Government

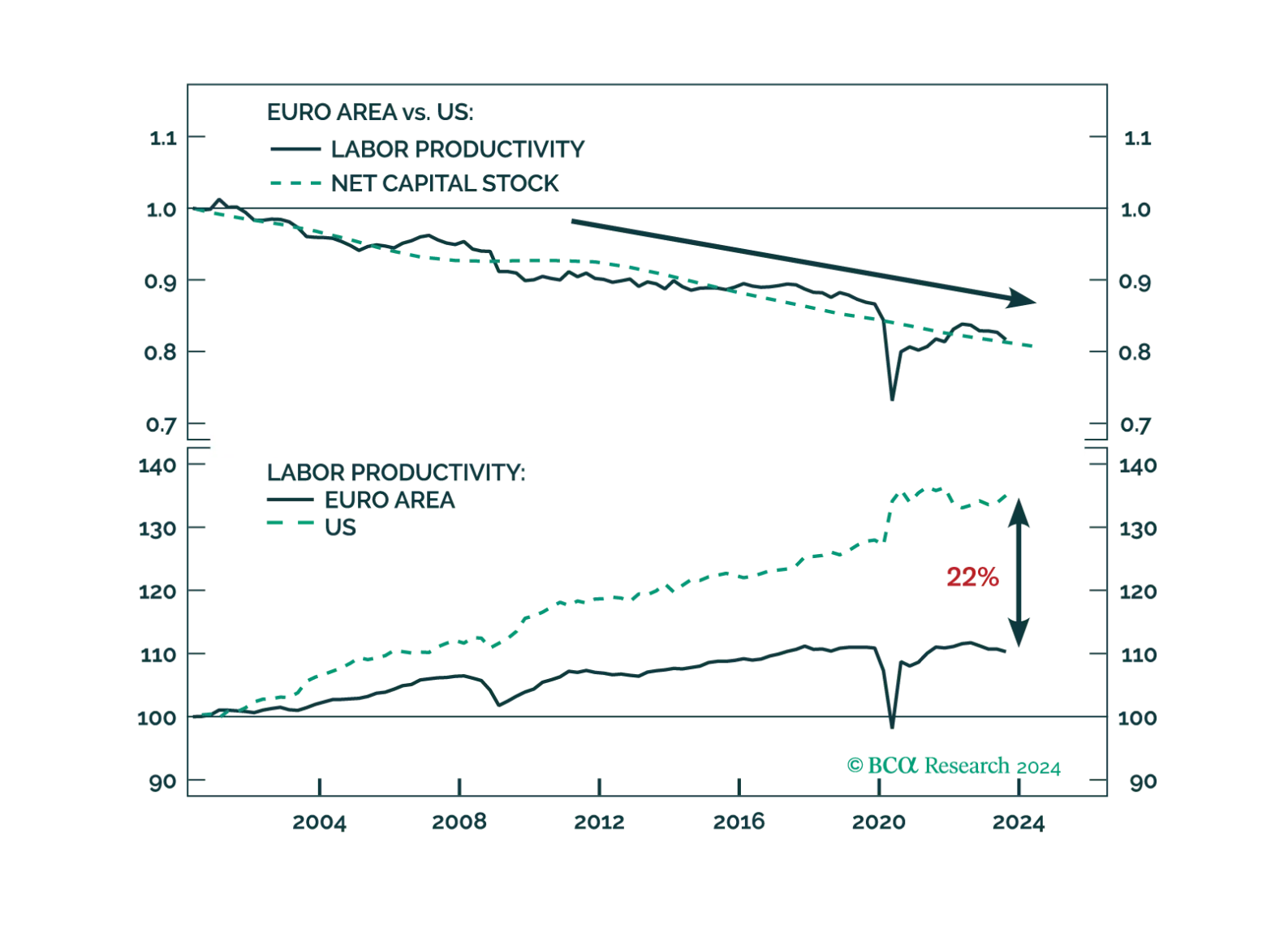

The Draghi report highlights sensible reforms that would address many of Europe’s productivity shortcomings. Whether European capitals heed Mario Draghi’s advices remains to be seen.

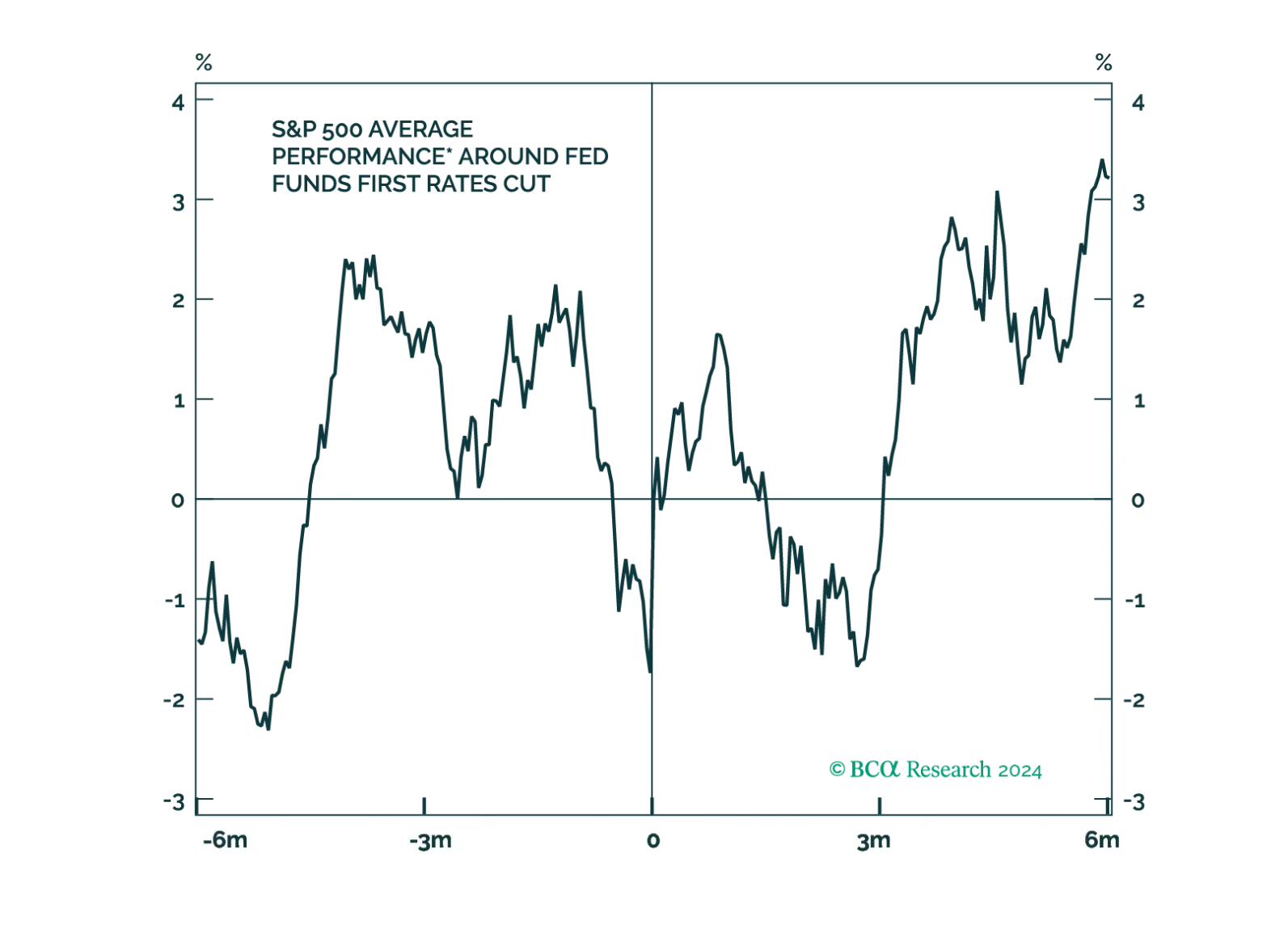

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

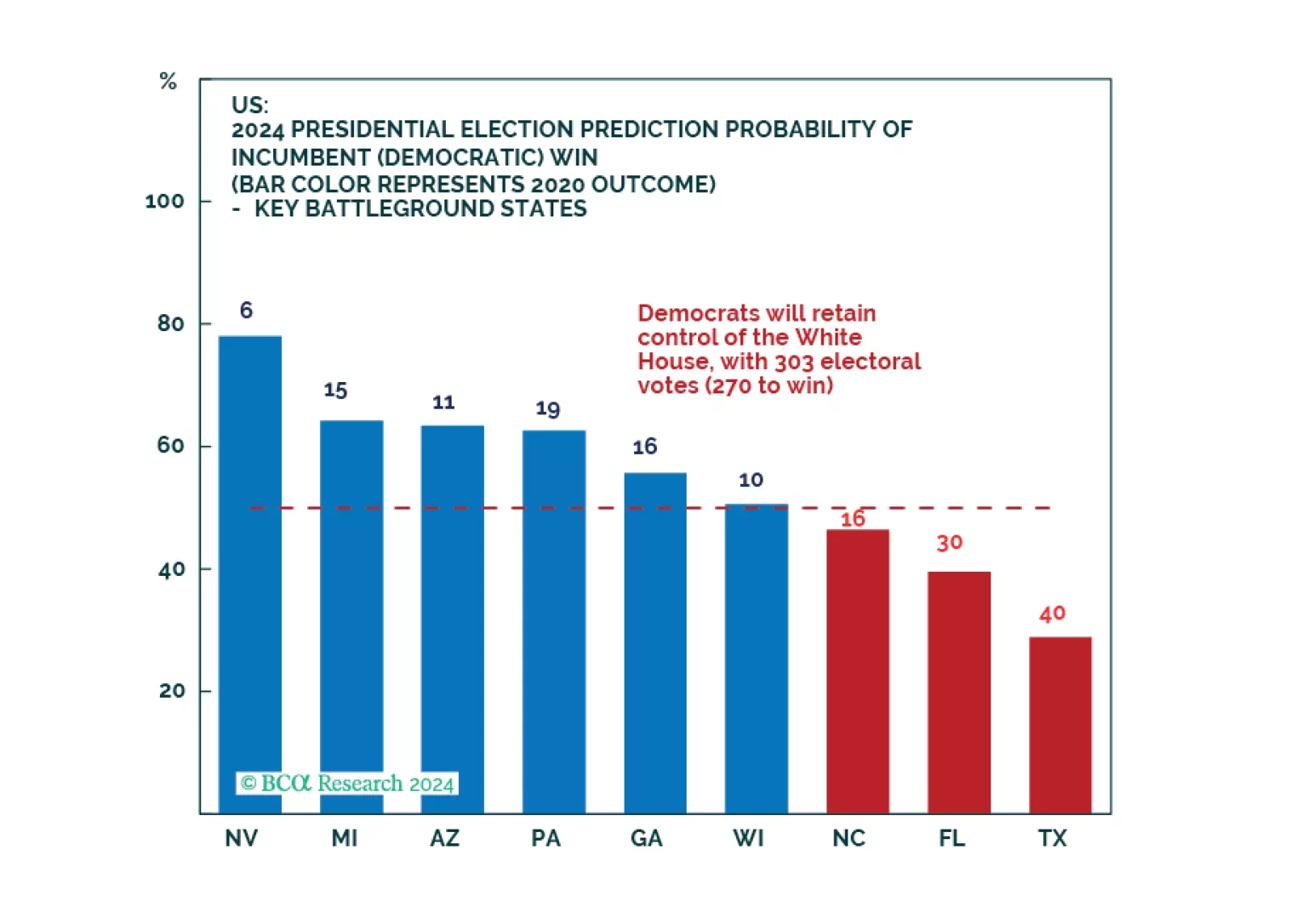

Democrats will not win a full sweep and implement drastic new tax hikes. However, our quant model still favors them to win the White House and just upgraded their odds. While we expect equity volatility around the election, investors do not need to worry about corporate tax hikes.

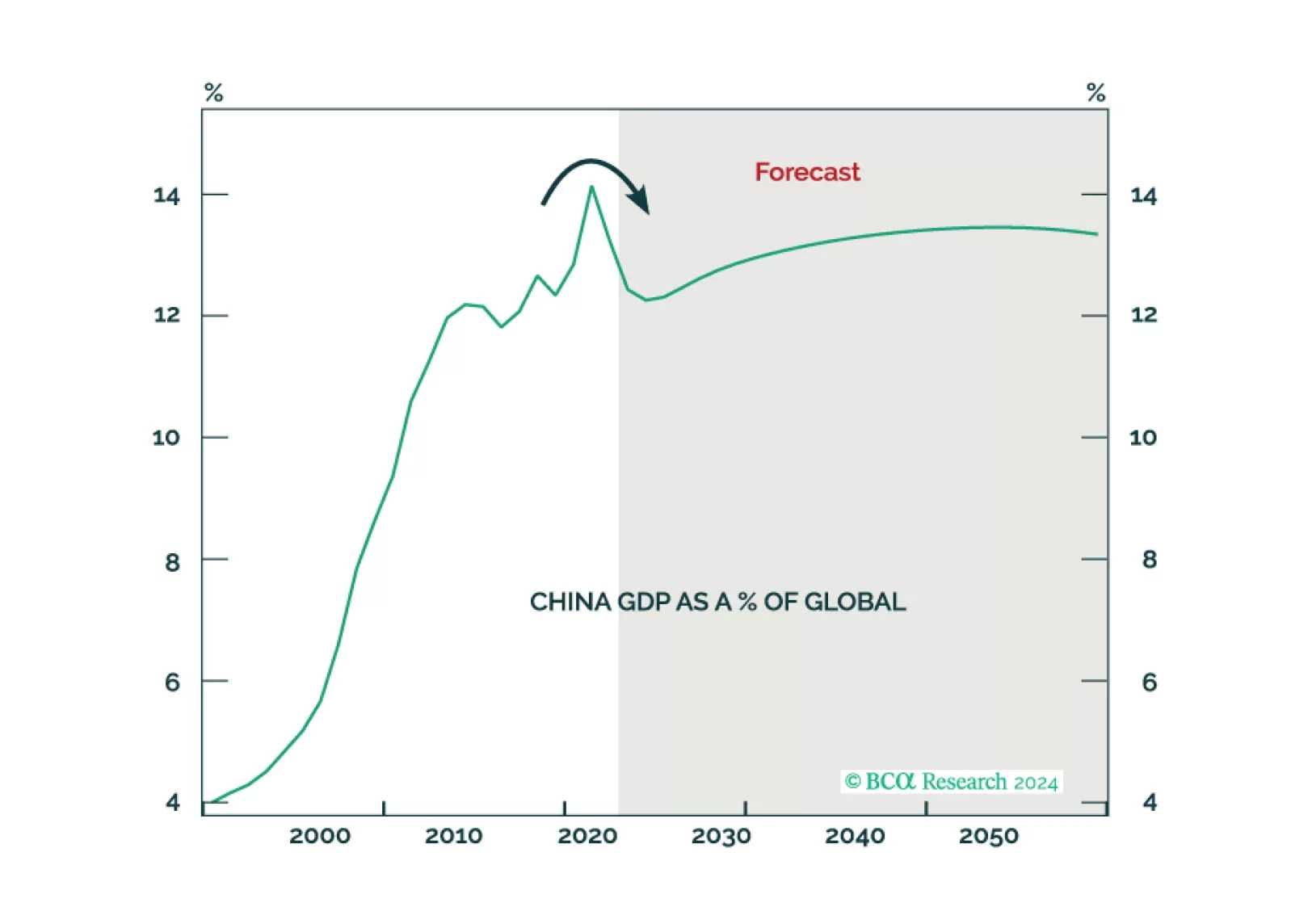

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

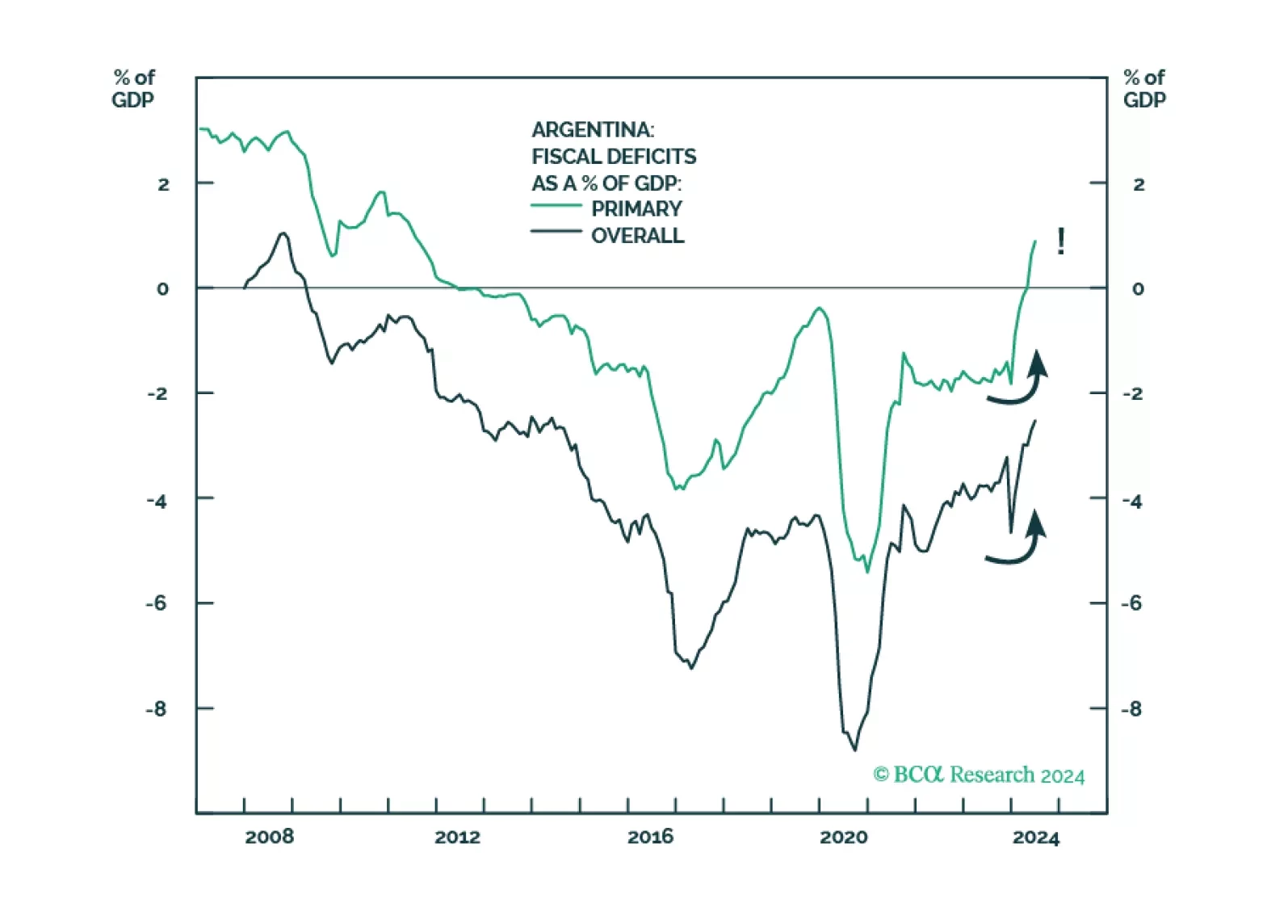

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

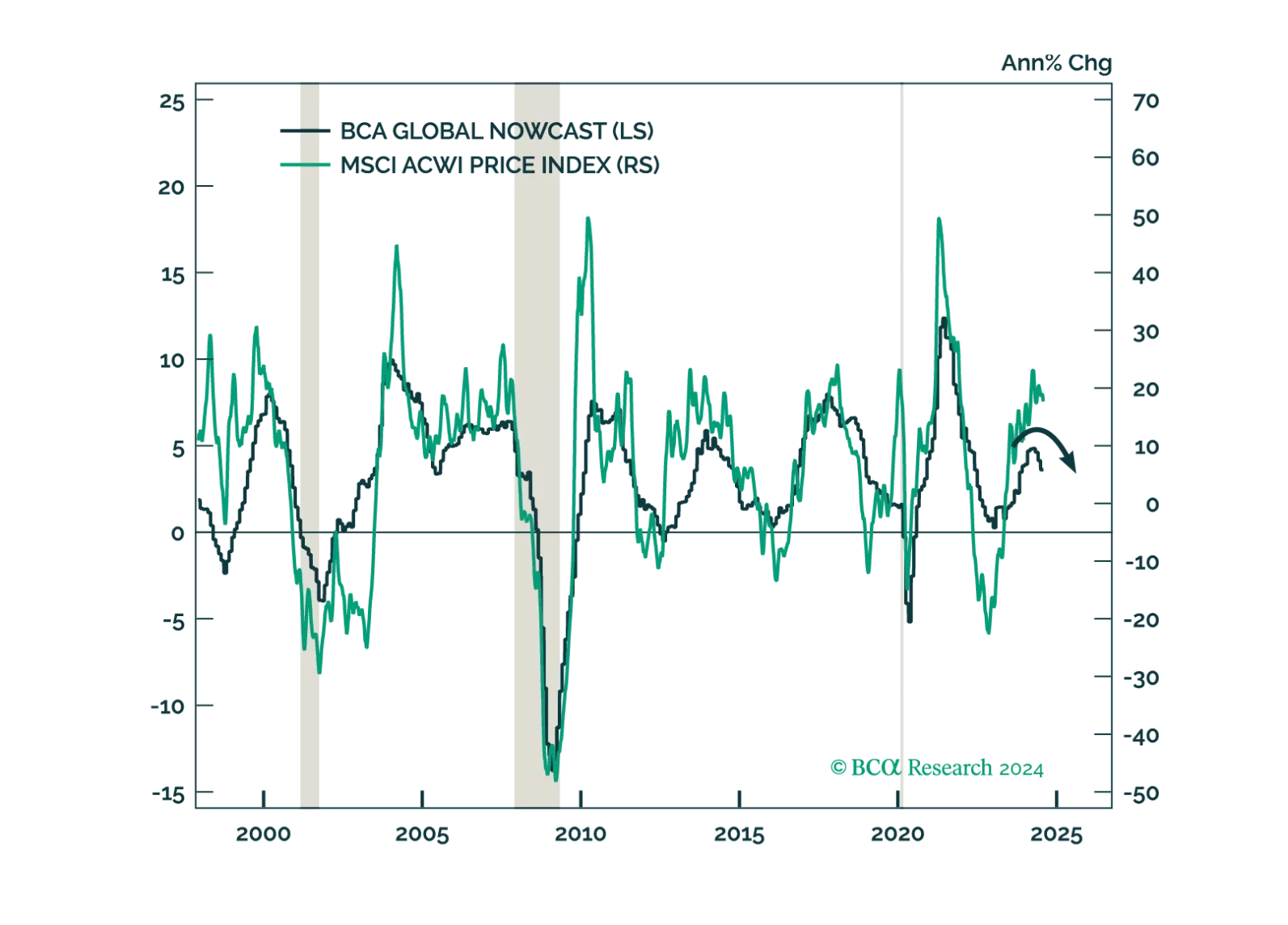

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.