India

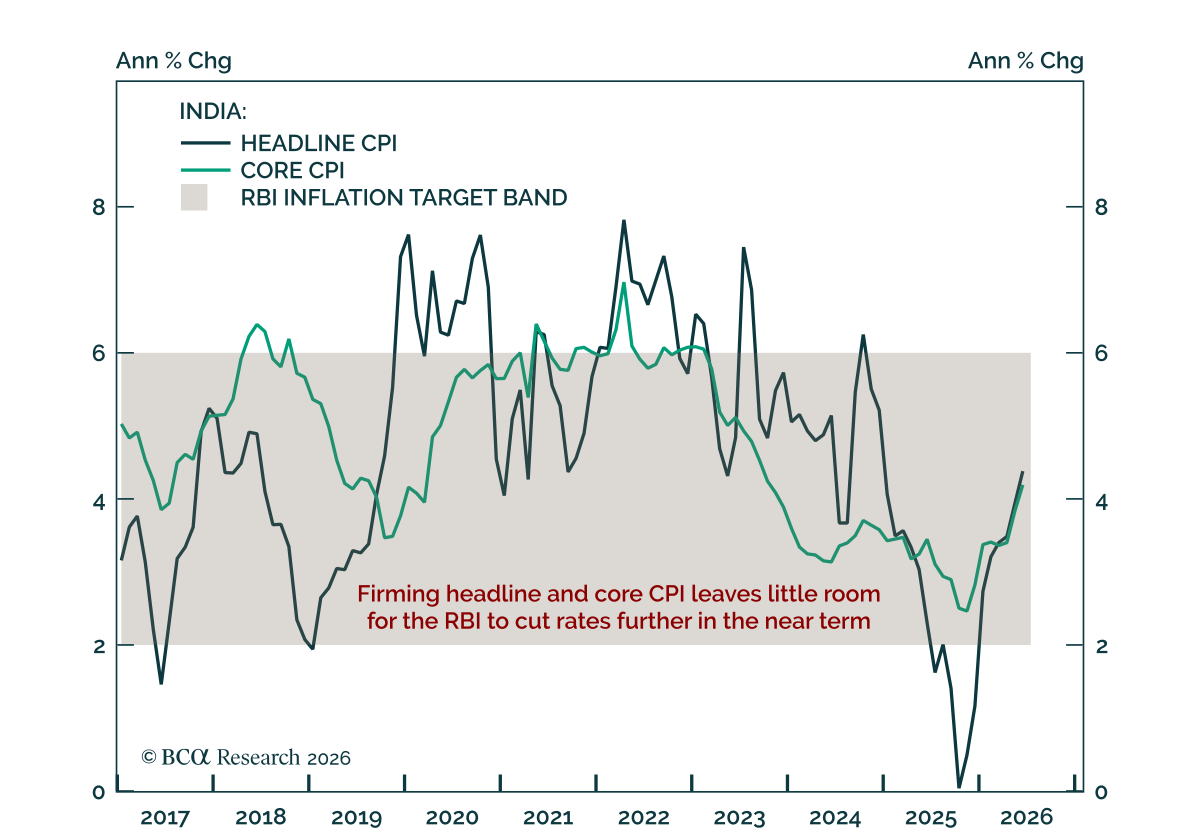

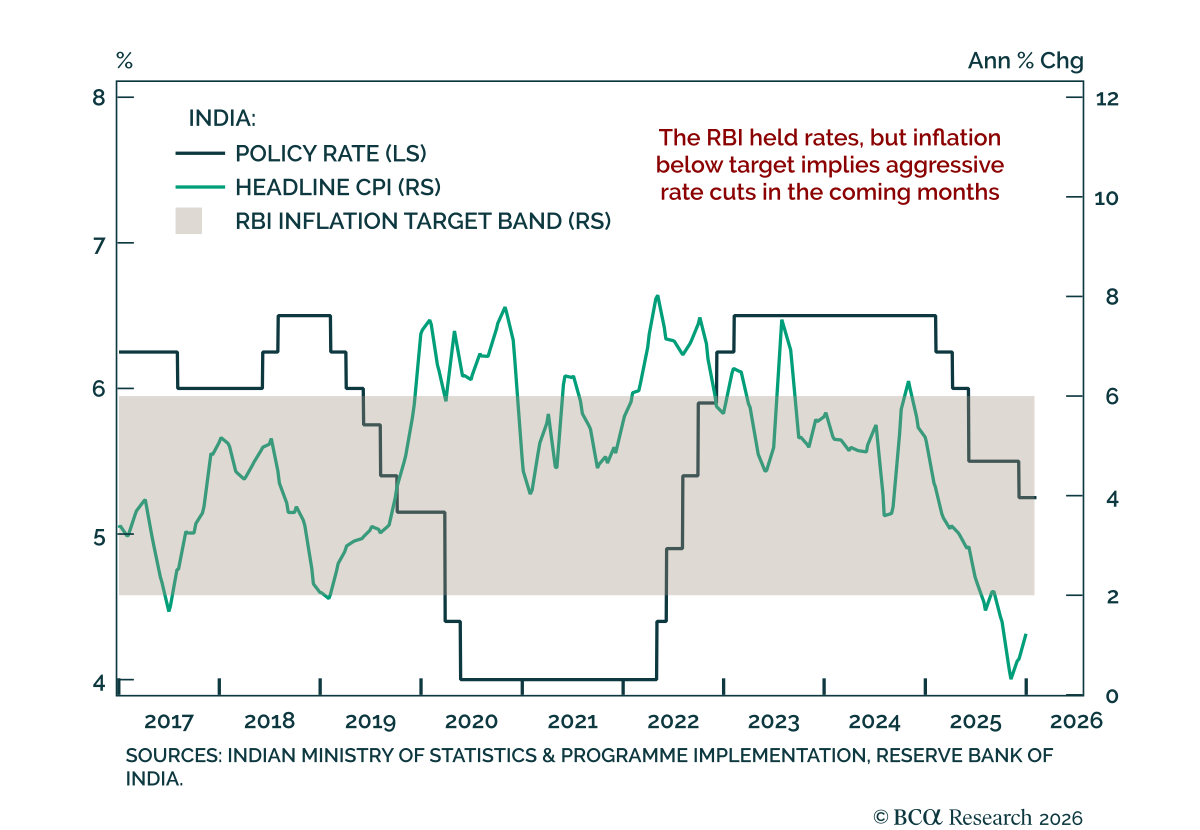

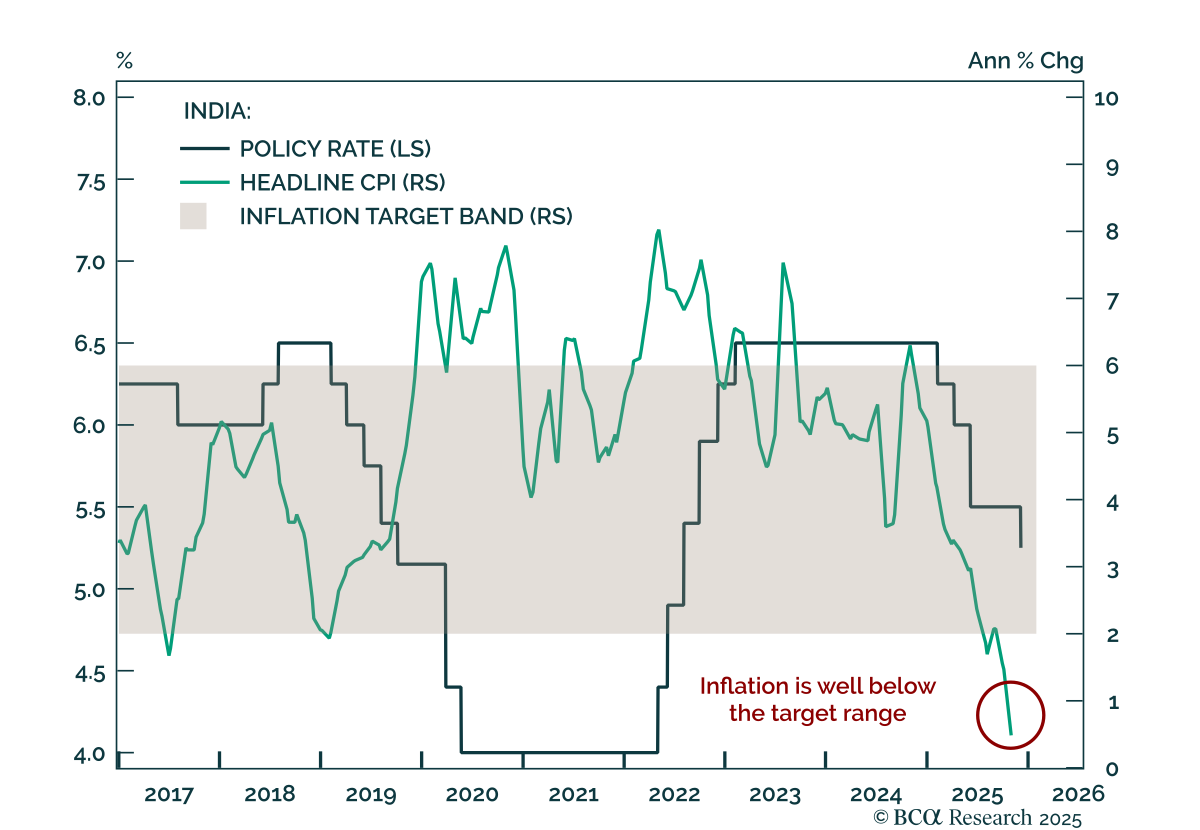

India is probably the most vulnerable among the G-20 economies should the Strait of Hormuz not reopen fully by the end of this month. Growth will slow, while inflation will rise materially. Investors should brace for further weakness in the currency and stock prices.

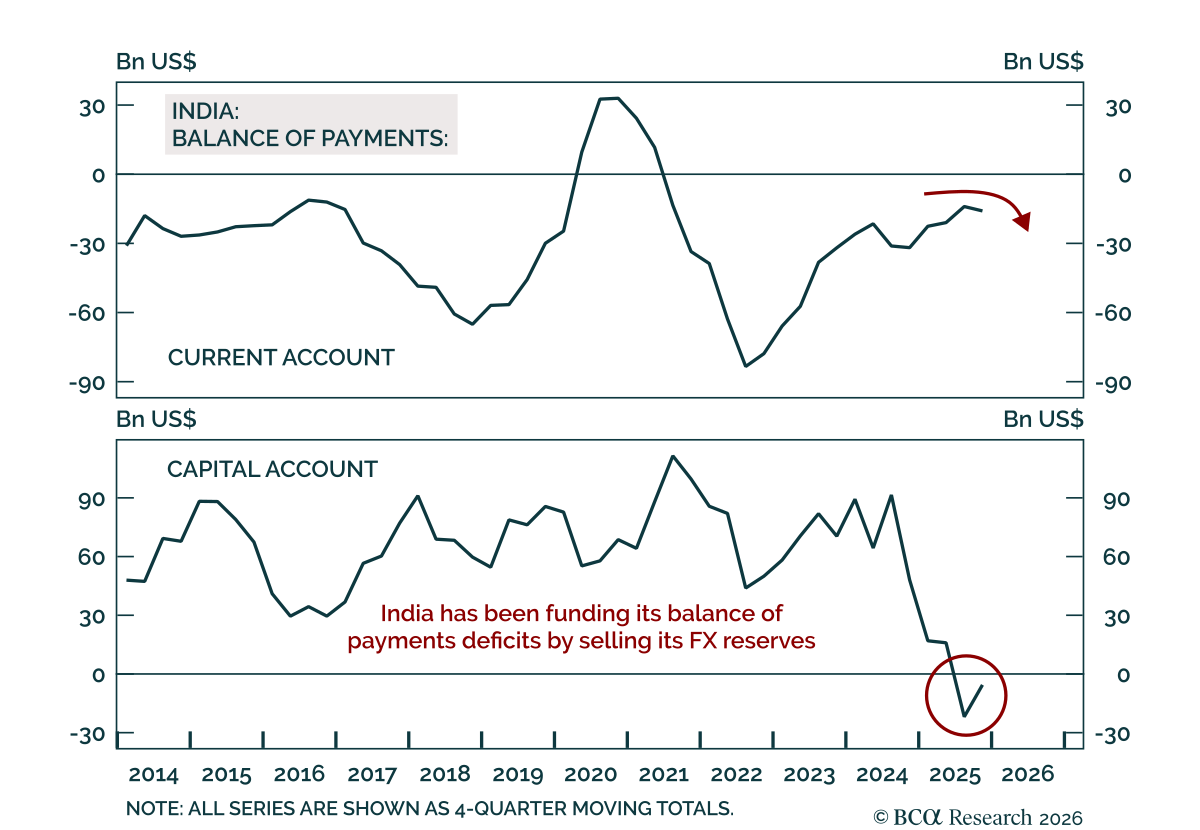

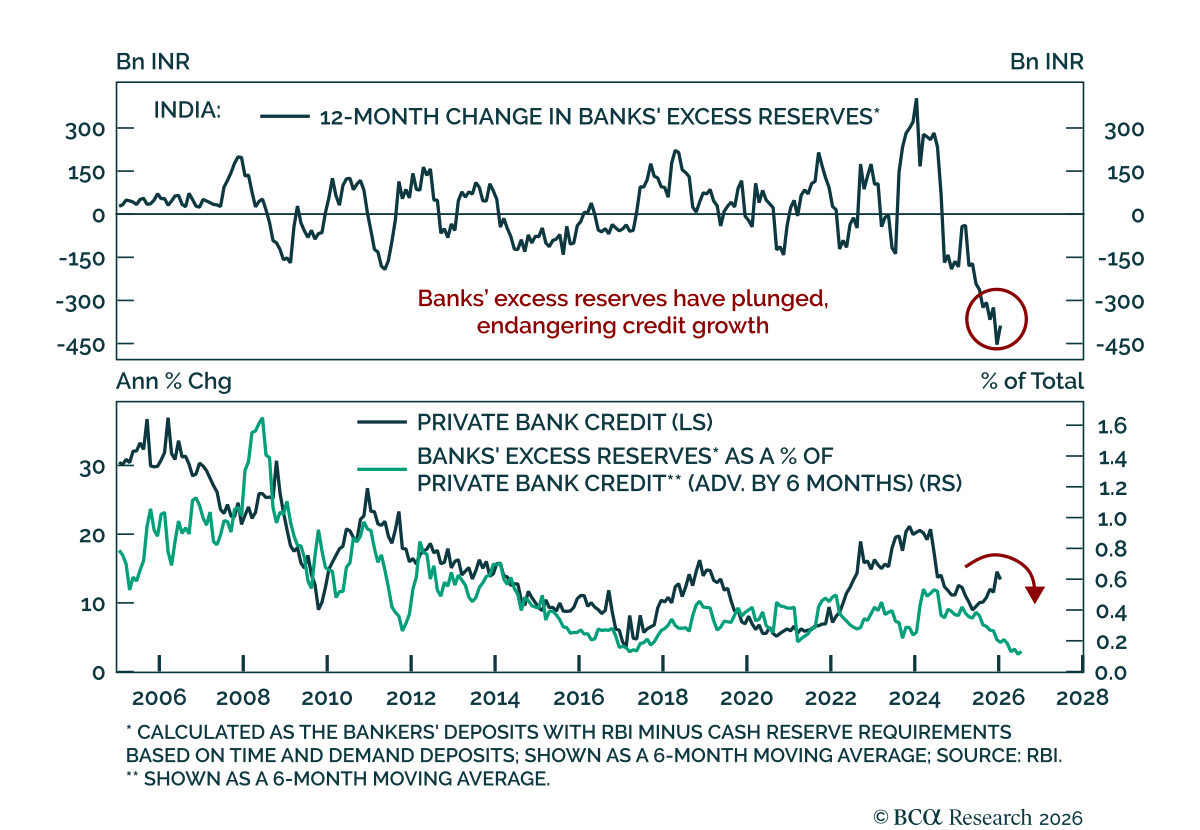

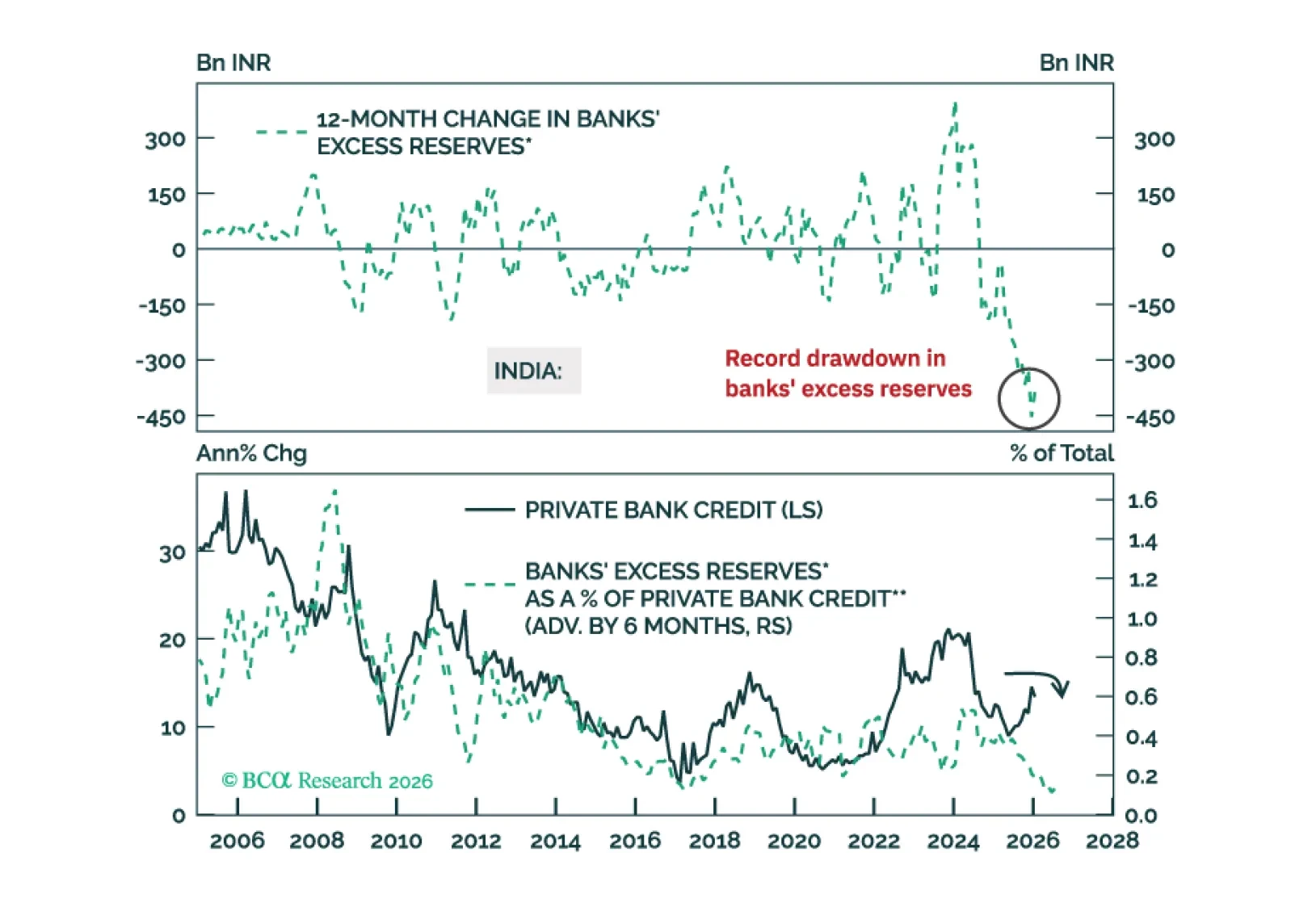

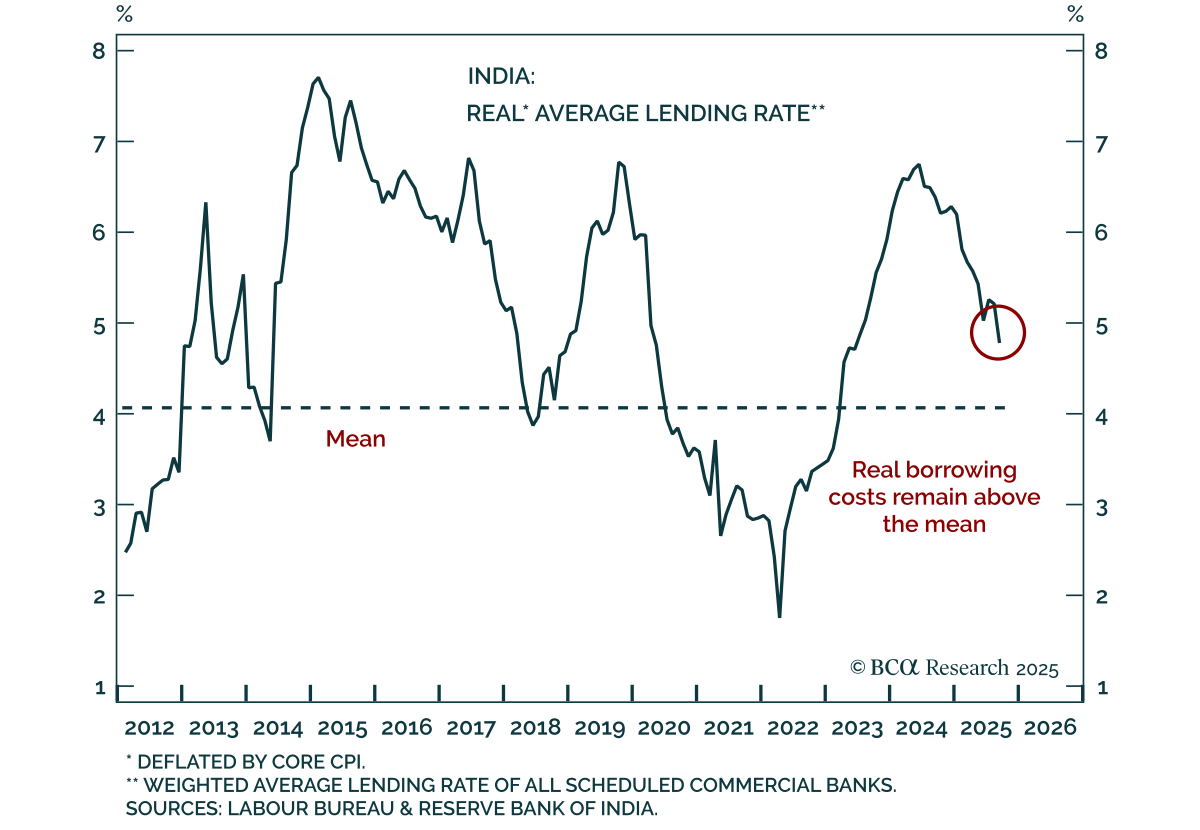

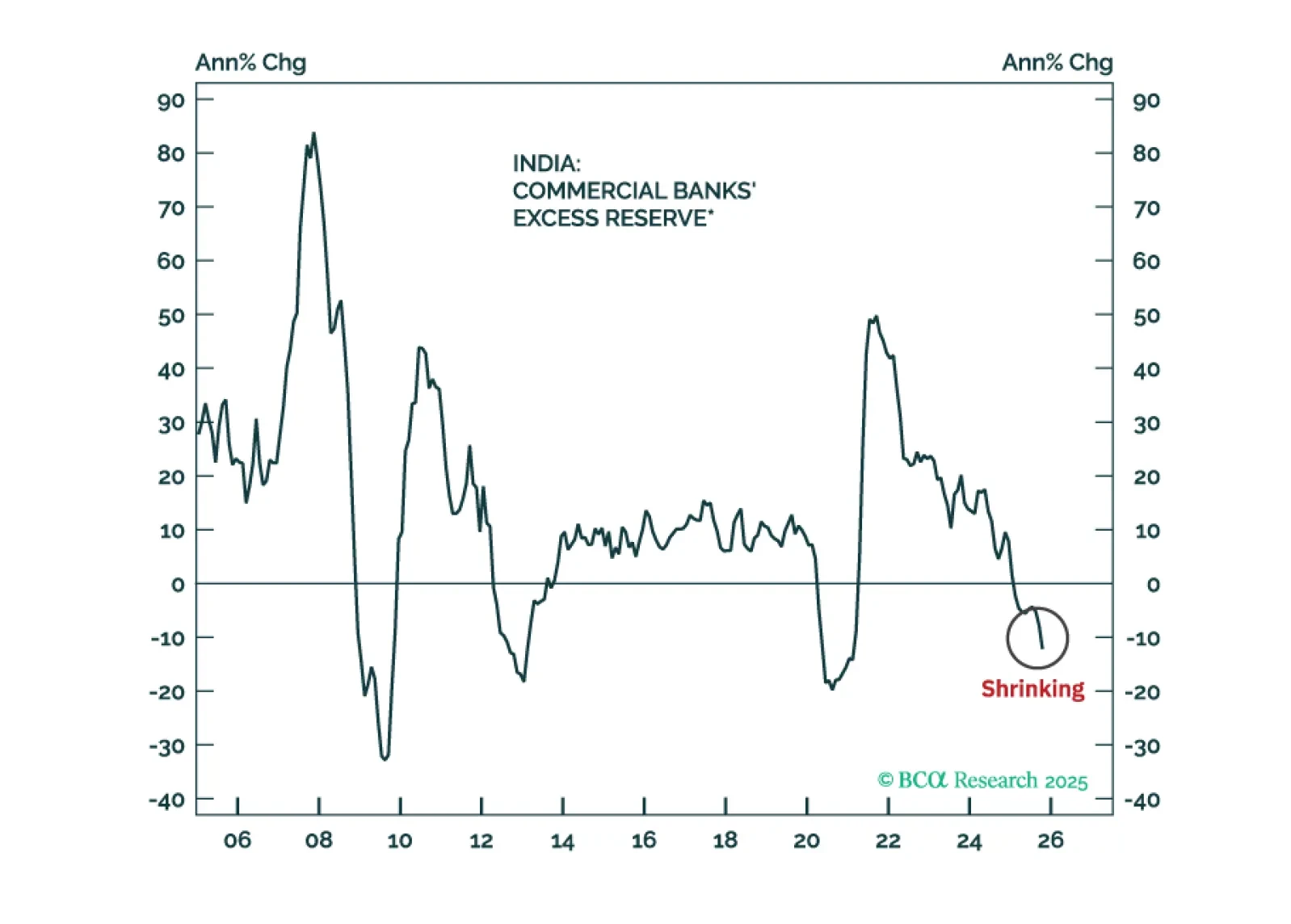

India is seeing net capital outflows for the first time in a generation. The central bank is selling foreign reserves to defend the rupee, which is draining banking system liquidity. The latter risks derailing the nascent credit revival. Indian stock prices remain vulnerable.

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

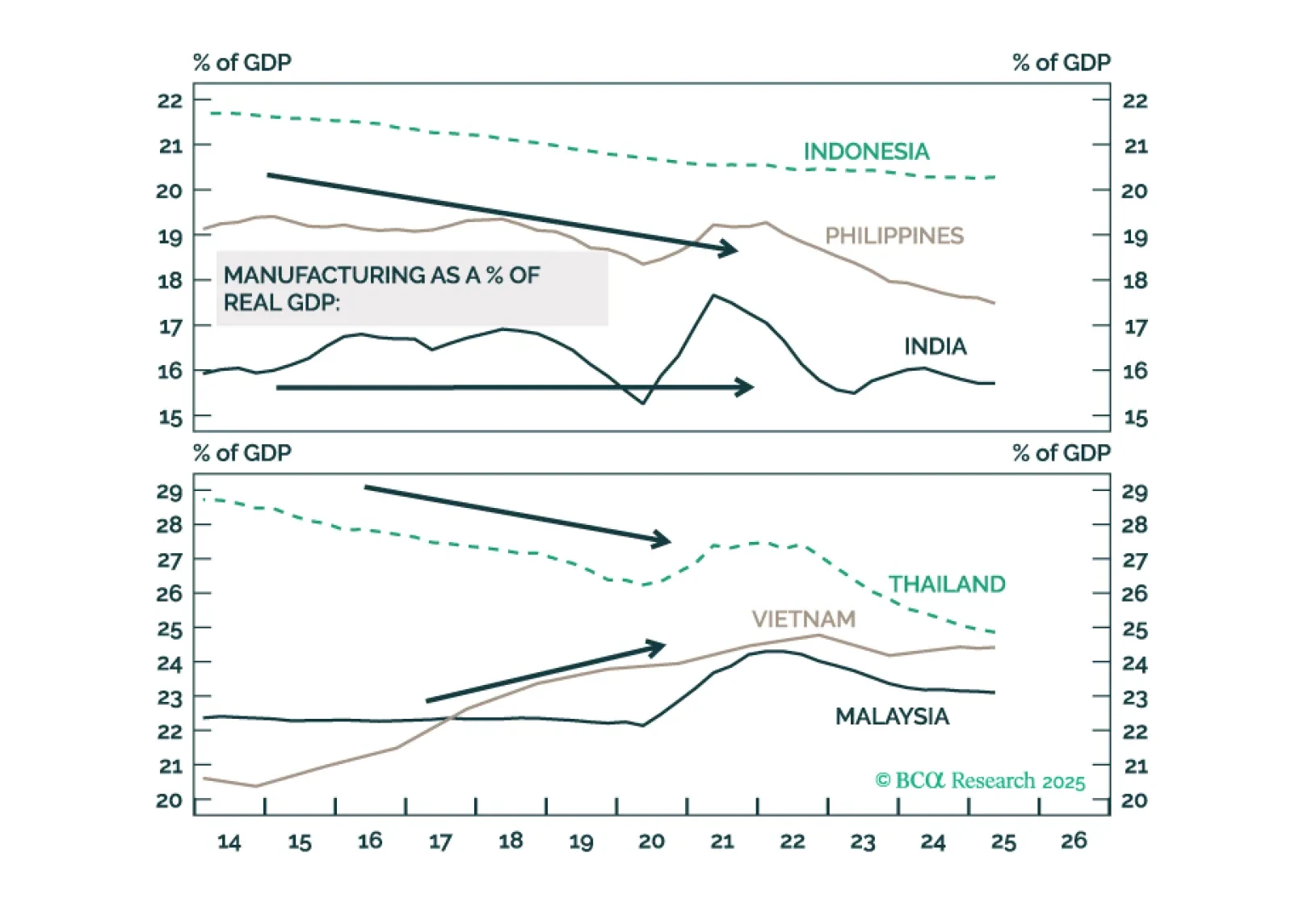

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.