Gov Sovereigns/Treasurys

Highlights Corporate Spreads: The Fed’s dovish pivot prolongs the period of time before the yield curve inverts, thus extending the window for corporate bond outperformance. Investors should remain overweight corporate bonds, with a preference for securities rated Baa and below, where spreads remain wide relative to our fair value estimates. Yield Curve: Investors should barbell their U.S. bond portfolios, favoring long-maturity (> 10 years) and short-maturity (< 2 years) securities while avoiding the 5-year and 7-year notes. This positioning will boost average portfolio yield and will benefit from any future hawkish re-assessment of Fed policy. MBS: Lower mortgage rates have led to a jump in mortgage refinancings and wider MBS spreads. However, MBS spreads remain quite low compared to history. Maintain a neutral allocation to MBS in U.S. bond portfolios. Feature Last December, we laid out our key fixed income themes for 2019 in a Special Report.1 In that report we also introduced a framework for splitting the economic cycle into three phases based on the slope of the yield curve. Specifically, we use the 3-year/10-year Treasury slope to divide each cycle into the following three phases:2 Phase 1 runs from the end of the last recession until the 3/10 slope flattens to below 50 bps. Phase 2 encompasses the period when the 3/10 slope is between 0 bps and 50 bps. Phase 3 begins after the 3/10 slope inverts and ends at the start of the next recession. Clearly, as is illustrated in Chart 1, we are smack dab in the middle of a Phase 2 environment. This has implications for how we should think about positioning a U.S. bond portfolio. Chart 1Firmly In Phase 2

Firmly In Phase 2

Firmly In Phase 2

What Makes The Middle Phase Awkward? Table 1 shows annualized excess returns for Treasuries and corporate bonds (both investment grade and high-yield) in each phase of every cycle stretching back to the mid-1970s. Treasury excess returns are calculated relative to cash, as a proxy for the returns from taking duration risk. Corporate excess returns are relative to a duration-matched position in Treasury securities. Table 1Bond Performance In Different Yield Curve Regimes

The Long Awkward Middle Phase

The Long Awkward Middle Phase

A look at Table 1 reveals why we call Phase 2 the “awkward” middle phase of the cycle. The excess returns earned from taking both duration and corporate spread risk tend to be underwhelming. On duration, we observe that in three of the four complete cycles in our sample, Treasury excess returns are lowest in Phase 2. This lines up well with intuition. The flatter yield curve means that Treasuries offer a lower term premium in Phase 2 than in Phase 1. Meanwhile, Phase 3 periods tend to coincide with rapid Fed rate cuts, and thus large capital gains. Phase 2 periods, in contrast, often contain Fed tightening cycles. On corporate credit, we observe that excess returns tend to be lower in Phase 2 than in Phase 1, but are usually still positive. Returns tend not to turn consistently negative until after the 3/10 slope inverts and we enter Phase 3. Overall, if we know nothing other than that we are in Phase 2 of the cycle, our results suggest that we should take less duration risk in our portfolio than in Phases 1 or 3. Overall, if we know nothing other than that we are in Phase 2 of the cycle, our results suggest that we should take less duration risk in our portfolio than in Phases 1 or 3. The results also suggest that we should prefer corporate credit over Treasuries, though to a lesser extent than in Phase 1. What Makes The Middle Phase Long? In last December’s Special Report, we argued that the U.S. economy would remain in a Phase 2 environment for a long time, at least until late 2019. Our reasoning was that, in the absence of inflationary pressures, the Fed would be reluctant to tighten policy enough to invert the 3/10 curve. The Fed’s recent dovish pivot, and the resultant steepening of the curve (see Chart 1), only prolongs the current Phase 2 environment. We now think it will be well into 2020, and possibly later, before the 3/10 slope inverts and the economy enters Phase 3. One obvious investment implication of an extended Phase 2 environment is that we should remain overweight corporate bonds relative to duration-matched Treasuries. However, we also need to consider valuation before drawing too firm of a conclusion. Charts 2A and 2B show spreads for each corporate credit tier, encompassing both investment grade and high-yield, along with our spread targets. The spread targets are the median levels observed in prior Phase 2 environments, adjusted for changes in the average duration of the bond indexes over time.3 The charts reveal that Aaa-rated bonds already look expensive, while Aa and A-rated bonds are close to fairly valued. Baa-rated bonds are 13 bps cheap relative to our target, while the high-yield credit tiers offer significantly more value. Chart 2AInvestment Grade Spread Targets

Investment Grade Spread Targets

Investment Grade Spread Targets

Chart 2BHigh-Yield Spread Targets

High-Yield Spread Targets

High-Yield Spread Targets

As discussed in last week’s report, the Fed’s dovish pivot will cause corporate spreads to tighten in the near-term, but it will take longer before Treasury yields respond by moving higher.4 For Treasury yields to move higher, investors must first become convinced that the Fed’s reflationary efforts are translating into stronger global economic growth. Ultimately, we expect this will occur in the second half of this year and Treasury yields will be higher 12 months from now, as the Fed will fail to deliver the 92 bps of rate cuts that are currently priced. The flat yield curve means that the yield give-up is small, and we expect global growth to improve in the second half of the year. Bottom Line: The Fed’s dovish pivot prolongs the period of time before the yield curve inverts, thus extending the window for corporate bond outperformance. Investors should remain overweight corporate bonds, with a preference for securities rated Baa and below, where spreads remain wide relative to our fair value estimates. Investors should also keep portfolio duration low. The flat yield curve means that the yield give-up is small, and we expect global growth to improve in the second half of the year. Barbell Your Portfolio Chart 3Barbell Your Portfolio

Barbell Your Portfolio

Barbell Your Portfolio

For those unwilling or unable to deviate portfolio duration significantly from benchmark, there is another way to bet on the Fed delivering fewer cuts than are currently priced into the market. Investors can run a barbelled portfolio, favoring short-maturity (< 2 years) and long-maturity (> 10 years) securities, while avoiding the belly (5-year/7-year) of the curve. This sort of positioning has a few advantages. First, since the financial crisis, the yield curve has tended to steepen out to the 5-year/7-year point and flatten beyond that point whenever our 12-month Fed Funds Discounter rises (Chart 3). Conversely, whenever the market prices in more cuts/fewer hikes and our discounter falls, the yield curve has flattened out to the 5-year/7-year maturity point and steepened beyond that point. This correlation has been very consistent during the past few years, and continued to hold during the most recent decline in rate expectations. Notice that the 5-year yield has fallen by more than either the 2-year or 10-year yields since our Discounter's early-November peak (Table 2). Table 2The Belly Of The Curve Is Most Sensitive To Rate Expectations

The Long Awkward Middle Phase

The Long Awkward Middle Phase

The upshot is that, if rate expectations rise during the next 12 months, as we expect, the 5-year and 7-year notes will endure the most damage. The second reason why a barbelled portfolio makes sense is that valuation is very attractive. Chart 4 shows that the 5-year yield is below the yield on a duration-matched 2/10 barbell. It also shows that this 2/5/10 butterfly spread is very low relative to our model’s fair value.5 Chart 42/10 Barbell Is Attractive Versus 5-Year Bullet

2/10 Barbell Is Attractive Versus 5-Year Bullet

2/10 Barbell Is Attractive Versus 5-Year Bullet

We run similar fair value models for every possible bullet/barbell combination along the yield curve, and barbells appear universally cheap (see Appendix). Bottom Line: Investors should barbell their U.S. bond portfolios, favoring long-maturity (> 10 years) and short-maturity (< 2 years) securities while avoiding the 5-year and 7-year notes. This positioning will boost average portfolio yield and will benefit from any future hawkish re-assessment of Fed policy. MBS & Housing: The Implications Of Lower Mortgage Rates Alongside bond yields, mortgage rates have fallen sharply during the past few months, a trend that has important implications for both MBS spreads and future housing data. We consider the outlook for both. MBS Spreads Lower mortgage rates encourage homeowners to refinance their loans, and any increase in refinancing activity puts upward pressure on MBS spreads. Not surprisingly, as mortgage rates have declined we have seen a jump in the MBA Refinance Index and a widening of nominal MBS spreads (Chart 5). Chart 5MBS Spreads Still Historically Tight

MBS Spreads Still Historically Tight

MBS Spreads Still Historically Tight

While spreads have widened somewhat, they remain low compared to history (Chart 5, top panel). As such, we do not see a compelling buying opportunity in MBS. This is especially true relative to corporate credit where spreads are more attractive. Chart 6Limited Upside For Refis

Limited Upside For Refis

Limited Upside For Refis

With the mortgage rate now below 4%, our rough calculation suggests that approximately 44% of the Bloomberg Barclays Conventional 30-year MBS index is refinanceable. A regression of the MBA Refi Index versus the refinanceable share suggests a fair value of 2014 for the Refi Index, slightly above its actual level of 1950 (Chart 6). We also calculate that a further drop in the mortgage rate to below 3.5%, where it troughed in mid-2016, would increase the refinanceable share to 77%. Our regression translates this 77% share to a level of 3309 on the Refi Index. It should be noted that when the refinanceable share rose to 77% in 2016, the MBA Refi Index peaked at 2870. This means that our simple regression analysis probably overstates the surge in refis that would occur if mortgage rates fell another 50 bps. In addition, we think it’s unlikely that mortgage rates will actually fall back to 3.5%, as they did in 2016, and as such, we are hesitant to position for further MBS spread widening. The improvement in housing actitivty is not uniform across all indicators. We recommend maintaining a neutral allocation to MBS for now. If mortgage rates drop and spreads widen further in the near-term, then a buying opportunity may present itself. Housing Activity Chart 7Housing Activity: A Mixed Picture

Housing Activity: A Mixed Picture

Housing Activity: A Mixed Picture

The drop in mortgage rates will also have a significant impact on housing activity data. This is important because, as we have demonstrated in prior reports, housing activity data – particularly single-family housing starts and new homes sales – are reliable indicators of U.S. recessions and interest rates.6 By all measures, housing activity weakened significantly as mortgage rates surged in 2018. But it has improved somewhat now that mortgage rates have declined. However, the improvement is not uniform across all indicators (Chart 7): New home sales jumped sharply early this year, then fell back more recently. The current trend is neutral, with the latest monthly print very close to the 12-month moving average (Chart 7, top panel). Housing starts and permits are both trending below their respective 12-month moving averages, though by less than in 2018 (Chart 7, panel 2 & 3). Existing home sales have popped, and are now exerting upward pressure on the 12-month average (Chart 7, panel 4). Likewise for mortgage purchase applications (Chart 7, panel 5). Homebuilders also report that lower mortgage rates have led to a jump in sales activity (Chart 7, bottom panel). With mortgage rates still low, the tentative rebound in housing activity data should continue in the coming months. Looking further out, we see significantly more upside in single-family housing starts and new home sales as builders shift construction toward lower-priced properties. The Bifurcated Housing Market Beyond the large swings in mortgage rates, another trend has significantly influenced housing activity in recent years. For the past few years, homebuilders have focused their attention on higher priced homes, and that segment of the market now looks oversupplied. Data from the American Enterprise Institute Housing Center show that the recent deceleration in home prices has been driven by falling prices for the most expensive homes. Homes in the lowest price tier have seen prices accelerate (Chart 8).7 The divergence is also evident in the supply data. New home inventories are roughly consistent with average historical levels, while existing home inventories are incredibly low (Chart 9). In fact, new home inventories now represent 6.4 months of demand while existing home inventories represent 4.3 months of demand (Chart 9, panel 3). Such a wide divergence is historically rare. Chart 8An Oversupply Of High ##br##Priced Homes...

An Oversupply Of High Priced Homes...

An Oversupply Of High Priced Homes...

Chart 9...And An Undersupply Of Low Priced Homes

...And An Undersupply Of Low Priced Homes

...And An Undersupply Of Low Priced Homes

The divergence between an oversupply of new homes and an undersupply of existing homes is a result of new construction having focused on higher priced homes in recent years. The median price for a new home used to be only slightly above the median price for an existing home, but the difference shot up to above 75k during the past few years (Chart 9, bottom panel). More recently, the price differential between new and existing homes has started to fall, as builders are starting to recognize that the greater growth opportunity lies at the low-end of the market where demand is strong relative to supply. As this supply-side adjustment plays out, it will provide an additional boost to new homes sales and housing starts going forward. Appendix The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com U.S. Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 3 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 3Butterfly Strategy Valuation: Raw Residuals In Basis Points (As of June 27, 2019)

The Long Awkward Middle Phase

The Long Awkward Middle Phase

Table 4 scales the raw residuals in Table 3 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 4Butterfly Strategy Valuation: Standardized Residuals (As of June 27 2019)

The Long Awkward Middle Phase

The Long Awkward Middle Phase

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 2 We use the 3/10 Treasury slope in place of the more commonly referenced 2/10 slope because it is a close proxy that provides an additional 14 years of historical data. 3 For more details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy / Global Fixed Income Strategy Weekly Report, “The Fed’s Got Your Back”, dated June 25, 2019, available at usbs.bcaresearch.com 5 For more details on our yield curve models please see U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “More Than One Reason To Own Steepeners”, dated September 25, 2018, available at usbs.bcaresearch.com 7 Low-tier homes are those in the bottom 40% of the price distribution in each metro area. High-tier homes are those that are both in the top 20% of the price distribution and exceed the GSE loan limit by more than 25%. For further details: http://www.aei.org/wp-content/uploads/2019/06/HPA_market_conditions_report_June_2019.pdf Fixed Income Sector Performance Recommended Portfolio Specification

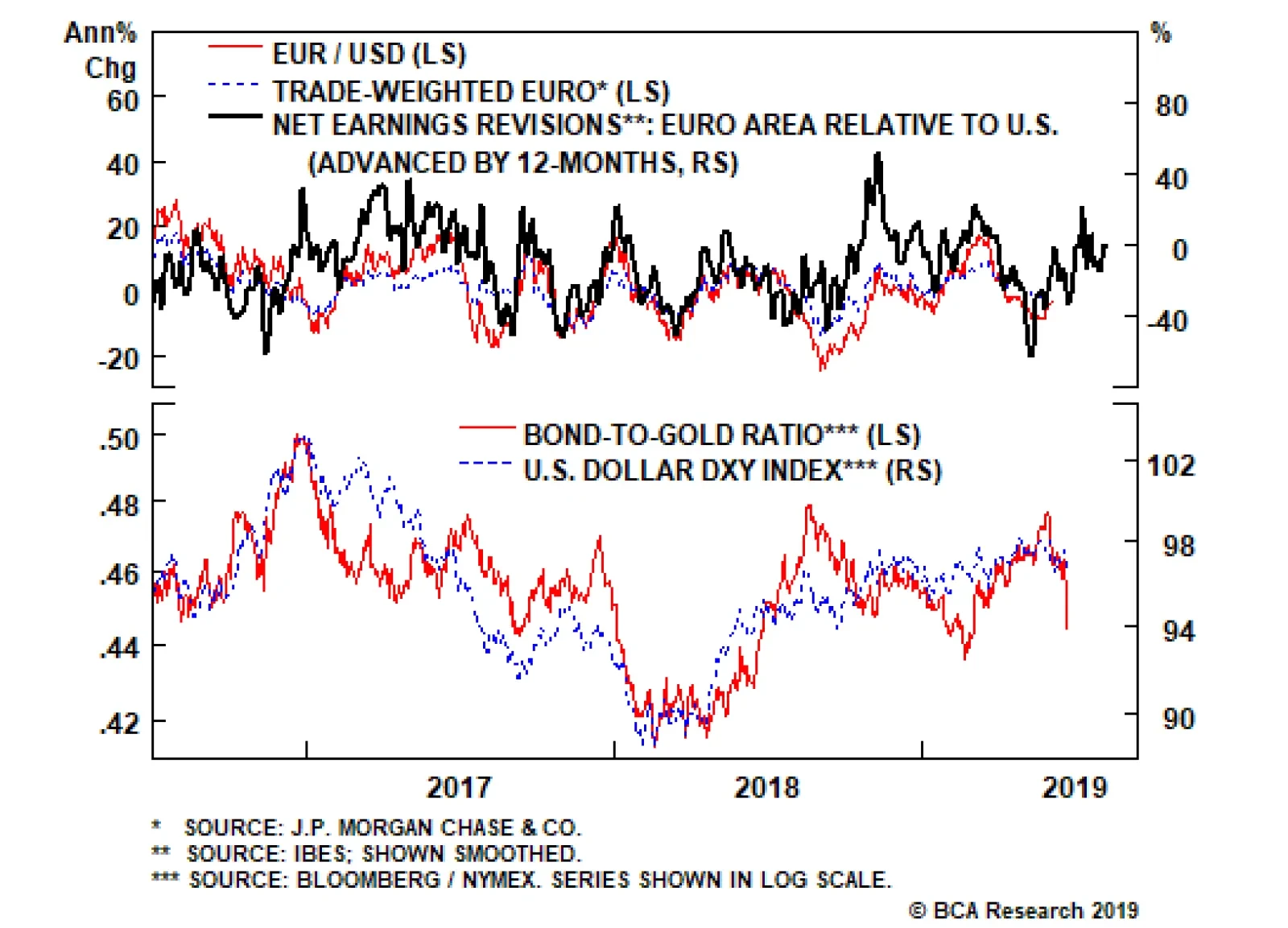

Highlights Relative Growth & Inflation: Underlying U.S. and European economic growth momentum remains surprisingly similar, with weakness concentrated in manufacturing industries most exposed to trade uncertainty. Realized inflation readings are also fairly close, although there is less spare capacity in the U.S. where wages are growing at a much faster rate. UST-Bund Spread: The yield gap between 10-year U.S. Treasuries and German Bunds is now fairly valued after the larger decline in U.S. yields seen in 2019. The Fed is more likely to deliver less easing relative to market expectations than the ECB, leaving the UST-Bund spread susceptible to a rebound over the 6-12 months. Hedged Vs Unhedged: We continue to recommend overweighting German Bunds vs U.S. Treasuries in global currency-hedged bond portfolios, given the substantial yield pickup gained by hedging into U.S. dollars out of euros. Feature “We should have Draghi instead of our Fed person.” – U.S. President Donald Trump Chart of the WeekIt’s Tough To Get A Weaker USD, Mr. President

It's Tough To Get A Weaker USD, Mr. President

It's Tough To Get A Weaker USD, Mr. President

In his own inimitable way, President Trump in the above quote has called out the glaring difference between the ECB, which seems very willing to deliver more policy stimulus to a struggling euro area economy, and the Fed, which is reluctantly being pulled towards a rate cut. Yet while the current ECB President will be looking for a new job in a few months after his term expires, the reality is that President Trump will have to live with the current Fed leadership for the foreseeable future. Our Central Bank Monitors do indicate a need for easier monetary policy on both sides of the Atlantic (Chart of the Week). The signal from our ECB Monitor is stronger than that of our Fed Monitor, but U.S. Treasury and German bund yields have both fallen sharply with markets pricing in lower inflation expectations and new policy stimulus. The result is a relatively modest narrowing of U.S.-European expected interest rate differentials that has had little impact in weakening the U.S. dollar (USD) versus the euro. With both the Fed and ECB now in play for rate cuts, this is a good time to review the drivers of the spread between U.S. Treasury (UST) yields and German government bond yields – specifically, the widely-followed 10-year Treasury-Bund spread. A Quick Trans-Atlantic Comparison Of Growth, Inflation & Interest Rates The global bond rally seen this year has driven the 10-year UST yield fall back to the 2% level last seen in 2016. The 10-year Bund yield, on the other hand, has plummeted to a new all-time low of -0.3%. The yield move in the U.S. was larger, thus the UST-Bund spread has narrowed from a 2019 peak of 253bps to the current level of 233bps. Breaking down the nominal 10-year yields into the real yield and inflation expectations components illustrates how the current wide UST-Bund spread is almost purely a “real” phenomenon (Chart 2). 10-year CPI rates are 1.9% and 1.4% in the U.S. and euro area, respectively, accounting for 50bps of the overall 233bps UST-Bund spread. Adjusting the nominal yields by those CPI swap rates leaves a real 10-year Treasury yield of +0.1%, compared to -1.7% in Europe (using the 10-year German yield versus 10-year euro CPI swap). Thus, the market-implied real yield differential is 180bps, accounting for the bulk of the nominal UST-Bund spread. Our proxy for the market’s expectation of the real neutral interest rate – the 5-year Overnight Index Swap (OIS) rate, 5-years forward minus the 5-year CPI swap rate, 5-years forward – is indicating that investors now think the neutral real fed funds rate is 0% and the neutral real ECB rate is around -1% (Chart 3). Chart 2Real Yields Dictating UST-Bund Spread

Real Yields Dictating UST-Bund Spread

Real Yields Dictating UST-Bund Spread

Chart 3Global Yields Discounting Fresh ECB QE?

Global Yields Discounting Fresh ECB QE?

Global Yields Discounting Fresh ECB QE?

Those market-implied measures typically follow the path of our estimate of the term premium for the 10-year Treasury and Bund. For both markets, however, the term premium is now at a much more negative level than suggested by the past relationship with our real neutral rate proxy. The gap between the 10-year UST term premium (-60bps) and the 10-year German Bund term premium (-124bps) now contributes about 64bps to the nominal UST-Bund spread. When looking at the relative cyclical state of the U.S. and European economies at present, there are surprisingly few differences that show up in the data. Term premia are heavily influenced by investor risk aversion and the demand for safe assets during periods of uncertainty. Given the numerous headline risks that investors are faced with at the moment (U.S.-China trade, slowing global growth, U.S.-Iran military tensions, the start of the 2020 U.S. Presidential election cycle), it is understandable that money has flooded into the safety of developed market government debt. Yet when looking at the relative cyclical state of the U.S. and European economies at present, there are surprisingly few differences that show up in the data (Chart 4). The euro area manufacturing PMI is now at 47.8, below the 50 line that indicates an expanding industrial sector, but may be starting to stabilize. The U.S. ISM manufacturing index, at the same time, now sits at 52.1 and is closing in on the levels seen in Europe. Meanwhile, consumer confidence measures remain elevated both in the U.S. and Europe, even after the recent small dips. Business confidence measures like the NFIB U.S. small business survey and the European Commission’s business climate indicator remain firm relative to the post-crisis history, although both are off their cyclical peaks. That relative dearth of spare capacity in the U.S. compared to Europe is the most fundamental reason for the higher level of U.S. interest rates relative to the euro area. Turning to the state of labor markets on both sides of the Atlantic, the stories are also similar (Chart 5). Unemployment rates are well below the OECD’s estimates of the full employment NAIRU level. Wages are starting to gain some upward momentum in Europe, but U.S. Average Hourly Earnings are growing about one percentage point faster than equivalent measures in the euro area. Chart 4Not A Huge U.S.-Europe Cyclical Growth Gap

Not A Huge U.S.-Europe Cyclical Growth Gap

Not A Huge U.S.-Europe Cyclical Growth Gap

Chart 5Not A Huge U.S.-Europe Structural Growth Gap

Not A Huge U.S.-Europe Structural Growth Gap

Not A Huge U.S.-Europe Structural Growth Gap

The implication here is that there is less slack in the U.S. labor market than in Europe, as exemplified by the fast rate of wage growth in the U.S. Chart 6A Bit More Wage Inflation In The U.S.

A Bit More Wage Inflation In The U.S.

A Bit More Wage Inflation In The U.S.

That relative dearth of spare capacity in the U.S. compared to Europe is the most fundamental reason for the higher level of U.S. interest rates relative to the euro area (Chart 6). U.S. potential GDP growth is only marginally faster than it is in Europe, with virtually the same rate of long-term labor productivity growth (about 0.5% per year, according to the OECD). Yet according to the New York Fed’s most recent estimates of the natural real interest rate (“r-star”), the level of the inflation-adjusted policy rate that would be considered neither stimulative nor restrictive given current estimates of spare capacity, is 0.7% in the U.S. and -0.4% in Europe.1 Looking ahead, both the Fed and ECB are likely to deliver some monetary easing in the coming months, perhaps as soon as the next set of policy meetings in late July. The market expects much more from the Fed, though, with 92bps of cuts discounted over the next twelve months. 16bps of cuts are also expected from the ECB, but that is more likely to be delivered than the market expectation for the Fed. There is even a chance that the ECB could restart their Asset Purchase Program, although likely not after delivering a small rate cut first. In any case, there is likely to be more disappointment from the Fed compared to the ECB over the next 6-12 months, with the result being some upward pressure placed on the UST-Bund spread. Bottom Line: Underlying U.S. and European economic growth momentum remains surprisingly similar, with weakness concentrated in manufacturing industries most exposed to trade uncertainty. Realized inflation readings are also fairly close, although there is less spare capacity in the U.S. where wages are growing at a much faster rate. There is likely to be more disappointment from the Fed compared to the ECB over the next 6-12 months, with the result being some upward pressure placed on the UST-Bund spread. Valuation & Currency Risk In The UST-Bund Spread Our valuation model for the 10-year Treasury-Bund spread indicates that the current spread level of 233bps is very close to fair value of 223bps (Chart 7). Chart 7UST-Bund Spread Fairly Valued

UST-Bund Spread Fairly Valued

UST-Bund Spread Fairly Valued

The main variables in the model are the spread between the fed funds rate and the ECB 1-week refinancing rate, the ratio of the unemployment rates of the U.S. and euro area, and the differential between the headline inflation rates of the U.S. and euro area. The model also includes the balance sheets of the Fed and ECB as variables, to capture any effects on the Treasury-Bund spread from quantitative easing programs. Historically, the UST-Bund spread has been driven mostly by the gap between Fed and ECB policy rates and, to a lesser extent, the relative state of unemployment. Inflation differentials have become less of a driver of the spread during the years since the 2008 financial crisis (Chart 8), although this is part of the broader issue of wage growth diverging from price inflation in the developed economies. The reaction function of the central banks, and of bond yields, is still rooted in the amount of perceived spare economic capacity – and future inflation potential – implied by unemployment rates. Looking ahead, if the Fed and ECB were both to deliver the full amount of easing over the next year discounted in the USD and EUR OIS curves, then the fair value of the spread would narrow to 208bps. The one-year-ahead forward rates for both the 10-year UST and German Bund imply a spread tightening to 229bps, which means that it would likely require the Fed delivering the full 92bps of easing discounted over the next twelve months – not our base case view – to make betting on additional UST-Bund spread tightening a profitable trade that would beat the forwards. So while the case for betting on additional UST-Bund spread narrowing is a poor one at current levels, the case for favoring Bunds over Treasuries on a currency-hedged basis in U.S. dollar terms is strong. Going long German government bonds vs U.S. Treasuries, while hedging the euro currency exposure into U.S. dollars, actually generates a pickup in yield, despite the fact that the entire German yield curve has negative yields out to 15-year maturities. Chart 9 shows the U.S.-German bond yield spreads for the 2-year, 5-year, 10-year and 30-year maturities. The solid line in all panels represents the yield spread in currency-unhedged terms, while the dotted line in all panels shows the spread after hedging the Bund yields into U.S. dollar equivalents (using 3-month currency forwards). Across all four maturities shown, the wide unhedged U.S.-German spreads turn into negative spreads after currency hedging. This is due to the considerably higher short-term interest rates in the U.S. that are gained when selling euros forward for dollars. Chart 8UST-Bund Spread Driven By Fed/ECB Gap

UST-Bund Spread Driven By Fed/ECB Gap

UST-Bund Spread Driven By Fed/ECB Gap

Chart 9UST-Bund Spreads Look VERY Different After Hedging FX Risk

UST-Bund Spreads Look VERY Different After Hedging FX Risk

UST-Bund Spreads Look VERY Different After Hedging FX Risk

Thus, going long German government bonds vs U.S. Treasuries, while hedging the euro currency exposure into U.S. dollars, actually generates a pickup in yield, despite the fact that the entire German yield curve has negative yields out to 15-year maturities. When looking at the relative performance of German bonds relative to not only U.S. Treasuries, but the overall Bloomberg Barclays Global Treasury index, Germany has basically matched the index over the past year in currency-hedged terms (Chart 10, middle panel). On an unhedged basis, the relative performance of German debt is obviously far more volatile given the swings in the euro. Yet even in unhedged terms, the relative performance of Germany versus the U.S. appears to be turning around, despite the recent additional narrowing of the UST-Bund spread (bottom panel). Chart 10Favor Bunds Over USTs In USD-Hedged Bond Portfolios

Favor Bunds Over USTs In USD-Hedged Bond Portfolios

Favor Bunds Over USTs In USD-Hedged Bond Portfolios

Chart 11UST-Bund Spread Tightening Looks Stretched

UST-Bund Spread Tightening Looks Stretched

UST-Bund Spread Tightening Looks Stretched

This highlights the risk of solely looking at the spread between yields denominated in different currencies. FX movements can dominate relative yield changes, as has been the case of late with the EUR/USD exchange rate rising off the 2019 lows on the back of falling UST yields. We continue to prefer viewing cross-country spread trades in currency-hedged terms when we make our recommendations. On that basis, we like hedged Bunds over U.S. Treasuries – especially with the current UST-Bund spread now discounting a lot of relatively bad news in the U.S. versus Europe (Chart 11). Bottom Line: The Fed is more likely to deliver less easing relative to market expectations than the ECB, leaving the UST-Bund spread susceptible to a rebound over the next 6-12 months. We continue to recommend overweighting German Bunds vs U.S. Treasuries in global currency-hedged bond portfolios, given the substantial yield pickup gained by hedging into U.S. dollars out of euros. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com 1 The New York Fed’s r-star estimates can be found here: https://www.newyorkfed.org/research/policy/rstar Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

What Next For The Treasury-Bund Spread?

What Next For The Treasury-Bund Spread?

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Central banks globally have turned dovish, with the Fed virtually promising to cut rates in July. But this will be an “insurance” cut, like 1995 and 1998, not the beginning of a pre-recessionary easing cycle. The global expansion remains intact, with the fundamental drivers of U.S. consumption robust and China likely to ramp up its credit stimulus over the coming months. The Fed will cut once or twice, but not four times over the next 10 months as the futures markets imply. Underlying U.S. inflation – properly measured – is trending higher to above 2%. U.S. GDP growth this year will be around 2.5%. Inflation expectations will move higher as the crude oil price rises. Unemployment is at a 50-year low and the U.S. stock market at an historical peak. These factors suggest bond yields are more likely to rise than fall from current levels. The upside for U.S. equities is limited, but earnings growth should be better than the 3% the bottom-up consensus expects. The key for allocation will be when to shift in the second half into higher-beta China-related plays, such as Europe and Emerging Markets. For now, we remain overweight the lower-beta U.S. equity market, neutral on credit, and underweight government bonds. To hedge against the positive impact of China stimulus, we raise Australia to neutral, and re-emphasize our overweights on the Industrials and Energy sectors. Feature Overview Precautionary Dovishness – Or Looming Recession? Recommendations

Quarterly Portfolio Outlook: Precautionary Dovishness – Or Looming Recession?

Quarterly Portfolio Outlook: Precautionary Dovishness – Or Looming Recession?

Central banks everywhere have taken a decidedly dovish turn in recent weeks. June’s FOMC statement confirmed that “uncertainties about the outlook have increased….[We] will act as appropriate to sustain the expansion,” hinting broadly at a rate cut in July. The Bank of Japan’s Kuroda said he would “take additional easing action without hesitation,” and hinted at a Modern Monetary Theory-style combination of fiscal and monetary policy. European Central Bank President Draghi mentioned the possibility of restarting asset purchases. There are two possible explanations. Either the global economy is heading into recession, and central banks are preparing for a full-blown easing cycle. Or these are “insurance” cuts aimed at prolonging the expansion, as happened in 1995 and 1998, or similar to when the Fed went on hold for 12 months in 2016 (Chart 1). Our view is that it is most likely the latter. The reason for this is that the main drivers of the global economy, U.S. consumption ($14 trillion) and the Chinese economy ($13 trillion) are likely to be strong over the next 12 months. U.S. wage growth continues to accelerate, consumer sentiment is close to a 50-year high, and the savings rate is elevated (Chart 2); as a result core U.S. retail sales have begun to pick up momentum in recent months (Chart 3). Unless something exogenous severely damages consumer optimism, it is hard to see how the U.S. can go into recession in the near future, considering that consumption is 70% of GDP. Moreover, despite weaknesses in the manufacturing sector – infected by the China-led slowdown in the rest of the world – U.S. service sector growth and the labor market remain solid. This resembles 1998 and 2016, but is different from the pre-recessionary environments of 2000 and 2007 (Chart 4). There is also no sign on the horizon of the two factors that have historically triggered recessions: a sharp rise in private-sector debt, or accelerating inflation (Chart 5). Chart 1Insurance Cuts, Or Full Easing Cycle?

Insurance Cuts, Or Full Easing Cycle?

Insurance Cuts, Or Full Easing Cycle?

Chart 2Consumption Fundamentals Are Strong...

Consumption Fundamentals Are Strong...

Consumption Fundamentals Are Strong...

Chart 3...Leading To Rebound In Retail Sales

...Leading To Rebound In Retail Sales

...Leading To Rebound In Retail Sales

Chart 4Manufacturing Weak, But Services Holding Up

Manufacturing Weak, But Services Holding Up

Manufacturing Weak, But Services Holding Up

Chart 5No Signs Of Usual Recession Triggers

No Signs Of Usual Recession Triggers

No Signs Of Usual Recession Triggers

China’s efforts to reflate via credit creation have been somewhat half-hearted since the start of the year. Investment by state-owned companies has picked up, but the private sector has been spooked by the risk of a trade war and has slowed capex (Chart 6). China may have hesitated from full-blown stimulus because the authorities in April were confident of a successful outcome to trade talks with the U.S., and a bit concerned that the liquidity was going into speculation rather than the real economy. But we see little reason why they will not open the taps fully if growth remains sluggish and trade tensions heighten.1 Chinese credit creation clearly has a major impact on many components of global growth – in particular European exports, Emerging Markets earnings, and commodity prices – but the impact often takes 6-12 months to come through (Chart 7). A key question is when investors should position for this to happen. We think this decision is a little premature now, but will be a key call for the second half of the year. Chart 6China's Half-Hearted Reflation

China's Half-Hearted Reflation

China's Half-Hearted Reflation

Chart 7China Credit Growth Affects The World

China Credit Growth Affects The World

China Credit Growth Affects The World

Chart 8Fed Won't Cut As Much As Market Wants...

Fed Won't Cut As Much As Market Wants...

Fed Won't Cut As Much As Market Wants...

The Fed has so clearly signaled rate cuts that we see it cutting by perhaps 50 basis points over the next few months (maybe all in one go in July if it wants to “shock and awe” the market). But the futures market is pricing in four 25 bps cuts by April next year. With GDP growth likely to be around 2.5% this year, unemployment at a 50-year low, trend inflation above 2%,2 and the stock market at an historical high, we find this improbable. Two cuts would be similar to what happened in 1995, 1998 and (to a degree) 2016 (Chart 8). In this environment, we think it likely that equities will outperform bonds over the next 12 months. When the Fed cuts by less than the market is expecting, long-term rates tend to rise (Chart 9). BCA’s U.S. bond strategists have shown that after mid-cycle rate cuts, yields typically rise: by 59 bps in 1995-6, 58 bps in 1998, and 19 bps in 2002.3 A combination of rising inflation, stronger growth ex-U.S., a less dovish Fed that the market expects, and a rising oil price (which will push up inflation expectations) makes it unlikely – absent an outright recession – that global risk-free yields will fall much below current levels. Moreover, June’s BOA Merrill Lynch survey cited long government bonds as the most crowded trade at the moment, and surveys of investor positioning suggest duration among active investors is as long as at any time since the Global Financial Crisis (Chart 10). Chart 9...So Bond Yields Are Likely To Rise

...So Bond Yields Are Likely To Rise

...So Bond Yields Are Likely To Rise

Chart 10Investors Betting On Further Rate Decline

Investors Betting On Further Rate Decline

Investors Betting On Further Rate Decline

The outlook for U.S. equities is not that exciting. Valuations are not cheap (with forward PE of 16.5x), but earnings should be revised up from the currently very cautious level: the bottom-up consensus forecasts S&P 500 EPS growth at only 3% in 2019 (and -3% YoY in Q2). We have sympathy for the view that there are three put options that will prop up stock prices in the event of external shocks: the Fed put, the Xi put, and the Trump put. Relating to the last of these, it is notable that President Trump tends to turn more aggressive in trade talks with China whenever the U.S. stock market is strong, but more conciliatory when it falls (Chart 11). For now, therefore, we remain overweight U.S. equities, as a lower beta way to play an environment that continues to be positive – but uncertain – for stocks. But we continue to watch for the timing to move into higher-beta China-related markets as the effects of China’s stimulus start to come through. Chart 11Trump Turns Softer When Market Falls

Trump Turns Softer When Market Falls

Trump Turns Softer When Market Falls

Garry Evans Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Chart 12Temporary Forces Drove Inflation Downturn

Temporary Forces Drove Inflation Downturn

Temporary Forces Drove Inflation Downturn

Why Is Inflation So Low? After reaching 2% in July 2018, U.S. core PCE currently stands at 1.6%, close to 18 month lows. This plunge in inflation, along with increased worries about the trade war and continued economic weakness, has led the market to believe that the Fed Funds Rate is currently above the neutral rate, and that several rate cuts are warranted in order to move policy away from restrictive territory. We believe that the recent bout of low inflation is temporary. The main contributor to the fall in core PCE has been financial services prices, which shaved off up to 40 basis points from core PCE (Chart 12, panel 1). However, assets under management are a big determinant of financial services prices, making this measure very sensitive to the stock market (panel 2). Therefore, we expect this component of core PCE to stabilize as equity prices continue to rise. The effect of higher equity prices, and the stabilization of other goods that were affected by the slowdown of global growth in late 2018 and early 2019, may already have started to push inflation higher. Month-on-month core PCE grew at an annualized rate of 3% in April, the highest pace since the end of 2017. Meanwhile, trimmed mean PCE, a measure that has historically been a more stable and reliable gauge of inflationary pressures, is at a near seven-year high (panel 3). The above implies that the market might be overestimating how much the Fed is going to ease. We believe that the Fed will likely cut once this year to soothe the pain caused by the trade war on financial markets. However, with unemployment at 50-year lows, and inflation set to rise again, the Fed is unlikely to deliver the 92 basis points of cuts currently priced by the OIS curve for the next 12 months. This implies that investors should continue to underweight bonds. Chart 13Turning On The Taps

Turning On The Taps

Turning On The Taps

Will China Really Ramp Up Its Stimulus? The direction of markets over the next 12 months (a bottoming of euro area and Emerging Markets growth, commodity prices, the direction of the USD) are highly dependent on whether China further increases monetary stimulus in the event of a breakdown in trade negotiations with the U.S. But we hear much skepticism from clients: aren’t the Chinese authorities, rather, focused on reducing debt and clamping down on shadow banking? Aren’t they worried that liquidity will simply flow into speculation and have little impact on the real economy? Now the government has someone to blame for a slowdown (President Trump), won’t they use that as an excuse – and, to that end, are preparing the population for a period of pain by quoting as analogies the Long March in the 1930s and the Korea War (when China ground down U.S. willingness to prolong the conflict)? We think it unlikely that the Chinese government would be prepared to allow growth to slump. Every time in the past 10 years that growth has slowed (with, for example, the manufacturing PMI falling significantly below 50) they have always accelerated credit growth – on the basis of the worst-case scenario (Chart 13, panel 1). Why would they react differently this time, particularly since 2019 is a politically sensitive year, with the 70th anniversary of the founding of the People’s Republic in October and several other important anniversaries? Moreover, the government is slipping behind in its target to double per capita income in the 10 years to end-2020 (panel 2). GDP growth needs to be 6.5-7% over the next 18 months to achieve the target. The government’s biggest worry is employment, where prospects are slipping rapidly (panel 3). This also makes it difficult for the authorities to retaliate against U.S. companies that have large operations, such as Apple or General Motors, since such measures would hurt their Chinese employees. Besides a significant revaluation of the RMB (which we think likely), China has few cards to play in the event of a full-blown trade war other than fully turning on the liquidity tap again.

Chart 14

Aren’t There Signs Of Bubbliness In Equity Markets? Clients have asked whether the current market environment has been showing any classic signs of euphoria. These usually appear with lots of initial public offerings (IPO), irrational M&A activity, and excess investor optimism. The IPO market has some similarities to the years leading up to the dot-com bubble, but it is important to look below the surface. The percentage of IPOs with negative earnings in 2018 was similar to the previous peak in 1999. However, the average first-day return of IPOs in 2019, while still above the historical average, has been much lower than that during the dot-com bubble period (Chart 14, panel 1). There is also a difference in the composition of firms going public. There are now many IPOs for biotech firms that have heavily invested in R&D, and so have relatively low sales currently but await a breakthrough in their products; by their nature, these are loss-making (panel 2). Cross-sector, unrelated M&A activity has also often been a sign of bubble peaks. It is a consequence of firms stretching to find inorganic growth late in the cycle. Such deals are characterized by high deal premiums, and are usually conducted through stock purchases rather than in cash. The current average deal premium is below its historical average (panel 3). Additionally, 2018 and 2019-to-date M&A deals conducted using cash represented 60% and 90% of the total respectively, compared to only 17% between 1996 and 2000. Investor sentiment is also moderately pessimistic despite the rally in the S&P 500 since the beginning of the year (panel 4). This caution suggests that investors are fearful of the risk of recession rather than overly positive about market prospects, despite the U.S. market being at an historical high. Given the above, we do not see any signals of the sort of euphoria and bubbliness that typically accompanies stock market tops. Will Japan Benefit From Chinese Reflation? Japan has been one of the worst-performing developed equity markets since March 2009, when global equities hit their post-crisis bottom in both USD (Chart 15) and local currency terms. Now with increasing market confidence in China’s reflationary policies, clients are asking if Japan is a good China play given its close ties with the Chinese economy. Our answer is No.

Chart 15

Chart 16Downgrade Japan To Underweight

Downgrade Japan To Underweight

Downgrade Japan To Underweight

It’s true that Japanese equities did respond to past Chinese reflationary efforts, but the outperformances were muted and short-lived (Chart 16, panel 1). Even though Japanese exports to China will benefit from Chinese reflationary policy (panel 5), MSCI Japan index earnings growth does not have strong correlation with Japanese exports to China, as shown in panel 4. This is not surprising given that exports to China account for only about 3% of nominal GDP in Japan (compared to almost 6% for Australia, for example). The MSCI Japan index is dominated by Industrials (21%) and Consumer Discretionary (18%). Financials, Info Tech, Communication Services and Healthcare each accounts for about 8-10%. Other than the Communication Services sector, all other major sectors in Japan have underperformed their global peers since the Global Financial Crisis (panels 2 and 3). The key culprit for such poor performance is Japan’s structural deflationary environment. Wage growth has been poor despite a tight labor market. This October’s consumption tax increase will put further downward pressure on domestic consumers. There is no sign of the two factors that have historically triggered recessions: a sharp rise in private-sector debt, or accelerating inflation. As such, we are downgrading Japan to a slight underweight in order to close our underweight in Australia (see page 16). This also aligns our recommendation with the output from our DM Country Allocation Quant Model, which has structurally underweighted Japan since its inception in January 2016. Global Economy Chart 17Is Consumption Enough To Prop Up U.S. Growth?

Is Consumption Enough To Prop Up U.S. Growth?

Is Consumption Enough To Prop Up U.S. Growth?

Overview: The tight monetary policy of last year (with the Fed raising rates and China slowing credit growth) has caused a slowdown in the global manufacturing sector, which is now threatening to damage worldwide consumption and the relatively closed U.S. economy too. The key to a rebound will be whether China ramps up the monetary stimulus it began in January but which has so far been rather half-hearted. Meanwhile, central banks everywhere are moving to cut rates as an “insurance” against further slowdown. U.S.: Growth data has been mixed in recent months. The manufacturing sector has been affected by the slowdown in EM and Europe, with the manufacturing ISM falling to 52.1 in May and threatening to dip below 50 (Chart 17, panel 2). However, consumption remains resilient, with no signs of stress in the labor market, average hourly earnings growing at 3.1% year-on-year, and consumer confidence at a high level. As a result, retail sales surprised to the upside in May, growing 3.2% YoY. The trade war may be having some negative impact on business sentiment, however, with capex intentions and durable goods orders weakening in recent months. Euro Area: Current conditions in manufacturing continue to look dire. The manufacturing PMI is below 50 and continues to decline (Chart 18, panel 1). In export-focused markets like Germany, the situation looks even worse: Germany’s manufacturing PMI is at 45.4, and expectations as measured by the ZEW survey have deteriorated again recently. Solid wage growth and some positive fiscal thrust (in Italy, France, and even Germany) have kept consumption stable, but the recent tick-up in German unemployment raises the question of how sustainable this is. Recovery will be dependent on Chinese stimulus triggering a rebound in global trade. Chart 18Few Signs Of Recovery In Global Ex-U.S. Growth

Few Signs Of Recovery In Global Ex-U.S. Growth

Few Signs Of Recovery In Global Ex-U.S. Growth

Japan: The slowdown in China continues to depress industrial production and leading indicators (panel 2). But maybe the first “green shoots” are appearing thanks to China’s stimulus: in April, manufacturing orders rose by 16.3% month-on-month, compared to -11.4% in March. Nonetheless, consumption looks vulnerable, with wage growth negative YoY each month so far this year, and the consumption tax rise in October likely to hit consumption further. The Bank of Japan’s six-year campaign of maximum monetary easing is having little effect, with core core inflation stuck at 0.5% YoY, despite a small pickup in recent months – no doubt because the easy monetary policy has been offset by a steady tightening of fiscal policy. Emerging Markets: China’s growth has slipped since the pickup in February and March caused by a sharp increase in credit creation. Seemingly, the authorities became more confident about a trade agreement with the U.S., and worried about how much of the extra credit was going into speculation, rather than the real economy. The manufacturing PMI, having jumped to almost 51 in March, has slipped back to 50.2. A breakdown of trade talks would undoubtedly force the government to inject more liquidity. Elsewhere in EM, growth has generally been weak, because of the softness in Chinese demand. In Q1, GDP growth was -3.2% QoQ annualized in South Africa, -1.7% in Korea, and -0.8% in both Brazil and Mexico. Only less China-sensitive markets such as Russia (3.3%) and India (6.5%) held up. Interest rates: U.S. inflation has softened on the surface, with the core PCE measure slipping to 1.6% in April. However, some of the softness was driven by transitory factors, notably the decline in financial advisor fees (which tend to move in line with the stock market) which deducted 0.5 points from core PCE inflation. A less volatile measure, the trimmed mean PCE deflator, however, continues to trend up and is above the Fed’s 2% target. Partly because of the weaker historical inflation data, inflation expectations have also fallen (panel 4). As a result, central banks everywhere have become more dovish, with the Australian and New Zealand reserve banks cutting rates and the Fed and ECB raising the possibility they may ease too. The consequence has been a big fall in 10-year government bonds yields: in the U.S. to only 2% from 3.1% as recently as last September. Global Equities Chart 19Worrisome Earnings Prospects

Worrisome Earnings Prospects

Worrisome Earnings Prospects

Remain Cautiously Optimistic, Adding Another China Hedge: Global equities managed to eke out a small gain of 3.3% in Q2 despite a sharp loss of 5.9% in May. Within equities, our defensive country allocation worked well as DM equities outperformed EM by 2.9% in Q2. Our cyclical tilt in global sector positioning, however, did not pan out, largely due to the 2% underperformance in global Energy as the oil price dropped by 2% in Q2. Going forward, BCA’s House View remains that global economic growth will pick up sometime in the second half thanks to accommodative monetary policies globally and the increasing likelihood of a large stimulus from China to counter the negative effect from trade tensions. This implies that equities are likely to rally again after a period of congestion within a trading range, supporting a cautiously optimistic portfolio allocation for the next 9-12 months. The “optimistic” side of our allocation is reflected in two aspects: 1) overweight equities vs. bonds at the asset class level; and 2) overweight cyclicals vs. defensives at the global sector level. However, corporate profit margins are rolling over and earnings growth revisions have been negative (Chart 19). Therefore, the “cautious” side of our allocation remains a defensive country allocation, reflected by overweighting DM vs. EM. Our macro view hinges largely on what happens to China. There is an increasing likelihood that China may be on a reflationary path to stimulate economic growth. We upgraded global Industrials in March to hedge against China’s re-acceleration. Now we upgrade Australia to neutral from a long-term underweight, by downgrading Japan to a slight underweight from neutral, because Australia will benefit more from China’s reflationary policies (see next page). Chart 20Australian Equities: Close The Underweight

Australian Equities: Close The Underweight

Australian Equities: Close The Underweight

Upgrade Australian Equities To Neutral The relative performance of MSCI Australian equities to global equities has been closely correlated with the CRB metal price most of the time. Since the end of 2015, however, the CRB metals index has increased by more than 40%, yet Australian equities did not outperform (Chart 20, panel 1). Why? The MSCI Australian index is concentrated in Financials (mostly banks) and Materials (mostly mining), as shown in panel 2. Aussie Materials have outperformed their global peers, but the banks have not (panel 3). The banks are a major source of financing for the mining companies (hence the positive correlation with metal prices). They are also the source of financing for the Aussie housing markets, which have weighed down on the banks’ performance over the past few years due to concerns about stretched valuations. We have been structurally underweight Australian equities because of our unfavorable view on industrial commodities, and also our concerns on the Australian housing market and the problems of the banks. This has served us well, as Australian equities have done poorly relative to the global aggregate since late 2012. Now interest rates in Australia have come down significantly. Lower mortgage rates should help stabilize house prices, which suffered in Q1 their worst year-on-year decline, 7.7%, in over three decades. Australian equity earnings growth is still slowing relative to the global earnings, but the speed of slowing down has decreased significantly. With 6% of GDP coming from exports to China, Aussie profit growth should benefit from reflationary policies from China (panel 4). Relative valuation, however, is not cheap (panel 5). All considered, we are closing our underweight in Australian equities as another hedge against a Chinese-led re-acceleration in economic growth. This is financed by downgrading Japan to a slight underweight (for more on Japan, see What Our Clients Are Asking, on page 11). Government Bonds Chart 21Limited Downside In Yields

Limited Downside In Yields

Limited Downside In Yields

Maintain Slight Underweight On Duration: After the Fed signaled at its June meeting that rates cuts were likely on the way, the U.S. 10-year Treasury yield dropped to 1.97% overnight on June 20, the lowest since November 2016. Overall, the 10-year yield dropped by 40 bps in Q2 to end the quarter at 2%. BCA’s Fed Monitor is now indicating that easier monetary policy is required. But that is already more than discounted in the 92 bps of rate cuts over the next 12 months priced in at the front end of the yield curve, and by the current low level of Treasury yields. (Chart 21). We see the likelihood of one or two “insurance” cuts by the Fed, but the current environment (with a record-high stock market, tight corporate spreads, 50-year low unemployment rate, and 2019 GDP on track to reach 2.5%) is not compatible with a full-out cutting campaign. In addition, the latest Merrill Lynch survey indicated that long duration is the most crowded global trade. Given BCA’s House View that the U.S. economy is not heading into a recession but rather experiencing a manufacturing slowdown mainly due to external shocks, the path of least resistance for Treasury yields is higher rather than lower. Investors should maintain a slight underweight on duration over the next 9-12 months. Chart 22Favor Linkers Over Nominal Bonds

Favor Linkers Over Nominal Bonds

Favor Linkers Over Nominal Bonds

Favor Linkers Vs. Nominal Bonds: Global inflation expectations have dropped anew in the second quarter, with the 10-year CPI swap rate now sitting at 1.55%, 41 bps lower than its 2018 high of 1.96%. However, historically, the change in the crude oil price tends to have a good correlation with inflation expectations. BCA’s Commodity & Energy Strategy service revised down its 2019 Brent crude forecast to an average of US$73 per barrel from US$75, but this implies an average of US$79 in H2. (Chart 22). This would cause a significant rise in inflation expectations in the second half, supporting our preference for inflation-linked over nominal bonds. We also favor linkers in Japan and Australia over their respective nominal bonds. Corporate Bonds Chart 23Profit Growth Should Still Outpace Debt Growth

Profit Growth Should Still Outpace Debt Growth

Profit Growth Should Still Outpace Debt Growth

We turned cyclically overweight on credit within a fixed-income portfolio in February. Since then, corporate bonds have produced 120 basis points of excess return over duration-matched Treasuries. We believe this bullish stance on credit will continue to pay dividends. The global leading economic indicators have started to stabilize while multiple credit impulses have started to perk up all over the world. Historically, improving global growth has been positive for corporate bonds (Chart 23, panel 1). A valid concern is the deceleration in profit growth in the U.S., as the yearly growth of pre-tax profits has fallen from 15% in 2018 Q4 to 7% in the first quarter of this year. In general, corporate bonds suffer when profit growth lags debt growth, as defaults tends to rise in this environment. Is this scenario likely over the coming year? We do not believe so. While weak global growth at the end of 2018 and beginning of 2019 is likely to weigh on revenues, the current contraction in unit labor costs should bolster profit margins and keep profit growth robust (panel 2). Additionally, the Fed’s Senior Loan Officer Survey shows that C&I loan demand has decreased significantly this year, suggesting that the pace of U.S. corporate debt growth is set to slow (panel 3). How long will we remain overweight? We expect that the Federal Reserve will do little to no tightening over the next 12 months. This will open a window for credit to outperform Treasuries in a fixed-income portfolio. We have also reduced our double underweight in EM debt, since an acceleration of Chinese monetary stimulus would be positive for this asset class. Commodities Chart 24Watch Oil And Be Wary Of Gold

Watch Oil And Be Wary Of Gold

Watch Oil And Be Wary Of Gold

Energy (Overweight): Supply/demand fundamentals continue to be the main driver of crude oil prices. However, it seems as though the market is discounting something else. President Trump’s tweets, OPEC+ coalition statements, and concerns about future demand growth are contributing to price swings (Chart 24, panel 1). According to the Oxford Institute for Energy Studies, weak demand has reduced oil prices by $2/barrel this year. That should be offset, however, by a much larger contribution from supply cuts, speculative demand, and a deteriorating geopolitical environment. We see crude prices tilted to the upside, as OPEC’s ability to offset any supply disruptions (besides Iran and Venezuela) is limited (panel 2). We expect Brent to average $73 in 2019 and $75 in 2020. Industrial Metals (Neutral): A stronger USD accompanied by weakening global growth since 2018 has put downward pressure on industrial metal prices, which are down about 20% since January 2018. However, we now have renewed belief that the Chinese authorities will counter with a reflationary response though credit and fiscal stimulus. That should push industrial metal prices higher over the coming 12 months (panel 3). Precious Metals (Neutral): Allocators to gold are benefiting from the current environment of rising geopolitical risk, dovish central banks, a weaker USD, and the market’s flight to safety. Escalated trade tensions, falling global yields, and lower growth prospects are some of the factors that have supported the bullion’s 18% return since its September 2018 low. Until evidence of a bottom in global growth emerges, we expect the copper-to-gold ratio – another barometer for global growth – to continue falling (panel 4). The months ahead could see a correction, as investors take profits with gold in overbought territory. Nevertheless, we continue to recommend gold as both an inflation hedge as well as against any uncertain escalated political tensions. Currencies Chart 25Stronger Global Growth Will Weigh On The Dollar

Stronger Global Growth Will Weigh On The Dollar

Stronger Global Growth Will Weigh On The Dollar

U.S. dollar: The trade-weighted dollar has been flat since we lowered our recommendation from positive to neutral in April. We expect that the Fed will cut rates at least once this year, easing financial conditions, and boosting economic activity. This will eventually prove negative for the dollar. However as long as the global economy is weak the greenback should hold up. Stay neutral for now. Euro: Since we turned bullish on the euro in April, EUR/USD has appreciated by 1.5%. Overall, we continue to be bullish on EUR/USD on a cyclical timeframe. Forward rate expectations continue to be near 2014 lows, suggesting that there is little room for U.S. monetary policy to tighten further vis-à-vis euro area monetary policy, creating a floor under the euro (Chart 25, panel 1). EM Currencies: We continue to be negative on emerging market currencies. However, some indicators suggest that Chinese weakness, the main engine behind the EM currency bear market might be reaching its end. Chinese marginal propensity to spend (proxied by M1 growth relative to M2 growth), has bottomed and seems to have stabilized (panel 2). The bond market has taken note of this development, as Chinese yields are now rising relative to U.S. ones (panel 3). Historically, both of these developments have resulted in a rally for emerging market currencies. Thus, while we expect the bear market to continue for the time being, the pace of decline is likely to ease, making EM currencies an attractive buy by the end of the year. Accordingly, we are reducing our underweight in EM currencies from double underweight to a smaller underweight position. Alternatives

Chart 26

Return Enhancers: Hedge funds historically display a negative correlation with global growth momentum. Despite growth slowing over the past year, hedge funds underperformed the overall GAA Alternatives Index as well as private equity. Hedge funds usually outperform other risky alternatives during recessions or periods of high credit market stress. Credit spreads have been slow to rise in response to the slowing economy and worsening political environment. A pickup in spreads should support hedge fund outperformance (Chart 26, panel 2). Inflation Hedges: As we approach the end of the cycle, we continue to recommend investors reduce their real estate exposure and increase allocations towards commodity futures. Our May 2019 Special Report4 analyzed how different asset classes perform in periods of rising inflation. Our expectation is that inflation will pick up by the end of the year. An allocation to commodity futures, particularly energy, historically achieved excess returns of nearly 40% during periods of mild inflation (panel 3). Volatility Dampeners: Realized volatility in the catastrophe bond market is generally low. In fact, absent any catastrophe losses, catastrophe bonds provide stable returns, with volatility that is comparable to global bonds (panel 4). In a December 2017 Special Report,5 we tested for how the inclusion of catastrophe bonds in a traditional 60/40 equity-bond portfolio would have impacted portfolio risk-return characteristics. Replacing global equities with catastrophe bonds reduced annualized volatility by more than 1.5%. Risks To Our View Chart 27What Risk Of Recession?

What Risk Of Recession?

What Risk Of Recession?

Our main scenario is sanguine on global growth, which means we argue that bond yields will not fall much below current levels. The risks to this view are mostly to the downside. There could be a full-blown recession. Most likely this would be caused either by China failing to do stimulus, or by U.S. rates being more restrictive than the Fed believes. Both of these explanations seem implausible. As we argue elsewhere, we think it unlikely that China would simply allow growth to slow without reacting with monetary and fiscal stimulus. If current Fed policy is too tight for the economy to withstand, it would imply that the neutral rate of interest is zero or below, something that seems improbable given how strong U.S. growth has been despite rising rates. Formal models of recession do not indicate an elevated risk currently (Chart 27). We continue to watch for the timing to move into higher-beta China-related markets as the effects of China’s stimulus start to come through. Even if growth is as strong as we forecast, is there a possibility that bond yields fall further. This could come about – for a while, at least – if the Fed is aggressively dovish, oil prices fall (perhaps because of a positive supply shock), inflation softens further, and global growth remains sluggish. Absent a recession, we find those outcomes unlikely. The copper-to-gold ratio has been a good indicator of U.S. bond yields (Chart 28). It suggests that, at 2%, the 10-year Treasury yield has slightly overshot. In fact, in June copper prices started to rebound, as the market began to price in growing Chinese demand. Chart 28Can Bond Yields Fall Any Further?

Can Bond Yields Fall Any Further?

Can Bond Yields Fall Any Further?

Chart 29Are Analysts Right To Be So Gloomy?

Are Analysts Right To Be So Gloomy?

Are Analysts Right To Be So Gloomy?

For U.S. equities to rise much further, multiple expansion will not be enough; the earnings outlook needs to improve. Analysts are still cautious with their bottom-up forecasts, expecting only 3% EPS growth for the S&P500 this year (Chart 29). This seems easy to beat. But a combination of further dollar strength, worsening trade war, further slowdown in Europe and Emerging Markets, and higher U.S. wages would put it at risk. Footnotes 1 Please see What Our Clients Are Asking on page 9 of this Quarterly for further discussion on why we are confident China will ramp up stimulus if necessary. 2 Trimmed Mean PCE inflation, a better indicator of underlying inflation than the Core PCE deflator, is above 2%. Please see What Our Clients Are Asking on page 8 of this Quarterly for details. 3 Please see U.S. Bond Strategy Weekly Report, “Track Records,” dated June 18, available at usb.bcaresearch.com. 4 Please see Global Asset Allocation Special Report “Investors’ Guide To Inflation Hedging: How To Invest When Inflation Rises,” dated May 22, 2019 available at gaa.bcaresearch.com 5 Please see Global Asset Allocation Special Report “A Primer On Catastrophe Bonds,” dated December 12, 2017 available at gaa.bcaresearch.com GAA Asset Allocation

Image

Highlights Fed policy is likely to proceed in two stages: An initial stage characterized by a highly accommodative monetary policy, followed by a second stage where the Fed is raising rates aggressively in response to galloping inflation. The first stage, which will end in late 2021, will be heaven for risk assets. The subsequent stage, which will feature a global recession, will be hell. In the end, we expect the fed funds rate to reach 4.75%, representing thirteen more 25-basis point hikes than implied by current market pricing. For the time being, investors should maintain a pro-risk stance: Overweight global equities and high-yield credit relative to government bonds and cash. Regardless of what happens to the trade negotiations, China is stimulating its economy, which will benefit global growth. As a countercyclical currency, the dollar will weaken over the next 12 months. Cyclical stocks will outperform defensives. We expect to upgrade European and EM stocks this summer. Feature Dear Client, In lieu of next week’s report, I will be hosting a webcast on Wednesday, July 3rd at 10:00 AM EDT, where I will be discussing the major investment themes and views I see playing out for the rest of the year and beyond. Best regards, Peter Berezin, Chief Global Strategist Macro Outlook Right On Stocks, Wrong On Bonds We turned structurally bullish on global equities following December’s sell-off, having temporarily moved to the sidelines last June. This view has generally played out well. In contrast, our view that bond yields would rise this year as stocks recovered has been one gigantic flop. What went wrong with the bond view? The answer is that central banks are reacting to incoming news and data differently than in the past. As we discuss below, this has monumental implications for investment strategy. A Not So Recessionary Environment If one had been told at the start of the year that investors would be expecting the fed funds rate to fall to 1.5% by mid-2020 – with a 93% chance that the Fed would cut rates at least twice and a 62% chance it will cut rates three times in 2019 – one would probably have assumed that the U.S. had teetered into recession and that the stock market would be down on the year (Chart 1).

Chart 1

Instead, the S&P 500 is near an all-time high, while credit spreads have narrowed by 145 bps since the start of the year. Outside the manufacturing sector, the economy continues to grow at an above-trend pace and the unemployment rate is below most estimates of full employment. According to the Atlanta Fed, real final domestic demand is set to increase by 2.8% in Q2, up from 1.6% in Q1. Real personal consumption expenditures are tracking to rise at a 3.7% annualized pace (Chart 2).

Chart 2

So why is the Fed telegraphing rate cuts when real interest rates are barely above zero? A few reasons stand out: Global growth has slowed (Chart 3). The trade war has heated up again following President Trump’s decision to further increase tariffs on Chinese goods. Inflation expectations have fallen in the U.S. as well as around the world (Chart 4). Chart 3Global Growth Has Slowed

Global Growth Has Slowed

Global Growth Has Slowed

Chart 4Inflation Expectations Have Fallen Around The World

Inflation Expectations Have Fallen Around The World

Inflation Expectations Have Fallen Around The World

There’s More To The Story As important as they are, these three factors, even taken together, would not be enough to justify rate cuts were it not for an additional consideration: The Fed, like most other major central banks, has become increasingly worried that the neutral rate of interest – the rate consistent with full employment and stable inflation – is extremely low. This has resulted in a major shift in its reaction function. Nobody really knows exactly where the neutral rate is. According to the widely-cited Laubach Williams (L-W) model, the nominal neutral rate stands at 2.2% in the United States. This is close to current policy rates (Chart 5). The range for the longer-term interest rate dot in the Summary of Economic Projections is between 2.4% and 3.3%, which is higher than the L-W estimate. However, the range has trended lower since it was introduced in 2014 (Chart 6). Chart 5The Fed Thinks Rates Are Close To Neutral

The Fed Thinks Rates Are Close To Neutral

The Fed Thinks Rates Are Close To Neutral

Chart 6

A Fundamental Asymmetry Given that inflation expectations are quite low and there is considerable uncertainty over the level of the neutral rate, it does make some sense for policymakers to err on the side of being too dovish rather than too hawkish. This is because there is an asymmetry in monetary policy in the current environment. If the neutral rate turns out to be higher than expected and inflation starts to accelerate, central banks can always raise rates. In contrast, if the neutral rate turns out to be very low, the decision to hike rates could plunge the economy into a downward spiral. Historically, the Fed has cut rates by over five percentage points during recessions (Chart 7). At the present rate of inflation, the zero-lower bound on interest rates would be quickly reached, at which point monetary policy would become largely impotent. Chart 7The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

The asymmetry described above argues in favor of letting the economy run hot in order to allow inflation to rise. A higher inflation rate going into a recession would let a central bank push real rates deeper into negative territory before the zero bound is reached. In addition, a higher inflation rate would facilitate wage adjustments in response to economic shocks. Firms typically try to reduce costs when demand for their products and services declines, but employers are often wary of cutting nominal wages. Even though it is not fully rational, workers get more upset when they are told that their wages will fall by 2% when inflation is 1% than when they are told their wages will rise by 1% when inflation is 3%. More controversially, a modestly higher inflation rate could improve financial stability. In a low-inflation, low-nominal-rate environment, risky borrowers are likely to be able to roll over loans for an extended period of time. This could lead to the proliferation of bad debt. Chart 8Higher Underlying Inflation Can Cushion Nominal Asset Price Declines

Higher Underlying Inflation Can Cushion Nominal Asset Price Declines

Higher Underlying Inflation Can Cushion Nominal Asset Price Declines

Higher inflation can also cushion the blow from a burst asset bubble. For example, the Case-Shiller 20-City Composite Index fell by 34% between 2006 and 2012, or 41% in real terms. If inflation had averaged 4% over this period and real home prices had fallen by the same amount, nominal home prices would have declined by only 26%, resulting in fewer underwater mortgages (Chart 8). A New Reaction Function It is usually a mistake to base market views on an opinion about what policymakers should do rather than what they will do. On rare occasions, however, the opposite is true. And, where our Fed call is concerned, this seems to be the case. Where we fumbled earlier this year was in assuming the Fed would follow a more traditional, Taylor Rule-based monetary framework, which calls for raising rates as the output gap shrinks. Instead, the Fed has adopted a risk-based approach of the sort described above, reminiscent in many ways of the optimal control framework that Janet Yellen set out in 2012. The New Normal Becomes The New Consensus

Chart 9