Inflation/Deflation

We are strategically bullish on the outlook of the energy sector. Domestic and external political constraints asserted themselves, restraining the most negative impulse against this sector by the Biden administration. Go long energy versus cyclicals (ex-tech).

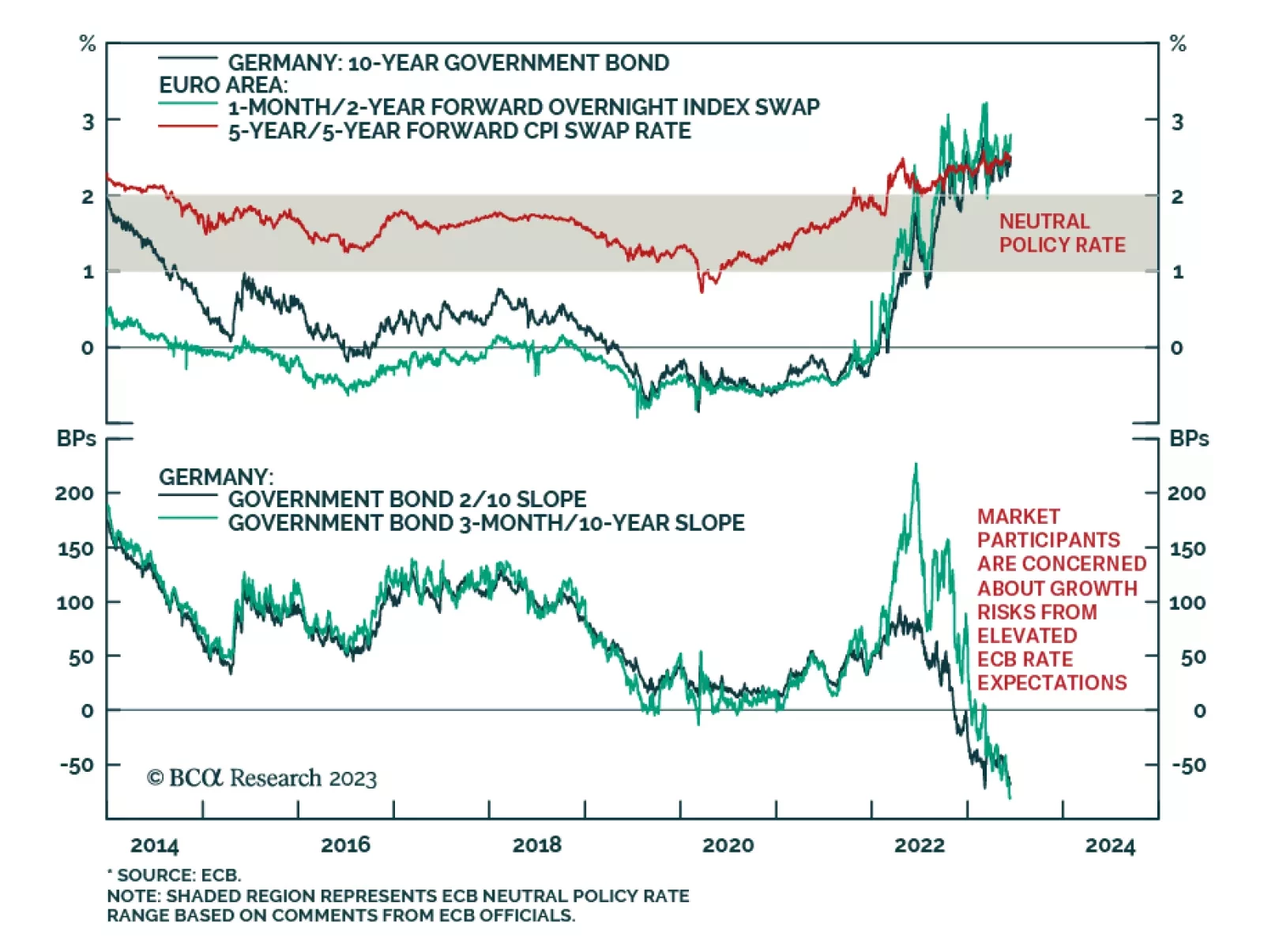

This week’s report examines three potential catalysts that could push Treasury yields meaningfully higher within the next few months. We also consider the rebuild of the Treasury’s cash holdings and its implications for the Fed’s balance sheet policy and financial markets.

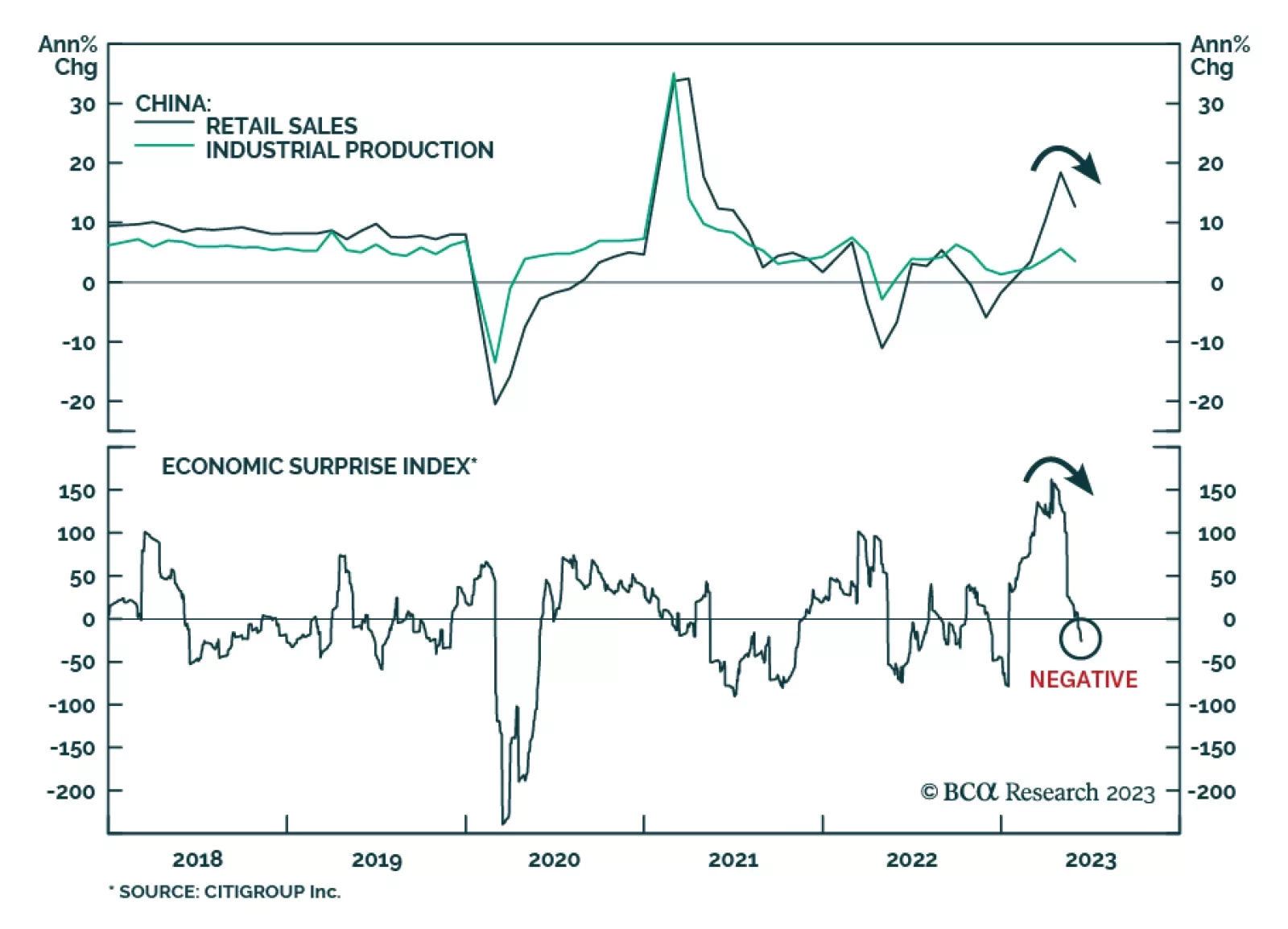

China is facing a risk of deflation. Marginal interest rate cuts and targeted stimulus will be insufficient to boost China’s growth given the current deflationary mindset and the danger is that the economy may be entering a liquidity trap. Deflation is bullish for government bonds, but negative for equity prices. Chinese share prices will continue to decline.

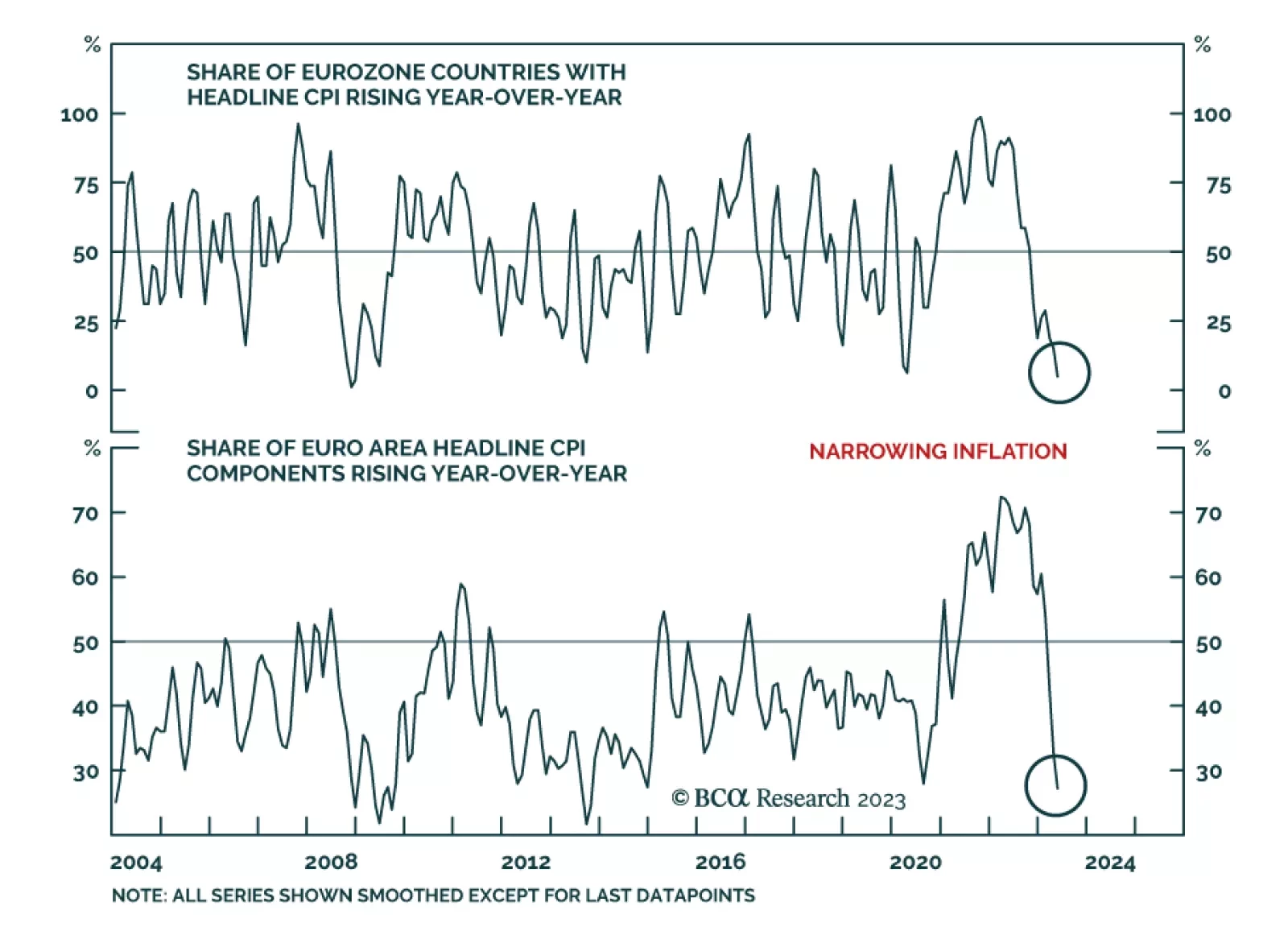

The Eurozone just experienced two consecutive quarters of GDP contraction. For the remainder of the year, can growth pick up or will the ECB decimate activity?

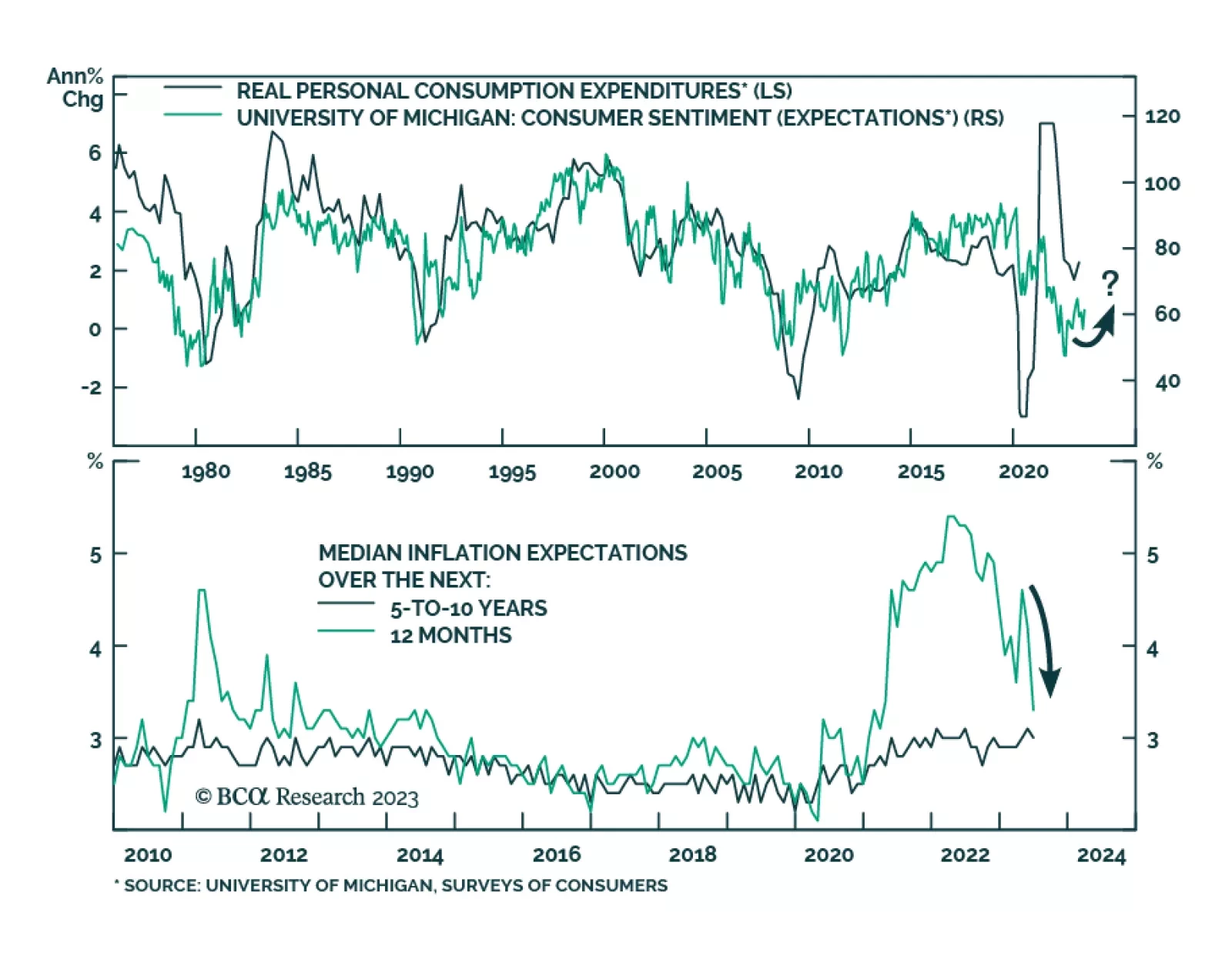

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.