Gov Sovereigns/Treasurys

Highlights Fed: Depressed U.S. Treasury yields now discount more rate cuts than the FOMC is likely to deliver, even for “insurance” purposes to offset the negative growth impacts from trade policy uncertainty. Maintain a below-benchmark strategic U.S. duration stance, and stay underweight the U.S. in global hedged government bond portfolios. JGBs: The low yield beta of Japanese government bonds can be a useful diversifier of duration risk in global government bond portfolios. We recommend taking advantage of this by increasing allocations to Japan, out of U.S. Treasuries, on a currency-hedged basis (in USD). Feature June FOMC Preview: Hawks & Doves, Living Together, Mass Hysteria! The next two days will be critical for global bond markets, with the U.S. Federal Reserve set to update its outlook for U.S. monetary policy. The only logical interpretation of current market pricing is that bond investors now expect a major hit to U.S. (and global) business confidence and economic growth from a U.S.-China trade war - without any lasting pickup in U.S. inflation from the tariffs. The Fed is stuck in a difficult position at the moment. Looking purely at the state of the economy, there is no immediate need for rate cuts. The unemployment rate is still low at 3.6%; real GDP growth was a solid 3.1% in Q1 and the Atlanta Fed’s GDPNow model estimates Q2 growth will be a trend-like 2.1%; and consumer confidence remains healthy. Our Global Duration Indicator has hooked up, driven by an improving global leading economic indicator and stabilizing economic sentiment surveys. Yet despite this, U.S. Treasury yields have melted down to levels consistent with much weaker economic growth and inflation, with -83bps of Fed rate cuts now discounted over the next twelve months (Chart of the Week). Chart of the WeekToo Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Too Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Too Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Chart 2U.S. Business Confidence: Fraying On The Edges

U.S. Business Confidence: Fraying On The Edges

U.S. Business Confidence: Fraying On The Edges

The only logical interpretation of current market pricing is that bond investors now expect a major hit to U.S. (and global) business confidence and economic growth from a U.S.-China trade war - without any lasting pickup in U.S. inflation from the tariffs. Reducing interest rates now would be the appropriate pre-emptive policy response, even if the current health of the economy does not justify a need to ease. A look at various U.S. business confidence surveys confirms that interpretation. Both the NFIB Small Business Confidence index and the Duke CFO U.S. Economic Outlook index are still at fairly high levels, but have clearly softened in recent months (Chart 2, top panel). The deterioration in the Duke CFO measure has come from a sharp fall in the percentage of respondents who are more optimistic on the U.S. economic outlook – a move mirrored by the deterioration in the Conference Board’s survey of CEO Confidence (second panel). On the inflation side, the Duke CFO survey shows that companies have dramatically cut back on their planned increases for labor compensation over the next year, from 5.1% in the March survey to 3.8% in the June survey (third panel). Plans for price increases over the next year have also collapsed from 2.7% to 1.4% in the June survey (bottom panel). As the FOMC deliberates, the doves will make the following case for an insurance rate cut now (Chart 3): The U.S. manufacturing sector has caught up with the global downturn. Market-based inflation expectations remain below levels consistent with the Fed’s 2% PCE inflation target (between 2.3% and 2.4% using CPI-based TIPS breakevens). The 10-year/3-month U.S. Treasury yield curve remains inverted, typically a sign that monetary policy has become restrictive. The trade-weighted dollar remains near the post-crisis highs, even as U.S. bond yields have plunged. Global economic policy uncertainty remains elevated. Meanwhile, the hawks on the FOMC will argue that easing would be premature (Chart 4): Chart 3The Case For Fed Rate Cuts

The Case For Fed Rate Cuts

The Case For Fed Rate Cuts

Chart 4The Case Against Fed Rate Cuts

The Case Against Fed Rate Cuts

The Case Against Fed Rate Cuts

U.S. equities are only 2% below the all-time high. High-yield spreads are stable and nowhere close to the peaks seen during previous bouts of market turmoil. A similar argument applies for market volatility, with the VIX index also relatively subdued in the mid-teens. Global leading economic indicators are bottoming out. Underlying realized inflation trends – average hourly earnings growth, trimmed mean inflation measures – are sticky, at cyclical highs. Given the compelling arguments on both sides, the most likely outcome tomorrow will be the Fed holding off on cutting rates, but making a clear case for what it will take to ease at the July 30-31 FOMC meeting. We imagine that checklist to include: a) Failure of U.S.-China trade talks at the G-20 summit later this month to progress toward an agreement. b) The June U.S. Payrolls report, to be released on July 5th, confirming that the soft May reading was not a one-off. c) The June Consumer Price Index report to be released on July 11th, and the May PCE deflator reading out on July 28th, showing no acceleration of some of the “transitory” components that the Fed believes has been dampening U.S. core inflation. d) A major pullback in U.S. equities and/or a widening of U.S. corporate bond spreads, leading to tighter U.S. financial conditions. Chart 5The Market & FOMC Disagree On The Terminal Rate

The Market & FOMC Disagree On The Terminal Rate

The Market & FOMC Disagree On The Terminal Rate

A new set of FOMC economic projections will be unveiled at this meeting, providing the intellectual cover for the Fed to signal that a rate cut is imminent. A new set of interest rate projections will also be provided. While this current edition of the FOMC has been downplaying the importance of the message implied by those interest rate projections, any movement in the “dots” will be noticed by the markets. The dot plot has only existed in a phase of expected Fed tightening. A shift to a projected ease would be momentous. In particular, any shift in the longer run “terminal rate” dot would be critical to ascertaining the Fed’s reaction function (Chart 5). This is especially true given the wide gap between our estimate of the market expectation of the terminal funds rate for this cycle (the 5-year U.S. Overnight Index Swap rate, 5-years forward, which is currently at 2%) and the median FOMC member estimate of the terminal rate from the last set of economic projections in March (2.8%). If the Fed were to make the case for an insurance rate cut tomorrow, while also lowering the terminal rate estimate, this would suggest that the FOMC was growing more concerned over the medium-term economic outlook as fewer future rate hikes would be needed. More dovish guidance on near-term rate moves, but without any change in the terminal rate projection, would imply that the Fed would view any insurance rate cut as a temporary measure that would need to be reversed at a later date if global uncertainty abates, U.S. growth recovers and U.S. inflation rebounds. Whatever the outcome of this week’s FOMC meeting, U.S. Treasury yields now discount a lot of bad news on both growth and inflation. Both the real and inflation expectations component of the benchmark 10-year Treasury yield are at critical support levels (Chart 6), suggesting that yields can only decline further in the face of incrementally more bearish economic data. Given the risk/reward tradeoff of yields at current levels, we do not recommend chasing this Treasury market rally, and prefer to position for an eventual rebound in yields. Chart 6Not Much Downside Left For Treasury Yields

Not Much Downside Left For Treasury Yields

Not Much Downside Left For Treasury Yields

It is possible that the Fed gives a message this week that is more hawkish than the market expects, similar to last December, leading to a sharp selloff in risk assets that temporarily pushes the 10-year Treasury yield to 2%. Such an outcome would eventually force the Fed’s hand to cut rates down the road to offset the tightening of financial conditions and stabilize equity and credit markets. This will eventually trigger a rebound in Treasury yields via rising inflation expectations and investors’ moving out of bonds into risky assets. Given the risk/reward tradeoff of yields at current levels, we do not recommend chasing this Treasury market rally, and prefer to position for an eventual rebound in yields. Bottom Line: Depressed U.S. Treasury yields now discount more rate cuts than the FOMC is likely to deliver, even for “insurance” purposes to offset the negative growth impacts from trade policy uncertainty. Maintain a below-benchmark strategic U.S. duration stance, and stay underweight the U.S. in global hedged government bond portfolios. JGBs As A Duration Management Tool In Global Bond Portfolios It has been quite some time since we have discussed Japanese government bonds (JGBs) in this publication. That is for a good reason – they are an incredibly boring asset. We can think of many more interesting investments than a bond market with no yield, no volatility, no inflation and a central bank with no other viable policy options. Yet low Japanese interest rates make borrowing in yen a good source of funding for carry trades. JGBs also offer the usual safe-haven appeal during periods of risk aversion and recessions. JGBs are a low-beta sovereign bond market, making them a useful way to manage duration risk in a global bond portfolio – especially in environments like today, where JGB yields are higher than U.S. Treasury yields on a currency hedged basis (in U.S. dollars). Chart 7JGBs Are Essentially A 'Global Duration' Bet

JGBs Are Essentially A 'Global Duration' Bet

JGBs Are Essentially A 'Global Duration' Bet

Most relevant for global bond investors - JGBs typically outperform their developed market peers during periods of rising global bond yields, and vice versa. That can be seen in Chart 7, where we show the total return of the Barclays Bloomberg Japan government bond index, hedged into U.S. dollars, on a duration-matched basis to the Global Treasury index. That return is plotted versus the overall Global Treasury index yield-to-maturity. The correlation is clear from the chart: JGBs outperform when the global yield rises, and underperform when the global yield is falling. In other words, JGBs are a low-beta sovereign bond market, making them a useful way to manage duration risk in a global bond portfolio – especially in environments like today, where JGB yields are higher than U.S. Treasury yields on a currency hedged basis (in U.S. dollars). For bond investors with a view that U.S. Treasury yields have fallen too far and are likely to begin rising again, JGBs are a compelling alternative. Selling Treasuries for JGBs, and hedging the currency risk back into U.S. dollars, can be a way to gain a yield pickup while reducing sensitivity to U.S. bond yield changes (i.e. duration) by owning an asset with a low, or even negative, beta to Treasuries. Chart 8BoJ Needs To Ease, But Options Are Limited

BoJ Needs To Ease, But Options Are Limited

BoJ Needs To Ease, But Options Are Limited

Japan’s export-led economy is sputtering on worries over U.S.-China trade tensions which are dampening global growth sentiment more broadly. The Bank of Japan’s (BoJ) widely-watched Tankan survey shows that business confidence has turned more pessimistic; the manufacturing PMI has fallen below 50; and the OECD leading economic indicator for Japan is falling sharply. Even with the unemployment rate at a multi-decade low of 2.4%, wage growth remains muted and consumer confidence is softening. Our own BoJ Monitor is signaling the need for easier monetary policy, and there are now -9bps of rate cuts discounted in the Japanese Overnight Index Swap curve (Chart 8). The BoJ’s policy options, however, are limited. The official policy rate (the discount rate) is already negative, and pushing that lower risks damaging Japanese bank profitability even further. More dovish forward guidance is of limited impact with markets already priced for a prolonged period of low rates. The BoJ cannot pursue more quantitative easing (QE) either, as it already owns nearly 50% of all outstanding JGBs - a massive presence that has, at times, disrupted functionality in the JGB market. There is nothing on the horizon indicating that JGB yields will move much from current levels, allowing JGBs to maintain their defensive status in global bond portfolios. The only real policy tool left is Yield Curve Control (YCC), where the BoJ has been targeting a 10-year JGB yield close to 0% and managing purchases to sustain the yield target. In our view, any upward adjustment of that yield target range (currently 0-0.2% on the 10yr JGB) would require a combination of three factors: The USD/JPY exchange rate must increase back to at least the 115-120 range, to provide a lower starting point for the likely yen appreciation that would occur if the BoJ targeted a higher bond yield. Japanese core CPI inflation and nominal wage growth must both rise and remain above 1.5%, which is close enough to the BoJ’s 2% inflation target to justify an increase in nominal bond yields. The momentum in the yield differential between 10-year Treasuries and JGBs must be overshooting to the upside; the BoJ would not want to keep JGB yields too depressed for too long if the global economy was strong enough to boost non-Japanese yields at a rapid pace. Chart 9BoJ Yield Curve Control Is Here To Stay

BoJ Yield Curve Control Is Here To Stay

BoJ Yield Curve Control Is Here To Stay

Currently, none of those criteria is in place (Chart 9). USD/JPY is down to 108; core CPI inflation is 0.6%; real wage growth is effectively zero; and the 10yr U.S.-Japan bond spread is contracting. There is nothing on the horizon indicating that JGB yields will move much from current levels, allowing JGBs to maintain their defensive status in global bond portfolios. Changes to our model bond portfolio We have been recommending an overweight stance on JGBs in our model portfolio for much of the past two years. This is in line with our long-held view that global bond yields had to rise on the back of improving global growth and the slow normalization of interest rates by the Fed and other central banks not named the Bank of Japan. Events this year have obviously challenged that view and we have reduced the size of our recommended overweight in our model bond portfolio. Given our view that U.S. Treasury yields are likely to grind higher in the next few months, we see a need to turn to Japan as a way to play defense against a rebound in global bond yields. That means increasing the Japan allocation, and decreasing the U.S. allocation, in our model bond portfolio. We can fine-tune that allocation shift based on the empirical yield betas of U.S. Treasuries to JGBs across different maturity buckets. In Chart 10, we show the rolling 52-week yield beta of JGBs to the other major developed bond markets, shown at the four critical yield curve points (2-year, 5-year, 10-year and 30-year). In all cases, the yield beta is low and fairly consistent across all maturities. When looking at those same rolling betas using yields hedged into U.S. dollars, shown in Chart 11, the story changes (note that we are using hedged yield data from Bloomberg Barclays, so the maturity buckets correspond to those used in the benchmark indices). The yield betas between JGBs and other markets are at or below zero in the 3-5 year and 7-10 year maturity buckets, with particularly large negative betas versus U.S. Treasuries. This implies that there is a gain to be made by focusing any Japan-for-U.S. switch in currency-hedged global bond portfolios on bonds with maturities between three and ten years. Chart 10JGBs Are Low-Beta To Global Yields...

JGBs Are Low-Beta To Global Yields...

JGBs Are Low-Beta To Global Yields...

Chart 11...And Even Negative-Beta After Hedging Into USD

...And Even Negative-Beta After Hedging Into USD

...And Even Negative-Beta After Hedging Into USD

Based on this analysis, and our view on U.S. Treasuries laid out earlier in this report, we are making a shift in our model bond portfolio on page 12 – cutting the weight in the maturity buckets in the middle of the Treasury curve and placing the proceeds into similar maturity buckets in Japan. Bottom Line: The low yield beta of Japanese government bonds can be a useful diversifier of duration risk in global government bond portfolios. We recommend taking advantage of this by increasing allocations to Japan, out of U.S. Treasuries, on a currency-hedged basis (into USD). Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA, Research Analyst ray@bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The Case For, And Against, Fed Rate Cuts

The Case For, And Against, Fed Rate Cuts

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights June FOMC Meeting: To appease markets, the Fed will at least have to signal that it stands ready to cut rates in July. While this is possible, there is a significant risk that the committee fails to deliver. We continue to advocate a cautious approach to corporate credit spreads in the near-term (0-3 months). Rate Cuts: The historical track record suggests that the 10-year Treasury yield can rise or fall in the immediate aftermath of a Fed rate cut. With a U.S. recession still far off, we see a good chance that Treasury yields will rise during the next 6-12 months, even if the Fed lowers rates in June or July. Treasury Yields: Yields have fallen a lot since the beginning of November, but the move isn't terribly anomalous relative to history. We use statistics to place recent price action in its appropriate historical context. Feature The Fed This Week Chart 1Credit Spreads At Risk

Credit Spreads At Risk

Credit Spreads At Risk

Tomorrow’s FOMC meeting is the main event in financial markets this week, with investors of all stripes eager to learn whether the Fed will deliver on the rate cut expectations that have already been priced into bond yields. As we’ve written in prior reports, our immediate concern is that the Fed may not sound dovish enough to appease markets, leading to further near-term widening in corporate bond spreads.1 Corporate bond excess returns have far outpaced commodity prices of late (Chart 1), leaving the sector vulnerable to any hawkish surprise. What’s Priced In, And Can The Fed Deliver? How dovish must the Fed be to prevent a sell-off in corporate credit? A look at current fed funds futures pricing shows that the market is looking for nearly three 25 basis point rate cuts spread over the next six FOMC meetings (Table 1). Roughly, the market expects one rate cut at either the June or July meeting, a second rate cut in either September or October, and a third rate cut in either December or January. To appease markets, the Fed will at least have to revise its 2019 funds rate projections down and signal that it stands ready to cut rates in July (Chart 2). While this is possible, there is a significant risk that the committee fails to deliver. We continue to advocate a cautious approach to corporate credit markets in the near-term (0-3 months). Table 1Fed Funds Futures: What's Priced In?

Track Records

Track Records

Chart 2Watch For Dot Plot Revisions

Watch For Dot Plot Revisions

Watch For Dot Plot Revisions

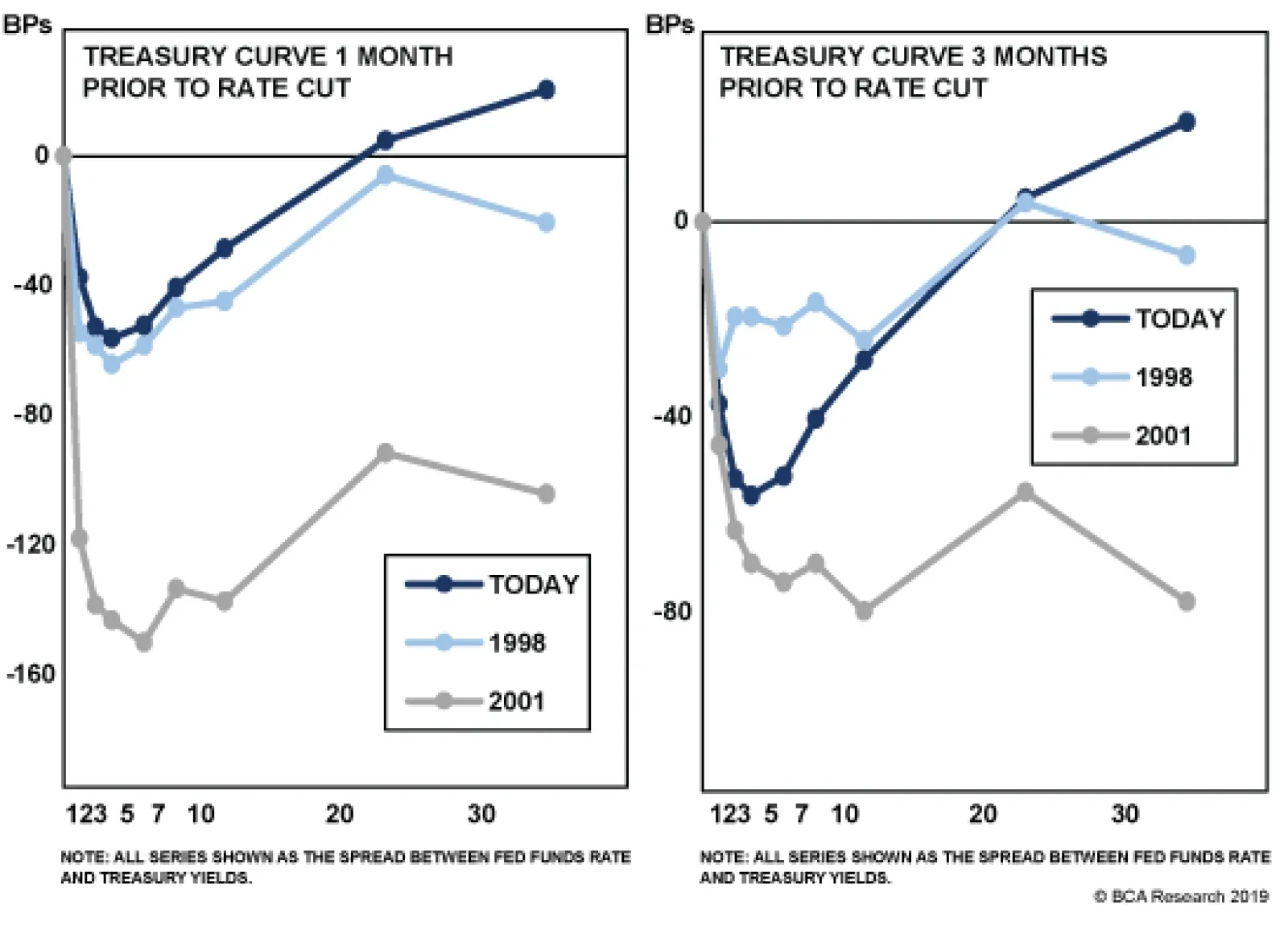

Fed Rate Cuts: A Track Record While we are cautious on corporate spreads in the near-term, we are also not willing to chase Treasury yields lower from current levels. Our view is that while the Fed might deliver a rate cut at one of the next few meetings, it is unlikely to lower rates by more than the 84 bps that are priced into the yield curve for the next 12 months. Ultimately, we expect Treasury yields to be higher on a 6-12 month horizon, even if the Fed cuts rates during the next few months. In response to this outlook, a few clients have asked whether it is possible for Treasury yields to rise so soon after a Fed rate cut. While we see no theoretical reason why it shouldn't be possible, it is always a good idea to stress test a theory against the historical track record. We therefore compiled a list of every Fed rate cut since 1995, and looked at how the 10-year Treasury yield reacted to each event. The results are displayed in Tables 2A-2D.

Chart

Chart

Chart

Chart

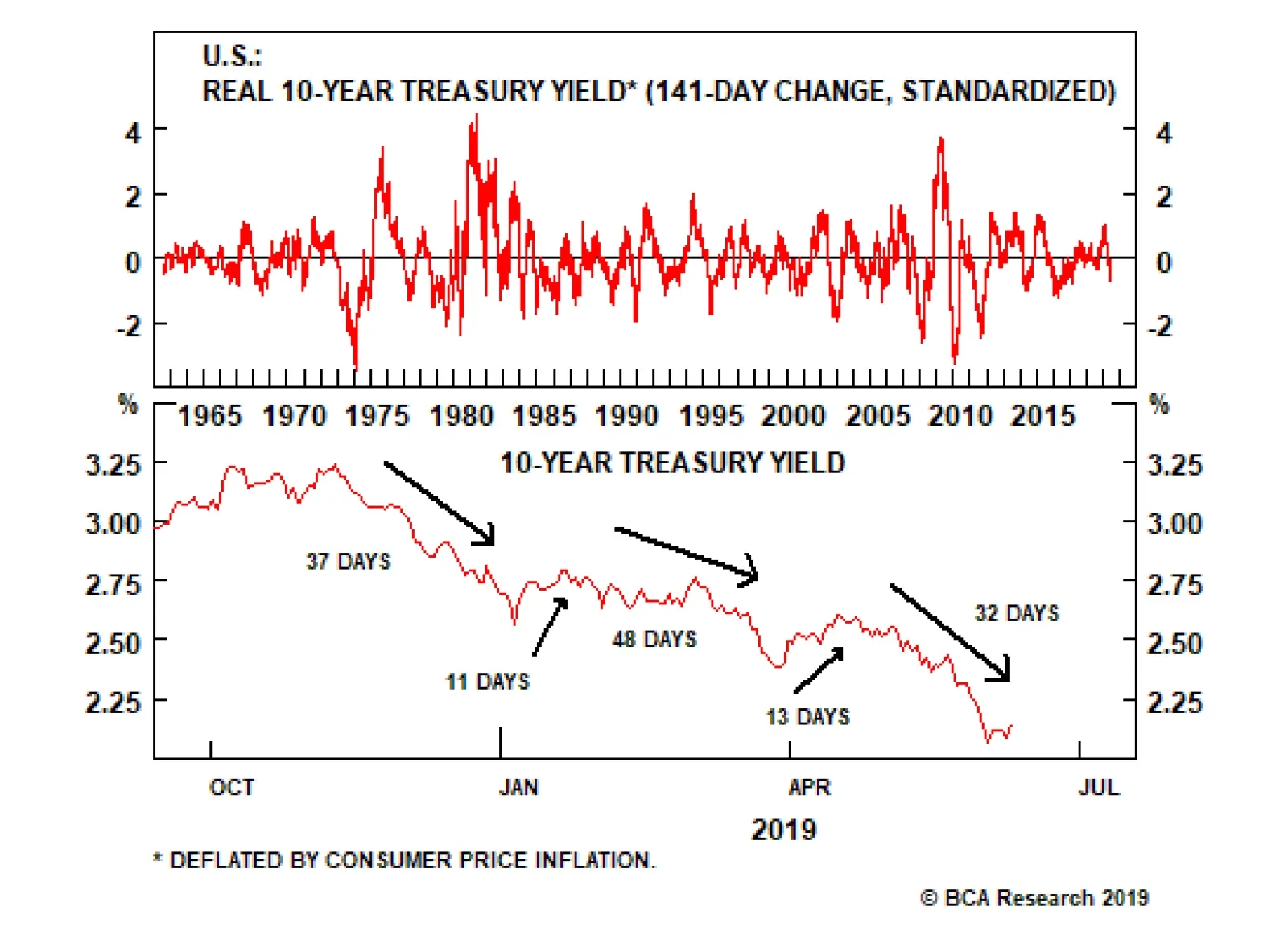

Table 2A shows the rate cuts that the Fed delivered in the mid-1990s, in response to persistently low U.S. inflation and slowing growth in the rest of the world. At the time, overall U.S. economic growth was quite solid and the U.S. economy didn’t fall into recession until 2001. The divergence between relatively strong U.S. economic growth and slower growth in the rest of the world makes the period look very similar to today, and we have long argued that the current cycle should be viewed in the context of the mid-1990s.2 Table 2A reveals that, on average, the 10-year Treasury yield tended to rise in the months following a rate cut, often even in the first 21 days. The historical track record suggests that the 10-year Treasury yield can rise or fall in the immediate aftermath of a Fed rate cut. Table 2C shows the rate cuts that were delivered during the economic recovery of the mid-2000s, and it paints a similar picture as Table 2A. In particular, the 10-year Treasury yield rose dramatically following the 2003 rate cut, and the Fed actually started to hike interest rates almost exactly one year after the 2003 cut. Tables 2B & 2D show the rate cuts that led into the 2001 and 2008 recessions. Not surprisingly, yields were much more likely to fall after the Fed cut rates in those episodes. Bottom Line: The historical track record suggests that the 10-year Treasury yield can rise or fall in the immediate aftermath of a Fed rate cut. The yield is much more likely to fall if the cut occurs in the run-up to a recession. With a U.S. recession still far off, we see a good chance that Treasury yields will rise during the next 6-12 months, even if the Fed lowers rates at one of the next few FOMC meetings. Treasury Yield Moves: A Track Record In recent weeks a BCA client who had been shaking his head at the large drop in Treasury yields reached out to see if we could put the recent moves in historical context. Specifically, he wondered how often such large yield moves have occurred in the past, and whether there is a tendency for moves of this magnitude to mean-revert. Our U.S. Investment Strategy team took a stab at answering these questions. The below analysis first appeared in last week's U.S. Investment Strategy report, but is re-printed here for the interest of U.S. bond clients.3 The ongoing decline in bond yields has felt like a big deal in real time, but it isn’t historically. The sharp decline in the 10-year Treasury yield that began in early November can be viewed as three separate declines (Chart 3). In the first, the 10-year yield fell by 68 basis points (“bps”) over a span of 37 trading days. After retracing a third of the decline over the next 11 sessions, it slid by another 40 bps over 48 days. Following a one-half retracement over the ensuing 13 days, it shed 53 basis points in 32 days, capped off by a 36-bps decline across the final eight sessions (Table 3). Chart 3The Path To 2.07%

The Path To 2.07%

The Path To 2.07%

Table 3A Lower 10-Year Treasury Yield In Three Steps

Track Records

Track Records

Using the daily 10-year Treasury yield series beginning in 1962, we compared the individual yield declines for prior 37-, 48- and 32-day periods, as well as for the aggregate 141-day session spanning the entire stretch from the November 8th peak to the June 3rd trough. We also looked at the May 21st to June 3rd crescendo relative to past eight-day segments. The standardized moves range from three-quarters of a standard deviation below the mean for the 48-day middle leg to 1.5 and 1.8 for the 37- and 8-day moves, respectively (Table 4). All in all, the entire move grades out to 1.3 standard deviations below the mean – a somewhat unusual move, but nothing too special. Table 4Standardized Values Of Nominal 10-Year Treasury Yield Declines

Track Records

Track Records

The current decline’s relative stature is undermined by the wild volatility of the late ‘70s and early ‘80s, when bond yields and annual inflation reached double-digit levels (Chart 4). To try to place the current episode on a more equal framework, we also calculated standardized moves in real (inflation-adjusted) yields. On a real basis, however, the current moves made even less of a splash. The 8-day decline (z-score = -1.2) was the only component that was more than a standard deviation from the mean, and the overall move amounted to just 0.7 standard deviations below the mean (Chart 5). Chart 4No Historical Anomaly In The Current Market

No Historical Anomaly In The Current Market

No Historical Anomaly In The Current Market

Chart 5Little Impact In Terms Of Real Yields

Little Impact In Terms Of Real Yields

Little Impact In Terms Of Real Yields

We are familiar with the electronic financial media’s increasingly popular convention of stating daily yield moves in proportion to the previous day’s closing yield.4 That convention has the advantage of fitting snugly aside stock price quotes on TV and computer screens, but it is ultimately nonsensical. The proportional change in a bond’s yield relative to its starting yield doesn’t come close to approximating the change in the value of that bond. Comparing proportional changes in bond yields across timeframes would be a way of putting today’s yield moves on a more equal footing with yield moves in the high-inflation, high-coupon era of the late seventies and early eighties, but it conveys no practical information. The standardized moves in real yields and Treasury index returns haven’t been a big deal. Our next steps were instead to compare Treasury total returns and the change in the slope of the yield curve to past flattening and steepening episodes. The moves here were also unavailing over both seven- and one-month periods, as the high-coupon ‘70s and ‘80s still dominated (Chart 6). In terms of the change in the 10-year Treasury yield, both nominal and real; Treasury index total returns; and the slope of the yield curve (3-month rate to 10-year yield), both the aggregate move since last October and its three component moves have amounted to one-standard-deviation events. They would only have had about a one-in-six chance of occurring randomly in a normally distributed population, but they do not represent unsustainable moves that cry out to be reversed. Chart 6Little Impact In Terms Of Treasury Total Returns, ...

Little Impact In Terms Of Treasury Total Returns, ...

Little Impact In Terms Of Treasury Total Returns, ...

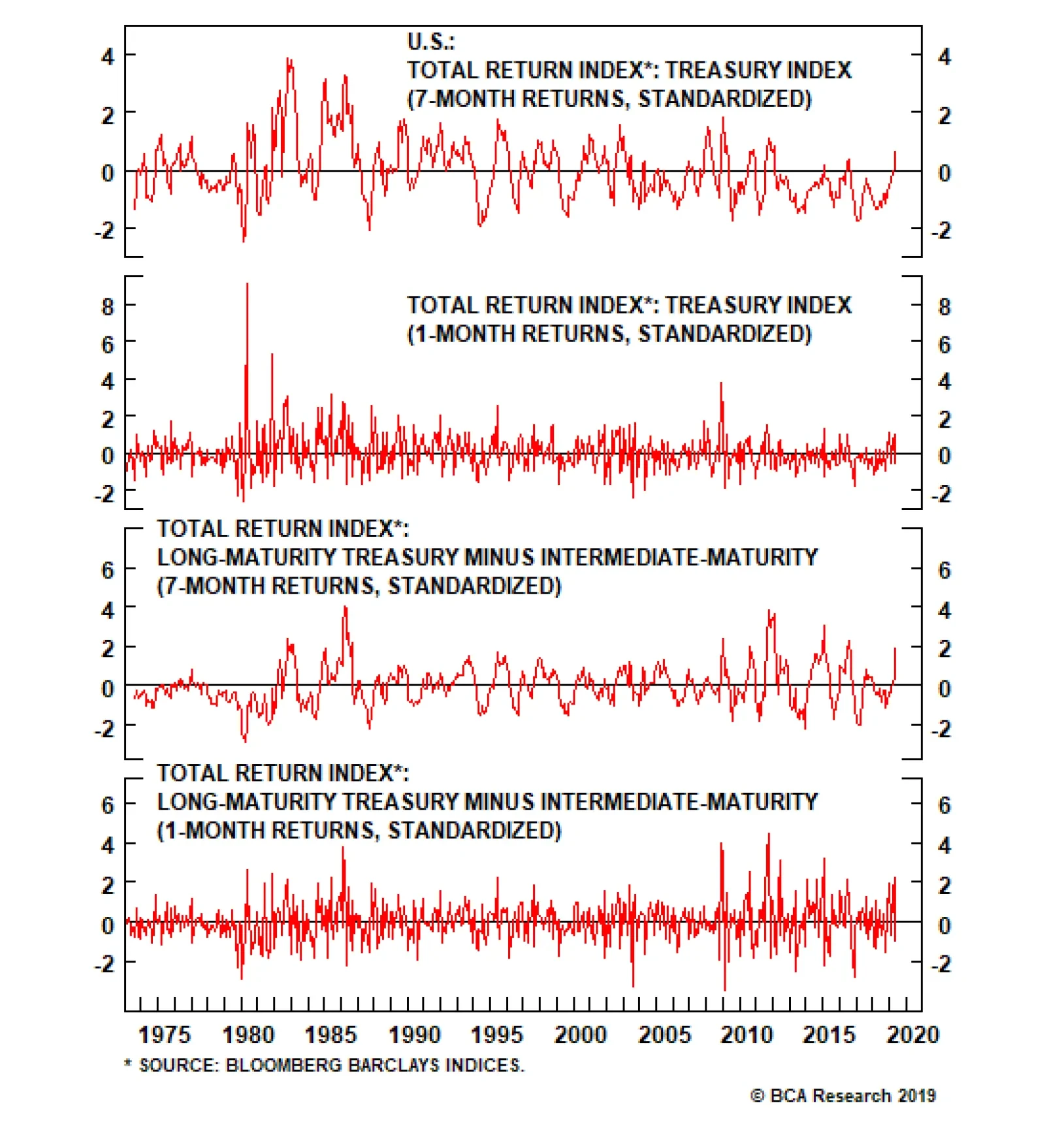

Digging a little deeper to consider total returns across different regions of the yield curve, we do find one apparent anomaly at the long end of the curve. The long Treasury index has outperformed the intermediate Treasury index by a two-standard-deviation margin over both a seven-month and a one-month timeframe (Chart 7). On a standalone basis, the long Treasury index has beaten the seven-month mean return by one-and-a-half standard deviations, and the one-month mean return by two standard deviations (Chart 8). The two-standard-deviation results would only be expected to occur one out of forty times, and thereby validate our client’s sense that something has been going on. Chart 7... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

Chart 8... And Long-Maturity Returns Have Been Elevated

... And Long-Maturity Returns Have Been Elevated

... And Long-Maturity Returns Have Been Elevated

The margin by which long-maturity Treasuries have outperformed intermediate-maturity Treasuries is unusual, and history suggests it will be partially unwound over the next six to twelve months. Moving on to the second part of his inquiry, we reviewed the standalone performance of the long Treasury index, and the relative long-versus-intermediate performance, over subsequent six- and twelve-month periods. We focused our analysis on instances when historical z-scores were greater than or equal to their current levels to try to determine if we should expect current performance to reverse and, if so, how sharply. On a standalone basis, long Treasury index performance has gently reverted to the mean over the subsequent six and twelve months, posting returns over those periods within +/- 0.2 standard deviations of its long-run average (Table 5). Table 5Standardized Values Of Future Long-Maturity Treasury Index Returns

Track Records

Track Records

Outlying relative long-versus-intermediate performance like we’ve witnessed over the last seven months has reversed more convincingly. The long Treasury index has underperformed its intermediate-maturity counterpart over six and twelve months when its z-scores were greater than or equal to their current levels over a seven- and one-month basis, falling roughly 0.5 standard deviations below the mean (Table 6). The future does not have to resemble the past, especially over small sample sizes, but relative long-end underperformance would accord with our constructive view of the U.S. economy. Table 6Standardized Values Of Future Difference Between Long- And Intermediate-Maturity Treasury Index Returns

Track Records

Track Records

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “Hedge Near-Term Credit Exposure”, dated May 28, 2019, available at usbs.bcaresearch.com 2 Please see U.S. Bond Strategy Weekly Report, “Tracking The Mid-1990s”, dated June 11, 2019, available at usbs.bcaresearch.com 3 Please see U.S. Investment Strategy Weekly Report, “Context”, dated June 10, 2019, available at usis.bcaresearch.com 4 If a bond yielding 3% at Friday’s close ends Monday’s session with a yield of 2.94%, 6 bps lower, its yield is shown as having declined 2% on the day (-.0006/.03 = -2%). Fixed Income Sector Performance Recommended Portfolio Specification

Employment growth usually starts to slow at least one year before the economy heads into recession. But it showed relatively little weakness in 1998 and 2015/16. If May’s downbeat payrolls number turns out to be the start of a trend, then we will have to…

Our main justification is that such a large number of rate cuts will only occur if the economy enters a recession. At present, the pre-conditions for an economic recession are simply not in place. Rather, the economy is experiencing an external shock – akin…

Highlights Fed: A Fed rate cut in June or July is not a done deal, but is looking increasingly likely purely from a risk management perspective, as it would both calm financial markets and potentially boost the inflation expectations component of Treasury yields. ECB: Easier monetary policy is required in Europe, and Mario Draghi hinted that rate cuts or even more QE are viable policy options. Depressed European bond yields (excluding Italy) suggest that this outcome is already fully priced. Maintain only a neutral allocation to core European government bonds. Feature Chart of the WeekA Lot Of "Negativity" In Bond Yields

A Lot Of "Negativity" In Bond Yields

A Lot Of "Negativity" In Bond Yields

The Great Global Bond Rally of 2019 has caught many by surprise – including, we admit with some humility, us. Not only has the pace of the decline in yields been impressive, but the outright yield levels seen in many markets are startlingly low. The 10-year German bund reach an all-time low of -0.25% last week, while sub-1% 10-year bond yields can be seen in “risky Peripherals” like Spain and Portugal. The ferocity of the global bond move has left 54% of all developed market government bonds trading with negative yields; the highest such percentage since July 2016 after the U.K. Brexit vote unnerved investors (Chart of the Week). There are parallels to today purely from a political risk perspective, given the trade tensions between the U.S. and China (and potentially any other country that the Trump Administration has issues with). Another comparison can be made versus three years ago when looking at more fundamental drivers of low global yields that require a response from policymakers – namely, slowing growth and sluggish inflation. Our Central Bank Monitors are now sending a clear message that easier monetary policy is needed in all the major developed economies (Chart 2). Given soft market-based inflation expectations, this suggests that policymakers must not only talk dovish, but act dovish, to defend the lower bound of price stability. Chart 2Pressure To Ease GLOBAL Monetary Policy

Pressure To Ease GLOBAL Monetary Policy

Pressure To Ease GLOBAL Monetary Policy

We’re seeing that in places like Australia and New Zealand, where policymakers have already cut rates. We can also see that in the euro area, where the ECB has introduced a new funding program to support bank lending (TLTRO3) and is now even contemplating restarting quantitative easing (QE). The Fed is next in line, with numerous Fed officials hinting that some easing of monetary policy could be on the horizon. Much easier monetary policy is already largely discounted in the current depressed level of global bond yields, though. While there are still risks to the growth outlook from trade uncertainty, we do not foresee a U.S./global recession on the immediate horizon. That means the risk/reward balance now favors some pickup in global bond yields, warranting a below-benchmark medium-term stance on duration exposure. Why “Insurance” Fed Cuts Are Likely Chart 3A Strong Dollar Is Disinflationary

A Strong Dollar Is Disinflationary

A Strong Dollar Is Disinflationary

Last week, the Federal Reserve held a research conference to discuss its monetary policy framework. Among the topics discussed were potential changes to the way the Fed manages its inflation target, including tolerating faster inflation after a period of below-target inflation. The goal of such “make-up” strategies would be to ensure that periods of low inflation do not get embedded into inflation expectations and bond yields. The problem with such strategies, however, is they are less likely to work if low interest rates and low inflation are a global phenomenon. The coordinated nature of the global bond rally has left the Fed facing a combination of rapidly falling Treasury yields alongside a strong U.S. dollar. With interest rate differentials continuing to favor the greenback, the currency is exerting downward pressure on commodity prices and, more generally, global inflation (Chart 3). Of course, the dollar does not only trade off interest rate differentials, but also global growth expectations, so some of the dollar rally seen this year reflects slowing non-U.S. economies and capital outflows from non-U.S. financial markets. What is clear, however, is that a strong dollar, and all it represents in terms of global growth, is disinflationary. Numerous Fed officials, including Fed Chairman Jay Powell, gave hints last week that they were open to considering interest rate cuts in response to signs of weakening U.S. growth and heightened trade uncertainty. With 5-year/5-year forward inflation expectations in the TIPS market now at 1.9% – still well below the 2.3-2.4% levels consistent with the Fed’s 2% target on the PCE deflator – the Fed has the cover to deliver one or two “insurance” rate cuts in the next few FOMC meetings. This would be consistent with their risk management framework. Our Central Bank Monitors are now sending a clear message that easier monetary policy is needed in all the major developed economies. Given soft market-based inflation expectations, this suggests that policymakers must not only talk dovish, but act dovish, to defend the lower bound of price stability. If the Fed fails to ratify markets’ dovish expectations at next week’s policy meeting, risk assets will likely sell off – perhaps violently, as occurred last December. That would deliver the kind of tightening in financial conditions that would force the Fed turn more dovish and eventually cut rates anyway. Alternatively, if the Fed actually cuts rates next week or in July and both the economy and inflation eventually recover, and risk assets surge higher, then the Fed can always take back those cuts with tighter policy later (especially if trade uncertainty diminishes with some sort of U.S.-China trade deal at the G20 meeting later this month). Such a strategy could even help Fed credibility by boosting inflation expectations back to levels more consistent with the Fed’s inflation target, which would also help put upward pressure on Treasury yields. Our Fed Monitor is now signaling the need for easier U.S. monetary policy, but that is already discounted in the 75bps of rate cuts (over the next twelve months) priced at the front-end of the yield curve, and in the current low level of Treasury yields (Chart 4). The Treasury rally also looks overdone when looking at other measures, such as the low level of mean-reverting U.S. data surprises, overbought price momentum and extended long duration positioning (Chart 5). Chart 4Treasuries Fully Priced For Fed Easing

Treasuries Fully Priced For Fed Easing

Treasuries Fully Priced For Fed Easing

Net-net, the medium-term risk/reward balance favors moderate below-benchmark duration positioning for Treasury investors, and underweight tilts for the U.S. in global government bond portfolios. More tactically, the amount of Fed rate cuts now discounted seems excessive with only the U.S. manufacturing sector cooling while the rest of the economy remains on firm footing. For that reason, we are already taking profits on one leg of our fed funds futures calendar spread trade initiated last week. The Treasury rally also looks overdone when looking at other measures, such as the low level of mean-reverting U.S. data surprises, overbought price momentum and extended long duration positioning Chart 5The Treasury Rally Looks Stretched

The Treasury Rally Looks Stretched

The Treasury Rally Looks Stretched

Chart 6Fed Funds Futures Trade: Exit Long Aug 2019, Stay Short Feb 2020

Fed Funds Futures Trade: Exit Long Aug 2019, Stay Short Feb 2020

Fed Funds Futures Trade: Exit Long Aug 2019, Stay Short Feb 2020

We recommended buying the August 2019 fed funds futures contract to hedge the risk that the Fed tries to get ahead of market sentiment by cutting rates in June or July. That contract would have returned a positive return in a scenario where the Fed delivered one 25 basis point rate cut in either June or July, and a negative return in a scenario where rates are unchanged. In only one week, that contract’s risk/reward profile has shifted dramatically. The contract is now priced for a loss in both the “one rate cut” and “no rate cut” scenarios. We therefore exit our long position in the August 2019 fed funds futures contract for a gain of +5bps. The second leg of our proposed trade was to short the February 2020 fed funds futures contract. This remains an excellent bet. As of last Friday, a short position in the February 2020 contract will earn a positive return as long as three or fewer rate cuts occur between now and next February (Chart 6). We are keeping this position on as a pure rates trade to play for the Fed delivering less than the market expects. Bottom Line: A Fed rate cut in June or July is not a done deal, but is looking increasingly likely purely from a risk management perspective, as it would both calm financial markets and potentially boost the inflation expectations component of Treasury yields. Are European Bond Yields Discounting More ECB QE? While we see little absolute value in U.S. Treasuries, there may not be much near-term upside in yields without an improvement in European economic growth. Simply put, Europe remains an anchor weighing on global bond yields. While we see little absolute value in U.S. Treasuries, there may not be much near-term upside in yields without an improvement in European economic growth. Simply put, Europe remains an anchor weighing on global bond yields. Our country diffusion indicators for the euro area – measuring the share of countries within the region that are seeing faster GDP growth, rising leading economic indicators and quickening headline inflation rates – all show that the current downturn is broad-based (Chart 7). Dating back to the introduction of the single currency zone in the late 1990s, there have been three periods where the country diffusion indicators were as weak as they are now. All three times lead to multiple interest rate cuts by the ECB. Chart 7A Broad-Based Slowing Of European Growth & Inflation

A Broad-Based Slowing Of European Growth & Inflation

A Broad-Based Slowing Of European Growth & Inflation

Our ECB Monitor is also calling for easier monetary policy in the euro area (Chart 8), driven by weakness in both the growth and inflation components. Chart 8Our ECB Monitor Says 'Ease', Bund Yields Agree

Our ECB Monitor Says 'Ease', Bund Yields Agree

Our ECB Monitor Says 'Ease', Bund Yields Agree

With the ECB policy rate already negative, however, the central bank is reluctant to push rates even lower and starve euro area banks of badly needed net interest margin. Chart 9TLTRO3 Will Help Italian & Spanish Banks The Most

TLTRO3 Will Help Italian & Spanish Banks The Most

TLTRO3 Will Help Italian & Spanish Banks The Most

At last week’s policy meeting, the ECB Governing Council committed to leaving rates unchanged through the first half of 2020. ECB President Mario Draghi noted in his press conference that forward guidance has “become the major monetary policy tool we have now”, suggesting that actual changes in interest rates will be more difficult to implement. Draghi also noted that the new TLTRO3 program was intended only as a “backstop” to sustain current levels of bank lending as the old TLTRO programs begin to roll off, not as a fresh source of stimulus. This was almost certainly aimed at the banks of Italy and Spain – countries that took up nearly 60% of the last TLTRO program that is now starting to roll off and where credit growth is contracting (Chart 9). The ECB worries that the weaker parts of the European banking system are becoming too reliant on cheap central bank funding, making it more difficult to end the liquidity program in the future without causing a credit crunch. German bunds have already priced in some sort of ECB easing (rate cuts or fresh bond buying). Our estimate of the term premium on the 10-year German bund yield is already deeply negative, which reflects both a risk aversion bid for safety and, potentially, some market expectation of incremental ECB QE. Chart 10Market Discounting Fresh ECB Bond Buying?

Market Discounting Fresh ECB Bond Buying?

Market Discounting Fresh ECB Bond Buying?

So if the ECB is reluctant to cut rates or subsidize more lending, what monetary ammunition is left? Draghi did hint last week that the topic of restarting the Asset Purchase Program (APP) came up in the ECB meeting as an option if the economic and inflation backdrop deteriorated further, or global trade uncertainty intensified. The ECB is facing a situation similar to when the APP was first announced in 2014. Inflation expectations, as measured by the 5-year/5-year forward euro CPI swap rate, are now down to 1.2% (Chart 10). It was a similar plunge in inflation expectations that wore down ECB hawks’ reticence to deploy quantitative easing back in 2014. German bunds have already priced in some sort of ECB easing (rate cuts or fresh bond buying). Our estimate of the term premium on the 10-year German bund yield is already deeply negative, which reflects both a risk aversion bid for safety and, potentially, some market expectation of incremental ECB QE. The latter interpretation would also explain the low level of bond yields seen in Peripheral Europe (excluding Italy, dealing with a deficit battle with the European Commission), as investors stretch for yield in anticipation of supportive future ECB policy. We see little investment value in euro area bonds at such low levels, given how much bad news on growth and inflation, and the potential monetary easing in response, is already discounted. Similar to U.S. Treasuries, the risk/reward balance favors a modest below-benchmark structural duration stance. The upside in European yields is still far more limited than for U.S. Treasury yields, given the much more fragile state of European growth and inflation expectations. Treasuries are thus more overpriced than bunds. Bottom Line: Easier monetary policy is required in Europe, and Mario Draghi hinted that rate cuts or even more QE are viable policy options. Depressed European bond yields (excluding Italy) suggest that this outcome is already fully priced. Maintain only a neutral allocation to core European government bonds. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations

Making Up Is Hard To Do

Making Up Is Hard To Do

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Our next steps were instead to compare Treasury total returns and the change in the slope of the yield curve to past flattening and steepening episodes. The moves here were also unavailing over both seven- and one-month periods, as the high-coupon ‘70s and…

In the first, the 10-year yield fell by 68 basis points (“bps”) over a span of 37 trading days. After retracing a third of the decline over the next 11 sessions, it slid by another 40 bps over 48 days. Following a one-half retracement over the ensuing 13…

Highlights Bond yields have fallen a lot since the beginning of November, … : At the close on November 8th, the 10-year Treasury bond yielded 3.24%. By last Monday, it was yielding just 2.07%. … but the move isn’t terribly anomalous relative to history: In terms of nominal yields, the decline was just over a one-standard-deviation event; per real yields, it amounted to a -0.7 sigma move. The Fed may be preparing for a rate cut, but overweight duration positions will only pay off if several more follow: A one-and-done rate cut would stretch out the expansion and the bull markets in equities and spread product, but Treasuries are priced for an extended rate-cutting cycle. Feature Stocks are said to be the only asset that people want more of when prices rise, and less of when they fall. Lately, bonds have also seemed to have an upward-sloping demand curve, because more and more people have bought them as they’ve gotten more expensive. A BCA client who’s been shaking his head at the action got in touch with us last week to try to make some sense of it all. Experience tells him that big moves like the one that’s been unfolding since last November don’t go on forever. When they stop, mean reversion would suggest that they’re prone to retrace a good bit of territory. He came to us for some historical context to support or contradict his intuition, as summed up in something like the following statement. “Over the past 50 years, the current move equates to an x-standard-deviation event. Following similar instances, rates have risen by x basis points over the next six months, and by y basis points over the next twelve months.” The Empirical Record The sharp decline in the 10-year Treasury yield that began in early November can be viewed as three separate declines (Chart 1). In the first, the 10-year yield fell by 68 basis points (“bps”) over a span of 37 trading days. After retracing a third of the decline over the next 11 sessions, it slid by another 40 bps over 48 days. Following a one-half retracement over the ensuing 13 days, it shed 53 basis points in 32 days, capped off by a 36-bps decline across the final eight sessions (Table 1). Chart 1The Path To 2.07%

The Path To 2.07%

The Path To 2.07%

Table 1A Lower 10-Year Treasury Yield In Three Steps

Context

Context

Using the daily 10-year Treasury yield series beginning in 1962, we compared the individual yield declines for prior 37-, 48- and 32-day periods, as well as for the aggregate 141-day session spanning the entire stretch from the November 8th peak to the June 3rd trough. We also looked at the May 21st to June 3rd crescendo relative to past eight-day segments. The standardized moves range from three-quarters of a standard deviation below the mean for the 48-day middle leg to 1.5 and 1.8 for the 37- and 8-day moves, respectively (Table 2). All in all, the entire move grades out to 1.3 standard deviations below the mean – a somewhat unusual move, but nothing too special. Table 2Standardized Values Of Nominal 10-Year Treasury Yield Declines

Context

Context

The current decline’s relative stature is undermined by the wild volatility of the late ‘70s and early ‘80s, when bond yields and annual inflation reached double-digit levels (Chart 2). To try to place the current episode on a more equal framework, we also calculated standardized moves in real (inflation-adjusted) yields. On a real basis, however, the current moves made even less of a splash. The 8-day decline (z-score = -1.2) was the only component that was more than a standard deviation from the mean, and the overall move amounted to just 0.7 standard deviations below the mean (Chart 3). Chart 2No Historical Anomaly In The Current Market

No Historical Anomaly In The Current Market

No Historical Anomaly In The Current Market

Chart 3Little Impact In Terms Of Real Yields

Little Impact In Terms Of Real Yields

Little Impact In Terms Of Real Yields

We are familiar with the electronic financial media’s increasingly popular convention of stating daily yield moves in proportion to the previous day’s closing yield.1 That convention has the advantage of fitting snugly aside stock price quotes on TV and computer screens, but it is ultimately nonsensical. The proportional change in a bond’s yield relative to its starting yield doesn’t come close to approximating the change in the value of that bond. Comparing proportional changes in bond yields across timeframes would be a way of putting today’s yield moves on a more equal footing with yield moves in the high-inflation, high-coupon era of the late seventies and early eighties, but it conveys no practical information. The margin by which long-maturity Treasuries have outperformed intermediate-maturity Treasuries is unusual, ... Our next steps were instead to compare Treasury total returns and the change in the slope of the yield curve to past flattening and steepening episodes. The moves here were also unavailing over both seven- and one-month periods, as the high-coupon ‘70s and ‘80s still dominated (Chart 4). In terms of the change in the 10-year Treasury yield, both nominal and real; Treasury index total returns; and the slope of the yield curve (3-month rate to 10-year yield), both the aggregate move since last October and its three component moves have amounted to one-standard-deviation events. They would only have had about a one-in-six chance of occurring randomly in a normally distributed population, but they do not represent unsustainable moves that cry out to be reversed. Chart 4Little Impact In Terms Of Treasury Total Returns, ...

Little Impact In Terms Of Treasury Total Returns, ...

Little Impact In Terms Of Treasury Total Returns, ...

Digging a little deeper to consider total returns across different regions of the yield curve, we do find one apparent anomaly at the long end of the curve. The long Treasury index has outperformed the intermediate Treasury index by a two-standard-deviation margin over both a seven-month and a one-month timeframe (Chart 5). On a standalone basis, the long Treasury index has beaten the seven-month mean return by one-and-a-half standard deviations, and the one-month mean return by two standard deviations (Chart 6). The two-standard-deviation results would only be expected to occur one out of forty times, and thereby validate our client’s sense that something has been going on. ... and history suggests they’ll be partially unwound over the next six to twelve months. Chart 5... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

... But The Spread Between Long- And Intermediate-Index Returns Is Wide, ...

Chart 6... And Long-Maturity Returns Have Been Elevated

... And Long-Maturity Returns Have Been Elevated

... And Long-Maturity Returns Have Been Elevated

Moving on to the second part of his inquiry, we reviewed the standalone performance of the long Treasury index, and the relative long-versus-intermediate performance, over subsequent six- and twelve-month periods. We focused our analysis on instances when historical z-scores were greater than or equal to their current levels to try to determine if we should expect current performance to reverse and, if so, how sharply. On a standalone basis, long Treasury index performance has gently reverted to the mean over the subsequent six and twelve months, posting returns over those periods within +/- 0.2 standard deviations of its long-run average (Table 3). Table 3Standardized Values Of Future Long-Maturity Treasury Index Returns

Context

Context

Outlying relative long-versus-intermediate performance like we’ve witnessed over the last seven months has reversed more convincingly. The long Treasury index has underperformed its intermediate-maturity counterpart over six and twelve months when its z-scores were greater than or equal to their current levels over a seven- and one-month basis, falling roughly 0.5 standard deviations below the mean (Table 4). The future does not have to resemble the past, especially over small sample sizes, but relative long-end underperformance would accord with our constructive view of the U.S. economy. It would also be consistent with our anti-duration and pro-inflation biases. Table 4Standardized Values Of Future Difference Between Long- And Intermediate-Maturity Treasury Index Returns

Context

Context

The Fed, Again The consistency of the comments from Fed officials last week would seem to suggest that they are trying to prepare the ground for a rate cut. A cut at next week’s FOMC meeting might be a little too abrupt, but it seems increasingly possible that the committee could guide markets to a cut at the next scheduled meeting at the end of July. Various officials have made it abundantly clear that they view trade tensions as a threat to the economy, and that the bank is prepared to adjust policy, if need be, to sustain the expansion. Uber-dovish St. Louis President Bullard, who said last Monday that, “a downward policy rate adjustment may be warranted soon,” no longer appears to be such an outlier. We do not think a rate cut is necessary, and we would be content to remain on the sidelines if we were on the committee, but our opinion is irrelevant. We endeavor not to be distracted by what we think should happen, devoting our focus instead to determining what’s most likely to happen. To that end, our estimate of the probability that the Fed’s next move might be a cut is rising by the speech/interview. When incorporating that probability into investment strategy, we have been thinking a lot about a question that keeps being raised within BCA: If the Fed cuts rates next week or next month, how will markets respond? Assuming the economic backdrop doesn’t deteriorate, we expect that a rate cut will keep the equity and credit bull markets going. The answer depends heavily on the context in which the Fed cuts, and we assume that if the Fed cuts after the economy has taken a dramatic turn for the worse, risk assets would decline. In that case, markets would presumably read the Fed’s decision as confirmation that things were even worse than they perceived and that a significant bout of risk aversion was right around the corner. On the other hand, if the cut came against a backdrop of decent, if unexciting, economic data, risk assets would likely rally. For an investor who cannot resist injecting his/her opinion into the mix, the market response would be supportive of risk assets if a rate cut was unnecessary, but negative if the economy couldn’t get along without it. Investment Implications We believe that the U.S. economy is doing just fine, thank you, and do not yet see the signs that the expansion requires more monetary accommodation if it is to continue. Assuming that the cast of the incoming data does not change enough to change our view, we would expect that a rate cut would defer the end of the expansion and thereby defer the end of the bull markets in risk assets. We are therefore content to stick with our recommendation that investors should remain at least equal weight equities and spread product. We are still looking for restrictive monetary policy to be the catalyst that ends the expansion, and anything that pushes restrictiveness further into the future ought to keep the market parties going. Our view has aligned with the house view over the last year, but there is no guarantee that it will continue to do so. A growing minority of managing editors has been repeatedly challenging the internal consensus in our daily meetings, and it will be debated vigorously at our monthly view meeting Monday morning in Montreal. It is possible that the house view, and the U.S. Investment Strategy view, could soon become less constructive, though our level of conviction remains fairly high. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 If a bond yielding 3% at Friday’s close ends Monday’s session with a yield of 2.94%, 6 bps lower, its yield is shown as having declined 2% on the day (-.0006/.03 = -2%).

Feature Through the past five years, the global long bond yield has tried to surpass 2.5 percent on three occasions – once in 2015, twice in 2018. But it has failed (Feature Chart). The global long bond yield’s five-year struggle to break through 2.5 percent convinces us that the so-called ‘neutral’ rate of interest is now extremely low, indeed zero in real terms. This is a very high conviction view though, to be clear, not every BCA strategist may necessarily concur. Feature ChartSince 2015, The Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, The Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, The Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

The neutral rate of interest is the interest rate at which monetary policy is neither accommodative nor restrictive, the interest rate consistent with the economy maintaining full employment while keeping inflation constant. That much is generally accepted. Here’s where we differ from the conventional thinking: what is setting the neutral rate now is not the economy’s direct sensitivity to the interest rate via rate sensitive sectors such as mortgage lending or home construction: rather, it is the economy’s indirect sensitivity to the interest rate via its impact on equities and other so-called ‘risky’ assets. This Special Report challenges the conventional wisdom on the neutral rate on three specific points: The neutral rate is based on the bond yield, not on the policy interest rate. The neutral rate is global, not European or region specific. The neutral rate is nominal, not real. The Neutral Rate Is Based On The Bond Yield, Not On The Policy Interest Rate

Chart I-2

The $400 trillion combined value of equities, corporate bonds, real estate and other risky assets dwarfs the $80 trillion global economy by five to one. These risky assets are long-duration assets, because their cash flows extend into the distant future. Hence, the market calibrates the expected return available on these risky assets from the supposedly less risky return available from long-duration bonds – the bond yield – plus a ‘risk premium’. Now comes the part of the story that is not well understood, even by central bankers, because it derives from recent advances outside their field of expertise. Years of research in behavioural finance conclude that the measure that best encapsulates our perception of an investment’s risk is not its volatility but its negative asymmetry: the potential largest loss as a multiple of the potential largest gain (Chart I-2). The $400 trillion combined value of equities, corporate bonds, real estate and other risky assets dwarfs the $80 trillion global economy by five to one. Crucially, when the bond yield gets low, the proximity of its lower bound dramatically reduces the potential for price gains while leaving open the potential for large losses. This sudden onset of negative asymmetry means that bonds are no longer less risky than equities or other risky assets (Chart I-3). So risky assets no longer need to deliver a higher expected return than bonds (Chart I-4).

Chart I-3

Chart I-4

Chart I-5Equities Offer Diversification Benefits Too!

Equities Offer Diversification Benefits Too!

Equities Offer Diversification Benefits Too!

Some people counter that bonds offer investors a diversification benefit and, because of this, investors still need a higher return from equities. This argument is wrong. Just as bonds can protect equity investors, equities can protect bond investors during vicious sell-offs in the bond market – such as after Trump’s shock victory in 2016 (Chart I-5). So we could equally argue that equities require the lower return. In fact, at a low bond yield, with the same negative asymmetry and diversification properties, both equities and bonds must offer the same prospective return. The upshot is that once the bond yield gets low and stays low, equity (and other risky asset) returns collapse to the feeble return offered by bonds with no additional ‘risk premium’ giving the valuation of $400 trillion of assets an exponential uplift (Chart I-6). The unfortunate corollary is that if the bond yield was no longer low, the valuation of $400 trillion of assets would suffer an exponential decline. And the consequent deterioration in financial conditions would send a chill wind through the global economy. Theoretically and empirically, the hyper-sensitivity of equity valuations to bond yields is greatest when the 10-year bond yield is in the 2-3 percent range. But which 10-year bond yield?1 Chart I-6Equities Are Now Priced To Generate A Feeble Long-Term Return

Equities Are Now Priced To Generate A Feeble Long-Term Return

Equities Are Now Priced To Generate A Feeble Long-Term Return

The Neutral Rate Is Global, Not European Or Region Specific The question: ‘will European equities go up or down?’ is essentially the same as ‘will U.S. equities go up or down?’ or ‘will Chinese equities go up or down?’ albeit the size of the moves can be quite different. The same applies to mainstream bond markets; in directional terms, bonds move together. Chart I-7The Global 10-Year Yield Is The Average Of The Euro Area, U.S., And China

The Global 10-Year Yield Is The Average Of The Euro Area, U.S., And China

The Global 10-Year Yield Is The Average Of The Euro Area, U.S., And China

Given this tight directional integration of global capital markets – and to some extent economies too – asset allocators make the asset class choice between equities and bonds their primary decision, and the regional allocation the subsidiary decision. It follows that the point of hyper-sensitivity of equity valuations, be it in Europe or any other region, is when the global 10-year bond yield is in the 2-3 percent range. What is the global 10-year bond yield? Previously, we defined it in terms of the German bund, U.S. T-bond, and JGB. But we now have an even better definition: it is the simple average of the 10-year yields in the world’s three major economies; the euro area, U.S., and China (Chart I-7).2 Given this yield’s five year struggle to surpass 2.5 percent, we can say that the ‘neutral’ rate, at which tighter financial conditions do not threaten any major economy, might be somewhere below this recent empirical limit, at around 2 percent. The Neutral Rate Is Nominal, Not Real

Chart I-8

Investors always think about the negative asymmetry of returns in nominal terms. This is because the losses they fear tend to be too short and too sharp for the real return to be meaningfully different from the nominal return.3 It follows that the aforementioned hyper-sensitivity of equity valuations is when the nominal bond yield is in the 2-3 percent range, resulting in a neutral nominal rate which might be 2 percent (Chart I-8). But if inflation is also running fairly close to 2 percent, as it is in the major economies, the upshot is that the neutral real rate of interest is zero. What Does All Of This Mean? To sum up, a decade of ultra-loose monetary policy has fostered an addiction to – or at least a dependency on – low bond yields (Chart I-9). But the dependency is not of the rate sensitive sectors in the economy per se, rather it is of the rich valuation of risky assets whose worth dwarfs the global economy by five to one (Chart I-10). Gradually, this dependency should diminish as economic and profit growth improves valuations, but this will take time. Chart I-9A Decade Of Ultra-Loose Monetary Policy...

A Decade Of Ultra-Loose Monetary Policy...

A Decade Of Ultra-Loose Monetary Policy...

Chart I-10...Has Made The Rich Valuation Of Risky Assets Dependent On Low Bond Yields

...Has Made The Rich Valuation Of Risky Assets Dependent On Low Bond Yields

...Has Made The Rich Valuation Of Risky Assets Dependent On Low Bond Yields

In the meantime, the integration of global capital markets means that the valuation cue for European – and all regional – stock markets now comes from the global 10-year bond yield. Given its recent decline to slightly below neutral, stock markets are unlikely to free fall. A decade of ultra-loose monetary policy has fostered an addiction to – or at least a dependency on – low bond yields. That said, the aggregate market is likely to be in a sideways structural pattern, as it has been for the past eighteen months, and the big opportunities will continue to come from sector rotation: in the second half of the year switch out of economically sensitives such as industrials, and into defensives such as healthcare. A final point is that any decline in the global bond yield to below neutral will come disproportionately from higher yielding bond markets. This will underpin the lower yielding major currencies such as the euro. But our first choice for the second half of the year remains the Japanese yen. Fractal Trading System* This week, we see an excellent opportunity to short Russia’s recent strong outperformance versus Japan. The recommended trade is short MOEX versus Nikkei225 with a profit target of 5 percent and symmetrical stop-loss. In other trades, short WTI crude versus LMEX achieved its profit target. Against this, short the French OAT reached its stop-loss. This leaves three open positions. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

Russia (MOEX) VS. Japan (NIKKEI225)

Russia (MOEX) VS. Japan (NIKKEI225)

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Consider what happens to valuations when bond yields decline from 4% to 2%. At a 4% bond yield, equities possess significantly more negative asymmetry than 10-year bonds. So investors will demand a comparatively higher return from equities, let’s say 8% a year. Whereas, at a 2% bond yield, equities and 10-year bonds possess the same negative asymmetry. So investors will demand the same return from equities as they can get from bonds, 2% a year. At the lower bond yield, the bond must deliver 2% a year less for ten years compared to previously, meaning its price must rise by 22%. But equities must deliver 6% a year less for ten years, so the equity market must surge by 80%. 2 We define the global 10-year bond yield as the simple average of the three 10-year bond yields in the euro area, U.S., and China, where the 10-year bond yield in the euro area is the issue-weighted average of the euro area’s individual 10-year bond yields. 3 For example, if bonds had a countertrend correction of 10% in a month when the economy was suffering severe deflation of 10% (per annum), it would still equate to a 9% loss in real terms! Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - ##br##Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch -##br## Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch -##br## Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - ##br##Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights The May official PMI shows that manufacturing in China will slow over the coming year unless the recent doubling of U.S. import tariffs can be reversed and the imposition of the remaining tariffs can be avoided. The divergence between H-shares and both A-shares and the domestic fixed-income market suggests that China’s domestic financial market participants are pricing in some probability of a major reflationary response by Chinese authorities. We agree that such a response will occur over the coming 6-12 months, and would recommend that investors stay overweight Chinese equities within a global equity portfolio over that time horizon. Feature Tables 1 and 2 on pages 2 and 3 highlight key developments in China’s economy and its financial markets over the past month. On the growth front, April’s activity data provided early evidence that the trajectory of the economy was beginning to turn prior to the breakdown in U.S./China trade talks, in response to a meaningful credit improvement in Q1. The May Caixin manufacturing PMI was stable, but the official PMI fell and the experience of last year clearly shows that manufacturing in China will slow over the coming year unless the recent doubling of U.S. import tariffs can be reversed and the imposition of the remaining tariffs can be avoided. Assuming that the Trump administration follows through with its threat, investors are likely to see a repeat of last year’s perversely positive effects of tariff frontrunning on the Chinese trade data over the next few months; this should be viewed as confirmation of an impending collapse in trade activity, rather than a sign that the underlying trade situation is improving. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Within financial markets, the most notable development is the contrast between the relative performance of investable Chinese stocks on the one hand, and domestic equities and the Chinese fixed-income market on the other. The recent performance of investable stocks confirms that they have been driven nearly exclusively by trade war developments for the better part of the past year, whereas the somewhat better relative performance of A-shares and the calm in the government bond, corporate bond, and sovereign CDS markets suggests that China’s domestic financial market participants are pricing in some probability of a major reflationary response by Chinese authorities. We agree that such a response will occur over the coming 6-12 months, and would recommend that investors stay overweight Chinese equities within a global equity portfolio over that time horizon. In reference to Tables 1 and 2, we provide below several detailed observations concerning developments in China’s macro and financial market data: Chart 1A Strong Response From Policymakers Will Likely Offset The Coming Tariff Shock

A Strong Response From Policymakers Will Likely Offset The Coming Tariff Shock

A Strong Response From Policymakers Will Likely Offset The Coming Tariff Shock

Both Bloomberg’s and our alternative calculation of the Li Keqiang index (LKI) rose in April, albeit only fractionally in the case of the latter. Still, as we noted in last week’s report,1 the Q1 rebound in credit appears to have halted the decline in investment-relevant Chinese economic activity (Chart 1). This suggests that the trajectory of the economy was beginning to change in April prior to the breakdown in U.S./China trade talks, implying that an aggressively stimulative response from Chinese authorities to counter a full 25% tariff scenario has good odds of succeeding. This supports our cyclically overweight stance towards Chinese stocks. Our leading indicator for the LKI declined slightly in April, but remains in a very modest uptrend. The gap between accelerating credit growth and the sluggishness of our leading indicator is explained by the fact that growth in Chinese M2 and M3 has been slow to rise. A weaker-than-expected recovery in Chinese economic activity is much more likely if money growth remains weak, but we cannot reasonably envision an outcome where credit growth continues to trend higher and growth in the money supply does not meaningfully accelerate. The incoming Chinese housing data continues to provide conflicting signals. The annual change of the PBOC’s pledged supplementary lending injections declined further in April, which since 2015 has done an excellent job explaining weak housing demand. However, both floor space started and sold picked up in April (Chart 2), and house price growth remained steady despite a significant decline in the breadth of house price appreciation across 70 cities. Policymakers are likely to allow aggregate credit growth to accelerate significantly over the coming 6-12 months in order to counter the deflationary impact of a trade war with the U.S., but our sense is that policymakers will then refocus their financial stability efforts on the household sector (i.e. they will work to prevent another significant reacceleration in household debt growth). Given this, we continue to expect that housing demand will remain weak, although we will be closely watching floor space sold over the coming few months. The new export orders component of the official manufacturing PMI is signaling an external outlook that is as negative as the 2015/2016 episode. The May official manufacturing PMI fell back into contractionary territory, led by a very significant decline in the new export orders component (Chart 3). The Caixin manufacturing PMI was stable, but the outlook for manufacturing in China is clearly negative unless the recent doubling of U.S. import tariffs can be reversed and the imposition of the remaining tariffs can be avoided. Investors are likely to see a repeat of last year’s perversely positive effects of tariff frontrunning on the Chinese trade data over the next few months; this should be viewed as confirmation of an impending collapse in trade activity, rather than a sign that the underlying trade situation is improving. Chart 2Surprising Resilience In China's Housing Market (For Now)

Surprising Resilience In China's Housing Market (For Now)

Surprising Resilience In China's Housing Market (For Now)

Chart 3A Clearly Negative Outlook For Manufacturing

A Clearly Negative Outlook For Manufacturing

A Clearly Negative Outlook For Manufacturing