Hot Topic

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

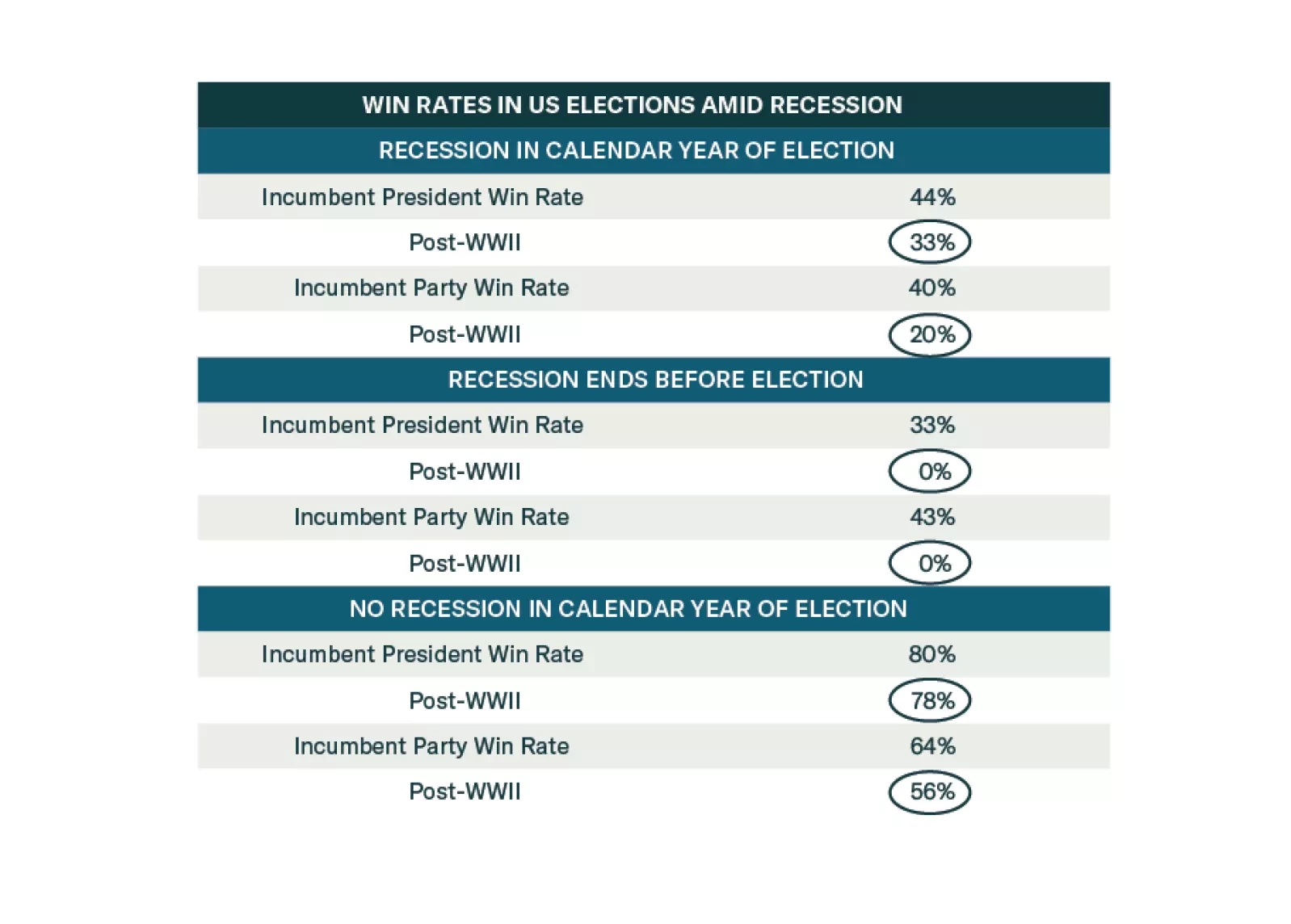

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

A series of notable events took place over the Thanksgiving holiday but none of them force us to change our fundamental assessments. The conflict in the Middle East is likely to escalate rather than de-escalate, while the Taiwan Strait has at least a 50/50 chance of seeing tensions escalate next year.

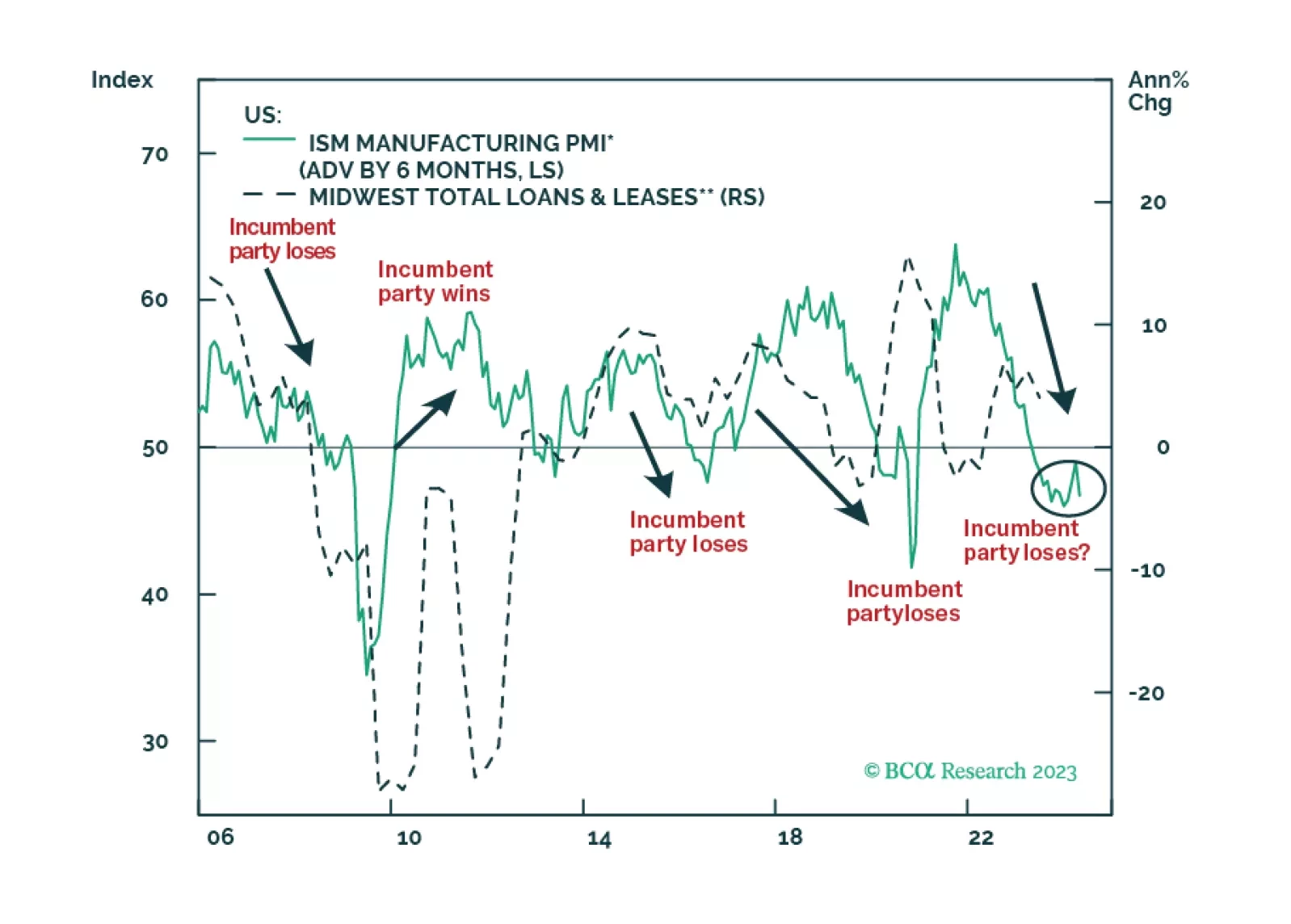

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

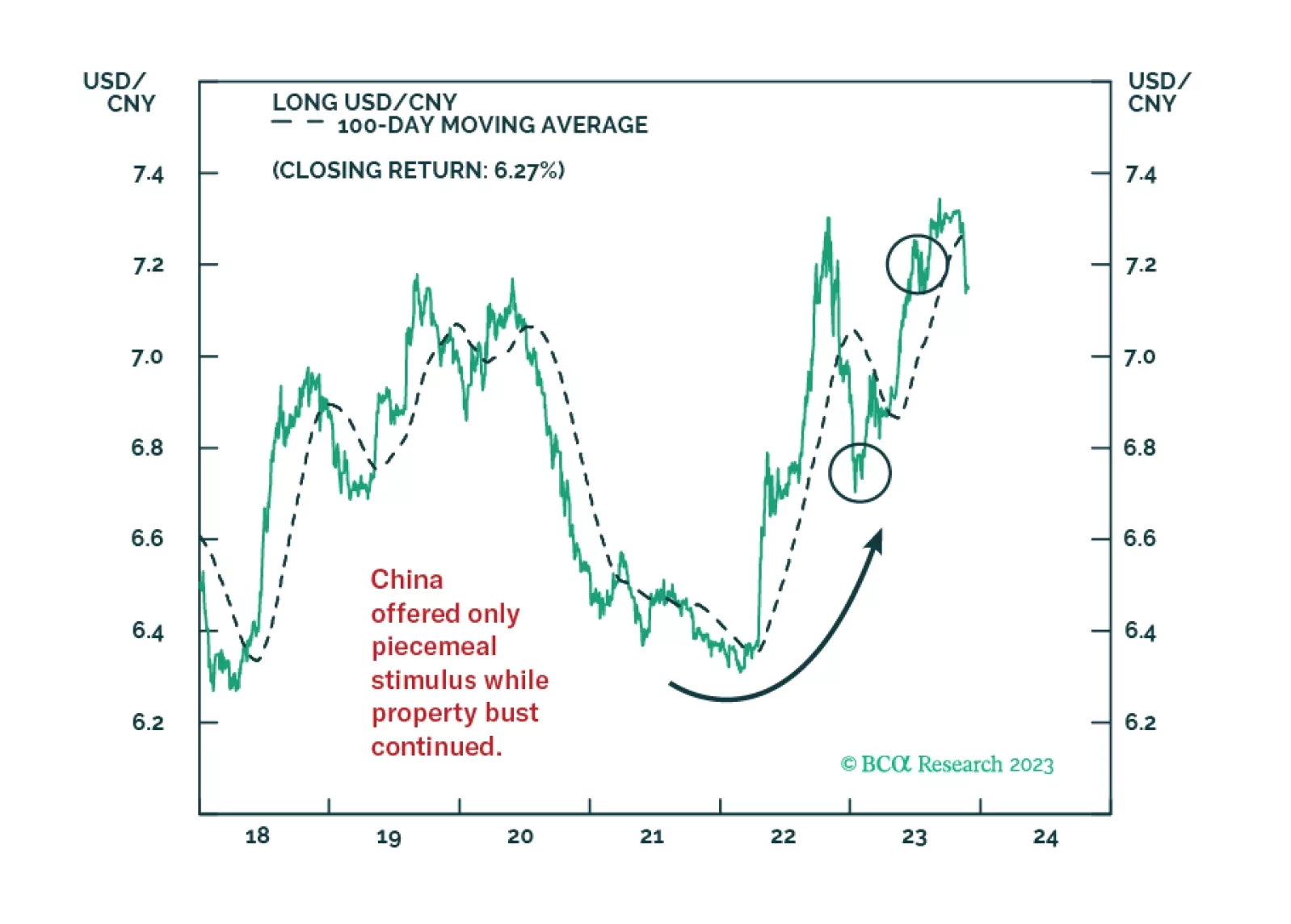

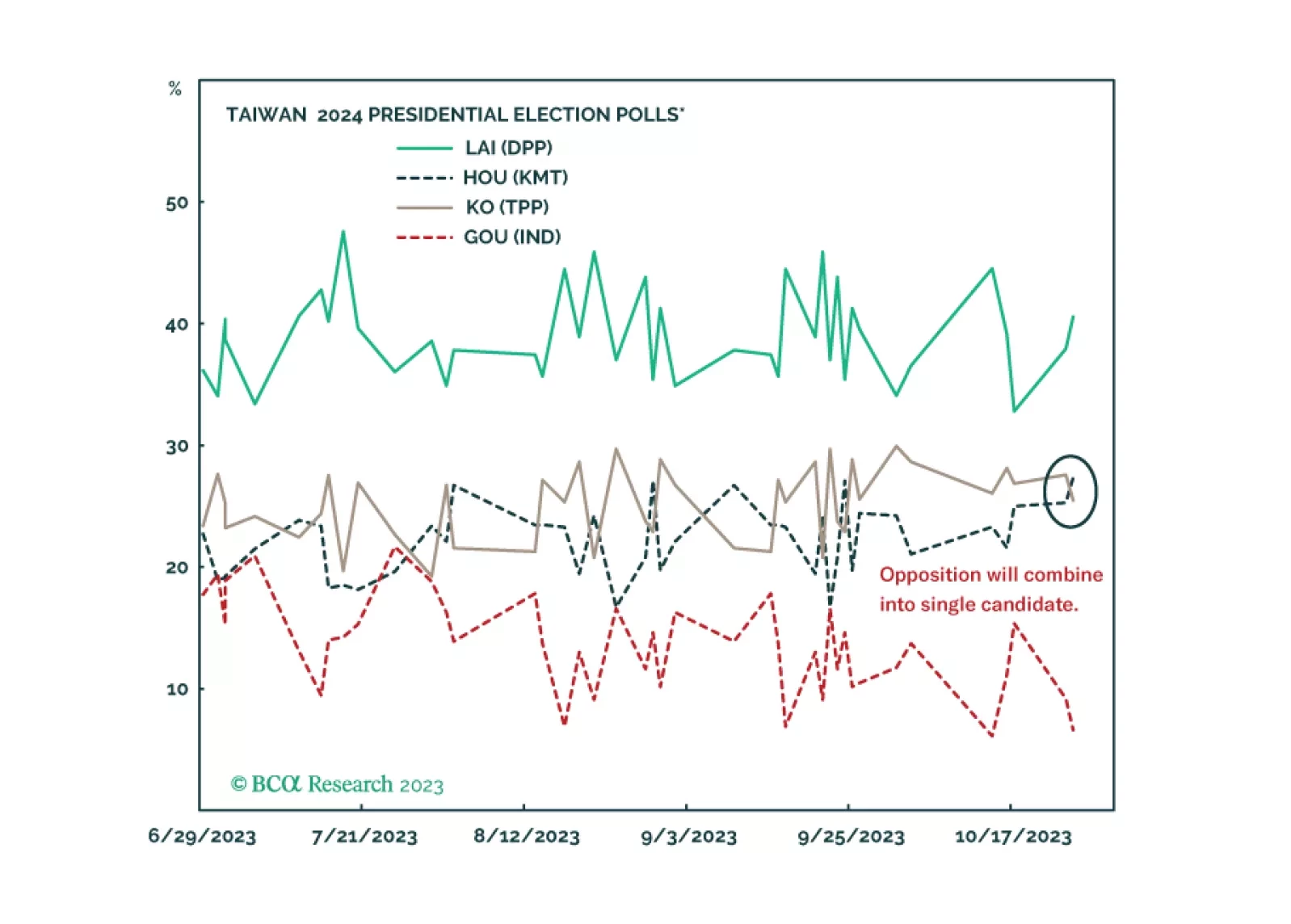

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

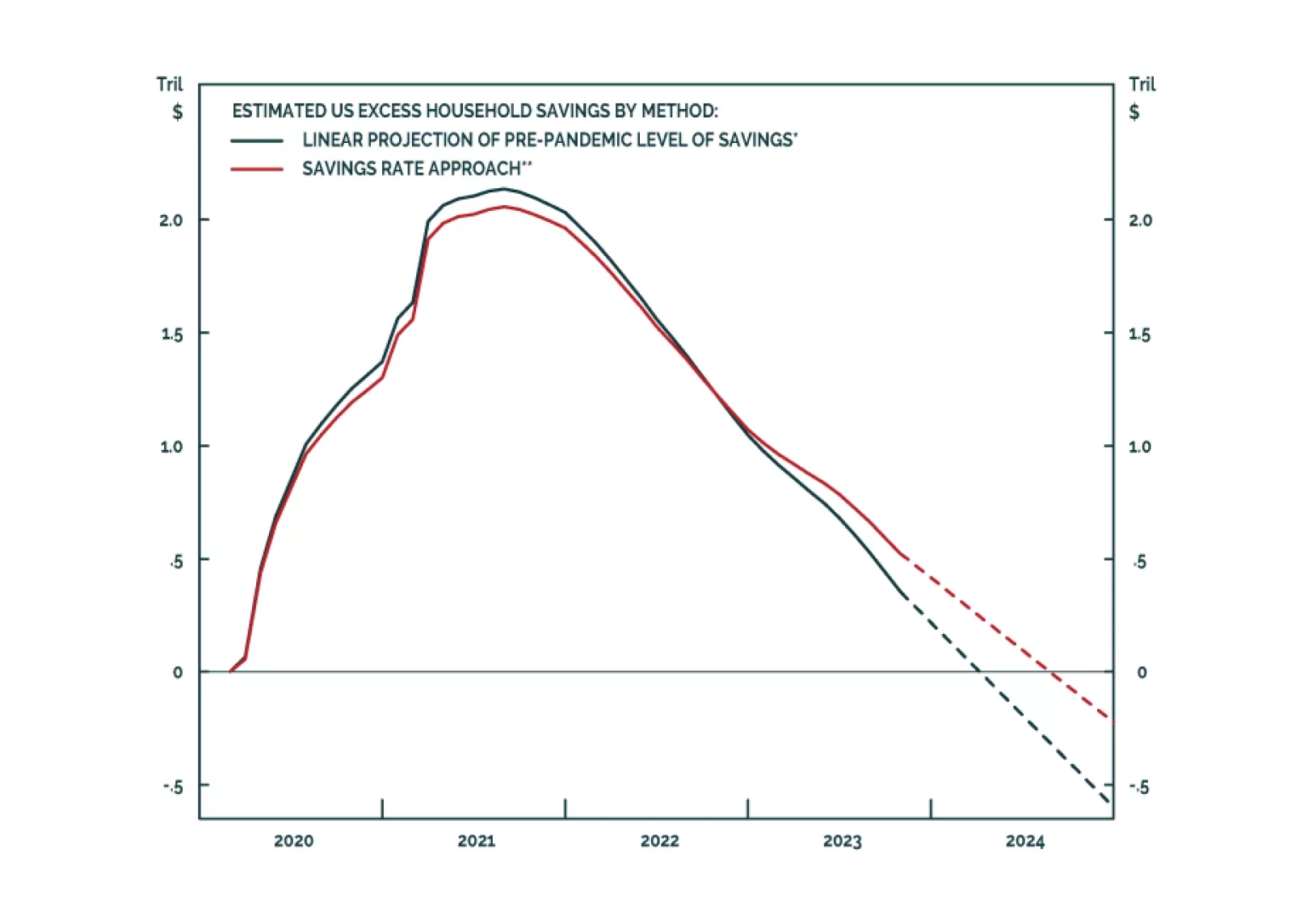

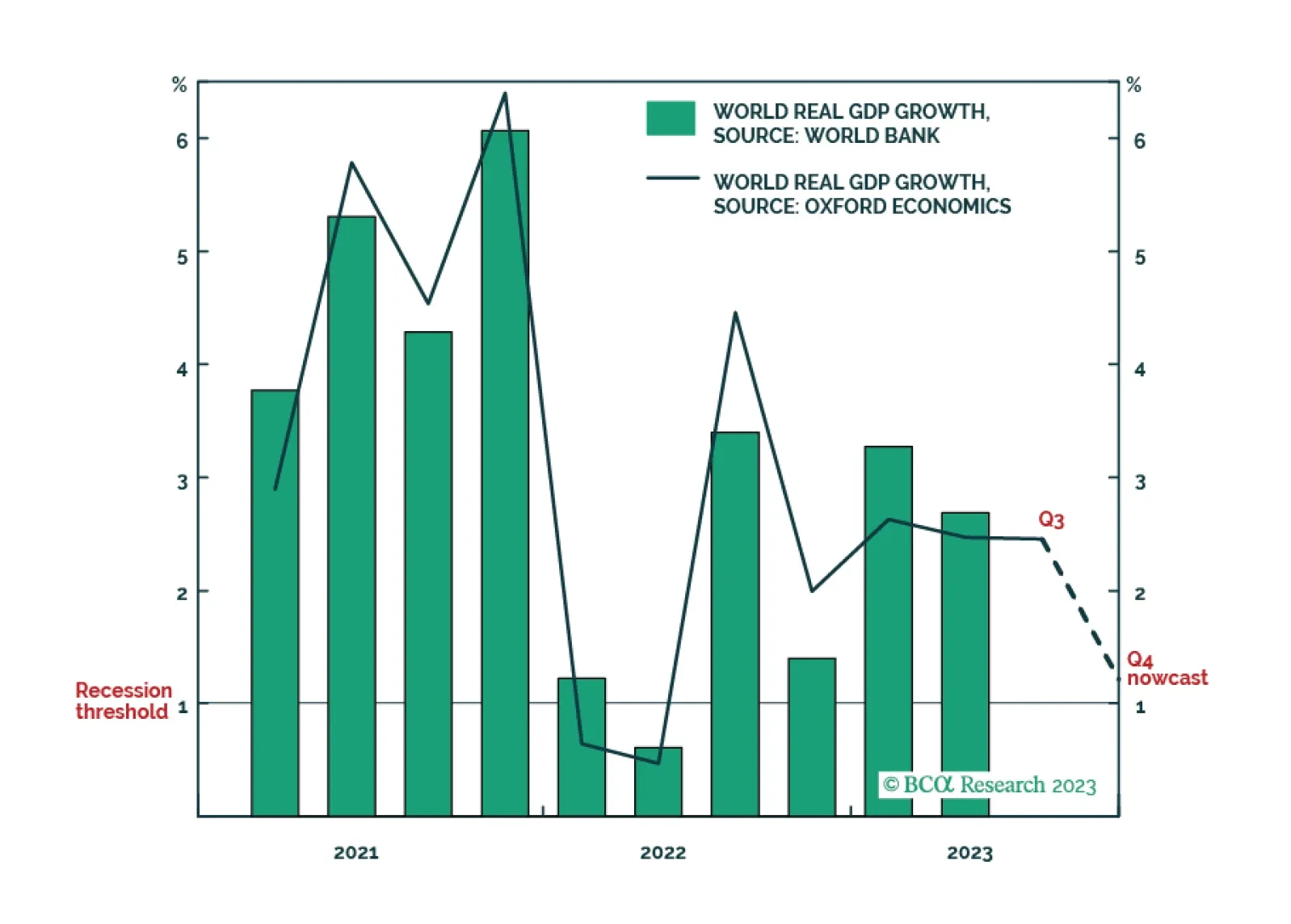

The latest ‘nowcast’ for world economic growth in the fourth quarter has plunged to just 1.2 percent, marking the cusp of another world recession. One important implication is that expectations for oil demand growth and industrial metal demand growth are way too optimistic.