Household Products

This is the time of the year when strategists are busy sending out their annual outlooks. Here on the Global Investment Strategy team, we decided to go one step further. Rather than pontificating about what could happen in 2025, we decided to harness the power of the multiverse to tell you what did happen (in at least one highly representative timeline).

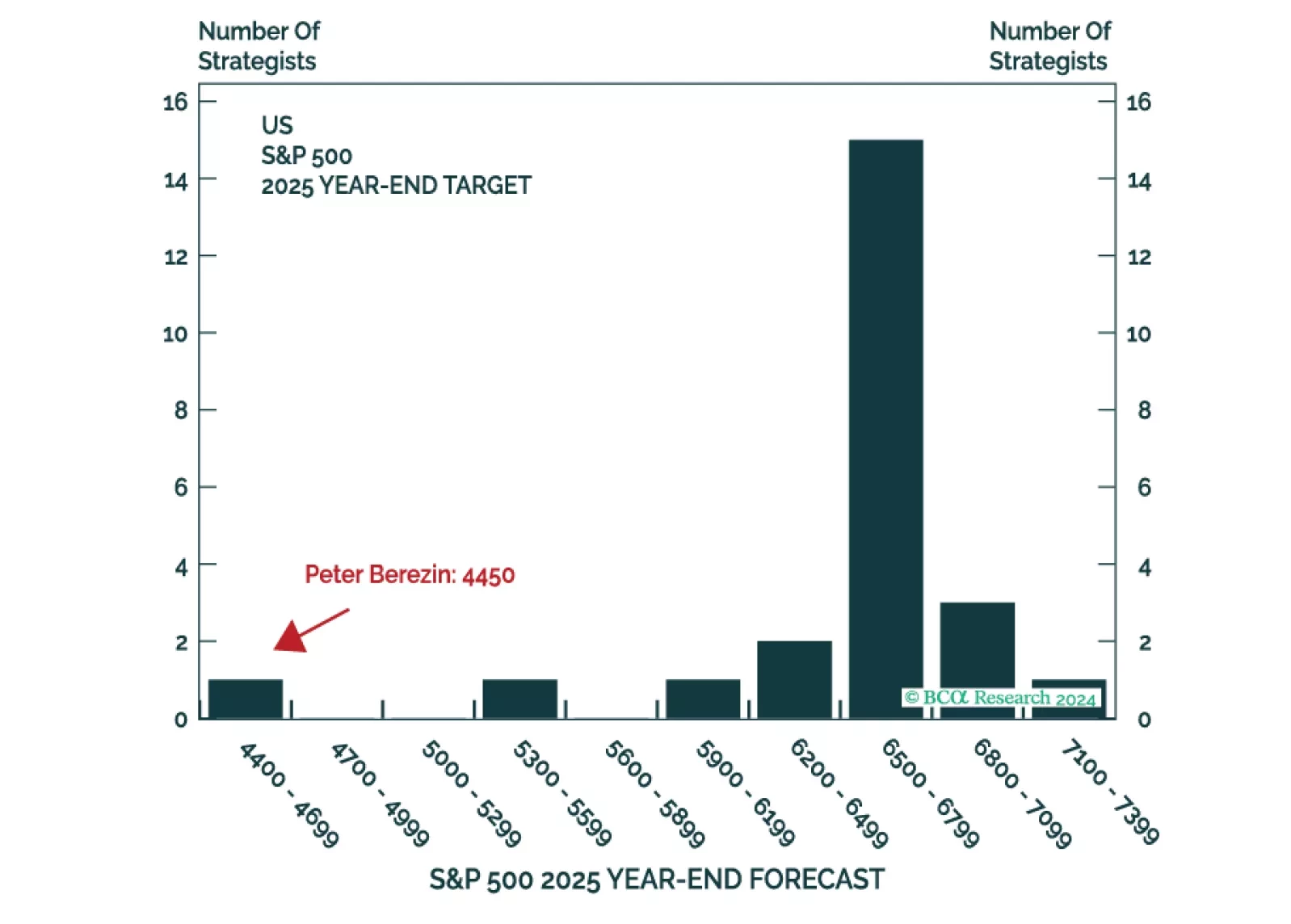

Next week, please join me for a Webcast on Tuesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets.

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2025. We will be back in the first week of January with our MacroQuant Model Update.

Stocks are a forward discounting mechanism and routinely top before recessions begin, even if they typically do not swoon until the recession has taken hold. According to BCA Research’s US Investment Strategy service, if consumers were losing momentum and a…

Neutral We remain neutral the S&P household products index. A V-shaped economic recovery following a recession has historically been synonymous with this defensive industry underperforming (top panel). However, the uniqueness of the current recession must be taken into account. The US consumer continues to binge on household products, which are currently outpacing overall retail sales growth by 13% year-over-year (middle panel, relative consumer spending shown truncated). This trend is slated to continue until a vaccine arrives as the second wave of infections emerges. The same story holds for foreign consumers who also have an incentive to keep up their spending on US household products: a softer US dollar. A weaker US dollar will boost competitiveness of US exporters, which will translate into robust top line growth (bottom panel). Bottom Line: Given the strangeness of the current recession, we remain neutral the S&P household products index. The ticker symbols for the stocks in this index are: BLBG: S5HOPR – PG, CL, KMB, CLX, CHD.

Frenetic trading continued unabated in the US equity markets with some bizarre moves now a daily phenomenon. One such occurrence is the positive correlation of the VIX with the SPX, which we had flagged as a negative omen in mid-February.1 Thus, risk management portfolio metrics are of the utmost importance when trading goes haywire. Following up from closing all our high-conviction trades last Friday, we are obeying all recently instituted rolling stops in our cyclical portfolio positions in order to protect profits. Our underweight position in homebuilders, and overweight positions in hypermarkets and household products have been all stopped out this week for a profit of 41%, 26% and 5%, respectively. As such, all three positions have reverted back to neutral. Bottom Line: Erratic trading patterns and heightened volatility compel us to obey our rolling stops. Book gains and move to neutral in the cyclically underweight S&P homebuilders, overweight in S&P hypermarkets and overweight in S&P household products positions for a profit of 41%, 26% and 5%, respectively. Stay tuned. Footnotes 1 Please see BCA Research US Equity Strategy Weekly Report, “Will The Fed Save The Day, Again?”, dated February 18, 2020, available at uses.bcareseach.com.

Highlights Portfolio Strategy We have identified 20 reasons to start buying equities. We highlight positive catalysts that should underpin the equity market as the pandemic progresses. Investors with higher risk tolerance should continue to layer in slowly and put cash to work with a cyclical 9-12 month time horizon. Consumer staples in general and hypermarkets and household products in particular are defensive areas where we are comfortable to deploy fresh longer-term oriented capital. Recent Changes Erratic trading compelled us to close out all our high-conviction calls for the year last Friday, booking handsome gains for our portfolio.1 Table 1 Feature Equities oscillated violently last week and remain mostly rudderless (Chart 1). While the relentless COVID-19 news bombardment kept on feeding the bears, on the flip side monumental monetary easing and fiscal packages the world over emboldened the bulls. This tug of war is far from over, but it is becoming crystal clear that both monetary and fiscal authorities will throw the proverbial kitchen sink at it until the hemorrhaging stops. Last week we showed that it takes a median two full years for the SPX to make fresh all-time highs following a bear market.2 This week we highlight the median and mean profile of the bear market recoveries since WWII (Chart 2). Crudely put, if history at least rhymes the SPX will not make any fresh all-time highs until early 2022. Chart 1Rudderless Chart 2Profile Of A Bear As a reminder, our equity market roadmap for the next few months is a drawn out consolidation phase leaving investors ample time to shift portfolios and put cash to work. This bottoming roadmap is something akin to the 1987, 2011, 2015/16 or early-2018 episodes.3 We cannot rule out further downside to equities. Moreover, we can neither time the tops nor the bottoms. However, the same way we were cautioning investors not to chase this market higher – as we were not willing to risk 100-200 points of SPX upside for a potential 1000 point drawdown – we are now compelled to nibble on the way down. Turning over to volatility, the VIX hit 85.47 intraday last week and clocked its highest close since the history of the data. Its sibling the VXO (volatility on the OEX or S&P 100) that predated the VIX hit an intraday high of 172.79 on Tuesday, following Black Monday, October 20, 1987, and clearly warns that if another crash takes root the VIX will explode higher.4 Importantly, vol at 85 translates into a 25% move in the SPX, in either direction, in the next 30 days. Chart 3 shows that actual SPX realized volatility jumped to 103 last week, trumping the VIX’s spike. Historically, when realized volatility trumps the VIX, it is time to sell the VIX; the opposite is also true. Given that we still do not expect a repeat of the GFC, or a depression, we recommend investors with higher risk tolerance start to deploy long-term oriented capital in the equity market. Chart 3Realized Versus Implied Vol Below are 20 reasons to start buying equities. We highlight positive catalysts that should underpin the equity market as the pandemic progresses. We are already in recession. Markets trough in recessions and historically offer enticing risk/reward return profiles. China’s manufacturing PMI and other hard data fell below the GFC lows. As a general rule of thumb investors should buy stocks when the global PMI is well below 50 (Chart 4). Cupboards are bare. A drawdown in inventories is usually followed by a jump in production. That is one of the reasons to be bullish staples. As for durables, pent-up demand due to delayed purchases will eventually be violently unleashed, especially given zero rates. Consumers will benefit from the oil market carnage and the super low mortgage refinancing rates. The Fed cut rates to zero, did QE5, and brought back the alphabet soup of programs like CPFF, PDCF and MMLF from the GFC, more will likely follow (Chart 5). Chart 4Time To Buy Chart 5The Fed Put The DXY has gone from 95 on March 9 to 103 on Friday. King dollar will soon have to reverse course and provide some much-needed relief globally as the Fed’s US dollar swap lines aim to alleviate the shortage of US dollars (Chart 6). Keep in mind what Dr. Bernanke told Scott Pelley in a 60 Minutes interview with regard to money creation: “PELLEY: Is that tax money that the Fed is spending? BERNANKE: It's not tax money. The banks have accounts with the Fed, much the same way that you have an account in a commercial bank. So, to lend to a bank, we simply use the computer to mark up the size of the account that they have with the Fed (emphasis ours). So it's much more akin to printing money than it is to borrowing.”5 Other global Central Banks are cutting rates and doing QE. Beyond Christine Lagarde’s recent €750bn bazooka, the ECB has the OMT ready from previous crises. Already last week the ECB intervened in Italian BTPs via Banca d’Italia. Germany has hinted that it would not be opposed to a “Covid-bond” A mega US fiscal package looms near the $1tn mark.6 The recession-related automatic stabilizers and government spending will soar. China’s fiscal response will likely be as large as in late 2008 (as a reminder in Q4/2008 the Chinese fiscal spending announcement equated “to 12.5% of China’s GDP in 2008, to be spent over 27 months”7). Germany and a slew of other countries have already pledged fiscal spending. Spain has announced a 20% of GDP package. Countries will bid-up the size of the bailout. IMF announced a $1tn bailout package. Nibbling at stocks when the VIX is at 85 makes sense versus when the VIX is at 12 (Chart 7). Chart 6Greenback Falls And Rates Rise When The Fed Does QE Chart 7Compelling Entry Point The yield curve slope is steepening (Chart 8). Chart 8The Yield Curve Always Leads Stocks The 10-year real Treasury yield hit a low of -50bps that indicator has also priced in recession (Chart 7). Chart 9Recession Nearly Fully Priced In Equity market internals have fully priced recession, small caps and weak balance sheet stocks in particular (Chart 9). Sentiment is washed out as per our Capitulation, Sentiment and Complacency-Anxiety Indicators (Chart 9). Bernie Sanders has lost his bid to become the nominee of the Democratic Party. Buffett will either bailout a company or two or buyout a company he likes. Jamie Dimon and/or other prominent CEOs (insiders) will start buying their own company stock. Social-distancing measures in the West will ultimately break the Epidemic Curve first derivative and arrest the panic. Even if COVID-19 comes back in force, the fact is that most of the patients who succumb to it are elderly. In Italy, the average age of death is 80 years old. As such, the final circuit-breaker ahead of a GFC would be desensitization by the population, as selective quarantines – targeting the elderly cohorts – get implemented in order to allow other people to return to work. Furthermore, two “silver bullet” solutions remain as tail risks to the bearish narrative. First, a biotech or pharmaceutical company may make a breakthrough in the fight against COVID-19. Not necessarily a vaccine, but a treatment. Finally, upcoming warm weather in the northern hemisphere may also help the fight against the virus. Nevertheless, there are some risks we are closely monitoring. First, if we are offside and this turns into a GFC, another big down-leg will ensue. One reason for this would be a Spanish Flu parallel where the second wave of deaths trounced the first wave. In that case, the GDP contraction will be longer-lived and SPX EPS will suffer a long-lasting setback. Second, a credit crunch can cause a credit event, which is a big risk as we have been highlighting recently. Counter party as well as bank insolvency risks will also come into play. Third, non-financial non tech corporate net debt-to-EBITDA is at all-time highs according to company reported data and non-financial corporate debt as a percent of GDP is at all-time highs according to national accounts (Chart 10). Finally, while lower rates are helpful in the long run, a long era of low rates in Japan and more recently the euro area have not helped equities in the longer-term. The NIKKEI 225 is still down 58% from the December 1989 all-time highs and the MSCI Eurozone index is down 46% from the March 2000 all-time highs (Chart 11). Chart 10Risk: Too Much Indebtedness Chart 11Japan And The Euro Area Are Scary ZIRP Parallels Netting it all out, following a nine-month cyclical period of being in the bearish camp, we are now selectively nibbling on stocks with a 9-12 month time horizon, as we deem the potential positive catalysts will overwhelm the few risks that we are closely monitoring. This week we reiterate our overweight stance in the second largest defensive sector – the S&P consumer staples index – and two of its key sub-components. Continue To Favor Defensive Staples… Consumer staples stocks have caught on fire lately as investors have been seeking refuge in defensive equities during the current “risk off” phase. Behind health care (15.6% of the SPX weight), their safe haven siblings, staples are the second largest defensive sector comprising 8.5% of the S&P 500, and we reiterate our overweight stance in this sector. Historically, staples equities thrive in recessions and in deflationary/disinflationary environments. The reason is the allure of their stable cash flows especially in times of duress when growth is really hard to come by, a staples company growing revenues 5%/annum is sought after aggressively. Currently, relative share prices have troughed near the GFC bottom, and are probing to break out of the one standard deviation below the historical time trend mean (Chart 12), offering a compelling entry point to deploy new capital. Chart 12Bouncing Last week’s jump in unemployment insurance claims to 281,000 is a small precursor of things to come as more parts of the US get locked down (middle panel, Chart 13). This recessionary backdrop, coupled with the surging VIX, which will take months to die down to 20 near the historical average, and investors hiding in Treasurys all argue that it pays to stay with defensive staples stocks (top & bottom panels, Chart 13). Two of our preferred vehicles to continue to explore an overweight in the consumer staples sector are via above benchmark allocation in both hypermarkets and household products stocks. Chart 13Sticks With Staples …Stick With Hypermarkets… Last summer, following our recession thought experiment report8 we upgraded the S&P hypermarkets index to overweight preparing our portfolio for the inevitable recession.9 Since then, hypermarket stocks have bested the SPX by over 36%. While a consolidation phase looms that will allow hypermarkets to build a base before vaulting higher, today we are instituting a rolling 10% stop from the highs in order to protect handsome gains for our portfolio. The savings rate more than trebled from the GFC lows as the once in a generation Great Recession scared consumers. The savings rate has remained elevated ever since and is primed to rise further in the current recession as consumers tighten their purse strings. Historically, relative share prices and the savings rate have been positively correlated as even wealthier consumers opt for rock bottom selling price points. The current message is to expect a durable bidding up phase of hypermarket equities (Chart 14). Chart 14When The Going Gets Tough, Buy Hypermarkets The soaring greenback is underpinning these pricing strategies from Big Box retailers as it keeps import prices in deflation, allowing retailers to pass these on to the consumer (fourth & bottom panels, Chart 15). The recent drubbing in oil prices is an added catalyst to boost hypermarket equities as lower prices at the pump will translate into more cash in consumers’ wallets (top panel, Chart 15). Keep in mind that WMT is the number one grocery store in the US with near 25% market share – COST is also a large mover of US groceries – thus the coronavirus pandemic will not deal a blow to their demand profile. Chart 15Defense Is… The 10-year Treasury yield recently melted to 0.31%, fully discounting ZIRP, QE5 and recession. Last week’s Philly Fed survey made for grim reading, a harbinger of acute economic pain in the weeks to come. Tack on the 40% jump in weekly unemployment insurance claims, and things are falling into place for additional gains in relative share prices (Chart 16). Finally, overall tighter financial conditions and the more than doubling in the junk spread also corroborate that the path of least resistance remains higher for hypermarket equities (second & middle panels, Chart 15). Bottom Line: We reiterate our overweight stance in the S&P hypermarkets index. Today, we are also instituting a risk management metric in order to protect profits: we are implementing a rolling 10% stop from the highs in order to protect gains. The ticker symbols for the stocks in this index are: BLBG: S5HYPC – WMT, COST. Chart 16…The Best Offense …And Overweight Household Products Household products stocks have recently bounced off of long-term support and have sling shot higher (Chart 17). While we continue to recommend an above benchmark allocation of this safe haven index, we are also obliged to initiate a 5% rolling stop in order to protect our recent explosive gains. We reckon that the COVID-19 experience will scar consumers and alter behaviors with long lasting effects. We doubt this sanitization craze will completely subside following the passing of the pandemic. Our sense is that use of disinfectants and cleaning products in general will experience a parallel shift higher in the demand curve. Chart 17Held The Line Therefore, consumer outlays on household products will continue to gain share from the overall spending pie and underpin relative share prices (top panel, Chart 18). US household products exports are another important source of demand for the industry. Exports recently ticked higher and the coronavirus pandemic underscores that US manufacturers that are held in high regard abroad especially sanitation household products will struggle to meet export demand (bottom panel, Chart 18). Domestically, overall grocery store level wholesale selling prices are expanding smartly paving the way for a similar trajectory for household products pricing power (second panel, Chart 18). Importantly, given the recent consumer behavior, shortages all but assure that non-durable goods factories will be humming at a time when almost all other industries will grind to a halt (third panel, Chart 18). Moreover, household products are part of consumer goods that have a fairly inelastic demand profile and really shine during recessions. The recent collapse of the Philly Fed survey heralds a durable outperformance phase for household products equities (Chart 18). While relative valuations appear expensive, relative forward EPS and revenues are slated to trail the market in the coming 12 months. If our thesis pans out then household products stocks will grow into their pricey valuations as profits will overwhelm (Chart 19). Chart 18Demand Driven Advance In fact, our macro based S&P household products sale per share growth model does an excellent job in capturing all these drivers and signals that top line growth will continue to accelerate for the rest of the year (Chart 20). Chart 19Low Bar To Surpass Chart 20Macro Model Says Buy Bottom Line: Stick with the S&P household products index, but institute a 5% rolling stop from the highs in order to protect profits. The ticker symbols for the stocks in this index are: BLBG: S5HOPRX – PG, CL, KMB, CLX, CHD. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA US Equity Strategy Daily Report, “Closing Out All High-Conviction Calls” dated March 20, 2020, available at uses.bcaresearch.com. 2 Please see BCA US Equity Strategy Weekly Report, “Inflection Point” dated March 16, 2020, available at uses.bcaresearch.com. 3 Please see BCA US Equity Strategy Daily Report, “Gravitational Pull” dated March 12, 2020, available at uses.bcaresearch.com. 4 http://www.cboe.com/products/vix-index-volatility/vix-options-and-futures/vix-index/vix-historical-data 5 https://www.cbsnews.com/news/ben-bernankes-greatest-challenge/2/ 6 Please see BCA US Equity Strategy Daily Report, “Don’t Be A Hero” dated March 11, 2020, available at uses.bcaresearch.com. 7 https://www.oecd.org/gov/budgeting/Public%20Governance%20Issues%20in%20China.pdf 8 Please see BCA US Equity Strategy Weekly Report, “A Recession Thought Experiment” dated June 10, 2019, available at uses.bcaresearch.com. 9 Please see BCA US Equity Strategy Weekly Report, “Divorced From Reality” dated July 15, 2019, available at uses.bcaresearch.com. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations Size And Style Views June 3, 2019 Stay neutral cyclicals over defensives (downgrade alert) January 22, 2018 Favor value over growth May 10, 2018 Favor large over small caps (Stop 10%) June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V).

Overweight Household products stocks are in a V-shaped recovery since the early-2018 market peak and these safe haven stocks have more upside in times of tumult (middle panel) despite their pricey valuations (bottom panel). Demand for staples remains robust despite the growth slowdown and the current message from the latest PCE report calls for additional relative share price gains (second panel). Not only domestic demand is upbeat, but industry exports are also on a roll, in spite of the U.S. dollar’s recent appreciation (fourth panel). This suggests that non-discretionary items remain in high demand in the rest of the developed world and the emerging markets despite the loss of consumer pricing power. Bottom Line: We reiterate our overweight stance on the S&P household products index. The ticker symbols for the stocks in this index are: PG, CL, CLX, KMB, CHD.

Overweight Procter & Gamble (PG), the heavyweight of the S&P household products sector, delivered excellent results this week and raised their guidance, despite a forecast of a nearly $1 billion after-tax currency headwind to earnings this fiscal year. The principal driver was a push to raise prices across their segments that appears to have gained traction. Our macro indicators agree with PG’s guidance; household product sales have been pushing higher (second panel), driven by a resurgence in pricing power (second panel). Meanwhile, exports have continued their two-year ascent despite the aforementioned tough currency environment and the upshot is that relative EPS growth will likely remain upbeat (bottom panel). In light of challenged EM consumer spending growth, this signal is very encouraging. Bottom Line: Recovering sales in a harsh global environment and growing profits irrespective of currency headwinds point to outsized relative EPS growth should either of these offsets soften; stay overweight. The ticker symbols for the stocks in this index are: PG, CL, CLX, KMB.

Household product stocks have typically performed well as retail gasoline prices have contracted; this iteration has proven no different. This boon to consumers has supported an uptick in spending on household products, which should translate into top line…

Overweight Household product stocks have typically performed well as retail gasoline prices have contracted; this iteration has proven no different (gasoline prices shown inverted, top panel). This boon to consumers has supported an uptick of the consumer’s wallet being deployed to household products which should translate into top line support for these equities (second panel). Curiously, the end of the bear market for this sector coincided with a moderating of S&P household products profit margins from their historically high level (third panel). The market is likely seeing ahead to a return to margin expansion. As noted above, the demand environment appears robust and, with commodity and labor costs well contained (bottom panel), things should continue looking up for the sector, especially given the recent success constituents have had in raising selling prices. Bottom Line: Earnings growth looks set to reaccelerate in the S&P household products index; we reiterate our overweight recommendation. The ticker symbols for the stocks in this index are: BLBG: S5HOPR – PG, CL, KMB, CLX and CHD.

Overweight The S&P household products index got a solid lift last week on the back of upbeat earnings from sector heavyweight Procter & Gamble (PG), though this was also part of a greater rotation into consumer staples. PG noted volume increases across all of their consumer staples segments with the global consumer remaining remarkably resilient. Despite a clearly healthy quarter, the company maintained their guidance for the next three quarters, suggesting the positive trend has some longevity. This broadly matches the macro signal, with exports of consumer goods staging a multi-year recovery, which should further underpin recent earnings outperformance (second panel). One minor negative anecdote, however, was the reference to the rising greenback that should eat into margins especially in early 2019, but rising volumes on the back of resilient demand should provide an offset. An appreciating U.S. dollar is an earnings risk we have been flagging in recent research for SPX exporters, especially if an EM accident materializes. Still, sector valuations remain depressed, implying bargains are still to be found in household products. We reiterate our overweight recommendation. The ticker symbols for the stocks in this index are: PG, CL, CLX, KMB.