Indonesia

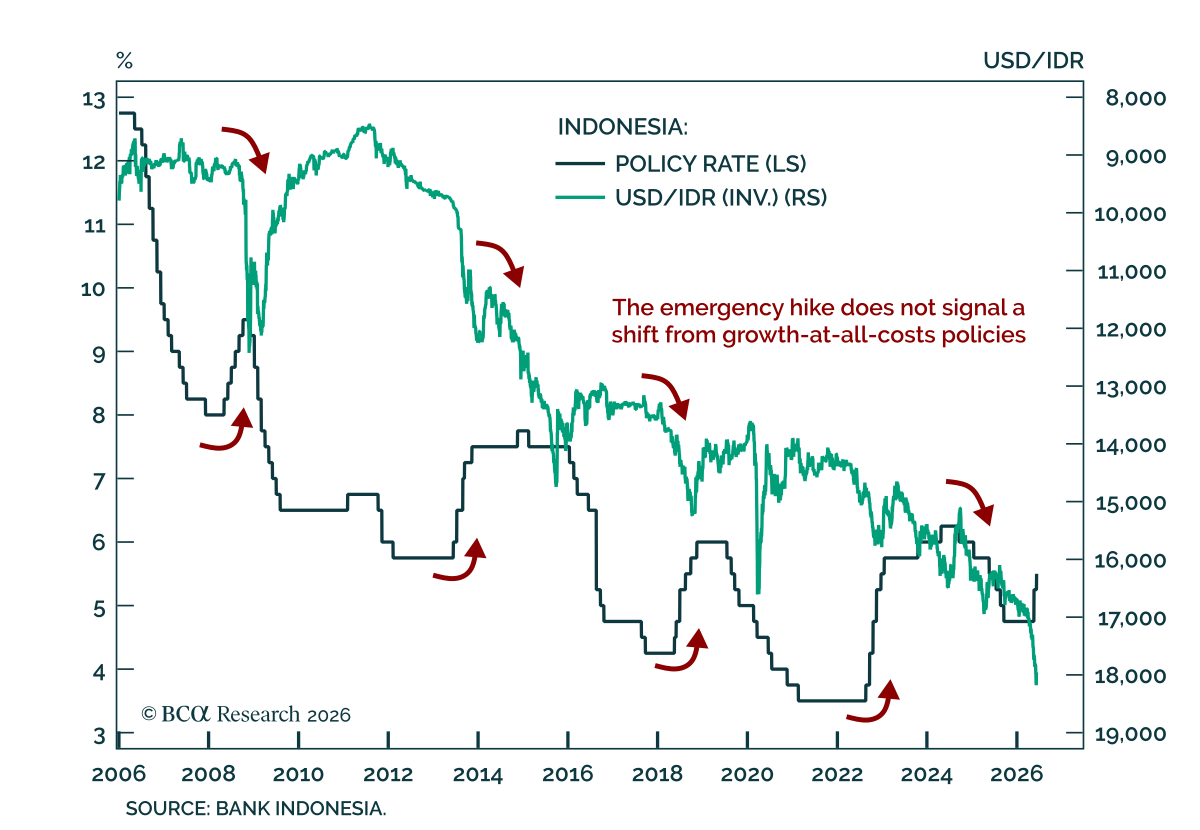

Bank Indonesia’s off-cycle rate hike was a defensive move to slow the rupiah’s slide, not a change in the broader policy story. After raising its policy rate to 5.25% at last week's scheduled meeting, the Indonesian central bank surprised with an unscheduled…

Bank Indonesia raised its policy rate by 50 bps to 5.25% last week, 25 bps above expectations, as a response to persistent rupiah weakness. The recent sell-off in the rupiah and local bonds was partly triggered by the finance minister's plan to spend an…

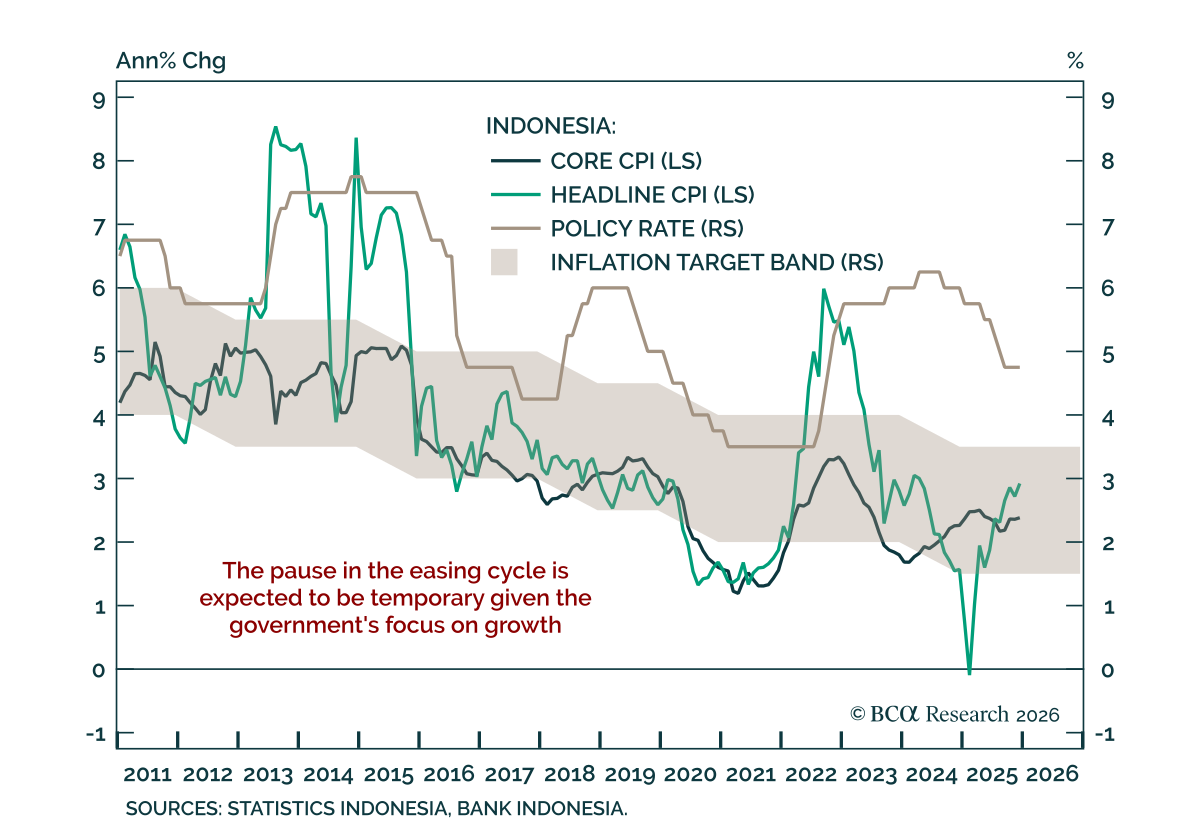

Indonesia’s policy mix remains negative for the rupiah and local fixed income. The central bank kept rates unchanged at 4.75%, in line with expectations and with our Emerging Markets strategists’ view that authorities remain unwilling to tighten policy…

Indonesian rupiah will continue to plunge, and its local-currency bond yields will rise materially. Investors should short domestic bonds, currency unhedged.

The Indonesian central bank kept its policy rate steady at 4.75%, in line with expectations. The decision comes as the rupiah has fallen to multi-year lows against the US dollar amid renewed foreign investor concerns over central bank independence and policy…

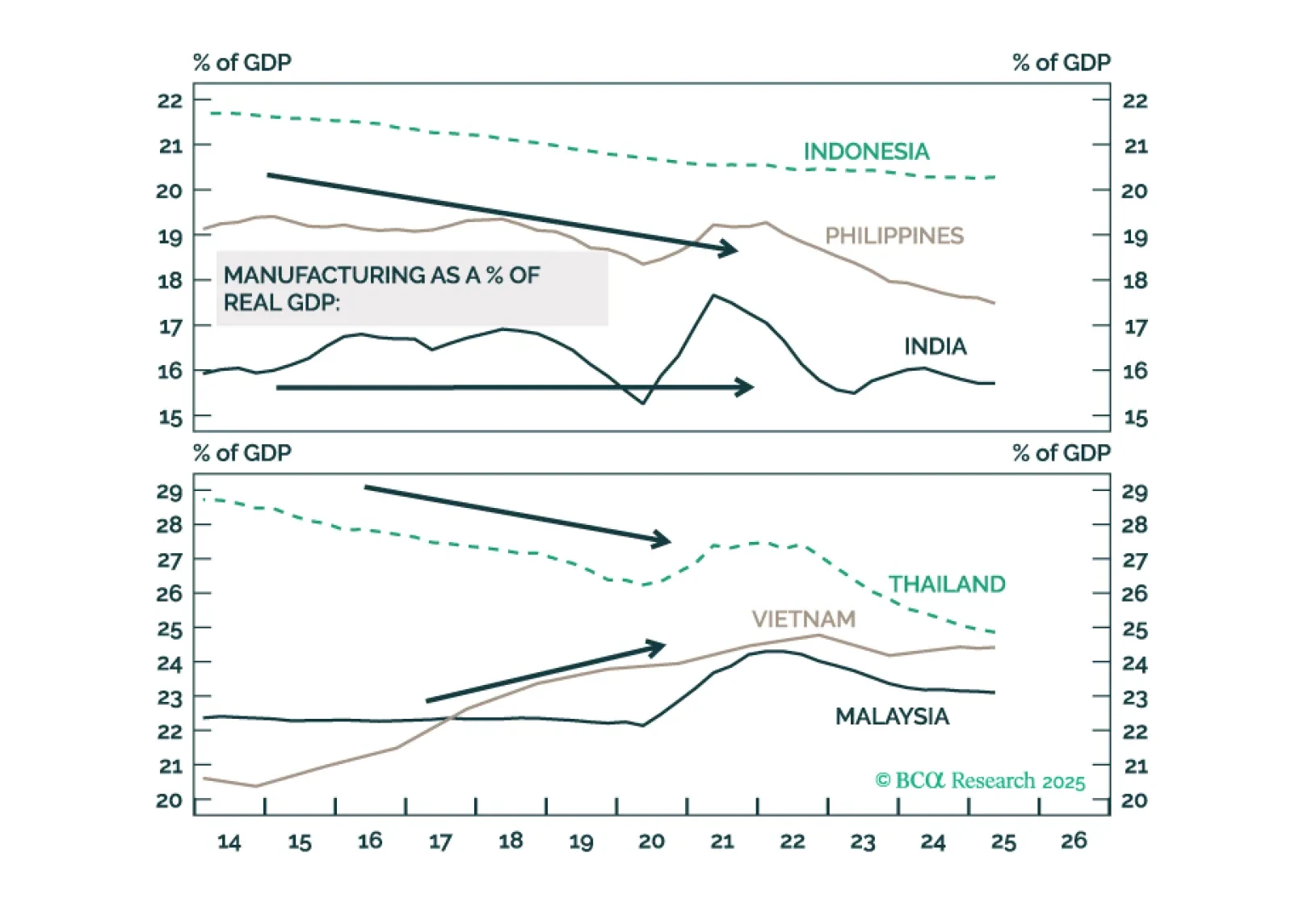

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

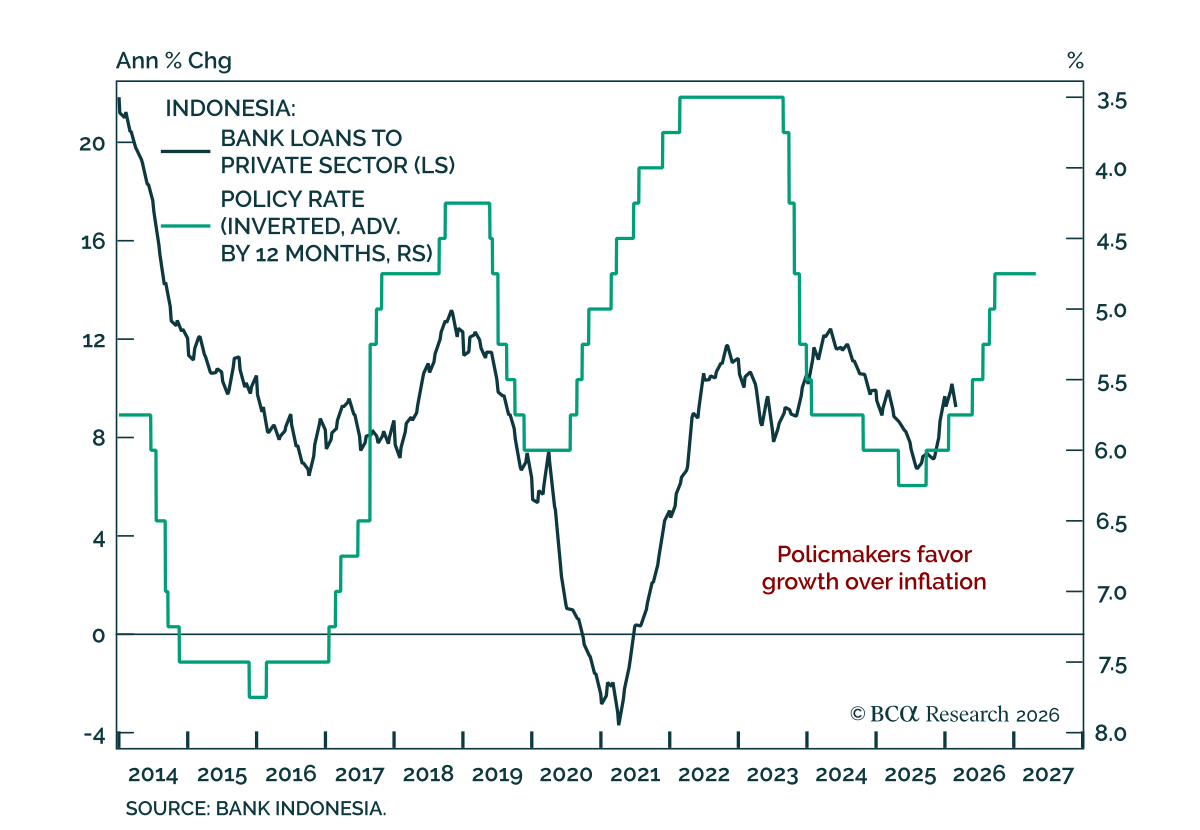

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

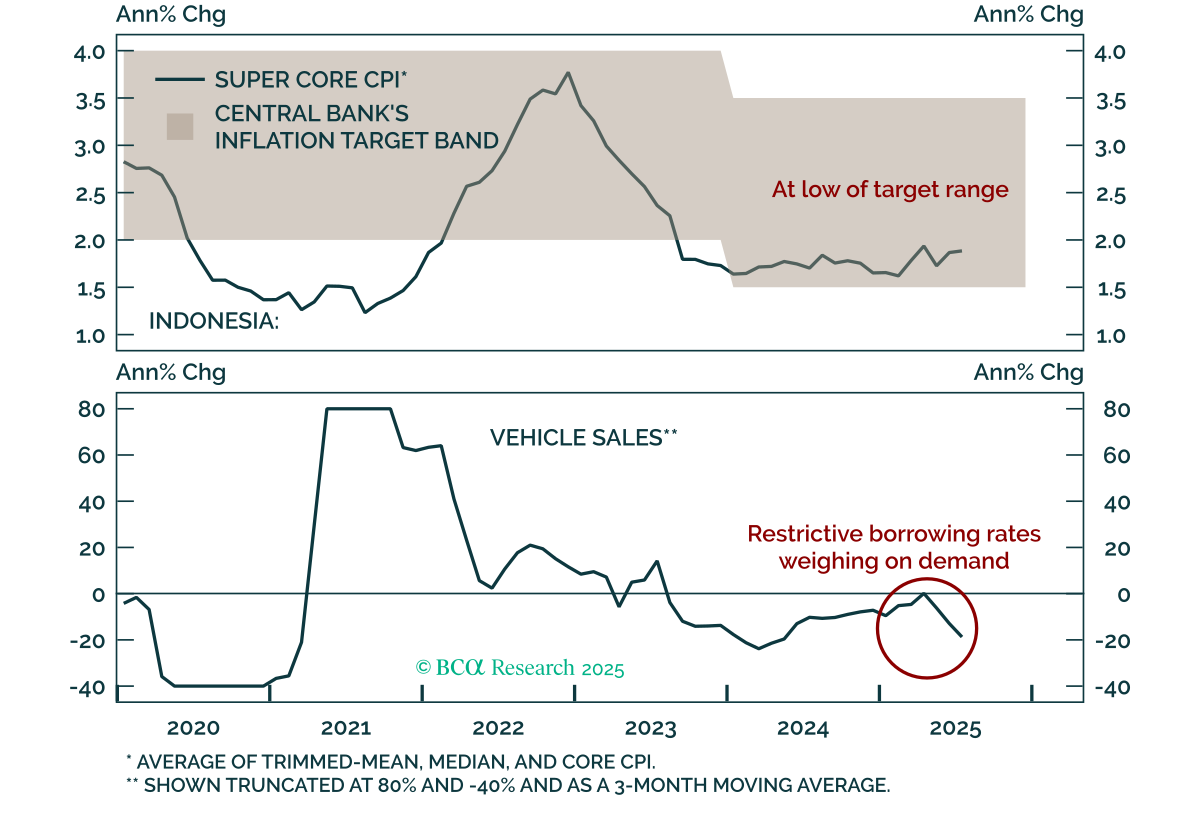

Indonesia’s surprise rate cut signals a dovish turn that will weigh on the rupiah. Bank Indonesia cut its policy rate by 25 bps to 5%, with low inflation and weak activity pointing to more easing ahead. Our Emerging Markets team’s proprietary super core…

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

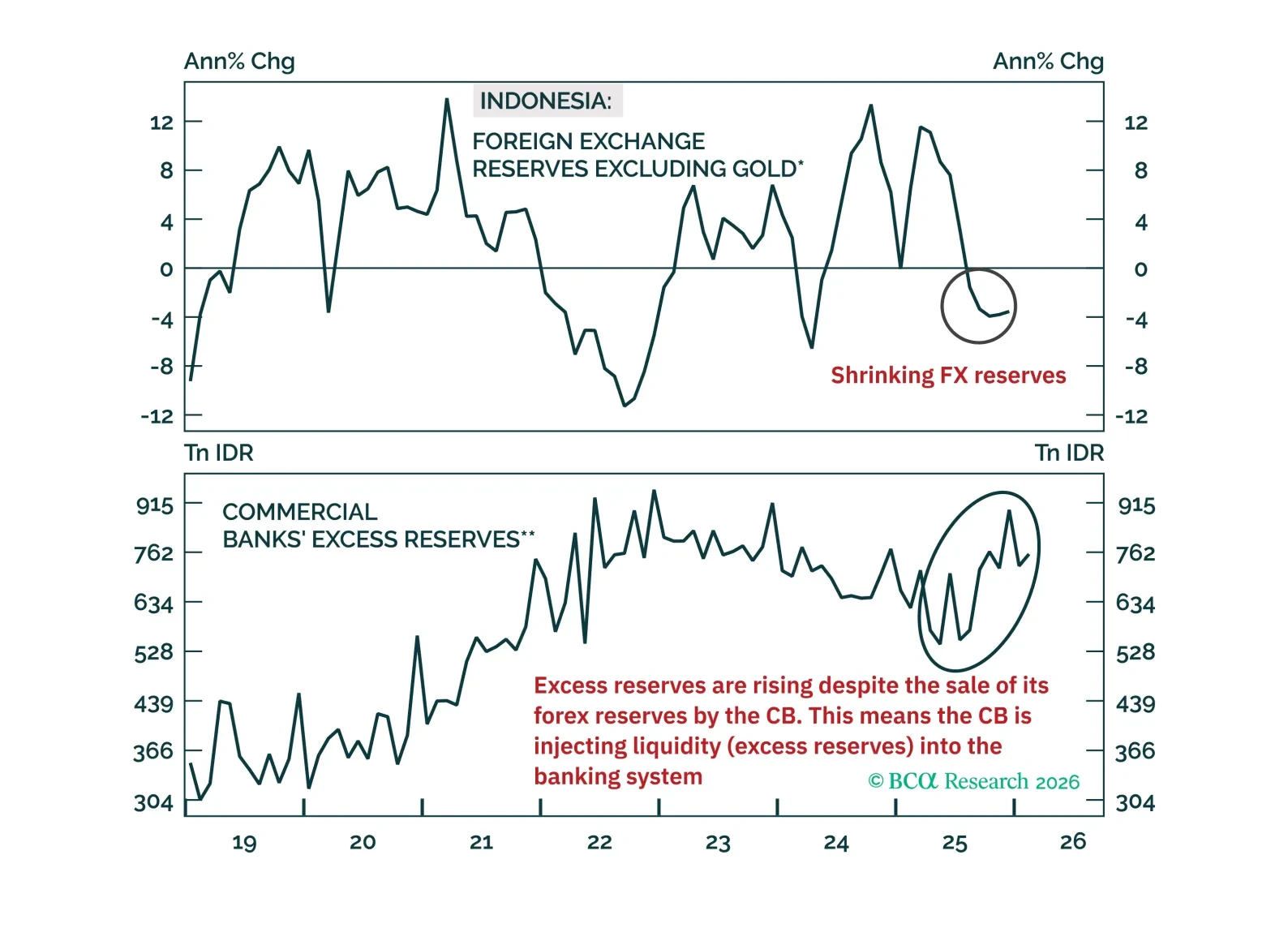

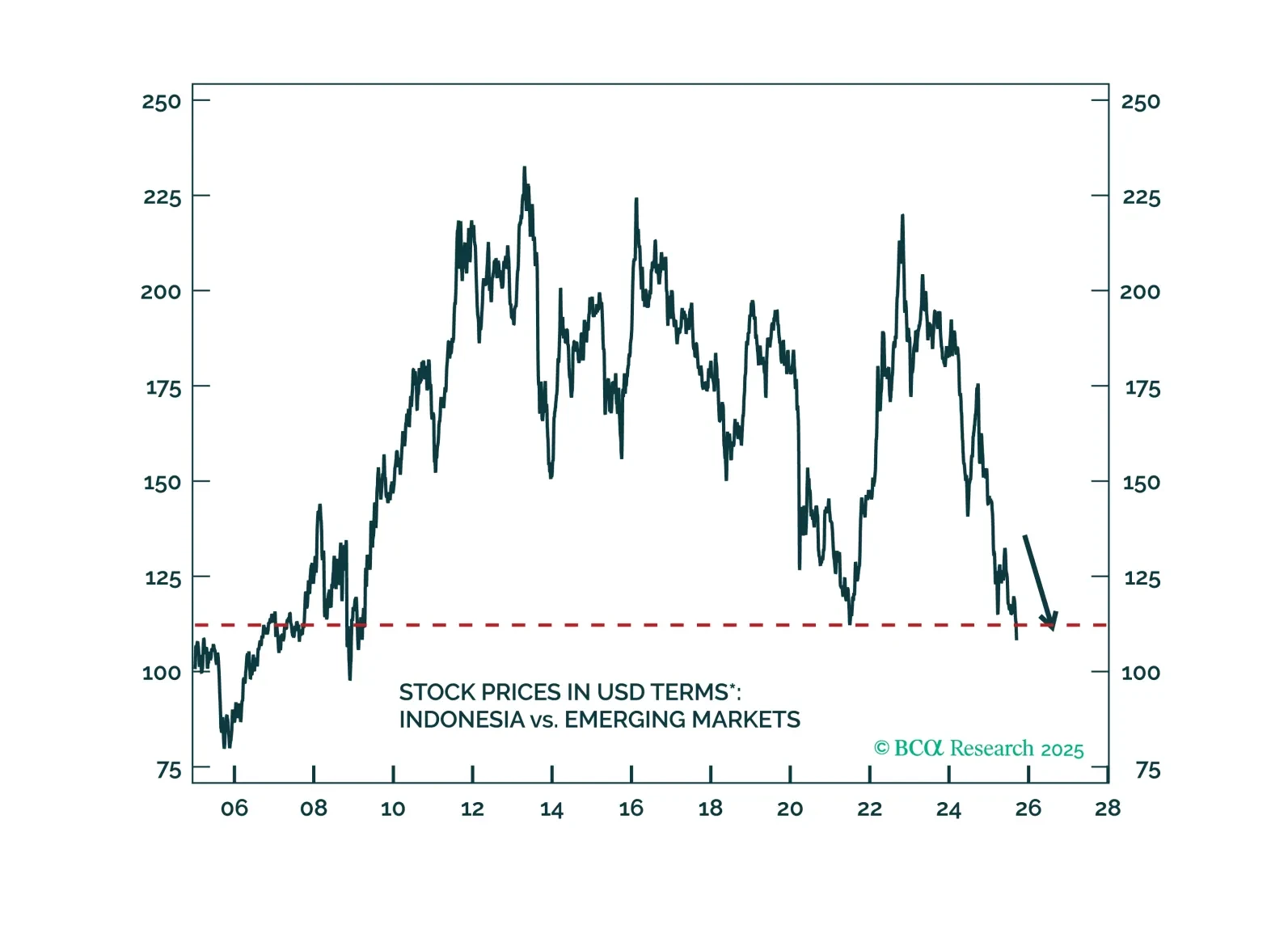

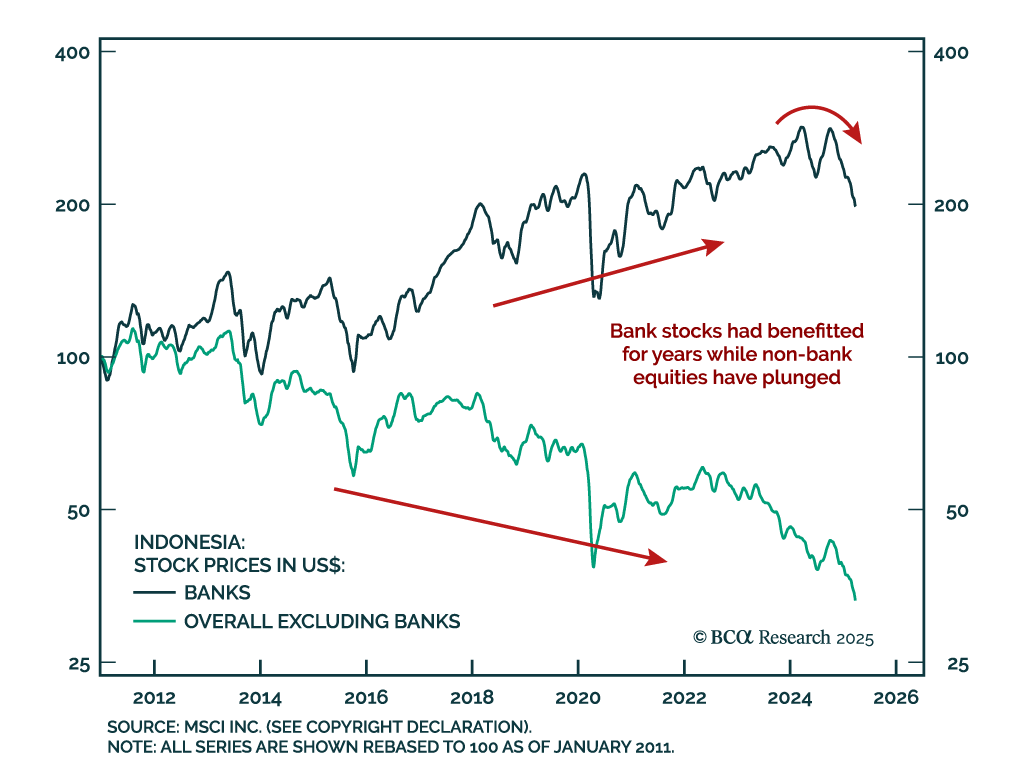

Our Emerging Markets strategists maintain a neutral view on Indonesia within EM equity and bond portfolios but continues to recommend shorting the rupiah versus the US dollar. They are closing their long Indonesian banks/short EM banks position due to…