Gov Sovereigns/Treasurys

Dear Client, BCA’s New York conference takes place next week on September 26-27, and I look forward to meeting some of you there. Because of the conference, our next report will come out on October 3. Dhaval Joshi Highlights If the WTI crude oil price breached $70, Germany’s net export growth would suffer a short-term relapse. If the WTI crude oil price breached $90, Germany’s economic growth would suffer a much longer setback. The WTI crude oil price is now trading at $59, well below even the first pain threshold. Hence, at the moment, the oil price ‘spike’ is a minor irritant rather than a major risk to a German (and European) economic rebound in the fourth quarter. Stay overweight the Eurostoxx50 versus the Shanghai Composite and Nikkei225. If the WTI price stabilises well below $70, we intend to initiate an overweight to the DAX versus global equities. German bunds are a structural short relative to U.S. T-bonds. Feature Chart of the WeekOil Price Oscillations Have Explained German Growth Oscillations With A Spooky Precision

Oil Price Oscillations Have Explained German Growth Oscillations With A Spooky Precision

Oil Price Oscillations Have Explained German Growth Oscillations With A Spooky Precision

It is touch and go whether Germany suffered a technical recession through the second and third quarters.1 We will know in about six weeks’ time, once the statisticians have finished crunching the numbers. But for the financial markets, this is old news. A technical recession in Germany during the second and third quarters is already baked in the market cake. The economy and financial markets are entwined in a perpetual dance. In a dance, sometimes one person decides the steps and sometimes the other person does, but the couple always moves together. And so it is with the economy and markets. The ZEW indicator of (German) economic sentiment recently hit its lowest level since 2011, and the performance of the DAX versus global equities has moved in near perfect lockstep (Chart I-2). Chart I-2A German Recession Is Already Baked In The Market Cake

A German Recession Is Already Baked In The Market Cake

A German Recession Is Already Baked In The Market Cake

Some people try to predict the movement of markets based on the releases of backward-looking economic data or even supposedly real-time economic data, such as sentiment surveys. Good luck with that. The markets instantaneously discount those releases. To predict the markets, the key question is: what will the future releases look like? If the German economy rebounds in the fourth quarter, then the stark underperformance of the DAX constitutes a compelling buying opportunity versus other equity markets. That said, a new potential risk has emerged: the spike in the crude oil price. Germany Is Highly Sensitive To The Oil Price Europeans are large importers of energy, with 55 percent of all energy needs met by net imports. Moreover, the volume of energy they import tends to be price inelastic. Hence, when energy prices plunge, it boosts net exports and thereby it boosts growth. Conversely, when energy prices soar – as they have recently – it depresses net exports and thereby it depresses growth.2 98 percent of Germany’s consumption of oil depends on imports. This is especially true for Germany whose energy import dependency, at 65 percent, is well above the European average. The most important energy source is still oil which accounts for over a third of Germany’s primary energy use (Chart I-3). Moreover, 98 percent of Germany’s consumption of oil depends on imports.3 Chart I-3Germany Is Highly Sensitive To The Oil Price

A German Recession Is Baked In The Market Cake. Now What?

A German Recession Is Baked In The Market Cake. Now What?

Most of Germany’s oil consumption is for transport. On a timeframe of decades, the planned decarbonisation of all sectors by 2050 should all but eliminate fossil oil from German energy consumption. However, on a timeframe of quarters, oil consumption for transport is highly inelastic and non-substitutable. Hence, in recent years, swings in the oil price have always caused swings in Germany’s net exports (Chart I-4). Based on this excellent relationship, a likely rebound in German net exports in the fourth quarter would be threatened if the WTI crude price reached and stayed in the mid $70s. Chart I-4Swings In The Oil Price Cause Swings In Germany's Net Exports

Swings In The Oil Price Cause Swings In Germany's Net Exports

Swings In The Oil Price Cause Swings In Germany's Net Exports

For Economic Growth, The Oil Price Impulse Is What Matters Empirically, we have found that the German economy is much more sensitive to the oil price than other European economies (Chart I-5 and Chart I-6). This could be because other drivers of the economy such as credit developments are less significant in Germany. Chart I-5Germany Is More Sensitive To The Oil Price...

Germany Is More Sensitive To The Oil Price...

Germany Is More Sensitive To The Oil Price...

Chart I-6...Than Other European ##br##Economies

...Than Other European Economies

...Than Other European Economies

Most analysts argue that it is the change in the oil price that is relevant for the economy. This is obviously correct for the impact on inflation, which is, by definition, the change in a price. However, it is incorrect to argue that the change in the oil price drives economic growth. Instead, it is the impulse of the oil price – the change in its change – that drives economic growth. To understand why, consider a simplified example. Let’s say a 20 percent drop in the oil price added to Germany’s net exports, causing the economy to grow 1 percent. In the following period, another 20 percent drop in the oil would cause the economy to grow again by 1 percent, so growth would stay unchanged. On the other hand, if the oil price dropped by 10 percent, the economy would still grow, but now at a reduced rate of 0.5 percent. Therefore somewhat paradoxically, though the oil price has declined by 10 percent, growth has slowed. This is because the second drop in the price (10 percent) is less than the first (20 percent) – which means the tailwind impulse has faded. Now let’s put in the actual numbers for the oil price’s 6-month impulse. The period ending around June 2019 constituted a severe headwind impulse. This is because a 30 percent increase in the oil price followed a 40 percent decline in the previous period, equating to a headwind impulse of 70 percent.4 Allowing for typical lags of a few months, this severe headwind impulse is a likely culprit, or at least a contributing culprit, for Germany’s slowdown during the second and third quarters. As the Chart of the Week compellingly illustrates, oscillations in the oil price’s 6-month impulse have explained the oscillations in Germany’s 6-month economic growth with a spooky precision. Empirically, other explanatory factors are not needed. The period ending June 2019 constituted a severe headwind impulse from the oil price. Now the good news. Until the last few days, the oil price’s severe headwind impulse had eased – and this fading of the headwind strongly suggested a rebound in German economic growth during the fourth quarter and beyond. This raises a crucial question: to what level would the crude oil price have to spike for the maximum headwind impulse to return, and thereby extinguish the chance of such a rebound? By reverse engineering the price from the maximum headwind impulse, the answer is the WTI crude price at $90. Pulling all of this together, the first pain threshold is WTI breaching $70, at which Germany’s net export growth could suffer a short-term relapse. The second and greater pain threshold is WTI breaching $90, at which Germany’s economic growth could be stifled for much longer. Having said all that, WTI is now trading at $59, well below even the first pain threshold. Hence, at the moment, this is a minor irritant rather than a major risk to a German (and European) economic rebound. Stay overweight the Eurostoxx50 versus the Shanghai Composite and Nikkei225. And in the coming week or so, if the WTI price stabilises well below $70, we intend to initiate an overweight to the DAX versus global equities. The ECB Fired A Dud So much for the ECB’s promise to ‘shock and awe’ the markets. The bazooka ended up firing a dud! Unlimited QE is not really unlimited when the ECB’s asset purchase program is running close to its individual issuer limit, and its country composition cannot deviate too far from the ECB’s capital key. QE is nothing more than a signal of intent to keep policy interest rates ultra-low for a protracted period. In any case, QE is nothing more than a signal of intent to keep policy interest rates ultra-low for a protracted period. But once the markets have fully discounted this intent – as they have in the euro area and Japan – the monetary policy armoury is effectively out of ammunition (Chart I-7-Chart I-10). So it is not surprising that the ECB fired a dud. Chart I-7Monetary Policy Is Exhausted In The Euro Area...

Monetary Policy Is Exhausted In The Euro Area...

Monetary Policy Is Exhausted In The Euro Area...

Chart I-8...But The U.S. Still Has ##br##Ammunition

...But The U.S. Still Has Ammunition

...But The U.S. Still Has Ammunition

Chart I-9Monetary Policy Is Exhausted In Japan...

Monetary Policy Is Exhausted In Japan...

Monetary Policy Is Exhausted In Japan...

Chart I-10...But China Still Has Ammunition

...But China Still Has Ammunition

...But China Still Has Ammunition

Some people counter that there are even more exotic monetary policy options in the pipeline, such as ‘helicopter money’. However, as Mario Draghi correctly pointed out, “giving money to people in whatever form is not a monetary policy task, it’s a fiscal policy task.” Helicopter money might be a step too far, but its notion encapsulates the shape of things to come in Europe. With euro area monetary policy exhausted, the baton is passing to fiscal policy. The upshot is that in a bond portfolio, German bunds are a structural short relative to U.S. T-bonds. Fractal Trading System* Although we are structurally overweight Italian long-dated BTPs, the 130-day fractal dimension is signalling that the pace of the rally is now technically extended and therefore vulnerable to a countertrend correction. This week’s trade recommendation is to express this via a short position in the Italian 10-year BTP, setting a profit target of 3 percent with a symmetrical stop-loss. In other trades, short the U.S. 10-year T-bond quickly achieved its profit target, while short financial services versus market reached the end of its holding period in slight loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

Italy 30-Year Govt. Bond

Italy 30-Year Govt. Bond

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 We define a technical recession as two consecutive quarters of contraction in real GDP. 2 Energy dependence = (imports – exports) / gross available energy. 3 According to the Federal Institute for Geosciences and Natural Resources. 4 The 6-month steps in the WTI crude oil price were $74.15, $45.21, and $58.24. The first change equated to a 40 percent decrease and the second change equated to a 30 percent increase. So the 6-month impulse was 70 percent. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

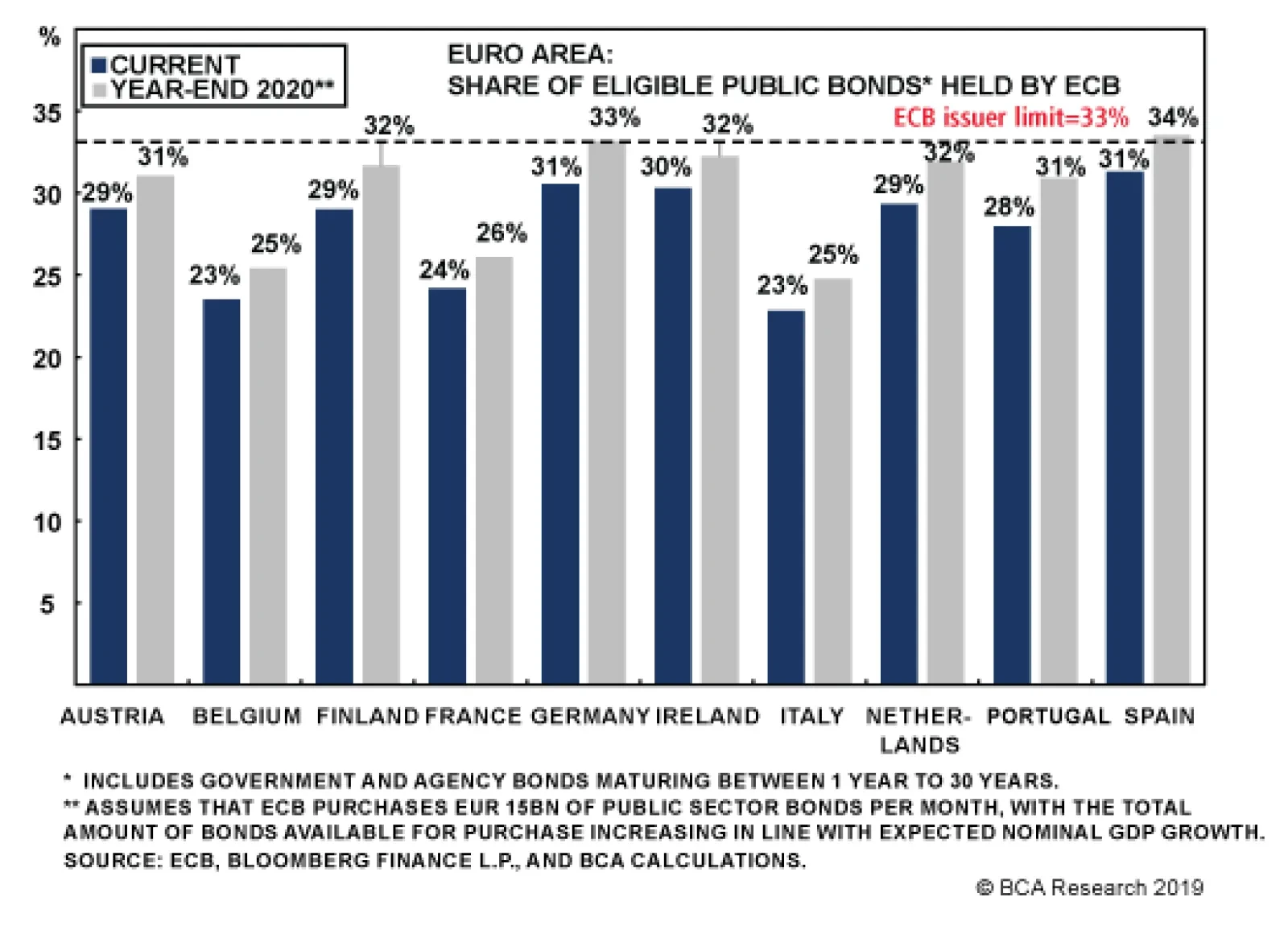

Looking ahead, the ECB will run into some difficulties on running a “QE Forever” program given the current self-imposed constraints on the APP. The ECB cannot own more than 33% of the outstanding pubic debt of any single country. At the moment, the ECB…

Highlights Fed: The Fed will cut rates by 25bps this week, accompanied by a balanced message on future moves given firm domestic U.S. growth amid global uncertainties. This could trigger additional near-term increases in Treasury yields if the market prices out future expected rate cuts. More likely, higher Treasury yields will manifest via higher inflation expectations, as investors price in Fed accommodation amid the recent acceleration of realized inflation. ECB: The ECB’s easing package last week fell short of market expectations, as policymakers face the operational constraints of cutting already-negative interest rates and restarting asset purchases. Portfolio Recommendations: Return to below-benchmark on overall interest rate duration on a tactical (0-3 months) basis, with global leading economic indicators bottoming and U.S.-China trade tensions easing. Within country allocation, maintain an underweight stance on U.S. Treasuries versus German Bunds on a USD-hedged basis. Feature Dear Client, Next week, we will be publishing a joint Special Report on the U.K. with our colleagues at BCA Foreign Exchange Strategy and BCA Geopolitical Strategy. The report will be sent to clients this Friday, September 20, on the regular publishing day of the other two services. Thus, Global Fixed Income Strategy clients will be receiving their next report a few days early. We will return to our usual publishing schedule on Tuesday, October 1. Best regards, Rob Robis Chart of the WeekA Fundamental Bottoming Of Bond Yields

A Fundamental Bottoming Of Bond Yields

A Fundamental Bottoming Of Bond Yields

The bond market has been full of surprises over the past year, and the price action so far this month is no exception. The benchmark 10-year U.S. Treasury yield has climbed +42bps from the September 3 inter-day low of 1.43%, while the 10-year German Bund yield also rose by +23bps over that same period, even as the ECB announced a fresh set of policy easing measures last week. There are several possible reasons for this increase in yields: profit-taking in deeply overbought government bond markets; global central bankers delivering incrementally less dovish surprises; and hints of progress in the U.S-China trade negotiations. We prefer a more fundamental explanation – bond markets may be sniffing out an end of the 2019 global growth downturn. The message from the improving trend in both our global leading economic indicator (LEI) and our Duration Indicator is that global growth (Chart of the Week) is stabilizing, which should help boost government bond yields from current depressed levels. The recent attack on oil facilities in Saudi Arabia does represent a near term risk to this potentially more optimistic narrative on the world economy. Our colleagues at BCA Geopolitical Strategy do expect a military response from the U.S., although U.S. President Trump will attempt to keep it limited. A full-blown U.S.-Iran conflict would likely further raise the risk premium on global oil prices, potentially creating the kind of major spike that has preceded past global recessions – an outcome that Trump would prefer to avoid heading into an election year. For now, we prefer to heed the message from our cyclical indicators, which point to additional increases in bond yields in the next few months. For now, we prefer to heed the message from our cyclical indicators, which point to additional increases in bond yields in the next few months, led by some improvement in inflation expectations and a reduction in the amount of monetary easing discounted in markets – most notably, in the U.S. We now see less of a need for the cautious near-term view on overall duration exposure that we’ve maintained since the announcement of fresh U.S. tariffs on China in early August, especially given the recent easing of U.S.-China trade tensions ahead of the next round of talks in early October. Thus, we recommend shifting to a below-benchmark stance on overall portfolio duration on a tactical (0-3 months) basis, bringing that view back in line with our cyclical (up to 12 months) call, which has remained bearish on bonds (see the table on Page 12 for changes to our model bond portfolio). FOMC Preview: 25bps This Week, With No Promises After That While there is still a lot of investor angst over the underlying health of the global economy, the “recession narrative” appears to be receding. The New York Fed’s recession probability model, based on the slope of the U.S. Treasury curve, has seen the odds of a 2020 downturn fall from a peak of 42% in August to 32% today. At the same time, there has been a sharp drop in the number of Google searches involving the word “recession” (Chart 2). Chart 2Hold Off On That Inevitable Recession

Hold Off On That Inevitable Recession

Hold Off On That Inevitable Recession

A similar message can be seen in financial markets, where classic risk-off/save haven assets like gold, and the VIX index have pulled back a bit from recent highs (Chart 3). Government bond volatility measures like the MOVE index remain elevated, though, as fixed income markets continue to price in expectations of low inflation and easier monetary policy – especially in the U.S. Chart 3Yields Discount A Lot Of Risk-Aversion

Yields Discount A Lot Of Risk-Aversion

Yields Discount A Lot Of Risk-Aversion

This week’s FOMC meeting, including an update to the committee’s own growth and rate forecasts, will shed light on the Fed’s latest thinking. A modest downgrade of the Fed’s U.S. growth projections is likely given the downturn in the U.S. manufacturing sector. Yet with U.S. financial conditions easing (Chart 4) and the U.S. consumer remaining confident and willing to spend – purely a function of a robust labor market and despite media coverage of the growing threat of recession – the risk is that the Fed does not end up downgrading its growth projections much. Already, the annual growth rate of core U.S. retail sales is up to a solid 5.3%, after the nearly 10% (annualized) surge seen over the June-August period. Chart 4U.S. Domestic Economic Growth Is Rebounding

U.S. Domestic Economic Growth Is Rebounding

U.S. Domestic Economic Growth Is Rebounding

Chart 5U.S. Inflation Is Accelerating Inflation Could Use A Boost

U.S. Inflation Is Accelerating Inflation Could Use A Boost

U.S. Inflation Is Accelerating Inflation Could Use A Boost

A similar story exists in realized U.S. inflation measures, the majority of which are accelerating. Core CPI in August rose to 2.4% on year-over-year basis, after a surge of 3.4% annualized over the previous three months – the fast such rate over such a short window since May 2006 (Chart 5). Core PCE inflation has also picked up, and is now up 1.6% year-over-year and 2.2% – above the Fed’s 2% target – on a 3-month annualized basis. Wage growth, measured using average hourly earnings, continues to grow at a solid 3.6% year-over-year rate. Given these readings, combined with a persistently low unemployment rate, the FOMC is likely to make few (if any) changes to its inflation forecasts at this week’s meeting. Chart 6Stretched Treasury Yields Can Keep Climbing

Stretched Treasury Yields Can Keep Climbing

Stretched Treasury Yields Can Keep Climbing

Given the underlying firm trends in the U.S. economic and inflation data, odds are low that the Fed will deliver an incremental dovish surprise to markets. The reverse is more likely. At the same time, the Fed is keenly aware of the fragility of non-U.S. economic growth, and U.S. financial markets, amid the persistent drag on U.S. manufacturing activity and business confidence from the U.S.-China tariff war. Once again, Fed Chair Jerome Powell will have to thread the needle with a message that sounds neither too dovish nor too hawkish. We fully expect another 25bp rate cut to be delivered this week. However, we also expect forward guidance to reflect a balanced outlook for a strong U.S. economy juxtaposed against concern for non-U.S. growth. In other words, the same message the Fed has been giving the markets since mid-year. Given the current stretched momentum of Treasury yields/prices, amid large overweight positioning according to measures like the J.P. Morgan client duration survey, any sign of a less dovish Fed should trigger some increase in Treasury yields (Chart 6). This is especially true with the U.S. Overnight Index Swap (OIS) curve still discounting 71bps of rate cuts over the next twelve months – an amount of easing that is unlikely to be delivered. In our view, though, the bigger near-term threat of rising Treasury yields will not come from the Fed being too hawkish, but from appearing too dovish amid accelerating inflation and firm U.S. economic growth. In our view, though, the bigger near-term threat of rising Treasury yields will not come from the Fed being too hawkish, but from appearing too dovish amid accelerating inflation and firm U.S. economic growth. Market-based inflation expectations remain depressed, with the 10-year TIPS breakeven rate now at 1.68%. That is well below levels consistent with the Fed’s 2% PCE inflation target despite the persistent tightness of the U.S. labor market and the acceleration seen in realized inflation measures. We recommend that clients shift back to a below-benchmark duration stance in the U.S. this week, while maintaining the maximum exposure to TIPS versus nominal Treasuries to position for higher inflation expectations that will also result in some steepening of the Treasury yield curve. Bottom Line: The Fed will cut rates by 25bps this week, accompanied by a balanced message on future moves given firm domestic U.S. growth amid global uncertainties. This could trigger additional near-term increases in Treasury yields if the market prices out future expected rate cuts. More likely, higher Treasury yields will manifest via rising inflation expectations, as investors price in Fed accommodation amid the recent acceleration of realized inflation. ECB: Take It To The Limit One More Time Last week’s much anticipated policy easing announcement by the European Central Bank (ECB) was comprehensive in scope, but disappointing in size. Short-term interest rates were cut, but only through a modest -10bp reduction in the overnight deposit rate. The Asset Purchase Program (APP) was restarted, but only at a pace of €20bn per month, well off the €80bn peak pace of the 2015-18 APP (Chart 7). Chart 7A Relatively Modest Easing Package From The ECB

A Relatively Modest Easing Package From The ECB

A Relatively Modest Easing Package From The ECB

Those new initiatives fell short of the consensus forecast of a -20bp cut and €30bn of new APP. The ECB did introduce some tools to help struggling euro area banks - allowing some portion of banks’ excess reserves to Chart 8No Wonder There Is Disagreement With The ECB

No Wonder There Is Disagreement With The ECB

No Wonder There Is Disagreement With The ECB

avoid the negative deposit rate (a.k.a. “tiering”) and extending the maturity of the TLTRO III program announced earlier this year from two to three years. Nonetheless, the overall stimulus package fell short of a “big bazooka” that did not break new ground on policy instruments (like buying equities in the APP). The biggest change from previous ECB easing initiatives was by making these new programs “open-ended”, with no specific expiration date. Instead, the asset purchases and lower interest rates would be maintained until euro zone inflation sustainably converged to the ECB’s inflation target of just under 2%. With the ECB’s newly revised forecasts calling for headline inflation to only climb to 1.5% by 2021, the new program has already been mockingly branded “QE Forever” by those who do not expect inflation to ever return to 2%. A big reason why the ECB was unable to deliver a bigger package was the disagreement within the ECB Governing Council on the need for more aggressive stimulus. Prior to last week’s meeting, several ECB officials publically voiced their reluctance to restart asset purchases and deliver deeper interest rate cuts, believing that they would have little impact on future euro area growth and inflation. While the opposition to fresh bond buying came from predictable sources like Germany and Austria, there was also an unprecedented level of public dissent after the ECB meeting, with the heads of the Dutch, Austrian and French central banks publically expressing doubts on the effectiveness of the new easing measures. This came after outgoing ECB President Mario Draghi noted in his post-meeting press conference last week that the consensus on restarting APP within the Governing Council was so broad that “there was no need to take a vote.” Given the diverging economic and inflation trends within the euro area, it should not be a surprise that a broad consensus within the Governing Council was hard to produce. For example, Germany is suffering through a much deeper manufacturing downturn than the other major euro area countries, judging by the trends in manufacturing PMIs (Chart 8). At the same time, Germany has a much lower unemployment rate and higher inflation rates than Italy and Spain. Focusing only on the German manufacturing downturn when setting monetary policy may produce results that are too stimulative – especially when the services sides of euro area economies appear in better shape (most notably in Germany). The ECB will run into some difficulties on running a “QE Forever” program of asset purchases given the current self-imposed constraints on the APP. Looking ahead, the ECB will run into some difficulties on running a “QE Forever” program of asset purchases given the current self-imposed constraints on the APP. The ECB cannot own more than 33% of the outstanding pubic debt of any single country (counting both sovereign debt and government agency bonds). At the moment, the ECB ownership shares are below that 33% threshold for the largest countries, based on our calculations that are presented in Chart 9. Chart 9"QE Forever" Is Not Credible Under Current Constraints

The World Is Not Ending: Return To Below-Benchmark Portfolio Duration

The World Is Not Ending: Return To Below-Benchmark Portfolio Duration

However, that 33% limit will be threatened by the end of 2020 in several countries: the ECB will buy €15bn per month of government bonds under the new APP1 the ECB continues to allocate its bond buying in line with the size of each country (as determined by the ECB Capital Key) the stock of debt eligible for the APP expands at the same rate as consensus forecasts of nominal GDP growth Draghi also noted in his press conference that there was “relevant headroom to go on for quite a long time at this rhythm without the need to raise the discussion about limits.”2 We disagree, as our calculations show that the 33% threshold will be at threat of being reached by the end of next year in Germany, Spain, the Netherlands, Finland & Ireland (see the gray bars of Chart 9). If the ECB truly wants to commit itself to buying bonds until inflation returns to just under 2%, however long that takes, then one of three things must happen: the ECB must raise the issuer limit from 33% the ECB must allocate its bond buying using different weights than the Capital Key the supply of available government debt must increase through easier fiscal policy. Chart 10The ECB Will Have To Raise Issuer Limits To BoJ Levels

The ECB Will Have To Raise Issuer Limits To BoJ Levels

The ECB Will Have To Raise Issuer Limits To BoJ Levels

Of those three options, altering the country weights away from the Capital Key is the most politically contentious, as it would involve more purchases from countries with weaker government finances, like Italy and Spain. Raising the issuer limit from 33% is a more realistic option, as that is a completely self-imposed rule with no economic grounds, although it raises the risk of the ECB bond ownership approaching Bank of Japan type levels (Chart 10). Solving the ECB’s “headroom” constraint by issuing more government debt through fiscal expansion is the one option that could truly help Europe get out of its low inflation trap. Yet that is also an option fraught with political tension in places like Germany where keeping low levels of government debt has been a politically popular choice. With the new ECB President, Christine Lagarde, set to take over from Draghi in November, the policy debate within Europe will turn toward the need for more fiscal stimulus. Already, there have been media reports suggesting the German government is considering new stimulus measures to boost a Germany economy that is now in a technical recession. Solving the ECB’s “headroom” constraint by issuing more government debt through fiscal expansion is the one option that could truly help Europe get out of its low inflation trap. Chart 11Inflation Expectations & Bund Yields Are Stabilizing

Inflation Expectations & Bund Yields Are Stabilizing

Inflation Expectations & Bund Yields Are Stabilizing

If the ECB’s APP capacity issues are not eventually resolved, then the market will soon come to the realization that there can be no “QE Forever”. Combined with the known limitations on pushing policy rates deeper into negative territory - for fears of reaching a “reversal rate” that will cause banks to horde cash and make fewer loans - there is limited scope for additional declines in euro area bond yields from the deeply depressed current levels under the new policy announcements made last week. For now, we continue to favor overweighting core euro area government debt in global fixed income portfolios, on a currency-hedged basis. Despite the persistent negative yields on offer, those can be transformed into positive-yielding assets when the currency exposure is swapped into U.S. dollars. Furthermore, the so-called “convexity buying” of longer-dated euro area government bonds by asset-liability managers like insurers and pension funds will continue to anchor the long-end of euro area yield curves (Chart 11) – although that same factor can potentially hyper-charge a rise in yields as convexity buying turns into convexity selling if the economic fundamentals were to swing in a bond-bearish fashion (which is a topic we plan on covering in a future report). Bottom Line: The ECB’s easing package last week fell short of market expectations, as policymakers face the operational limits of cutting already-negative interest rates and restarting asset purchases. Yet for now, the economic/inflation backdrop in Europe remains bond friendly. Maintain a strategic overweight stance on Germany versus the U.S. in global government bond portfolios, with Bunds still supported by ECB buying and with USD-hedged Bund yields continuing to offer a yield pickup over Treasuries. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The other €5bn per month is assumed to go towards the purchases of corporate debt. 2 The full transcript of Draghi’s press conference can be found here: https://www.ecb.europa.eu/press/pressconf/2019/html/ecb.is190912~658eb51d68.en.htm The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The World Is Not Ending: Return To Below-Benchmark Portfolio Duration

The World Is Not Ending: Return To Below-Benchmark Portfolio Duration

Recommendations Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Duration: The ebbing of U.S. / China trade tensions and swing toward positive data surprises are enough for us to re-initiate a below-benchmark duration recommendation, on both tactical (0-3 month) and cyclical (6-12 month) time horizons. While not our base case, a continued deterioration in the Manufacturing PMI or CRB Raw Industrials, or a significant appreciation of the U.S. dollar would cause us to question our view. Credit: Corporate debt levels are elevated, but still-low inflation expectations will ensure that monetary conditions remain accommodative for the time being. Easy Fed policy will support interest coverage ratios and prevent banks from tightening lending standards. Stay overweight corporate bonds, focusing on the Baa and high-yield credit tiers. Fed: The Fed will cut rates by 25 basis points tomorrow and Chairman Powell will do his best to sound dovish and prevent a tightening of financial conditions. Core inflation has strengthened in recent months, but the Fed needs to see a rebound in inflation expectations before turning hawkish. Feature Move Back To Below-Benchmark Portfolio Duration The sensitivity of bond yields to U.S./China trade policy was on full display last week. President Trump took significant steps to de-escalate tensions between the two nations, delaying the October 1st tariff hike and scheduling talks between principal negotiators for October. The result is that the bond market sold off dramatically. The 10-year Treasury yield rose from 1.55% at the start of the week to 1.90% as of last Friday. As we go to press, the yield has fallen back to 1.85% in response to the drone attacks in Saudi Arabia and resulting spike in oil prices. Chart 1Has The Tide Turned?

Has The Tide Turned?

Has The Tide Turned?

Our Geopolitical Strategy service discussed the near-term outlook for U.S. / China trade negotiations in last week’s report.1 Our main takeaway is that the President has shifted into dealmaker mode, hoping to secure some “wins” in advance of next year’s election. Talk of a looming recession in the mainstream media is doubtless also encouraging the President to adopt a more conciliatory strategy. Our political strategists view a comprehensive U.S. / China trade agreement as unlikely. But if the U.S. and China can reach a détente where tariffs are no longer rising every few months and the immediate threat to economic growth dissipates, then U.S. bond yields have a lot of upside. Chart 1 shows that the 10-year Treasury yield fell much more sharply in recent months than would have been expected given the U.S. economic data. The chart also shows that economic data are now beating expectations for the first time since February. Positive data surprises usually coincide with rising Treasury yields, and the chart suggests that yields still have a lot of catching-up to do. The de-escalation of trade tensions and shift in data surprises is enough for us to remove our tactical “at benchmark” duration stance, which had been in place since August 6. Investors should keep portfolio duration low on both tactical (0-3 month) and cyclical (6-12 month) time horizons. Risks To The Duration View There are three main risks to our below-benchmark duration positioning. The first is that the global manufacturing data – Manufacturing PMIs and the CRB Raw Industrials index – have not yet rebounded (Chart 2). We have written extensively about why we expect a bounce-back before the end of the year, and an ebbing of U.S. / China trade tensions will only speed that process along, as firms gain more confidence in the outlook and initiate long-delayed investments.2 However, until we actually see the data improve we cannot be certain. It’s notable, and concerning, that the ratio between the CRB Raw Industrials index and Gold did not increase alongside Treasury yields during the past week (Chart 2, bottom panel). If the dollar continues to appreciate as Treasury yields move up, it will limit how high yields rise. The second risk to our view comes from the dollar. If it continues to appreciate as Treasury yields move up, it will limit how high yields rise. Treasury yields can increase alongside a stronger dollar when global leading indicators are improving, as was the case in the second half of 2016 (Chart 3). But a strong dollar will eventually undermine global growth and cap the upside in yields. Chart 2Risk 1: Global Manufacturing Still Weak

Risk 1: Global Manufacturing Still Weak

Risk 1: Global Manufacturing Still Weak

Chart 3Risk 2: Stronger Dollar

Risk 2: Stronger Dollar

Risk 2: Stronger Dollar

The third risk is that the recent attack on Saudi oil installations prompts a military response from the U.S. government that escalates into all-out war. The lesson from the oil crash of 2014 is that any negative effects on the U.S. consumer from a spike in the oil price will be offset by greater investment from U.S. energy firms. However, if the situation dissolves into a significant military conflict, then U.S. bonds would benefit from flight to quality flows. Our Geopolitical and Commodity teams discussed the still-unfolding situation in a Special Alert yesterday.3 Bottom Line: The ebbing of U.S. / China trade tensions and swing toward positive data surprises are enough for us to re-initiate a below-benchmark duration recommendation, on both tactical (0-3 month) and cyclical (6-12 month) time horizons. While not our base case, a continued deterioration in the Manufacturing PMI or CRB Raw Industrials, or a significant appreciation of the U.S. dollar would cause us to question our view. Corporate Bonds: Weak Balance Sheets Vs. Easy Money The slope of the yield curve is an important and useful indicator for corporate bond investors. In fact, our research has demonstrated that corporate bond excess returns versus Treasuries tend to be highest early in the recovery when the yield curve is steep. On the flipside, we’ve also shown that an inverted yield curve is often a good signal to scale back exposure.4 Corporate balance sheets are highly levered today, as they were in the mid-1990s. For this purpose, our preferred measure of the yield curve has been the 3-year/10-year slope, calculated on a monthly basis using average daily closing values. Chart 4 shows this slope with vertical lines denoting the first inversion of each cycle. Notice that we have not yet received an inversion signal from this measure in the current cycle, but it is getting close. Chart 4Yield Curve & Corporate Spreads

Yield Curve & Corporate Spreads

Yield Curve & Corporate Spreads

Even if we get an inversion signal in the next few months, Chart 4 reveals an interesting contrast between the mid-2000s cycle and the mid-1990s cycle. In the mid-1990s, 3/10 curve inversion was an excellent signal to reduce corporate credit exposure. Spreads widened almost immediately, and didn’t peak until four years later. Conversely, spreads continued to tighten for another year after the yield curve inverted in 2006. So how should we view the current cycle in relation to these prior two episodes? Should we expect further outperformance after the yield curve inverts, as in the mid-2000s? Or should we prepare to reduce corporate bond exposure as soon as the yield curve sends a signal, as in the 1990s? Balance Sheets Are In Poor Health … Chart 5Firms Carrying A lot Of Debt

Firms Carrying A lot Of Debt

Firms Carrying A lot Of Debt

The first thing to consider is how corporate balance sheets stack up compared to each of these prior two episodes. Chart 5 makes it apparent that balance sheets are highly levered today, as they were in the mid-1990s. Net debt-to-EBITDA for the median high-yield firm in our dynamic bottom-up sample is above 4.0x, even higher than in the late 1990s. Similarly, the median firm’s debt-to-assets ratio is reminiscent of the 1990s. Chart 5 clearly shows that balance sheets were in poor health in the 1990s, and are in a similar state today. This is in sharp contrast to the mid-2000s, when balance sheets were pristine. The sole exception is interest coverage, which remains robust (Chart 5, bottom panel). This is the result of still-accommodative monetary policy (more on this below). … But The Monetary Environment Is Supportive While today’s corporate balance sheets have more in common with the mid-1990s than the mid-2000s, today’s monetary environment looks more like the mid-2000s, and is probably even more supportive. Chart 6Supportive Monetary Environment: Reminiscent Of The Mid-2000s

Supportive Monetary Environment: Reminiscent Of The Mid-2000s

Supportive Monetary Environment: Reminiscent Of The Mid-2000s

Chart 6 shows that when the yield curve inverted in the 1990s, banks’ commercial & industrial (C&I) lending standards were on the cusp of tightening, as were the terms that banks offered on C&I loans. In contrast, C&I lending standards and loan terms continued to ease for some time after the curve inverted in the mid-2000s. Today, C&I lending standards and C&I loan terms are both in “net easing” territory. But most crucially, inflation expectations are extremely depressed (Chart 6, bottom panel). Low inflation expectations mean that the Fed must ensure that monetary policy stays accommodative until inflation expectations are re-anchored at levels closer to its target. Accommodative Fed policy will keep firms’ interest costs down, and give lenders the confidence to extend credit, even if firms are already loaded with debt. Bringing it all together, we find that both credit quality metrics and monetary indicators help explain the corporate default rate (Chart 7). Our top-down measure of gross leverage (total debt over pre-tax profits) lines up well with the default rate over time, but has diverged during the past few years (Chart 7, top panel). Meanwhile, C&I lending standards also correlate tightly with the default rate, and this relationship continues to track (Chart 7, panel 3). Chart 7Drivers Of The Corporate Default Rate

Drivers Of The Corporate Default Rate

Drivers Of The Corporate Default Rate

Overall, we find the divergence between gross leverage and the default rate concerning, and reminiscent of 2007/08 when it predicted a surge in the default rate. However, unlike in 2007/08, lending standards are moving deeper into “net easing” territory and interest coverage remains steady. Considering all the evidence, we are inclined to remain bullish on corporate credit spreads for the time being. Yes, corporate debt levels are a worry, as they were in the 1990s. But, with inflation expectations still very low, the Fed has a strong incentive to keep policy easy. Historically, banks do not tighten lending standards unless the monetary environment is restrictive. Our sense is that, in this cycle, banks will turn a blind eye to corporate debt levels until inflation expectations rise and the Fed moves interest rates into restrictive territory. Credit Investment Strategy Chart 8Focus On The Baa And High-Yield Credit Tiers

Focus On The Baa And High-Yield Credit Tiers

Focus On The Baa And High-Yield Credit Tiers

Our relatively bullish assessment of the credit cycle means that we will continue to abide by the spread targets we introduced in February.5 To obtain those targets we calculated the median 12-month breakeven spread for each credit tier during periods when the yield curve was very flat (less than 50 bps), but not yet inverted.6 We then converted those breakeven spreads into option-adjusted spread targets using current index duration and the current index credit rating distribution. Chart 8 shows that investment grade spreads are slightly above target, but this is only due to the cheapness of Baa-rated debt. Aaa, Aa and A-rated credits all trade at spreads below our targets, and we recommend focusing investment grade exposure on the Baa space. Chart 8 also shows that high-yield spreads are much more attractive relative to target. This is partly because the negatively convex nature of high-yield debt means that index duration fell sharply as bonds rallied this year (Chart 8, bottom panel). All else equal, lower index duration means that more spread widening is required before investors see losses. Thus, spreads appear more attractive. Bottom Line: Corporate debt levels are elevated, but still-low inflation expectations will ensure that monetary conditions remain accommodative for the time being. Easy Fed policy will support interest coverage ratios and prevent banks from tightening lending standards. Stay overweight corporate bonds, focusing on the Baa and high-yield credit tiers. FOMC Preview: Fed Will Do Its Best To Stay Dovish The results of this week’s FOMC meeting will be made public tomorrow afternoon. A 25 basis point rate cut is widely anticipated, and we expect that is what will be delivered. A 25 basis point rate cut is widely anticipated, and we expect that is what will be delivered. Judging from recent remarks, Fed Chairman Jerome Powell is well aware that easy financial conditions will encourage a recovery in economic growth.7 He also understands that in order for financial conditions to stay easy, the market must continue to believe that monetary policy is supportive. We therefore think that Chairman Powell will do everything he can to prevent a hawkish surprise following tomorrow’s FOMC statement and press conference. However, the Chairman cannot control the placement of each FOMC participant’s interest rate forecast (or “dot”), and there is a risk that the end-of-2019 forecasts don’t fall enough to appease markets. Chart 9 shows the fed funds rate along with a projection based on current pricing in the fed funds futures market. It shows that the market expects a 25 bps rate cut tomorrow, followed by one more 25 bps cut before the end of the year. We don’t expect the majority of FOMC participants to forecast such a dovish outcome, but as long as a significant number of participants forecast one more cut before the end of the year, a hawkish surprise should be avoided. Chart 9Can The Fed Avoid Sounding Hawkish?

Can The Fed Avoid Sounding Hawkish?

Can The Fed Avoid Sounding Hawkish?

Case in point, the Fed avoided a hawkish surprise following the June meeting. Heading into that meeting the market was priced for an end-of-2019 funds rate of 1.75% (denoted by the ‘X’ in Chart 9). The June FOMC dots show that 7 FOMC participants expected a similar outcome (also shown in Chart 9). If around 7 participants place their 2019 dot in the 1.50%-1.75% range following tomorrow’s meeting, it should be enough to prevent a hawkish surprise. Will Strong Inflation Sway The Fed? There has been some speculation that the recent spate of strong inflation data might prevent the Fed from delivering a sufficiently dovish message. We think this is unlikely. It’s true that core inflation has rebounded sharply, but inflation expectations remain downtrodden (Chart 10). At this juncture, the Fed is principally concerned with re-anchoring inflation expectations near target levels. It may require an overshoot of the actual inflation target to achieve this goal. Investors should focus more on inflation expectations to assess Fed policy going forward. Chart 10Still Well Anchored?

Still Well Anchored?

Still Well Anchored?

Chart 11Unsustainable Uptrend in Goods

Unsustainable Uptrend in Goods

Unsustainable Uptrend in Goods

Further, if we dig into the details of the recent inflation prints, we find some reason to believe that the recent uptrend is not sustainable. Chart 11 shows that a substantial portion of inflation’s rise has been driven by the core goods component, which tracks non-oil import prices with a lag of about 1½ years (Chart 11, panel 2). For their part, import prices have already rolled over and will continue to decelerate unless we see a significant depreciation of the dollar (Chart 12). Chart 12Import Prices & The Dollar

Import Prices & The Dollar

Import Prices & The Dollar

Bottom Line: The Fed will cut rates by 25 basis points tomorrow and Chairman Powell will do his best to sound dovish and prevent a tightening of financial conditions. Core inflation has strengthened in recent months, but the Fed needs to see a rebound in inflation expectations before turning hawkish. Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Weekly Report, “Trump’s Tactical Retreat”, dated September 13, 2019, available at gps.bcaresearch.com 2 Please see U.S. Bond Strategy / Global Fixed Income Strategy Weekly Report, “Where’s The Positive Carry In Bond Markets?”, dated August 20, 2019, available at usbs.bcaresearch.com 3 Please see Commodity & Energy Strategy / Geopolitical Strategy Special Alert, “Attacks On Critical Infrastructure In KSA Raise Questions About U.S. Response”, dated September 16, 2019, available at ces.bcaresearch.com 4 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 5 Please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 6 The 12-month breakeven spread is the spread widening required before a corporate bond sees losses versus a duration-matched Treasury bond on a 12-month horizon. It can be calculated roughly as the option-adjusted spread per unit of duration. 7 https://www.cnbc.com/2019/09/06/watch-fed-chairman-jerome-powells-qa-in-zurich-live.html Fixed Income Sector Performance Recommended Portfolio Specification

Highlights The ECB loaded a bazooka, and core Eurozone yields rose: The ECB surprised dovishly last Thursday, and European bond yields duly fell … for an hour. Then they began to back up as fast as they fell, and when Friday’s trading ended, only Greek and Italian yields were lower than where they started. The market action supports our contention that things are not so bad, assuming the worst-case trade scenarios do not materialize: Underpinned by a robust labor market, the U.S. should have little trouble growing at a trend pace over the next twelve months. Meanwhile, the global economy may be in the process of turning. Reversals within the U.S. equity market have gotten a lot of attention so far this month, but it’s too early to claim that a broad factor inflection is underway: If global growth prospects have bottomed, defensive sectors’ outperformance is due to reverse, which will cause havoc for momentum strategies. It is premature to call for a value revival, however. Feature Maybe long Treasury yields aren’t going to zero after all. After bottoming just below 1.43% the day after Labor Day, the 10-year Treasury yield surged 45 basis points across eight sessions as of Friday’s lunchtime peak (Chart 1). The move has been enough to retrace better than three-fifths of its steep slide from mid-July to the beginning of September, but relative to the extended plunge from 3.24% that began last November, the bounce barely registers. Chart 1Up, Up And Away

Here Comes The Cavalry (Again)

Here Comes The Cavalry (Again)

Chart 2Pulled Lower By Expected Rate Cuts...

Pulled Lower By Expected Rate Cuts...

Pulled Lower By Expected Rate Cuts...

The takeaway is that it’s important to keep the moves in context. Just as the collapse in Treasury yields didn’t indicate that the U.S. economy was headed for an imminent recession, their modest, if rapid, recovery doesn’t indicate that all the dark clouds are gone from the horizon. From a purely domestic perspective, the 180-basis-point (“bps”) peak-to-trough decline in the 10-year Treasury yield unfolded nearly step-for-step with an equivalent decline in the expected fed funds rate twelve months out (Chart 2). Since a 1.25% target fed funds rate this time next year is incompatible with our view of the economy, we expect rates will move higher. The ECB committed itself to accommodation for longer than markets had expected; … Chart 3...And Other Sovereign Yields

...And Other Sovereign Yields

...And Other Sovereign Yields

Chart 4Better Times Ahead?

Better Times Ahead?

Better Times Ahead?

The Treasury market doesn’t exist in a vacuum, however. Yield moves in similarly-rated sovereign bonds have an effect on Treasuries, and declines in European sovereign yields have exerted a gravitational pull all year long (Chart 3). The backup in yields that followed the ECB’s dovish surprise on Thursday suggests that Eurozone sovereign bond markets may have bought the rumor and sold the news. If global growth is in the process of bottoming, as global leading indicators suggest, falling yields would run counter to the fundamental backdrop (Chart 4). You May Fire When Ready, Draghi To judge by the spate of columns urging helicopter-style accommodation measures, the expectations bar for the European Central Bank’s long-awaited September meeting had been set pretty high. The cut in the ECB’s deposit facility rate to -0.5% from -0.4%, with provisions to mitigate the pressure negative rates exert on banks, was in line with the market consensus, as was a resumption of quantitative easing. Investors did not foresee that the ECB would embark on open-ended bond purchases, however, a plan quickly labeled “QE Infinity.” The ECB also dumped its no-hikes-before-mid-2020 guidance – now it won’t move until the inflation outlook “robustly” moves toward its 2% target – and lengthened the maturities on TLTRO loans while lowering their rates.1 The surprise indicated that the ECB is taking the slowdown seriously, at home (most evident in Germany, which is flirting with recession after a quarter-over-quarter GDP contraction) and abroad. It is premature to declare the action a flop, as headline writers were quick to do, citing the evanescent decline in core bond yields and the euro, because QE impacts are subject to several factors. Sovereign yields can rise on QE announcements if markets judge the impact of relaxed inflation vigilance will outweigh the impact of the entry of a new, price-insensitive buyer to the marketplace. As long as real yields fall, the central bank will have achieved its goal. … if it develops that the incremental accommodation wasn’t necessary, equities and spread product should reap the benefits. U.S. investors are mostly concerned with the impact on global markets and the global economy. Even if nominal sovereign yields have bottomed and competitive devaluation has neutered the currency channel, incremental easing should boost risk assets’ prospects, via pushing incumbent sovereign holders into spread product (the portfolio balance effect), promoting business and consumer confidence, incentivizing bank lending, and nudging other central banks (like Denmark’s, which immediately cut its policy rate in response) to ease monetary conditions themselves (Figure 1). On those counts, we view the ECB’s surprise as modestly improving the prospects for risk assets. TINA is alive and well. Figure 1Monetary Policy And The Economy

Here Comes The Cavalry (Again)

Here Comes The Cavalry (Again)

The Employment Situation We have repeatedly cited the robustness of the labor market as a reason for not giving up on the U.S. economy, or equities and spread product. If expanding payrolls and increasing compensation can keep consumption growing at just a 2% clip, the probability of a U.S. recession, and of an equity bear market and a new default cycle, is fairly slim. If the labor market isn’t as strong as we’ve judged, more defensive portfolio positioning may be in order. Since the beginning of the second quarter, the monthly employment situation reports have revealed a slowing in hiring activity, halting the quickening that stretched from last year through the end of the first quarter (Chart 5). The slowing trend is less concerning than it might appear to be on its face. The current expansion, 122 months old and counting, is the longest on record, and now that it has already drawn considerable numbers of people back into the labor force and back to work, it has become increasingly difficult to find and attract new workers. Even the current monthly pace of job gains, 156,000 over the last three months, still puts downward pressure on the unemployment rate, as it takes less than 110,000 new jobs to maintain the status quo. With net job gains outpacing new entrants into the labor force, wages should rise. Average hourly earnings rose 3.2% in August on a year-over-year basis, though the 0.4% month-over-month gain suggests they may be about to challenge the top end of the tight 3.1-3.2% range that’s prevailed all year. Investors’ and economists’ patience with the Phillips Curve is increasingly wearing thin, as they wait for the decline in the unemployment rate to show up in wage gains, but we consider the underlying supply-demand relationship to be immutable. The prime-age employment-to-population ratio hit an 11-year high in August, and is solidly back in the middle of the range that has prevailed over the 30 years that female participation gains have stabilized (Chart 6). Chart 5Slower Payroll Gains...

Slower Payroll Gains...

Slower Payroll Gains...

Chart 6...Will Still Tighten The Labor Market

...Will Still Tighten The Labor Market

...Will Still Tighten The Labor Market

Chart 7The Unkinked Phillips Curve

Here Comes The Cavalry (Again)

Here Comes The Cavalry (Again)

The prime-age employment-to-population ratio is an important measure for the Phillips Curve because it exhibits a consistent linear relationship with wage gains. The fit between the non-employment-to-population ratio (1 minus the employment-to-population ratio) and the employment cost index (Chart 7, top panel) is a little tighter than the fit with average hourly earnings (Chart 7, bottom panel), but both regression equations project an annual increase in wages of 3.3% at the current 20% (1-80%) level, and a 7-bps gain for every 20-bps decline in the prime-age non-employment-to-population ratio. Given that our payrolls model projects a pickup in the pace of hiring (Chart 8, top panel), and the quits rate just moved off of its extended plateau (Chart 9), upward pressure on wages will continue to build. Chart 8Demand For Workers Is Still Solid

Demand For Workers Is Still Solid

Demand For Workers Is Still Solid

Chart 9Movin' On Up

Movin' On Up

Movin' On Up

Bottom Line: Payroll gains are slowing, but they remain robust enough to push the key prime-age employment-to-population ratio higher, and exert upward pressure on wages. Factor Rotation Chart 10Momentum Hits The Wall,...

Momentum Hits The Wall,...

Momentum Hits The Wall,...

Reversals within the U.S. equity market have been drawing increasing amounts of attention, as momentum stocks have hit a wall while long-suffering value stocks have begun to peel themselves off the canvas (Chart 10). We can easily see a scenario in which the momentum factor has a very difficult time, if relative performance shifts from defensive sectors to cyclical sectors as investors begin to perceive that they have been overly pessimistic about the domestic and global business cycle, and cease to hide in bond proxies like Utilities and REITs. Given the defensives’ run of outperformance over the last year, momentum indexes disproportionately favor them over cyclicals. The S&P 500, MidCap 400 and SmallCap 600 Momentum Indexes all show a pronounced defensives bias, with Health Care, Utilities and Real Estate all commanding double their baseline weight in at least one index (Table 1), making S&P’s momentum indexes vulnerable to a defensives-to-cyclicals rotation. Table 1The Dullest Stocks Have Been The Hottest

Here Comes The Cavalry (Again)

Here Comes The Cavalry (Again)

Over the last three years, we have thought a lot about the value factor, asking how it should be defined, which financial statement metrics indicate its presence, and the business and monetary policy cycle backdrops that are most conducive to its outperformance. Low-priced stocks have been in a punishing extended slump versus high-priced stocks since early 2007 (Chart 11), and we think they have yet to bottom. The recent value stock rally has been a function of higher 10-year Treasury yields, and banks’ (which account for an outsized share of popular value benchmarks) recent tendency to trade in lockstep with them. We do not think a two-week backup in yields is the stuff that a genuine value factor inflection point is made of. Chart 11...But The Value Factor Has Yet To Turn

...But The Value Factor Has Yet To Turn

...But The Value Factor Has Yet To Turn

A detailed explanation of our rationale is beyond the scope of this report,2 but the following points summarize our take: The value factor has gotten killed since the crisis, but we doubt that it’s dead. Value has historically treaded water during bull markets, and shined in bear markets. The fed funds rate cycle is the best predictor of value’s relative performance. Value has historically crushed the overall market when monetary policy is restrictive. The most popular style indexes have barely any factor merit. The S&P 500’s Growth and Value indexes are little more than Tech and Financials proxies. Value will shine again, but not until monetary policy is restrictive. If the Fed doesn’t hike the fed funds rate above the equilibrium fed funds rate until 2021, value investors will have to gut out another year-plus of underperformance. Bottom Line: The momentum factor could suffer in the near term if cyclicals reassert primacy over formerly hot defensives. The value factor’s fortunes will not turn for at least another year. Investment Implications We understand the discomfort of investors who feel like ZIRP, NIRP and QE have obliterated normal investing relationships. Disorienting as it has been to see nominal Treasury returns shrivel, the rising tide of negative-yielding bonds is like a surreal detail from a David Lynch movie. The investment world has indeed turned upside-down when investors buy bonds for capital gains to offset the interest they have to pay for the privilege of lending. Austrian School advocates are surely not the only dearly departed investing veterans rolling in their graves. It’s not the environment we wanted, but it’s the environment we got, so we’re going to buck up and do our best to squeeze excess returns out of it. We have to invest in the markets we have, however, not the markets we want. It does neither ourselves nor our clients any good to throw up our hands, bitterly lament our fate and wish ill upon the exponents of the activist, ultra-accommodative approach to central banking that is now in fashion. Some old relationships still apply, and the combination of a quietly improving global economic backdrop with incremental monetary accommodation everywhere one turns is good for risk assets. We continue to recommend that investors resist the urge to get defensive before the excess-return window closes for this cycle. We are not advocating that investors let their guard down, and assume that central banks will be able to keep the plates spinning indefinitely. They will not – monetary interventions are a poor substitute for organic growth in productivity or the size of the working-age population, and so are inefficiently directed fiscal spending programs – but we bet they can through the next quarterly or annual period over which an institutional manager is going to be evaluated. The upshot is that investors should remain especially vigilant for signs of trouble, and be prepared to act more tactically than normal to adjust their portfolios, but shouldn’t de-risk them yet, lest they miss the last of the fat-year returns they’ll need to tide themselves over during the coming lean years. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Targeted longer-term refinancing operations (TLTROs) are ECB loans to banks intended to encourage lending to households and non-financial corporations. 2 Interested readers should see the May 16, 2018 Global ETF Strategy/Equity Trading Strategy Special Report, “Smart-Beta ETF Selection Update – Is Value Still Worth It?,” the October 2018 Bank Credit Analyst Special Report, “Is It Time To Buy Value Stocks?,” and the October 2, 2018 U.S. Investment Strategy Special Report, “When Will Value Work Again?,” available at etf.bcaresearch.com, www.bcaresearch.com and usis.bcaresearch.com, respectively.

Highlights The lack of dollar liquidity has been a tailwind behind the dollar bull market. Going forward, an end to a contraction in the Federal Reserve’s balance sheet should help stem the global shortage of dollars. Outside of a few basket cases, there remains scant evidence that the shortage of dollars has begun to trigger widespread negative feedback loops, symptomatic of a funding crisis. If the global economy picks up steam, a deterioration in the U.S. current account and rising FX reserves will improve the dollar liquidity situation. A trade war remains the key risk to this view. For the remainder of the year, portfolio managers should focus on relative value trades on the crosses rather than outright dollar bets. The European Central Bank’s resumption of quantitative easing could be paradoxically bullish for the euro beyond the near term. For now, stay short the euro versus a basket of petro-currencies. Feature At the center of the global financial architecture is the U.S. dollar and the Federal Reserve. The process behind the creation of dollars is a simple one, which goes as follows: In order to stimulate the U.S. economy, the authorities pursue macroeconomic policies that tend to weaken the dollar, such as lowering rates and/or running a wider fiscal deficit. The central bank helps finance this fiscal deficit via expanding the monetary base (seignorage). The drop in rates causes the yield curve to steepen. This incentivizes banks to lend, which in turn boosts U.S. money supply. As the economy recovers, and demand for imports (machinery, commodities, consumer goods) rises, the current account deficit widens. As a reserve currency, the U.S. trade deficit is settled in dollars. This leads to a flow of greenbacks outside U.S. borders. Wary of losing competitiveness via a rising exchange rate, other central banks will purchase these dollars from the private sector in exchange for local currency. The rise in foreign exchange reserves can be reinvested back into Treasurys and held in custody at the Fed, meaning that the current account deficit (or capital account surplus) finances the budget deficit. Call this an exorbitant privilege. The key question is whether dollar liquidity will ease over the near term or the shortage will intensify. A few factors suggest the former. The sum of the Fed’s custody holdings together with the U.S. monetary base constitutes the root of global dollar liquidity. Each time this measure has severely contracted, the reduction in dollars has triggered a blowup somewhere, typically among other countries running twin deficits (Chart I-1). For example, since the Global Financial Crisis, a fall in the growth of this measure below the critical zero line coincided with the European debt crisis, China’s slowdown, and more recently slowing global trade and a manufacturing recession. Importantly, the slowdown in global trade preceded escalation in trade tensions between the U.S. and China, meaning other endogenous factors were also at play. Lack of dollar liquidity was perhaps a factor. Chart I-1A Liquidity Squeeze Of Dollars

A Liquidity Squeeze Of Dollars

A Liquidity Squeeze Of Dollars

Chart I-2The U.S. Budget Deficit Needs To Be Financed

The U.S. Budget Deficit Needs To Be Financed

The U.S. Budget Deficit Needs To Be Financed

In the past, the Fed was quick to correct the situation: most episodes when the U.S. current account deficit was shrinking, the domestic economy was on the cusp of a slowdown or recession. This time around, easy fiscal policy and a trade-hawkish President have allowed the Fed to ignore the liquidity crisis happening outside the U.S. Key to this is that the lines are now blurred between how much of the trade slowdown is tariff escalation, and how much is due to endogenous factors. As a result, the Fed no longer felt obliged to intervene for markets outside the U.S., especially if the U.S. domestic economy was faring well. A shrinking U.S. current account deficit is incompatible with a resolution to the dollar crisis, especially as the greenback remains the global reserve currency (Chart I-2). On the surface, this is dollar bullish. Meanwhile, our geopolitical strategists contend that the trade war is just a symptom of a much larger battle for hegemonic supremacy, which will last for many years to come. However, the key question is whether dollar liquidity will ease over the near term or the shortage will intensify. A few factors suggest the former. Balance Sheet, Current Account And Foreign Debt Chart I-3The Contraction In Custody Holdings Is Over

The Contraction In Custody Holdings Is Over

The Contraction In Custody Holdings Is Over

The Fed’s tapering of asset purchases has been a net drain on global dollar liquidity. But that is slated to change. The Fed’s balance sheet peaked a nudge above US$4.5 trillion in early 2015 and has been falling since. This has triggered a severe contraction in the U.S. monetary base, and severely curtailed commercial banks’ excess reserves. The Federal Reserve’s custody holdings argue that this was a huge drag on international dollar liquidity, even worse than during the 2008 crisis (Chart I-3). The good news is that the Fed has ended the tapering of its balance sheet and has started cutting rates. This combination will improve dollar's liquidity going forward. Meanwhile, balance-of-payment dynamics are heading in the wrong direction. Over the next five years, the U.S. Congressional Budget Office (CBO) estimates that the U.S. budget deficit will swell to 4.8% of GDP. Assuming the current account deficit widens a bit and then stabilizes, this will pin the twin deficits at around 8% of GDP. This assumes no recession, which would have the potential to swell the deficit even further. Part of these deficits will need to be funded through money printing. One difference between now and the past is that over the last several years, the dollar has become expensive. The narrowing of the U.S. current account balance might therefore be over. The U.S. saw its twin deficits swell to almost 13% of GDP following the financial crisis. However, then the dollar was cheap and commodity currencies were overvalued, following a natural resource bust. One way to solve an overvaluation problem is to increase the supply of dollars. Dollar liquidity shortages tend to be vicious because they trigger negative feedback loops. As the velocity of international U.S. dollars rises, offshore dollar rates begin to rise, lifting the cost of capital for borrowing countries. Debt repayment replaces capital spending. Yet there is little evidence that a dollar shortage has been triggering this sort of negative feedback loop. U.S. dollar funding to external entities is growing by circa 4% a year and has slowed to a crawl among both developed and emerging markets (Chart I-4). Historically, this slowdown has been symptomatic of a funding crisis in EM. Yet this time around, there have been other forces at play: The growth in euro- and yen-denominated debt is exploding, which mirrors the gradual shift in the allocation of FX reserves away from dollars into other currencies. The growth in euro- and yen-denominated debt is exploding (Chart I-5). This is much smaller in outstanding amounts than U.S.-denominated debt, but mirrors the gradual shift in the allocation of FX reserves away from dollars into other currencies. If the U.S. has started to weaponize the U.S. dollar, foreign entities may have no other choice than to rally into other currency blocs, which may eventually entail the Chinese yuan. Chart I-4Growth In The Dollar Short Position Has Eased

Growth In The Dollar Short Position Has Eased

Growth In The Dollar Short Position Has Eased

Chart I-5Lots Of Yen And Euro Debt ##br##Issuance

Lots Of Yen And Euro Debt Issuance

Lots Of Yen And Euro Debt Issuance

The fall in the use of dollars gradually redistributes the “exhorbitant priviledge” of the U.S. currency. This alleviates the need for the U.S. to run a wider current account deficit (President Trump’s goal). This means lower growth in foreign exchange reserves could become the norm rather than the exception (Chart I-6). Historically, current account imbalances have been a major source of currency crises, meaning the system could actually be more stable. Chart I-6The Drop In FX Reserves Is Not Precarious

The Drop In FX Reserves Is Not Precarious

The Drop In FX Reserves Is Not Precarious

The performance of some emerging market currency pairs will determine if the so-called funding crisis stays benign or becomes more malignant. Despite a deeper liquidity shortage than during the 2015-2016 crisis, most EM currency pairs are still trading within well-defined wedges and/or above critical thresholds (Chart I-7). Meanwhile, EM volatility remains much subdued – not symptomatic of a funding crisis (Chart I-8). Chart I-7EM Currency Pairs Remain Outside The Danger Zone

EM Currencies Pairs Remain Outside The Danger Zone

EM Currencies Pairs Remain Outside The Danger Zone

Chart I-8EM FX Volatility##br## Is Low

EM FX Volatility Is Low

EM FX Volatility Is Low

Bottom Line: One way to track if a dollar-funding crisis is becoming more acute is through the convenience yield, or cross-currency basis swap.1 This measures the difference in yield between an actual Treasury and a synthetic one trading in the offshore market. On this basis, it remains well below the panic levels observed in 2008, 2011 and 2015-2016, suggesting the dollar shortage is not as acute as back then (Chart I-9). Chart I-9The Convenience Yield For The Dollar Remains Low

The Convenience Yield For The Dollar Remains Low

The Convenience Yield For The Dollar Remains Low

The ECB Bazooka Chart I-10Relative R-Star* In The Eurozone Could Rebound

Relative R-Star* In The Eurozone Could Rebound

Relative R-Star* In The Eurozone Could Rebound

The ECB provided the stimulus the market wanted: they cut rates 10 basis points, offered a tiered system for their marginal deposit facility, and are starting an open-ended QE program at €20 billion a month in November. Yet the euro bounced. Our bias is that European rates were already well below equilibrium compared to the U.S., and the ECB’s dovish shift will help further lift the euro area’s growth potential (Chart I-10). If a central bank eases financing conditions at a time when growth is hitting a nadir, it is hardly bearish for the currency. Since the introduction of the euro, most of the economic imbalances from the region have stemmed from the standard contradiction of a common currency regime. This has been that interest rates have always been too low for one nation, while expensive for others. As such, the euro has typically been caught in a tug-of-war between a rising equilibrium rate of interest for one country, but a very low neutral rate for others.2 In the early 2000s, Spanish and Irish long-term rates were too low, and the reverse was true for Germany. The result was a massive boom in Spanish real estate, the accumulation of debt and buildup of major imbalances. Once bond vigilantes started punishing the periphery for their sins after the Great Recession, Germany found itself with rates that were too low relative to its newly reformed economy, while the periphery deflated. Capital spending in the peripheral countries has been rising faster than in core Europe, suggesting the spread between the cost of capital in these countries and the return on capital remains wide. The good news is this has not been the case for a few months now: 10-year government bond yields in France, Spain and even Portugal now sit at -24 basis points, 22 basis points and 24 basis points respectively, much below the neutral rate. This is severely easing financial conditions across the entire euro zone (Chart I-11). Chart I-11The Common-Currency Dilemma Solved

The Common-Currency Dilemma Solved

The Common-Currency Dilemma Solved

There has been a reason behind the collapse in spreads, aside from a dovish ECB. Labor market reforms in Mediterranean Europe have seen unit labor costs in Greece, Ireland, Portugal and Spain collectively contract by almost 10%. This has effectively eliminated the competitiveness gap that had accumulated over the past two decades (Chart I-12). Italy remains saddled with a rigid and less productive workforce, but overall adjustments have still come a long way to closing a key fissure plaguing the common-currency area. The result is in the numbers. Capital spending in the peripheral countries has been rising faster than in core Europe, suggesting the spread between the cost of capital in these countries and the return on capital remains wide (Chart I-13). More rapid capital spending in the periphery is a key channel to close the productivity gap between member nations and lift the neutral rate of interest for the entire euro zone. Chart I-12The Competitiveness Gap Has Closed