shows that Agency CMBS offer a compelling risk/reward trade-off. An overweight allocation to this sector remains appropriate. Appendix A: The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the US Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. At present, the market is priced for 57 basis points of cuts during the next 12 months. We anticipate a flat fed funds rate over that time horizon, and therefore anticipate that below-benchmark portfolio duration positions will profit. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

We can also use our Golden Rule framework to make 12-month total return and excess return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the fed funds rate. Excess returns are relative to the Bloomberg Barclays Cash index. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with 95% confidence intervals. Excess returns are calculated by subtracting assumed cash returns in each scenario from our total return projections.

Contagion

Contagion

Contagion

Contagion

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of January 31, 2020)

Contagion

Contagion

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of January 31, 2020)

Contagion

Contagion

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 33 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 33 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

Contagion

Contagion

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Excess Return Bond Map (As Of January 31, 2020)

Contagion

Contagion

Footnotes 1 Please see US Bond Strategy Special Report, “2020 Key Views: US Fixed Income”, dated December 10, 2019, available at usbs.bcaresearch.com 2 For details on how we calculate our spread targets please see US Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 3 For details on how we calculate our spread targets please see US Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Caa-Rated Bonds: Warning Sign Or Buying Opportunity?”, dated November 26, 2019, available at usbs.bcaresearch.com 5 Please see US Bond Strategy Weekly Report, “A Perspective On Risk And Reward”, dated October 15, 2019, available at usbs.bcaresearch.com 6 Please see Emerging Markets Strategy Weekly Report, “Country Insights: Malaysia, Mexico & Central Europe”, dated October 31, 2019, available at ems.bcaresearch.com 7 Please see US Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 8 Please see US Bond Strategy Special Report, “2020 Key Views: US Fixed Income”, dated December 10, 2019, available at usbs.bcaresearch.com 9 For further details on our recommended yield curve trade please see US Bond Strategy Weekly Report, “The Best Spot On The Yield Curve”, dated January 21, 2020, available at usbs.bcaresearch.com 10 For further details on our Adaptive Expectations Model please see US Bond Strategy Weekly Report, “Adaptive Expectations In The TIPS Market”, dated November 20, 2018, available at usbs.bcaresearch.com 11 Please see US Bond Strategy Special Report, “2020 Key Views: US Fixed Income”, dated December 10, 2019, available at usbs.bcaresearch.com 12 Please see US Investment Strategy / US Bond Strategy Special Report, “Commercial Real Estate And US Financial Stability”, dated January 27, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

Highlights Global Growth Fears: Efforts to contain the China coronavirus outbreak risk creating the outcome that investors feared most in 2019 from the US-China trade war – weaker global growth and a severe disruption to supply chains worldwide. Monetary Policy Responses: Global bond yields have plunged as investors have piled into safe haven assets and priced in additional monetary easing from major central banks. Some of that decline in yields, however, may be a repricing of future rate hike probabilities with central banks like the Fed and ECB rethinking their inflation mandates and how to achieve them. Duration Strategy: Maintain a moderate below-benchmark cyclical (6-12 months) stance on overall interest rate duration in global fixed income portfolios. Yields now discount a significant hit to global economic growth from China. This outcome is far from certain, especially if China delivers more aggressive fiscal and monetary policy easing to mitigate the deflationary effects of the public health crisis. Feature Chart of the WeekBond Yields Have "Gone Viral"

Bond Yields Have "Gone Viral"

Bond Yields Have "Gone Viral"

Global bond yields have declined sharply over the past two weeks, as investors have tried to process the potential implications of the China coronavirus outbreak. Scenes of empty streets in Chinese cities under quarantine look like something out of a Hollywood science fiction movie. Fears of a “zombie apocalypse” scenario plunging the global economy into recession are proliferating among doomsayers. The viral outbreak is interrupting global growth just as it is starting to show signs of recovery from the manufacturing slump of 2019 (Chart of the Week). Global bond yields had been slowly rising alongside that economic improvement, and risk premia in equity and credit markets had begun to narrow in earnest. Against that backdrop with markets priced for perfection, a massive public health crisis in the most marginal driver of global growth, China, was a potent trigger for a correction in risk assets. The story is obviously very fluid, with the number of infected continuing to grow in China and more cases being discovered across the world. At least 50 million Chinese citizens are now under quarantine, across several major cities. More countries are instituting travel bans to and from China, and important global companies like Apple are shuttering their China operations until further notice. The ultimate hit to global growth is yet to be determined, but measures being taken to slow the spread of the coronavirus will clearly have an impact on global trade, supply chain management and, thus, economic growth. This risks a repeat of the May-August period last year, when markets were pricing in the potential negative effects of US-China trade tariffs on global growth, triggering a major decline in global bond yields. A big driver of that bond rally last year was a shift towards expectations of easier global monetary policy. Those were largely realized as central banks cut rates while global growth was actually slowing. Bond yields now discount another round of rate cuts, most importantly from the US Federal Reserve, despite no formal indication (yet) that policymakers are looking to deliver more easing. The risk now is that investors will become too pessimistic, setting up a swing of the pendulum in the opposite direction if the hit to global growth from the virus is less than feared. On that note, a significant Chinese economic growth slowdown now appears fully priced into global bond yields. The risk now is that investors will become too pessimistic, setting up a swing of the pendulum in the opposite direction if the hit to global growth from the virus is less than feared. On that note, a significant Chinese economic growth slowdown now appears fully priced into global bond yields, as we discuss later in this Weekly Report. Breaking Down The Latest Decline In Global Bond Yields The decline in government bond yields in the developed markets (DM) has been sharpest since Chinese authorities confirmed human-to-human transmission of the coronavirus on Monday, January 20. That appears to be the date when investors began to take the outbreak much more seriously. Growth-sensitive assets like emerging market (EM) equities, copper and oil prices peaked on Friday, January 17, while measures of volatility like the US VIX index and US high-yield credit spreads troughed (Chart 2). The price of safe haven assets like gold and the Japanese yen have also increased since that “pre-virus peak” on January 17, as have bond volatility measures like the US MOVE index or European swaption volatility (Chart 3). Importantly, the increases in rates volatility have been smaller to date compared to mid-2019, when the “convexity” trade triggered an insatiable demand for duration that drove longer-maturity global bond yields sharply lower. Chart 2A Pullback In Growth-Sensitive Assets

A Pullback In Growth-Sensitive Assets

A Pullback In Growth-Sensitive Assets

Chart 3A Mild Bid For Safe Havens Compared To 2019

A Mild Bid For Safe Havens Compared To 2019

A Mild Bid For Safe Havens Compared To 2019

A breakdown of the decline in the benchmark 10-year government bond yields in the major DM countries (US, Germany, Japan, the UK, Canada and Australia) since that “pre-virus peak” is shown in Table 1. Table 1Global Bond Yield Changes Since January 17, 2020

The China Syndrome

The China Syndrome

The biggest declines were in the US (-33bps), Canada (-29bps) and Australia (-23bps) where central bank monetary policy expectations also saw the largest shift. Our 12-month discounters, which measure the change in short-term interest rates over a one-year horizon priced into Overnight Index Swap (OIS) curves, have fallen by -30bps in the US, -26bps in Canada and -22bps in Australia – indicating that markets had fully priced in a rate cutting response to the coronavirus outbreak from the Fed, Bank of Canada and Reserve Bank of Australia. Bond yields have fallen to a lesser extent in Germany (-19bps), the UK (-11bps) and Japan (-7bps), but with very modest declines in our 12-month discounters for those three countries were policy interest rates are close to, or below, 0%. Therefore, the decline global yields over the past two weeks can, on the surface, be attributed to expectations of easier monetary policy in response to the potential hit to growth, and tightening of financial conditions as risk assets sell off, from the coronavirus (Chart 4). Chart 4Falling Yields Reflect Expectations Of More Rate Cuts In 2020...

Falling Yields Reflect Expectations Of More Rate Cuts In 2020...

Falling Yields Reflect Expectations Of More Rate Cuts In 2020...

Chart 5...But Also Expectations Of Lower Rates For Longer

...But Also Expectations Of Lower Rates For Longer

...But Also Expectations Of Lower Rates For Longer

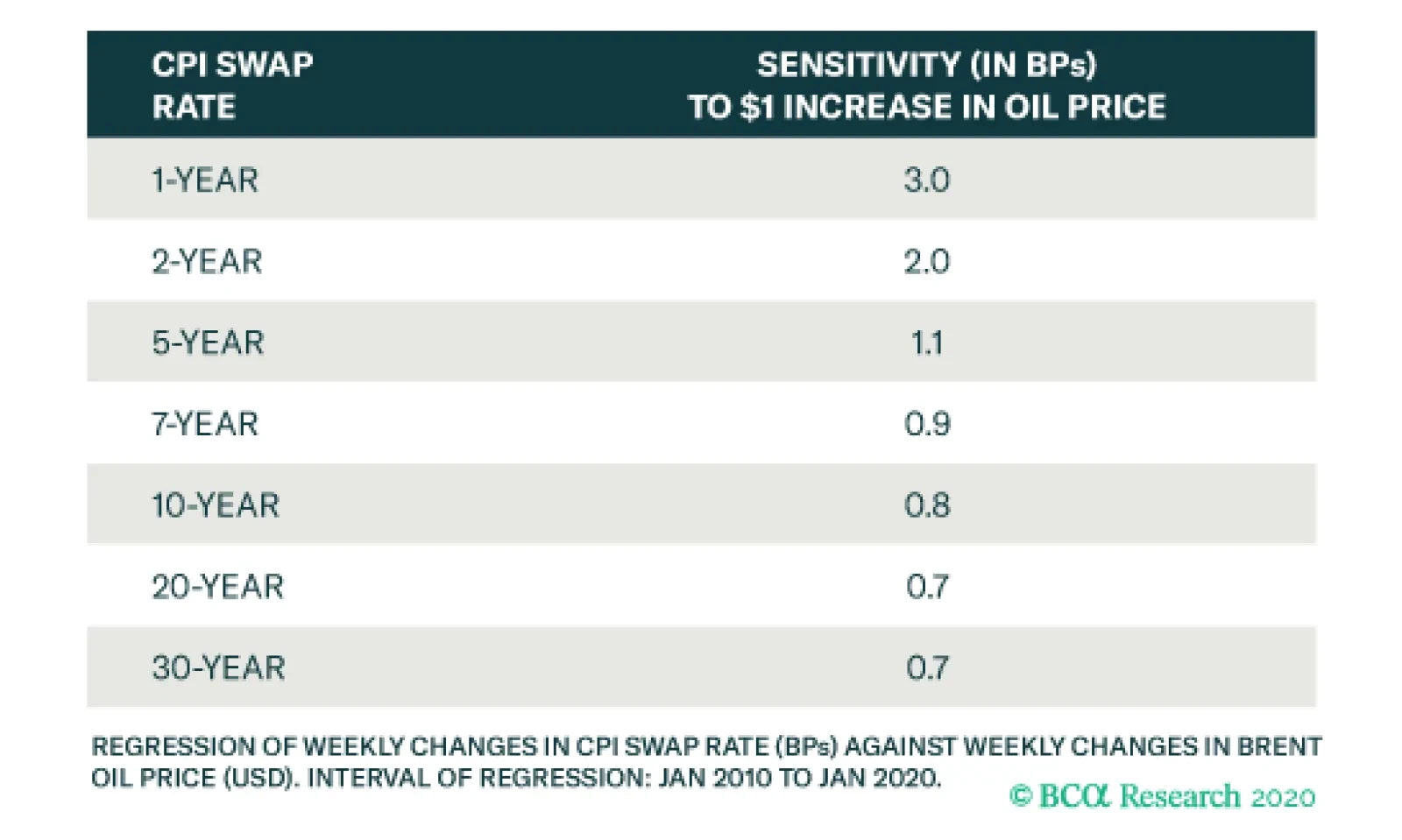

Yet when looking at our estimates of the term premium for all six countries, the decline in the nominal 10-year yields is almost equal to the reduction in the term premium. On the surface, this would be consistent with the idea that the fall in yields is due to risk aversion driving up the demand for the safety of government bonds – and can hence be unwound if the news were to turn less gloomy on the spread of the coronavirus. Yet interest rates further out the yield curve have also fallen by similar amounts in all countries shown, when looking at 1-year interest rates, 5-years forward (the bottom row of Table 1). That decline in longer-dated forwards does correlate strongly with lower inflation expectations as measured by 10-year CPI swap rates (Chart 5). This suggests an alternative explanation for the recent fall in global bond yields that is not related to worries over the coronavirus: bond markets increasingly believe that policy interest rates will be lower for a lot longer. An alternative explanation for the recent fall in global bond yields that is not related to worries over the coronavirus: bond markets increasingly believe that policy interest rates will be lower for a lot longer. With the Fed and ECB now openly discussing changing their monetary policy frameworks to manage achievement of their statutory inflation targets more proactively, the hurdle for contemplating any interest rate hikes in the future is now much higher. Thus, central banks are giving forward guidance to the markets that rates will be lower. That is a message that would also be consistent with the decline in the term premium, to the extent that the premium is compensation for the future volatility of short-term interest rates. When looking at all the components, the message from the most recent decline in global bond yields may be more complex than simple virus-driven risk aversion. Our Duration Indicator continues to improve alongside rebounding global economic sentiment, signaling cyclical upward pressure on yields (Chart 7) – assuming, of course, that the hit to Chinese growth from the coronavirus outbreak is no worse than currently discounted in financial asset prices. In the case of US Treasuries, the bond rally also has a cyclical component, with yields now down to levels more consistent with the softer pace of growth indicated by the ISM Manufacturing index and the recent softening trend in US data surprises (Chart 6). Yet with US monetary policy and financial conditions still highly accommodative, the odds still favor some improvement in the current trend-like pace for US GDP growth that will, eventually, begin to put moderate upward pressure on Treasury yields again. Chart 6Low UST Yields Are Not Just A coronavirus Story

Low UST Yields Are Not Just A coronavirus Story

Low UST Yields Are Not Just A coronavirus Story

Chart 7Global Yields Were Due For A Corrective Pullback

Global Yields Were Due For A Corrective Pullback

Global Yields Were Due For A Corrective Pullback

A similar message is given when we look at global bond yields, more generally. Our Duration Indicator continues to improve alongside rebounding global economic sentiment, signaling cyclical upward pressure on yields (Chart 7) – assuming, of course, that the hit to Chinese growth from the coronavirus outbreak is no worse than currently discounted in financial asset prices. Bottom Line: Efforts to contain the China coronavirus outbreak risk creating the outcome that investors feared most in 2019 from the US-China trade war – weaker Chinese growth and a severe disruption to global supply chains. Global bond yields have plunged as investors have piled into safe haven assets and priced in additional monetary easing from major central banks. Some of that decline in yields, however, may be a repricing of future rate hike probabilities with central banks like the Fed and ECB rethinking their inflation mandates and how to achieve them. How Much China Weakness Is Priced Into Global Bond Yields? The China coronavirus outbreak, and the response to contain it, represents a potentially severe hit to Chinese – and global – economic growth. A lot of comparisons have been made to the 2003 SARS outbreak to try and find a comparable past event. However, as our colleagues at BCA Research Emerging Markets Strategy have noted, China’s economy is so much larger now, rendering comparisons of the economic impact from SARS to that of the coronavirus far less meaningful.1 For example, China’s GDP at purchasing power parity accounts for 19.3% of world GDP compared to 8.3% in 2002 before the SARS outbreak occurred. China’s share of the global consumption of various industrial metals has surged, as well, from between 10-20% in 2002 to 50-60% today. A simple alternative way to measure the impact of any virus-driven slowing of Chinese economic growth would be to calculate the reduction in full-year 2020 GDP growth relative to consensus forecasts. In this sense, the comparison is made to current expectations rather than to a past episode – an approach that should be far more relevant for predicting the response of financial asset prices today. For example, the Bloomberg consensus expectation for Chinese nominal GDP growth for all of 2020 is currently 7.2%. Using that rate and the level of nominal GDP from 2019, we can calculate an expected level for nominal GDP for 2020. We can then make some simplifying assumptions for the impact on full-year growth from an extended period of lost output from the quarantines, government-ordered factory shutdowns and extended holidays, travel bans, etc. Assuming that one full month of expected nominal GDP growth is lost (i.e. 1/12th of the expected increase in the level of nominal China GDP), the full-year growth rate falls to 6.6% Assuming that two full months of expected nominal GDP growth are lost, the full year growth rate falls to 6.0% Global bond yields now reflect a considerable slowdown of Chinese economic activity from the coronavirus, representing between 1-2 months of expected full-year 2020 nominal GDP growth that will be lost. The last time that Chinese nominal GDP growth fell to a sub-7% pace was back in 2015 (Chart 8). The Caixin manufacturing PMI reached a low of 47.2 then, 3.9 points below the current level of 51.1. The level of global bond yields, using our “Major Countries” GDP-weighted aggregate, was at 0.72% - similar to today’s level. Global growth ex-China was also at similarly subdued levels in 2015 (i.e. the US ISM manufacturing index was below 50). Chart 8Global Yields Already Priced For A 2015-Type Slowdown In China

Global Yields Already Priced For A 2015-Type Slowdown In China

Global Yields Already Priced For A 2015-Type Slowdown In China

Chart 9New Stimulus Measures In China Are Inevitable

New Stimulus Measures In China Are Inevitable

New Stimulus Measures In China Are Inevitable

We conclude from this admittedly simple analysis that global bond yields now reflect a considerable slowdown of Chinese economic activity from the coronavirus, representing between 1-2 months of expected full-year 2020 nominal GDP growth that will be lost. The final impact on China economic growth in 2020 will likely be less than that full hit, as Chinese policymakers will surely look to ease monetary and fiscal policy to offset the hit to the economy (Chart 9). While BCA’s China strategists do not currently expect the same magnitude of policy responses as was seen in 2015/16, there will likely be enough to at least partially offset the hit to growth from containing the virus. In terms of timing, the critical point for financial markets – and bond yields – will be when the growth rate of new coronavirus cases peaks. During the 2003 SARS episode, global equity markets bottomed when that number of new cases peaked, which we believe to be a useful template for timing a potential turning point in the “fear narrative” (Chart 10). The number of new coronavirus infections continues to rise, however, suggesting that risk assets and bond yields will likely remain subdued in the near term. Chart 10Markets Bottomed In 2003 When The SARS Infection Rate Peaked

Markets Bottomed In 2003 When The SARS Infection Rate Peaked

Markets Bottomed In 2003 When The SARS Infection Rate Peaked

When that turn does happen, any potential increase in global bond yields will be driven more by unwinding the declines in real yields and term premia of the past two weeks shown earlier in this report in Table 1. Chart 11Only A Pause In The Cyclical Upturn In Yields?

Only A Pause In The Cyclical Upturn In Yields?

Only A Pause In The Cyclical Upturn In Yields?

That suggests a potential rise in the 10-year US Treasury yield of as much as 30bps, and a 23bps increase in the 10-year German bund yield. An additional increase of 5-10bps for both markets could come from higher inflation expectations, although that would likely need to be accompanied by a sizeable rebound in the price of oil and other industrial commodities. We are not seeing signs in our most favored leading indicators – like our global LEI diffusion index or the global ZEW index – suggesting that the next cyclical move in yields will be lower. We acknowledge that the recent fall in yields has gone against our expectations of a moderate grind higher global bond yields in 2020. However, we are not seeing signs in our most favored leading indicators – like our global LEI diffusion index or the global ZEW index – suggesting that the next cyclical move in yields will be lower (Chart 11). We will monitor those indicators in the coming months for any signs of a serious hit to global growth from the coronavirus outbreak. Bottom Line: Maintain a moderate below-benchmark cyclical (6-12 months) stance on overall interest rate duration in global fixed income portfolios. Yields now discount a significant hit to global economic growth from China. This outcome is far from certain, especially if China delivers more aggressive fiscal and monetary policy easing to mitigate the deflationary effects of the public health crisis. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Emerging Markets Strategy Weekly Report, "Coronavirus Versus SARS: Mind The Economic Differences", dated January 30, 2020, available at ems.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The China Syndrome

The China Syndrome

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Feature Everyone’s asset-allocation plans for the year have been disrupted by the novel coronavirus (2019-nCoV). Our view is that, while the virus is serious and will hurt the Chinese and global economy in the short term, it does not change the 12-month structural outlook for financial markets. Once the epidemic is under control (which it is not yet), there will be an excellent buying opportunity for risk assets and for the most affected asset classes. Many commentators have pointed to the lessons from SARS in 2003. Markets bottomed around the time that new cases of the disease peaked (Chart 1). But there are risks with such a simplistic comparison. The US invasion of Iraq happened at the same time – between 19 March and 1 May 2003 – with arguably a bigger impact on global markets. The Chinese economy was much less significant: China represented only 4% of global nominal GDP in 2003 (versus 17% now), 7% of global car sales (35% now), and 10-20% of commodity demand (50-60%). And it is still unclear how similar 2019-nCoV is to SARS: it appears to be spreading more rapidly (Chart 2) but (so far, at least) is less deadly, with a mortality rate of about 2%, compared to 10% for SARS. Recommended Allocation

Monthly Portfolio Update: Going Viral

Monthly Portfolio Update: Going Viral

Chart 1The Lesson From Sars

The Lesson From Sars

The Lesson From Sars

Chart 2But Is Novel Coronavirus Different?

Monthly Portfolio Update: Going Viral

Monthly Portfolio Update: Going Viral

Nonetheless, the basic theory that markets should bottom around the time that new cases and deaths peak is likely to prove correct. With the number of deaths still growing, however, that is not yet the case. Our advice to investors would be not to sell at this point. The hedges we have in our portfolio (overweight cash and gold) should help to cushion any further downside. But, within a few weeks, assets such as EM equities, airline stocks, commodities, or the Australian dollar should look very attractive again (Chart 3). For the next few months, economic data, particularly from China, will be hard to interpret. In 2003, Chinese GDP was reduced by 1.1% because of SARS, according to estimates by the Brookings Institute.1 The global economy is likely to be more heavily impacted this time, given today’s closely integrated supply chains. On the other hand, most academic research shows that consumption and production lost during an epidemic are later made up. Additionally, the Chinese government is likely to respond with easier fiscal and monetary policy. Once the air clears, we think our thesis that the manufacturing cycle bottomed in late 2019 will remain intact. The data over the past few weeks supports this. In Asia, in particular, PMIs for the major emerging economies are back above 50 (Chart 4). Europe’s rebound has lagged a little but, in the key German economy, indicators of business and investor sentiment have bottomed. Demand in the auto sector, crucial for Europe and Japan, is clearly starting to recover. Data in Europe and EM have generally surprised to the upside recently (Chart 5). Chart 3Some Assets May Soon Look Attractive

Some Assets May Soon Look Attractive

Some Assets May Soon Look Attractive

Chart 4Asian And European Data Picking Up

Asian And European Data Picking Up

Asian And European Data Picking Up

Chart 5Positive Surprises

Positive Surprises

Positive Surprises

The theory that markets should bottom around the time that new cases and deaths peak is likely to prove correct. To a degree, the new virus gave investors an excuse to take profits in some over-bought markets. The US equity market, in particular, looked expensive at the start of the year, with a forward PE of 19x. But we would dismiss the common view that investors had become too optimistic. The bull-bear ratio is not elevated (Chart 6), with only 37% of US individual investors at the start of January believing that the stock market would go up over the next six months, not particularly high by historical standards – it has fallen now to 32%. Last year, investors took money out of equity funds, despite strong returns from stocks. In the past – for example 2012 and 2016 – when this happened, it was followed by further gains for equities, as investors belatedly bought into the rally (Chart 7). Chart 6Retail Investors Aren't So Bullish...

Retail Investors Aren't So Bullish...

Retail Investors Aren't So Bullish...

Chart 7...Indeed, They Have Been Selling Stocks

...Indeed, They Have Been Selling Stocks

...Indeed, They Have Been Selling Stocks

On a 12-month investment horizon, therefore, we remain overweight risk assets such as equities and credit, albeit with some hedges. The upside to global growth remains underestimated: the economists’ consensus is for only 1.8% GDP growth in the US and 1.0% in the euro area this year. A combination of accelerating global growth and central banks that will stay dovish should allow equities to outperform bonds over the next 12 months (Chart 8). Chart 8If PMIs Pick Up, Equities Will Outperform

If PMIs Pick Up, Equities Will Outperform

If PMIs Pick Up, Equities Will Outperform

Chart 9First Signs Of US Equity Underperformance?

First Signs Of US Equity Underperformance?

First Signs Of US Equity Underperformance?

Equities: In December, we moved underweight US equities and recommended shifting into more cyclical markets: overweight the euro zone, and neutral on EM, the UK, and Australia. Before the outbreak of 2019-nCoV, this had worked in EM, but less well in Europe (Chart 9). Once the effects of the virus have cleared, we still believe this allocation will outperform as the global manufacturing cycle picks up. But we have a couple of concerns. (1) The recent US/China trade deal will require China to increase imports from the US by a highly unrealistic 83% year-on-year in 2020 (Chart 10). Our China strategists don’t expect this target to be fully met, but think any increase will come from substitution.2 This would hurt exporters in Europe and Asia. (2) The outperformance of euro area equities is very much determined by how banks fare. The headwinds against them continue: the ECB recently decreed that six major banks fall below required capital ratios; loan growth to corporates in the euro area has fallen to 3.2% year-on-year. Much, though, depends on the yield curve (Chart 11). If it steepens, as a result of stronger growth this year, as we expect, bank stocks should outperform, especially since they remain very cheap (the average price/book ratio of euro area banks is currently only 0.65). Chart 10China’s Import Targets Are Unrealistic

Monthly Portfolio Update: Going Viral

Monthly Portfolio Update: Going Viral

Chart 11Bank Performance Depends On The Yield Curve

Bank Performance Depends On The Yield Curve

Bank Performance Depends On The Yield Curve

Once the air clears, we think our thesis that the manufacturing cycle bottomed in late 2019 will remain intact. Fixed Income: Government bond yields have fallen in recent weeks as investors sought cover, with the US Treasury 10-year yield dropping to 1.55%. While it may test last September’s low of 1.46%, we do not see much further room for global yields to fall. They tend to be highly correlated with manufacturing PMIs, which we expect to rise over the next 12 months (Chart 12). Also, we see the Fed staying on hold this year, not cutting rates twice, as the market is now pricing in. This mildly hawkish surprise should push up rates (Chart 13). We continue to prefer credit over government bonds. Our global fixed-income strategists consider that, from a valuation standpoint, US high yield, and UK investment grade and high yield are the most attractive (Chart 14).3 Chart 12Rates Move In Line With PMIs

Rates Move In Line With PMIs

Rates Move In Line With PMIs

Chart 13What If The Fed Doesn't Cut Rates?

What If The Fed Doesn't Cut Rates?

What If The Fed Doesn't Cut Rates?

Chart 14US Junk Looks Most Attractive

Monthly Portfolio Update: Going Viral

Monthly Portfolio Update: Going Viral

Currencies: Defensive currencies such as the yen, Swiss franc, and US dollar have benefitted from the recent risk-off move. We see this as temporary. Once investors refocus on growth, the US dollar should start to depreciate again (the DXY index did fall by 3% between September and early January). The dollar is a counter-cyclical currency. It is 15% overvalued relative to PPP (Chart 15). It is also very momentum-driven – and, since December, momentum has pointed to depreciation and continues to do so (Chart 16). Chart 15Dollar Is 15% Overvalued...

Dollar Is 15% Overvalued...

Dollar Is 15% Overvalued...

Chart 16...And Momentum Has Moved Against USD

...And Momentum Has Moved Against USD

...And Momentum Has Moved Against USD

Commodities: Industrial metals prices had started to pick up over the past few months, reflecting the stabilization of Chinese growth (Chart 17). How they fare from now will depend on: (1) how sharply Chinese growth slows as a result of 2019nCoV, and (2) how much stimulus the Chinese government rolls out to offset this. Given the degree of decline in some commodity prices (zinc down by 16% since mid-January, and copper by 9%, for example), there should be an attractive buying opportunity in these assets over coming weeks. Gold has proved to be a handy hedge against geopolitical risks (Iran) and unexpected tail risks (the coronavirus), rising by 4% year-to-date. We continue to believe it has a useful place in investors’ portfolios as a diversifier and hedge, particularly in a world of very low interest rates where cash is unattractive (Chart 18). The oil price has been hit by the disruption to air travel in January, but supply remains tight (and OPEC is likely to cut supply further in response to the demand shock).4 As long as economic growth picks up later this year, we see the crude oil price recovering over the coming months. Chart 17Metals Reflect Chinese Growth

Chinese Slowdown Will Weigh On Metal Prices Metals Reflect Chinese Growth

Chinese Slowdown Will Weigh On Metal Prices Metals Reflect Chinese Growth

Chart 18Gold Attractive With Bond Yields So Low

Gold Attractive With Bond Yields So Low

Gold Attractive With Bond Yields So Low

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com Footnotes 1 Please see Globalization and Disease: The Case Of SARS, Jong-Wha Lee and Warwick J. McKibbin, Brookings Discussion Paper No. 156, available at https://www.brookings.edu/wp-content/uploads/2016/06/20040203-1.pdf 2 Please see China Investment Strategy Weekly Report “Managing Expectations,” dated 22 January 2020, available at cis.bcaresearch.com 3 Please see Global Fixed Income Strategy Weekly Report “How To Find Value In Corporate Bonds,” dated 21 January 2020, available at gfis.bcaresearch.com 4 Please see Commodity & Energy Strategy Weekly Report “Expect OPEC 2.0 To Cut Supply In Response to Demand Shock,” dated 30 January 2020, available at ces.bcaresearch.com GAA Asset Allocation

Highlights The coronavirus scare is the catalyst for the recent correction, not the cause. The true cause is that the stock market had reached a point of groupthink-triggered instability and therefore needed the slightest catalyst to correct. Bond yields will stay depressed for (at least) the first half of 2020. Long-term investors should use corrections to overweight equities versus bonds, provided bond yields stay near or below current levels. The pound and UK-exposed investments will come under near-term pressure as UK/EU trade deal tensions ratchet up. But ultimately, UK-exposed investments will enjoy a major leg up later this year if both the UK and EU blink. Feature Chart of the WeekThe Next Up-Leg In The Pound And UK-Exposed Investments Will Occur Later In 2020

The Next Up-Leg In The Pound And UK-Exposed Investments Will Occur Later in 2020

The Next Up-Leg In The Pound And UK-Exposed Investments Will Occur Later in 2020

Corrections, Catalysts, And Coronavirus Markets have suffered a correction, begging the question: what caused it? The question is a good one, because identifying the cause can help to inform our response. Yet the danger is that the knee-jerk narrative pinpoints the catalyst rather than the true cause. In which case our response will be wrong too. For example, consider the following two narratives: Tree foliage collapses because of 40 mph winds. Tree foliage collapses because it is autumn. The first narrative is exciting, satisfying, and headline grabbing, but it only pinpoints the catalyst for the foliage collapse: the puff of wind. The second explanation is dull and less newsworthy, but it pinpoints the true cause: in autumn, tree foliage is unstable. Likewise, the coronavirus scare is the catalyst for the recent correction. The true cause is that the stock market had reached a point of groupthink-triggered instability and therefore needed the slightest catalyst to correct. The catalyst could have come from anywhere at any time. If it hadn’t been the coronavirus scare, it would have been the next worry… or the one after that. On January 9 in Markets Are Fractally Fragile we warned that usually cautious value investors had become momentum traders – undermining market liquidity and stability. When this happens, there is a two in three chance of a tactical reversal (Chart I-2). Chart I-2When Markets Are Fractally Fragile, There Is A 2 In 3 Chance Of A Tactical Reversal

When Markets Are Fractally Fragile, There Is A 2 In 3 Chance Of A Tactical Reversal

When Markets Are Fractally Fragile, There Is A 2 In 3 Chance Of A Tactical Reversal

We also warned that the bond yield 6-month impulse – the change in the change – had recently become a severe 100 bps headwind to growth. At this severity of headwind, there is a nine in ten chance that bond yields have reached a near-term peak (Chart I-3). Chart I-3When The Bond Yield 6-Month Impulse Becomes A Severe Headwind, There Is A 9 In 10 Chance Of A Near-Term Peak In Yields

When The Bond Yield 6-Month Impulse Becomes A Severe Headwind, There Is A 9 In 10 Chance Of A Near-Term Peak In Yields

When The Bond Yield 6-Month Impulse Becomes A Severe Headwind, There Is A 9 In 10 Chance Of A Near-Term Peak In Yields

In combination, we warned that equities would underperform bonds by about 4 percent on a tactical horizon. Now that this anticipated correction has happened, what next? Long-term investors should use corrections to overweight equities versus bonds. First, irrespective of coronavirus – or any other catalyst – the recent severe headwind to growth from the bond yield impulse suggests that bond yields will stay depressed for (at least) the first half of 2020. Second, the good news is that the ultra-low bond yields justify and underpin the valuation of equities. Hence, at the current level of bond yields, long-term investors should use corrections to overweight equities versus bonds. Brexit Is “Done”. Or Is It? Rumour has it that Boris Johnson will banish the word Brexit from the UK government lexicon after January 31, because Brexit is now “done”. Good luck with that. When Britain wakes up bleary-eyed on Saturday February 1, what will have changed? Not a lot. The UK will have lost its voice and votes in the EU decision making institutions. Yet in practical terms nothing will have changed, because the UK and EU will enter an 11-month ‘standstill’ transition period in which existing arrangements will continue: the free movement of people, financial contributions, and full access to the single market without tariffs or customs checks. The Conservative government made a manifesto pledge not to extend the 11-month transition, so the more important question is: what will change when the standstill period ends on December 31? The answer depends on what sort of trade deal the UK and EU can negotiate in the limited space of 11 months. Or indeed whether they can negotiate a trade deal at all. Therein lies the problem. A free trade deal with the EU will require a mutual commitment to a ‘level playing field’. If the UK wants to diverge on food standards, environmental protection, labour rights, and state aid – as the Brexit purists yearn – then there is zero chance that the EU will agree to a free trade deal. This leaves two options, neither of which is appealing. The first is for the UK to end the 11-month standstill period without a trade deal. Technically, this would not be ‘no deal’ because the withdrawal agreement would still bind both sides on citizens’ rights, financial contributions, and arrangements for Northern Ireland. A free trade deal with the EU will require a mutual commitment to a ‘level playing field’. However, for UK companies, the option of ending the standstill period without a trade deal would constitute a painful dislocation from the single market involving tariffs and customs checks. It would also hurt the EU economies most exposed to the UK, notably Ireland and the Netherlands. Moreover, a full customs and tariff border in the Irish Sea would endanger the very existence of a ‘United’ Kingdom which included Northern Ireland. The second option is for the UK to accept a trade deal on EU terms, recognising that the EU is the larger and more economically powerful party in the negotiation. The EU will offer the UK a tariff-free and quota-free trade deal conditional on strict level playing field conditions where the UK chooses to diverge from EU standards, combined with a mechanism to adjudicate on any level playing field disputes. Though economically better than no trade deal at all, the Brexit purists would claim it isn’t Brexit. Meanwhile, even without tariffs and quotas, UK companies whose just-in-time supply chains depended on the EU would still suffer disruption, as the level playing field was policed at every border crossing. So this option would satisfy nobody in the UK. The bigger practical problem is a lack of time to leave the EU regulatory orbit smoothly. Nobody believes that eleven months is enough time to implement a system in Northern Ireland that prevent a hard border in the Irish Sea; or indeed to implement a new UK immigration system if free movement were to end at the end of 2020. So what’s the resolution? The answer is the same as it has always been for Brexit – a gradual ratcheting up of tension ahead of a hard deadline to focus minds and force progress. Followed by a ‘fudged resolution’ at the eleventh hour in which both sides blink – because neither side is prepared to go over the cliff-edge. Recall that to get the withdrawal agreement over the line, the UK blinked by allowing Northern Ireland to be treated differently; but the EU also blinked by allowing the withdrawal agreement to be reopened. And once this happened, the pound and UK-exposed investments enjoyed a major leg up (Chart I-1 and Chart I-4-Chart I-7). Chart I-4The FTSE 250 Is A UK-Exposed ##br##Investment

The FTSE 250 Is A UK-Exposed Investment

The FTSE 250 Is A UK-Exposed Investment

Chart I-5The FTSE 100 Is Not A UK-Exposed Investment

The FTSE 100 Is Not A UK-Exposed Investment

The FTSE 100 Is Not A UK-Exposed Investment

Chart I-6UK General Retail Is A UK-Exposed Investment

UK General Retail Is A UK-Exposed Investment

UK General Retail Is A UK-Exposed Investment

Chart I-7UK Clothing And Accessories Is Not A ##br##UK-Exposed Investment

UK Clothing And Accessories Is Not A UK-Exposed Investment

UK Clothing And Accessories Is Not A UK-Exposed Investment

In the next fudged resolution, the UK could blink by retaining full regulatory alignment with the EU in most areas for a little while longer, and where it doesn’t the EU could blink by becoming flexible in its interpretation of ‘level playing field’. Obviously, nobody would call this an extension to the transition, but the UK would, in most practical terms, still be in the single market on January 1 2021. UK-exposed investments will enjoy their next major leg up later this year In this playbook, the pound and UK-exposed investments will come under near-term pressure, as UK/EU trade deal tensions ratchet up. But ultimately, UK-exposed investments will enjoy their next major leg up later this year if both the UK and the EU blink (Chart I-8). Chart I-8The Pound Still Has A Brexit Discount

The Pound Still Has A Brexit Discount

The Pound Still Has A Brexit Discount

Fractal Trading System* There are no new trades this week. The rolling 1-year win ratio now stands at 62 percent. Chart I-9EUR/GBP

EUR/GBP

EUR/GBP

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Cyclical Recommendations Structural Recommendations

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Don't Mention The C-Word Or The B-Word

Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights BCA’s “Golden Rule of Bond Investing” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, also works in China. The relationship between unexpected changes in China’s de facto short-term policy rate and government bond yields has been surprisingly strong over the past decade. Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The persistent historical gap between economic growth and bond yields in China makes it difficult to forecast the structural outlook for yields using conventional methods. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, we believe that bond yields are more likely to structurally rise than fall. Over the coming 6-12 months, investors should underweight Chinese government bonds versus Chinese equities and onshore corporate bonds. Within a regional government bond portfolio, however, investors should overweight USD-hedged China versus US and developed markets ex-US, as well as in unhedged terms. Feature Last year’s inclusion of Chinese onshore government and policy bank bonds in the Bloomberg Barclays Global Aggregate Index was a significant milestone of China’s journey to internationalize its capital markets. Other bond benchmark providers have since followed suit, highlighting that the trend of increased passive exposure to Chinese assets is likely to continue. Over the past year, the bulk of the market discussion concerning the addition of China to the major bond indices has focused on estimating the size of potential capital inflows that could be triggered and the related impact on onshore bond yields. By contrast, comparatively little work has been done to analyze the core drivers of Chinese government bond yields, and how they compare to the factors that influence yields in the developed markets that dominate the bond indices. This Special Report attempts to fill a hole in the analysis of Chinese bonds. This Special Report attempts to fill that hole in the analysis of Chinese bonds. We look at the predictability of China’s government bond market through the lens of BCA’s “golden rule” framework, and find a surprisingly strong relationship between changes in China’s de facto short-term policy rate and government bond yields. We then present our cyclical (6-12 month) and secular outlooks for government yields given this relationship, and conclude by presenting four specific investment recommendations pertaining to China’s fixed-income market with two audiences in mind: mainland/onshore investors who are focused on returns in unhedged RMB terms, and global fixed-income investors who are primarily focused on hedged US-dollar regional bond exposure. The Golden Rule Of Bond Investing, With Chinese Characteristics In a July 2018 Special Report,1 BCA’s Chief US Bond Strategist, Ryan Swift, elegantly distilled the cyclical US government bond call into a simple question: During the next 12-months, will the Federal Reserve move interest rates by more or less than what is currently priced into the market? Chart 1The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

Ryan argued that a predictive framework for US Treasury returns built around the answer to this question has historically worked so well that it should be referred to as the “Golden Rule of bond investing” (Chart 1). In a follow-up report, our Global Fixed Income Strategy service confirmed that the Golden Rule also largely works in non-US developed market economies, with the exception of Japan due to the absence of any meaningful fluctuation in policy rates over the past two decades.2 The Golden Rule provides a very strong framework to aid fixed-income investors with their cyclical (i.e. 6-12 month) asset allocation decisions, by quantitatively linking government bond returns relative to cash – in other words, the excess return earned by taking duration risk - to policy rate “surprises” compared to what is discounted in shorter-term money markets. The practical application is that a decision to allocate to longer-maturity government bonds is reduced to a bet on whether a central bank will adjust policy rates by more or less than the market expects. The first question we address in this report is to what degree does the Golden Rule apply in China (in yield space rather than in return space), along with an explanation of any differences that may exist. However, we must first note why the Golden Rule of bond investing works, particularly in the US. The first reason is that there is a strong relationship between the US 3-month T-bill rate and Treasury yields of all other maturities. Conceptually, all fixed income investors have a choice when buying US government bonds: they can purchase a 3-month Treasury bill and simply perpetually roll over the position as it matures, or they can purchase a Treasury bond of a longer maturity. This means that yields on longer maturity Treasury bonds simply reflect investor expectations for the average 3-month T-bill rate over the life of the bond, plus some positive risk premium to compensate for the inherent uncertainty of the path and tendency of short-term yields. This helps explain the close link between cyclical changes in 3-month T-bill rates and yields on longer maturity Treasurys. Chart 2In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

The second reason for the Golden Rule’s success is that there is a very tight relationship between the effective Fed funds rate and the 3-month T-bill rate. While it is the (higher) discount rate that is the theoretical no-arbitrage ceiling for the 3-month rate, in practice T-bill rates trade extremely close to the Fed funds rate (Chart 2). This means that Fed funds rate “surprises” (relative to traded market expectations) are akin to surprises in the 3-month rate, which in turn strongly influence the expected future path of short-term interest rates and thus yields on longer maturity Treasurys. In China, we noted in a February 2018 Special Report3 that the 7-day interbank repo rate is now the de jure short-term policy rate in China following the establishment of an interest rate corridor system in 2015. Chart 3 presents our first test of the Golden Rule in China (in yield space rather than in return space), by plotting the annual change in the level of Chinese government bond yields alongside the 7-day repo rate “surprise” over the past year from 2010 to the present. Here, we use the first principal component of zero coupon Chinese government bond yields to represent the average level of yields (rather than selecting a particular maturity), and we use the 12-month RMB swap rate (versus 7-day repo) to represent market expectations for the policy rate. The chart highlights that the fit is good, as measured by a 50% R-squared between the two series. However, deviations in the relationship do exist, with the most notable exception having occurred in 2017: Chinese government bond yields rose considerably more than what the annual surprise in the 7-day repo rate would have suggested. Chart 3In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

Chart 4...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

Chart 4 helps resolve a good portion of the 2017 discrepancy, and clarifies the link between Chinese monetary policy and government bond yields. Chart 4 is similar to Chart 3, except that it replaces the 7-day repo rate surprise with that of 3-month SHIBOR (which trades very closely to the 3-month repo rate). The chart illustrates an even closer fit between the two series (with an R-squared close to 80%), and shows that the 3-month SHIBOR surprise does a meaningfully better job at explaining the 2017 rise in Chinese government bond yields. The Golden Rule of bond investing works surprisingly well in China. The fact that the annual surprise in 3-month SHIBOR has done a better job at predicting changes in bond yields over the past decade underscores that the 3-month repo rate is the de facto short-term policy rate in China, a point that we have made in several previous reports. We have noted that the spike in the 3-month/7-day repo rate spread that occurred in late-2016 and lasted until mid-2018 happened because of China’s crackdown on shadow banking activity. This crackdown caused a funding squeeze for China’s small & medium banks, which caused a material rise in lending rates and government bond yields. This episode highlights that future changes in the 3-month repo rate are likely to reflect both underlying changes in net liquidity provided to large commercial banks (measured by the 7-day repo rate), and any dislocations in the interbank market that have the potential to push up lending rates and government bond yields. Bottom Line: BCA’s “Golden Rule” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, works for China as well – using the correct measure of the PBOC policy rate. This provides a useful investment framework for Chinese government bonds, which are now significant part of major global bond market benchmarks. The Cyclical Outlook For Chinese Government Bond Yields Given the establishment of the relationship between Chinese short-term interbank rates and government bond yields detailed above, we are now able to more precisely discuss the likely cyclical trajectory of Chinese government bond yields as a function of Chinese monetary policy. Two opposing forces have the potential to affect China’s government bond market this year. The first, a stabilization and modest rebound in Chinese economic activity, may exert upward pressure on yields due to expectations of eventual policy tightening. The second, continued attempts by the PBoC to ease corporate lending rates, may exert downward pressure on yields as it will reflect not just easy but easier monetary conditions. Yields at the long-end are likely to move modestly higher this year, at most. For investors, the raises the obvious question of whether Chinese government bond yields are likely to move up, down, or trend sideways this year. In our view, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. Yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. There are two reasons why yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. The first is that the PBoC is generally a reactive central bank and has historically lagged a pickup in economic activity, as illustrated in Chart 5. The chart shows the historical path of 3-month SHIBOR in the year following a bottom in economic activity in 2009, 2012, and 2015, and makes it clear that there has been no precedent for a significant rise in interbank rates in the first nine months of an economic recovery. The 2012 episode did see a very sharp rise in 3-month SHIBOR once the PBoC shifted into tightening mode, but we doubt that this experience will be repeated again unless economic growth accelerates much more aggressively than we expect. The second reason why we expect yields at the short-end of the curve to remain muted this year is because any additional easing by the PBoC is likely to be focused on reducing corporate lending rates, not interbank rates. Chart 6 highlights that while there is a strong correlation between changes in Chinese government bond yields and average lending rates in the economy, the former leads the latter. In the past, this relationship has existed because changes in interbank rates have coincided with reductions in the now obsolete benchmark lending rate, with the former usually occurring earlier than the latter. But in a scenario where the PBoC reduces the loan prime rate (LPR) and keeps net banking sector liquidity roughly constant, the extremely tight relationship shown in Chart 4 suggests that short-term bond yields are unlikely to be affected by a reduction in lending rates. Any meaningful decline in short-term yields below short-term interbank rates would simply prompt banks to stop buying these bonds. Chart 5The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

Chart 6Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Chart 7China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

Additional easing by the PBoC does have the potential to impact the long-end of the government bond curve if investors view these actions as a sign that interbank rates will remain low for some time. This view is reinforced by the fact that China’s yield curve is not particularly flat, and thus has room to move lower. However, Chart 7 also shows that China’s yield curve, defined here as the second principal component of zero coupon Chinese government bond yields, is positively correlated with the relative performance of investable Chinese equities. This suggests that there is a procyclical element to the curve. We suspect that this procyclical element will dominate a potential decline in expectations for future short-term interest rates, but that yields at the long-end are likely to move modestly higher this year, at most. Bottom Line: Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The Secular Outlook For Chinese Government Bond Yields A common approach to forecasting the likely structural trend for nominal government bond yields is to estimate the trajectory of real long-term potential output growth and to add the monetary authority’s inflation target. This framework is based on the idea that interest rates are in equilibrium when the cost of borrowing is roughly equal to nominal income growth, a condition that results in no change in the burden to service existing debt. Chart 8China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

Based on this framework, we would expect Chinese government bond yields to trend down over time, or possibly flat if the PBoC were to tolerate higher inflation over the coming decade. Chart 8 illustrates the IMF’s forecast of falling real potential growth in China over the coming several years, which is consistent with a shift in the composition of growth from investment to consumption as well as China’s looming demographic crisis. But Chart 9highlights an obvious problem with applying this framework to forecast the secular trend in Chinese government bond yields: over the past decade, yields have persistently averaged below actual nominal GDP growth, both in China and in the developed world. In the latter case, it is an open question whether this will continue to be true in the future, but in China’s case it is clear that government bond yields have little connection (in magnitude) to the pace of GDP growth. This reflects the longstanding strategy of Chinese policymakers to promote investment via persistently low interest rates, as has occurred in other manufacturing and export-oriented Asian economies (Chart 10). Chart 9...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

Chart 10In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice