Government

China’s credit data update for January delivered a mixed signal on Friday. The CNY 6.50 trillion increase in aggregate financing beat expectations of CNY 5.60 trillion and marked a significant acceleration from CNY 1.94 trillion in December. Similarly, the…

Thursday’s Chinese CPI and PPI release for January indicates that deflationary pressures continue to dominate the domestic economy. On the consumer side, prices registering the fastest pace of annual decline in 15 years. The CPI’s 0.8% y/y decrease is more…

Chinese domestic stocks have fared quite poorly over the past year. Since late-January 2023, the Shanghai Shenzhen 300 index fell roughly 24% to last week’s low, driven by ongoing weakness in China’s economy and a steady and ongoing collapse in investor…

According to BCA Research’s Commodity & Energy Strategy service, the US Department of Defense’s (DoD) first-ever industrial policy – dubbed the National Defense Industrial Strategy (NDIS) – is attempting to reverse post-Cold War decline in the DoD’s…

China’s industrial profits registered their second consecutive annual contraction last year, falling by 2.3% in 2023. The full year contraction comes despite a surge in industrial profits near year-end. Profit growth came in at 16.8% y/y in December…

According to BCA Research’s China Investment Strategy service, the current Pledged Supplementary Lending (PSL) program will provide much less support to the housing market and construction activity than the 2015-2018 program. China’s central bank…

The Central Bank of Brazil (BCB) has cut the Selic rate by 50 basis points in each of the past four meetings and has alluded to maintaining this size of cuts for the coming meetings. Governor Roberto Campos Neto stated last month that he aims to bring…

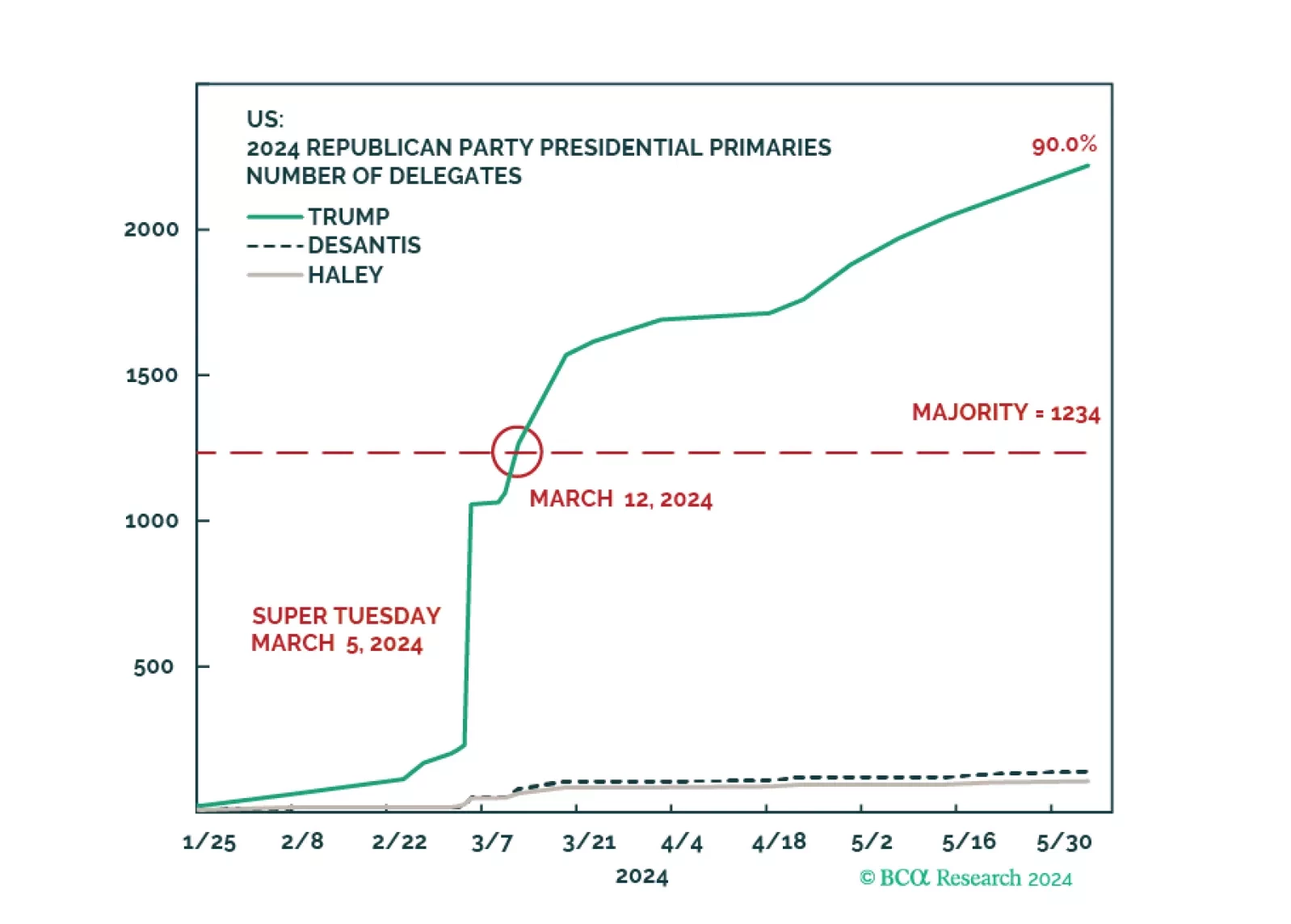

The market will eventually be forced to react to rising odds of a sharp US national policy reversal. Investors should overweight government bonds and defensive equity sectors.

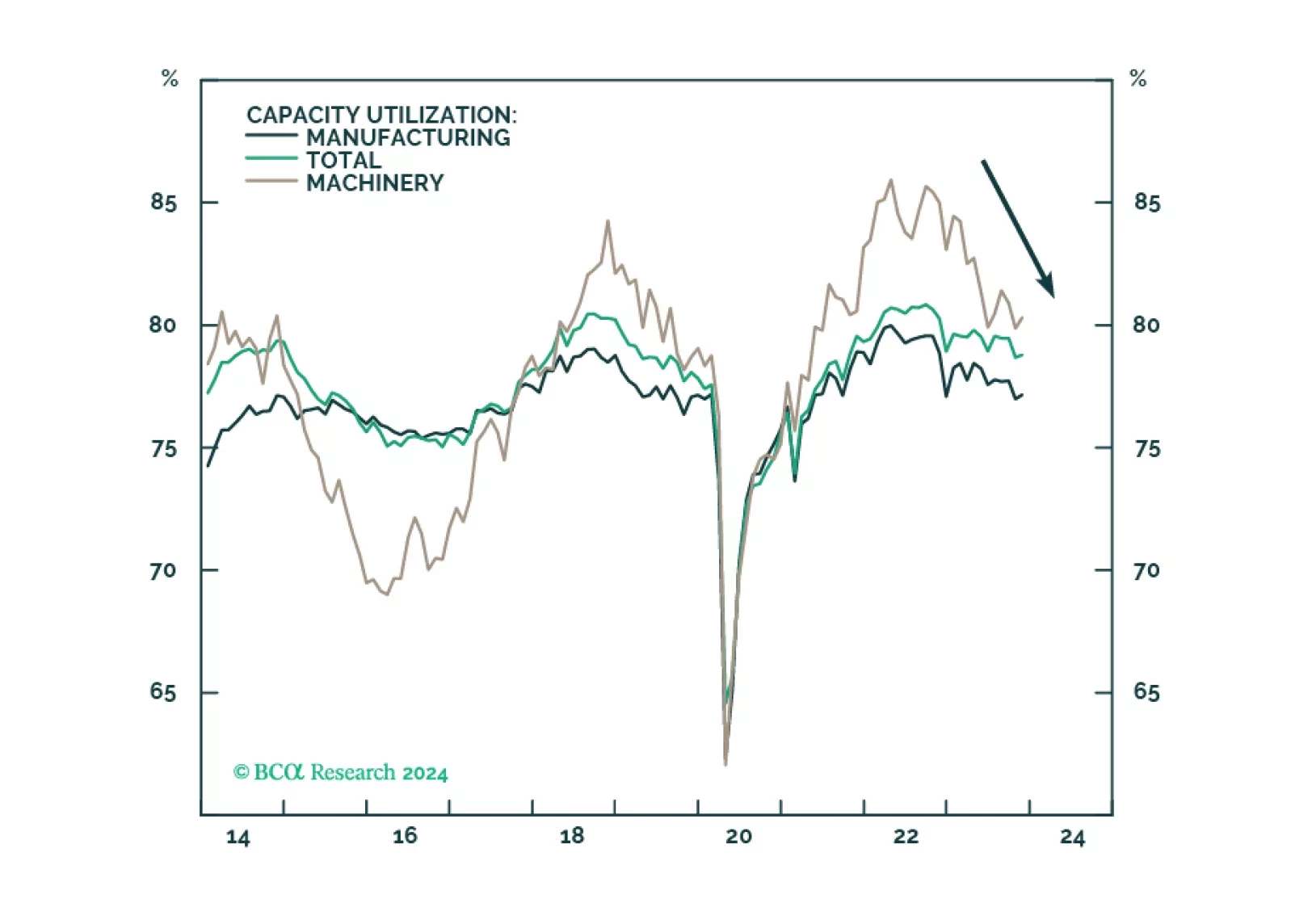

The US manufacturing renaissance, spurred on by reshoring, automation, and government spending, is running its course but progress has slowed on the back of tight monetary conditions and the manufacturing recession. The deceleration of these positive trends weighs on the outlook for the Capital Goods industry group, impeding its performance over the short term. However, we reiterate that positive long-term trends for the industry remain intact. We downgrade Capital Goods to a tactical underweight. It remains a strategic overweight.

China’s central bank unexpectedly held the medium-term policy rate unchanged at 2.5% on Monday, surprising expectations of a 10 basis point cut. Given that deflationary forces dominate China’s economy, the decision to stand pat underscores that policymakers…