India

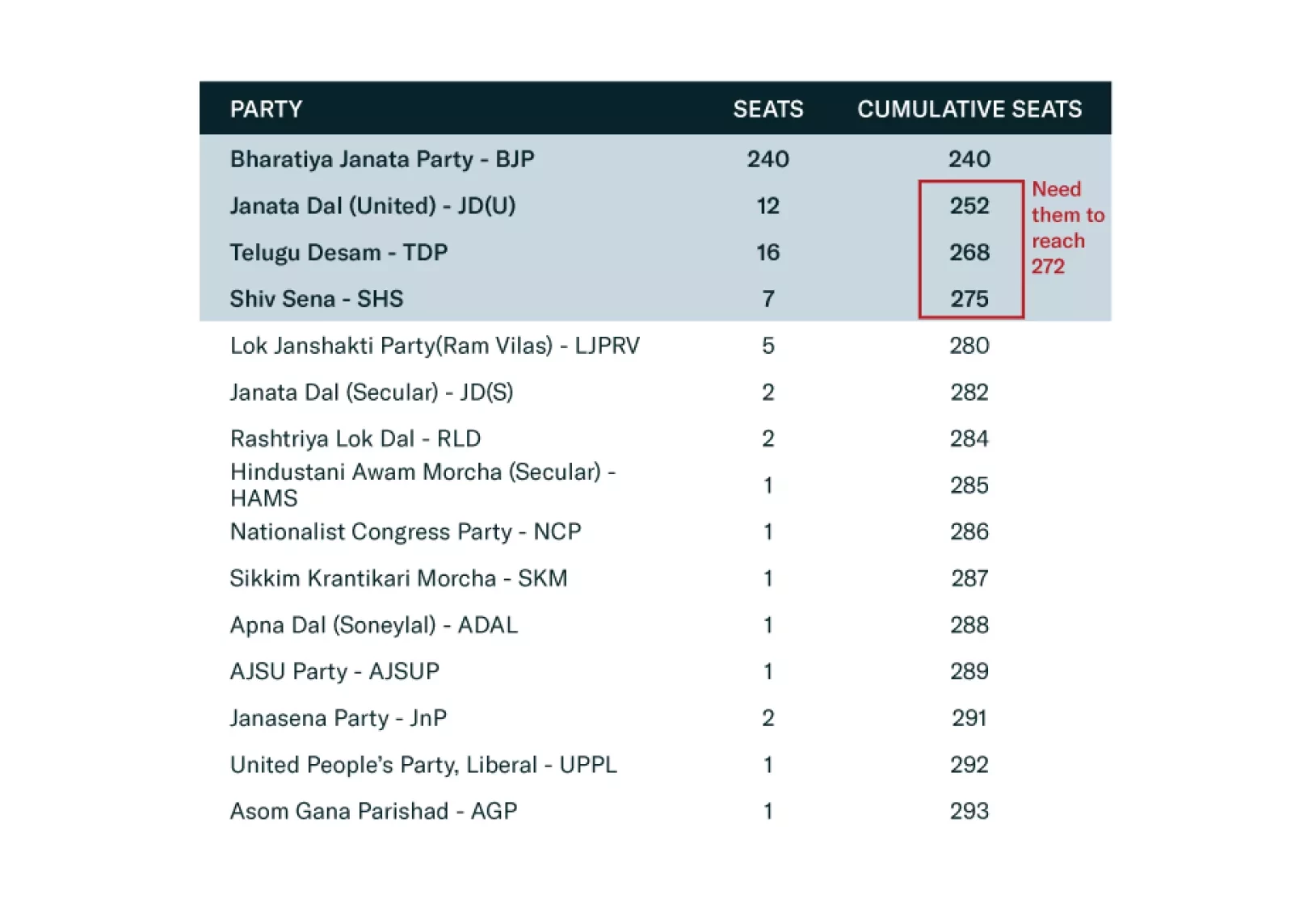

Prime Minister Narendra Modi won a third term and will become the third longest-serving prime minister of India. While investors responded negatively to the BJP’s loss of an outright majority, Modi and the NDA will continue to perpetuate the reforms they have already put into motion. The result also affirms that Indian democracy continues to thrive, contrary to the narrative that Modi had formed an authoritarian grip on the country, a view we always rejected.

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.

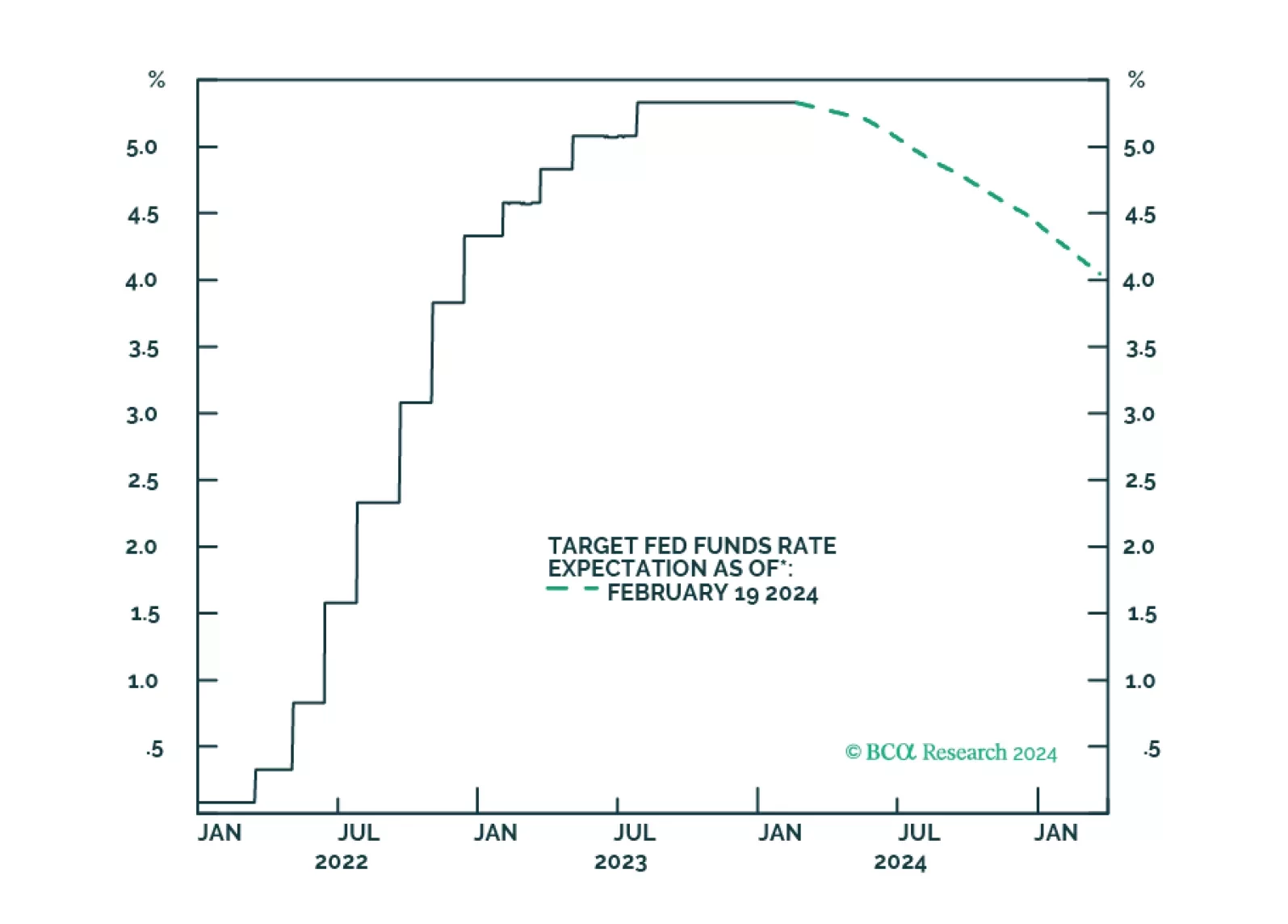

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.

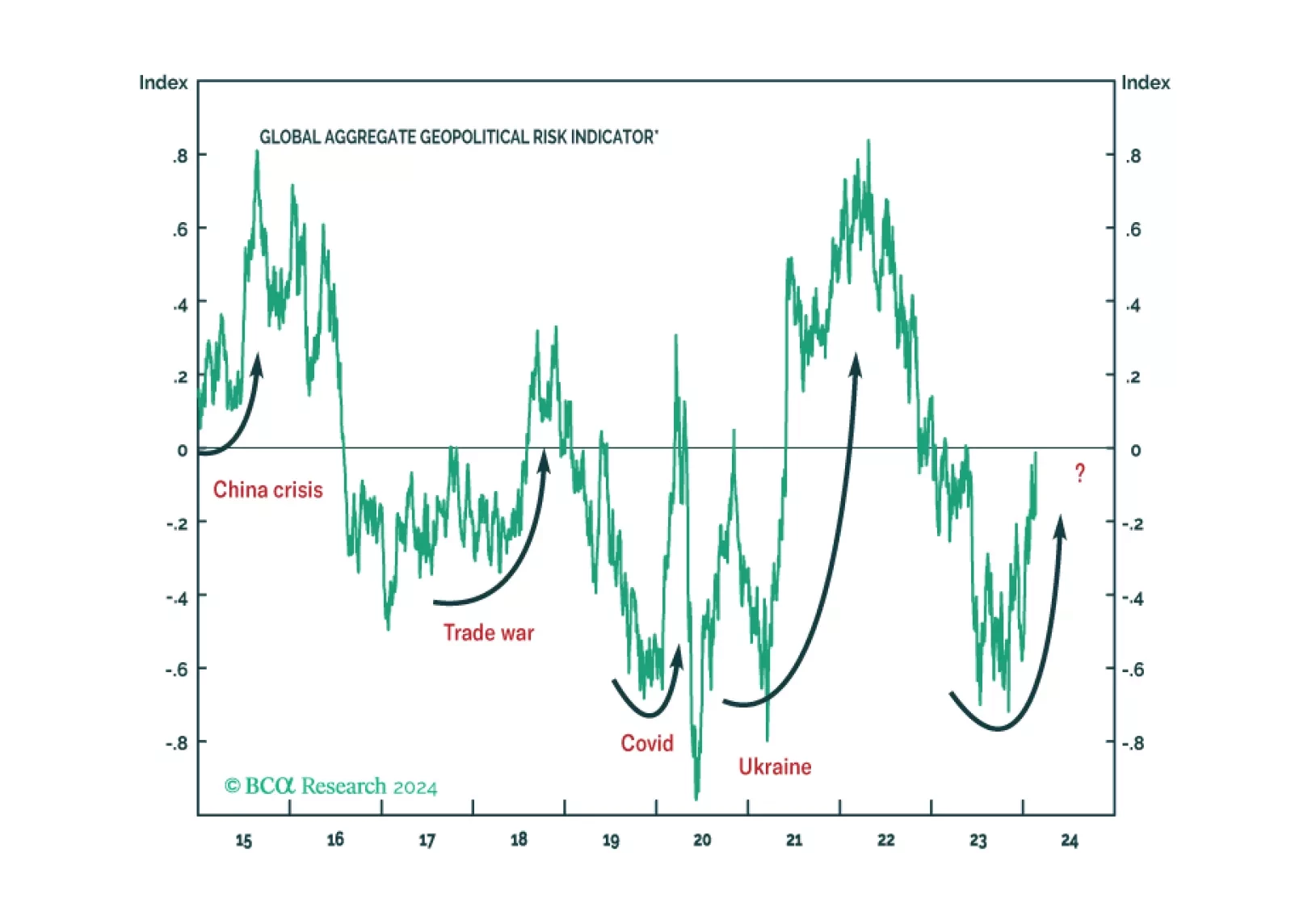

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

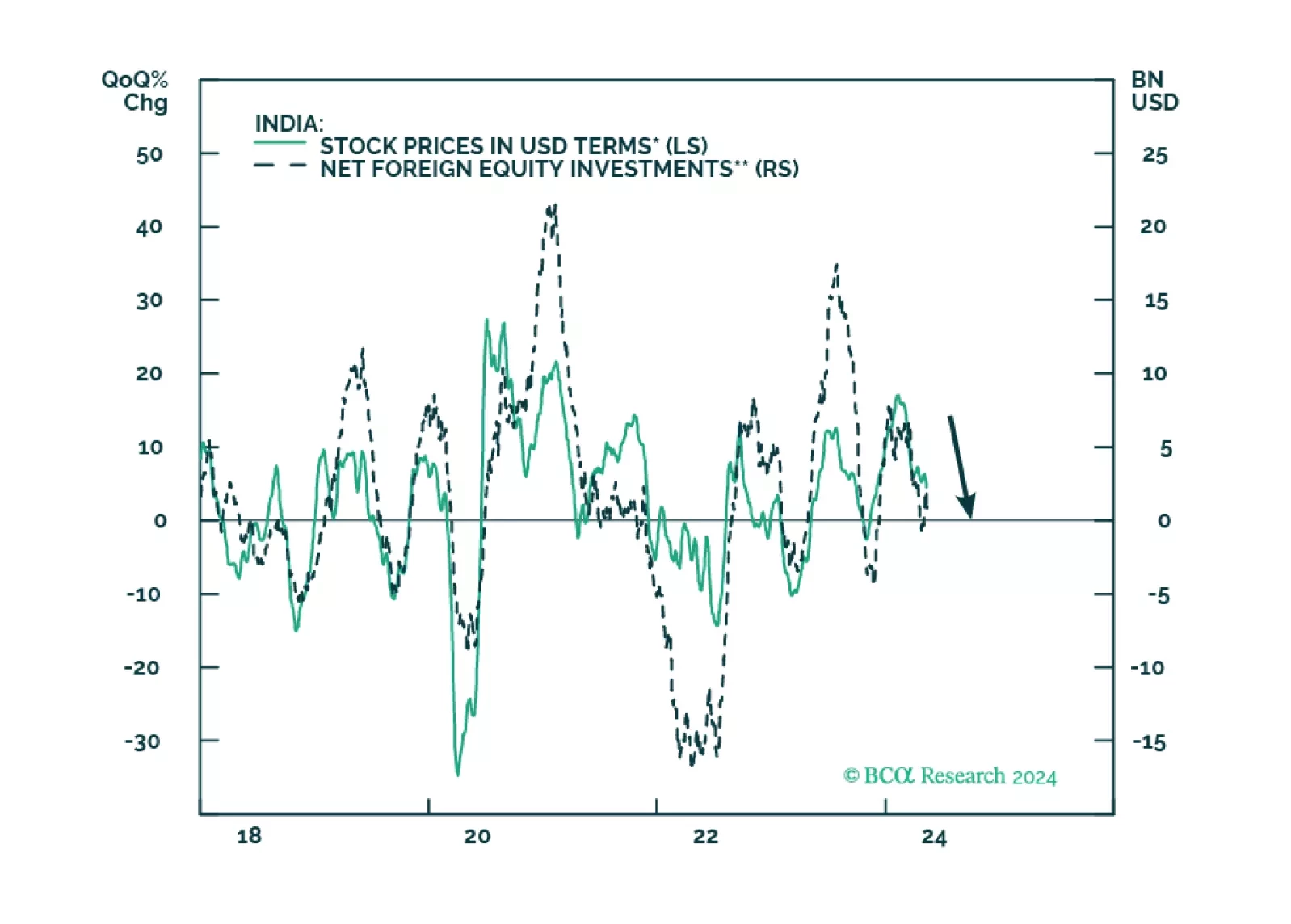

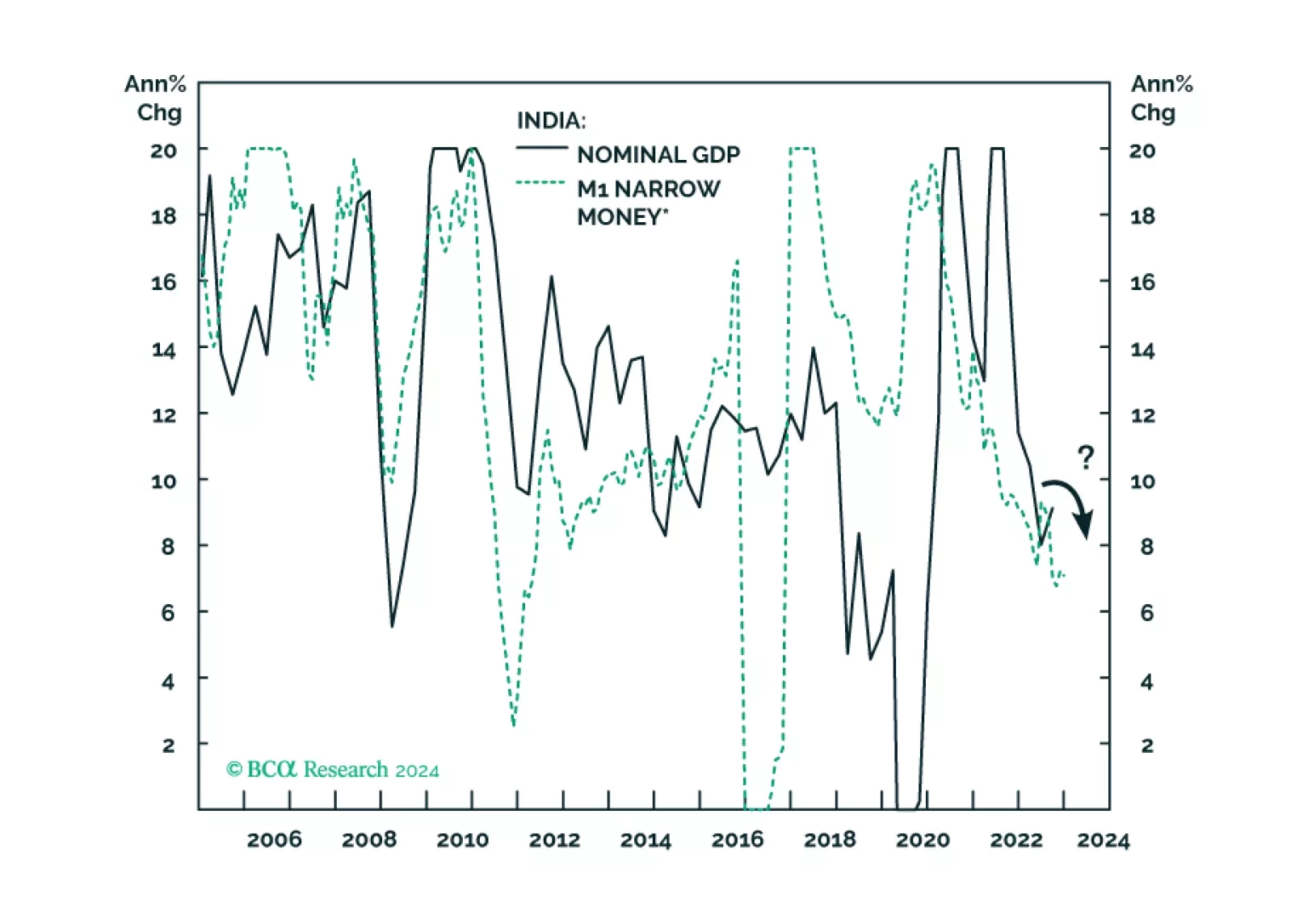

Decelerating nominal sales, a peaking credit cycle, and very high valuations - Indian stocks will not escape the carnage when risk assets globally begin to sell off.

India’s intake of industrial commodities is 10-to-20 times as small as China’s. Capital goods are five times as small. Hence, India is not in a position to offset any decline in Chinese demand for these commodities and goods.