Inflation/Deflation

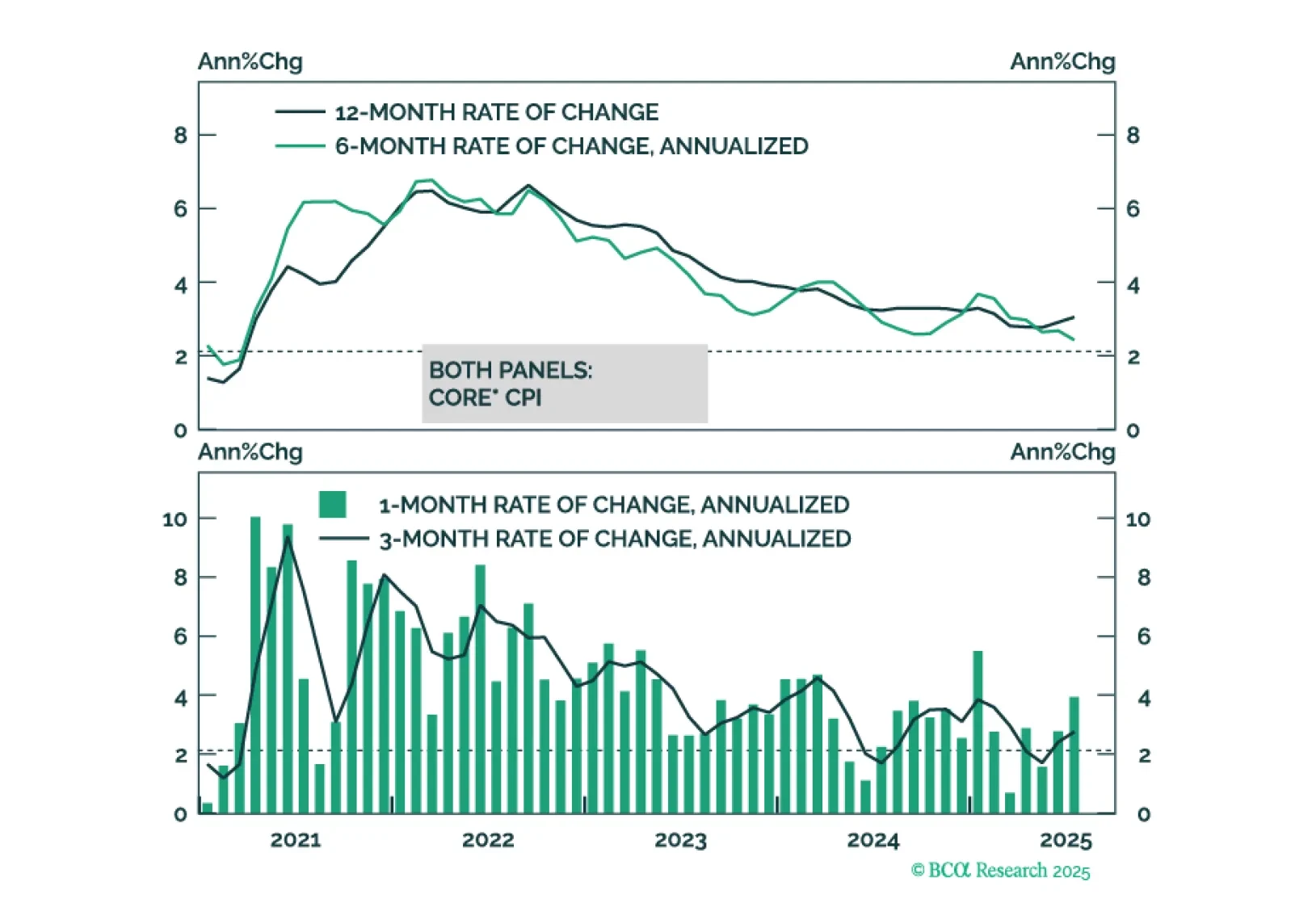

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

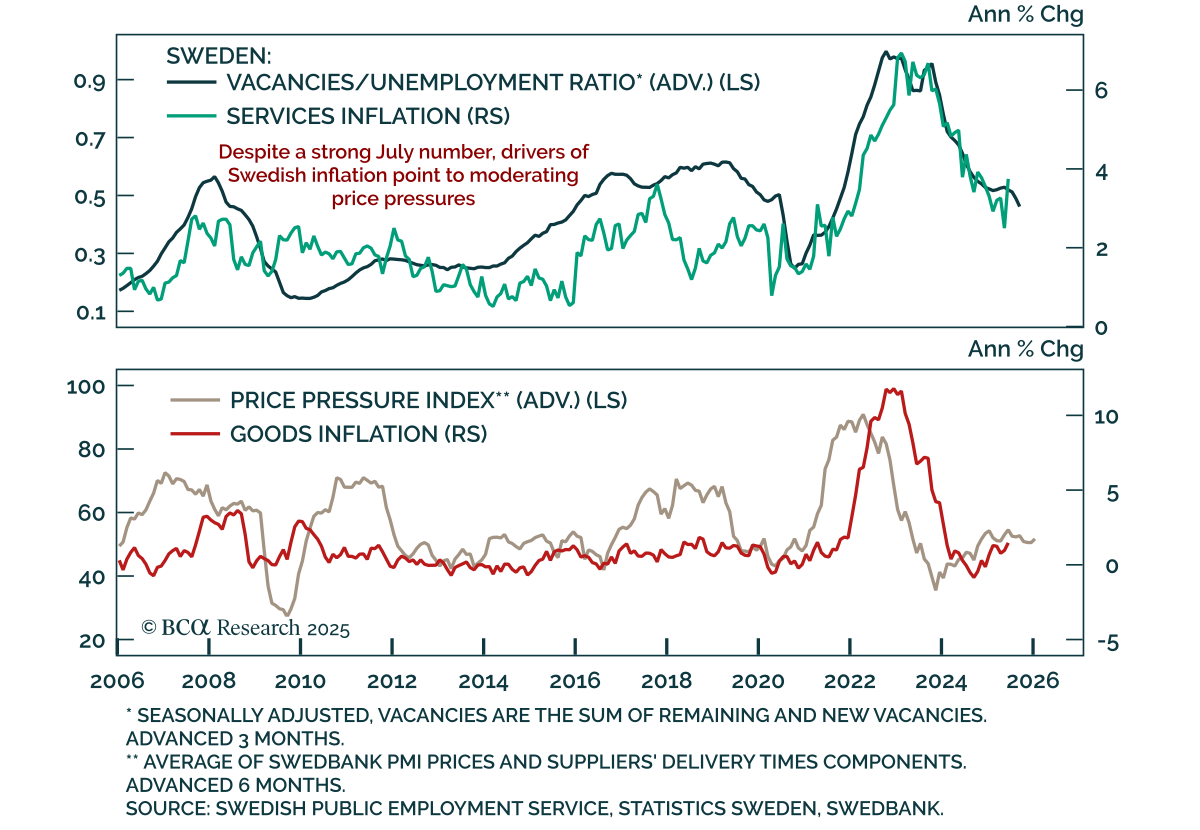

Sweden’s July inflation print came in cooler than expected, but core remains too high for an imminent Riksbank cut. CPI rose 0.8% y/y, while CPIF climbed to 3.0% and core CPIF decelerated to 3.1%, still above the Riksbank’s 2.8% July forecast and outside…

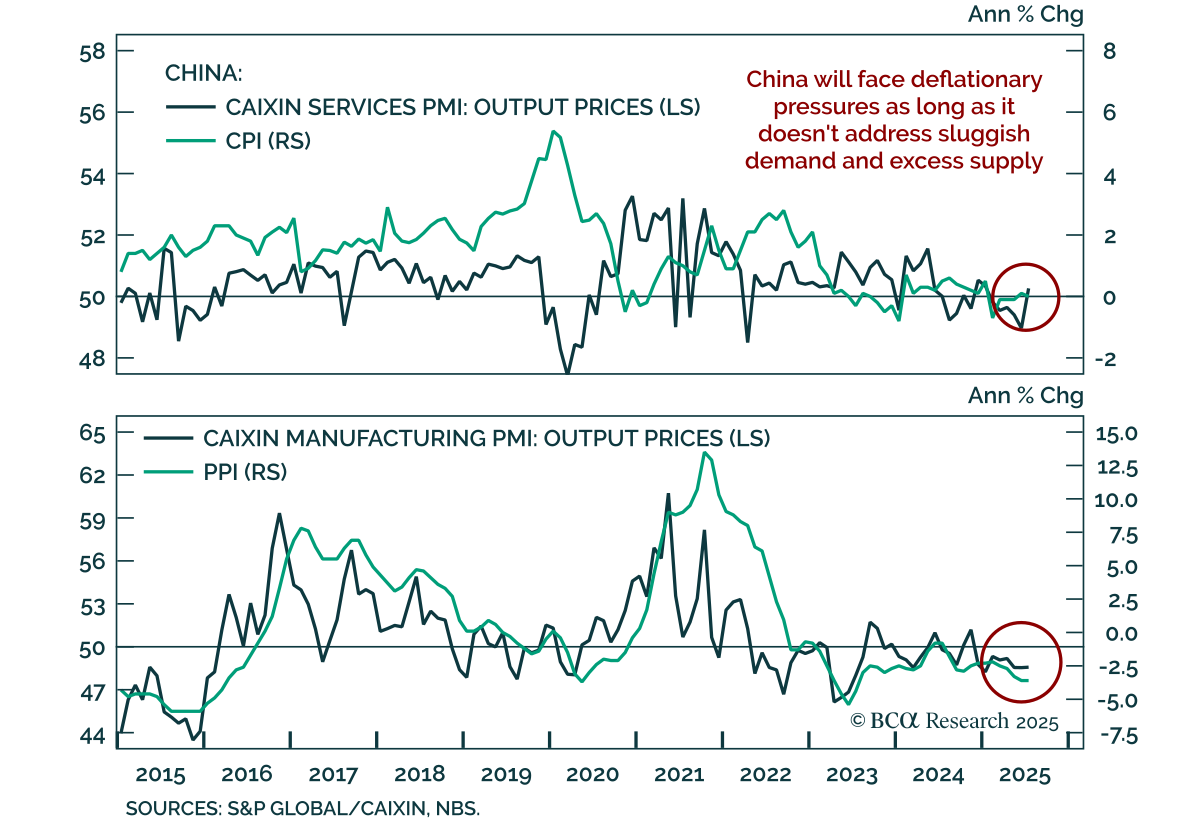

China’s July inflation data confirmed entrenched deflation, reinforcing our defensive stance on Chinese equities and overweight in onshore bonds. CPI slowed to 0% y/y from 0.1%, while factory-gate prices stayed deeply negative at -3.6% y/y. Weak…

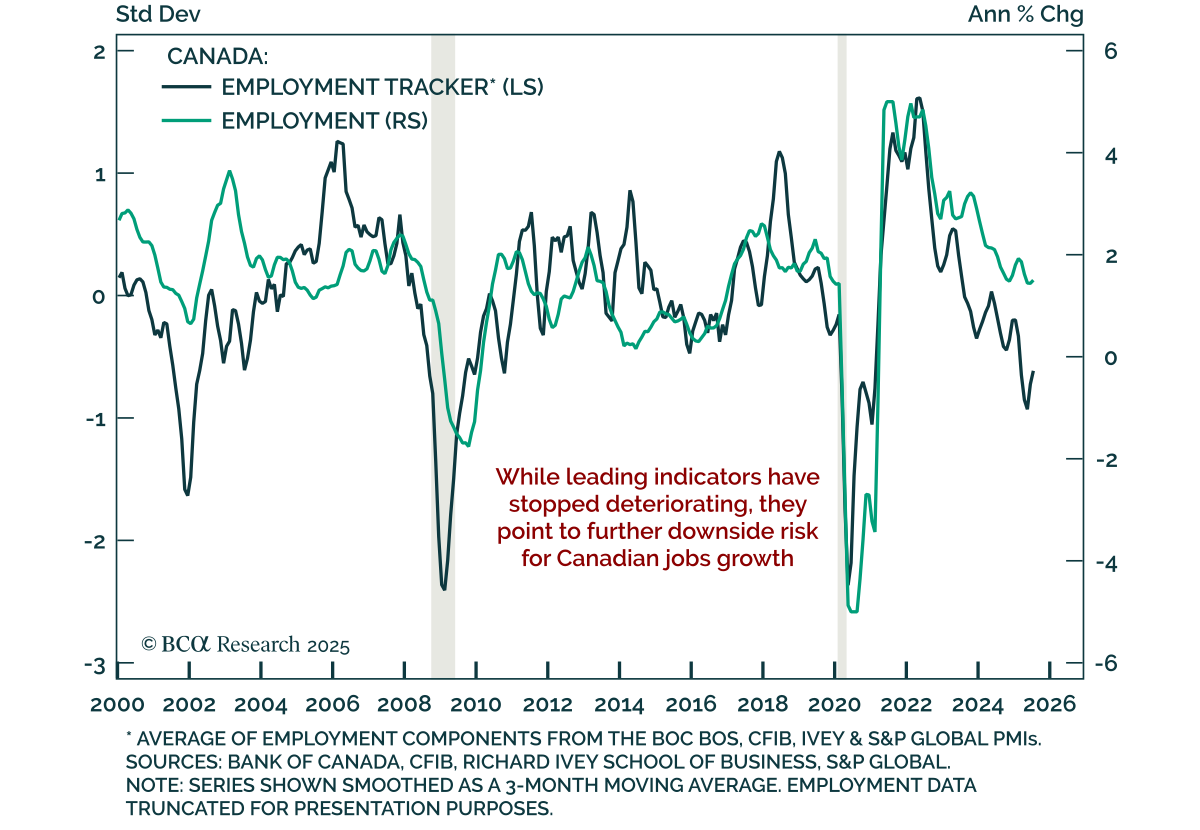

Canada’s July jobs report was mixed, but persistent slack and trade headwinds support our overweight in Canadian bonds and preference for 5s10s steepeners. Employment fell by 40.8k, driven by a 51k drop in full-time jobs, yet the unemployment rate held…

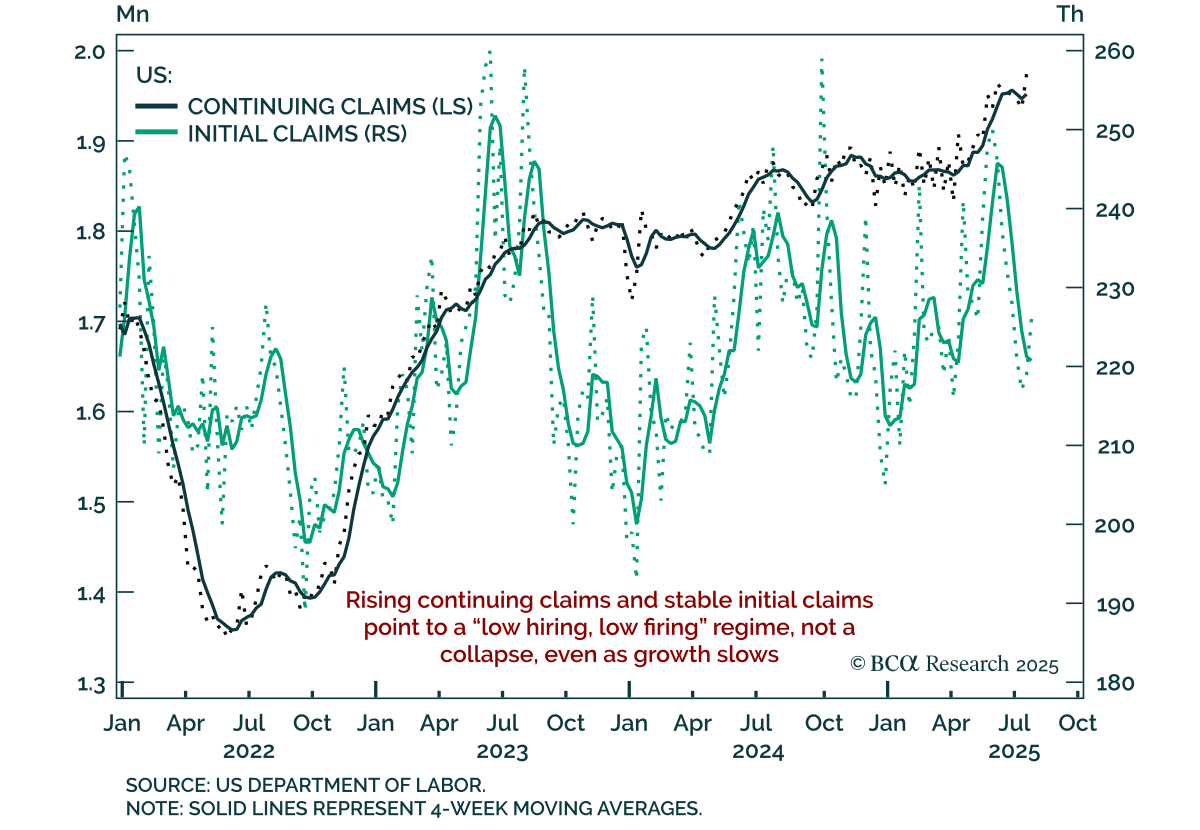

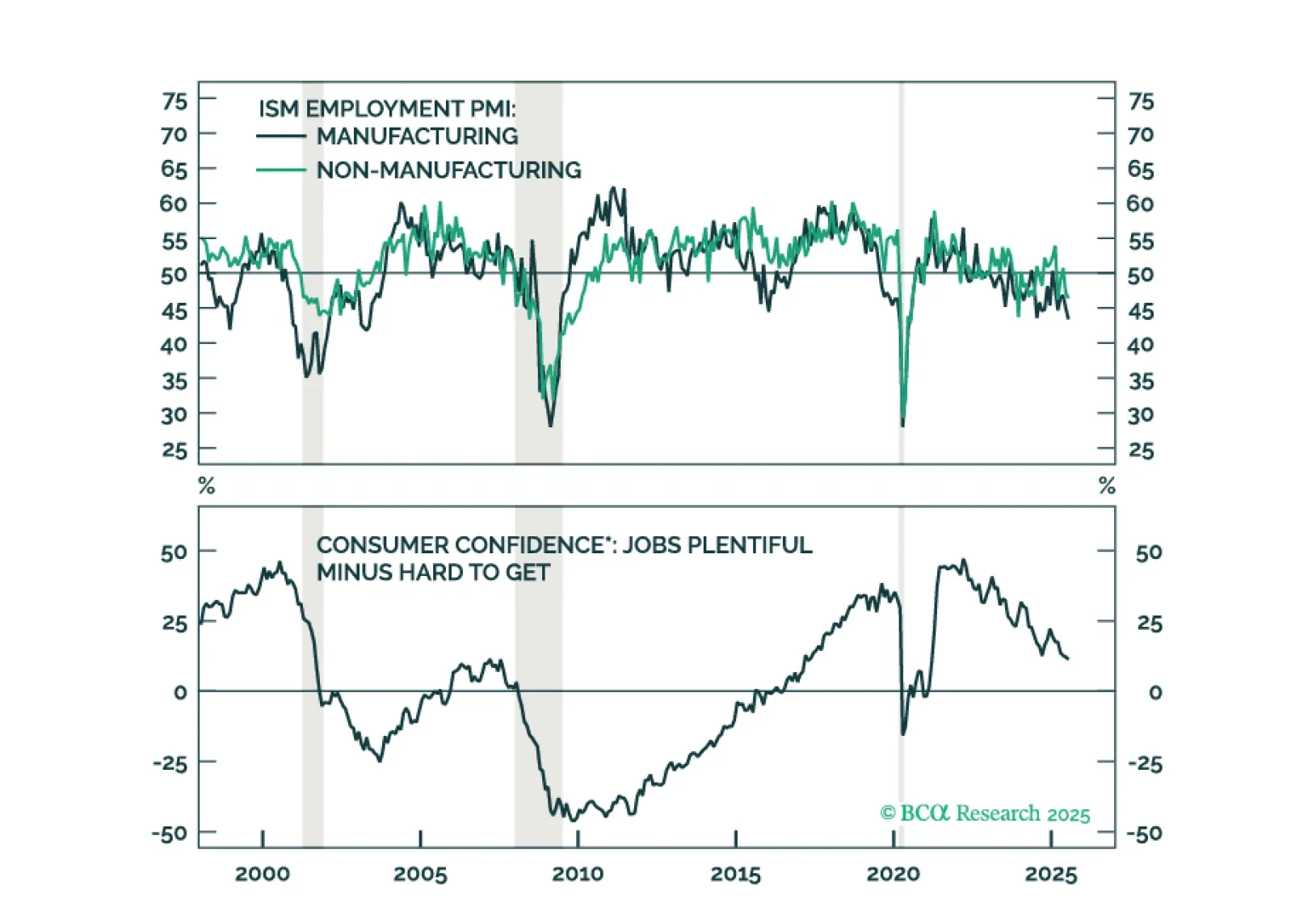

Rising continuing claims and slower job creation reinforce labor market softening, supporting a defensive stance. Continuing claims climbed to a post-COVID high of 1.974m, while initial claims held steady at 226k. Weekly claims data were closely watched…

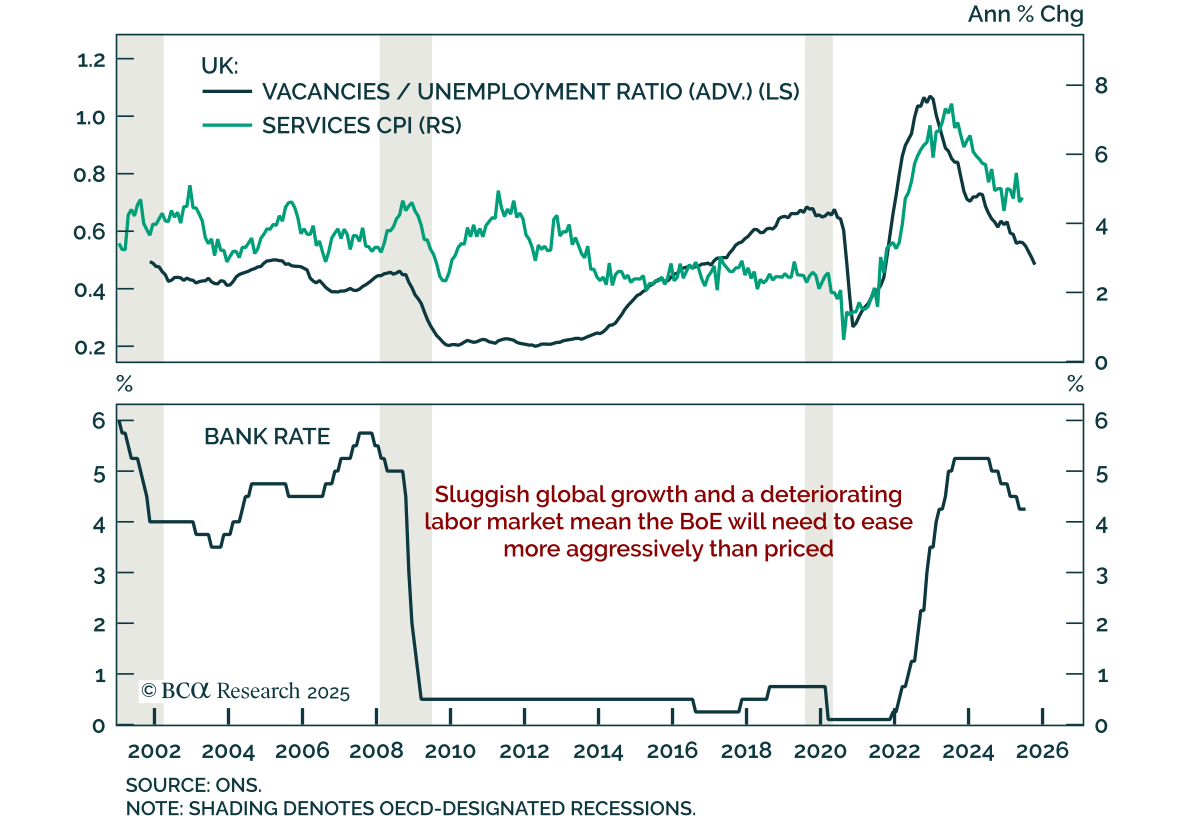

The BoE delivered a narrow rate cut to 4%, but a divided vote and fading growth momentum suggest markets are underpricing further easing. Stay overweight UK Gilts. The 5-4 split reflected concerns among dissenters about a stalling disinflation process as…

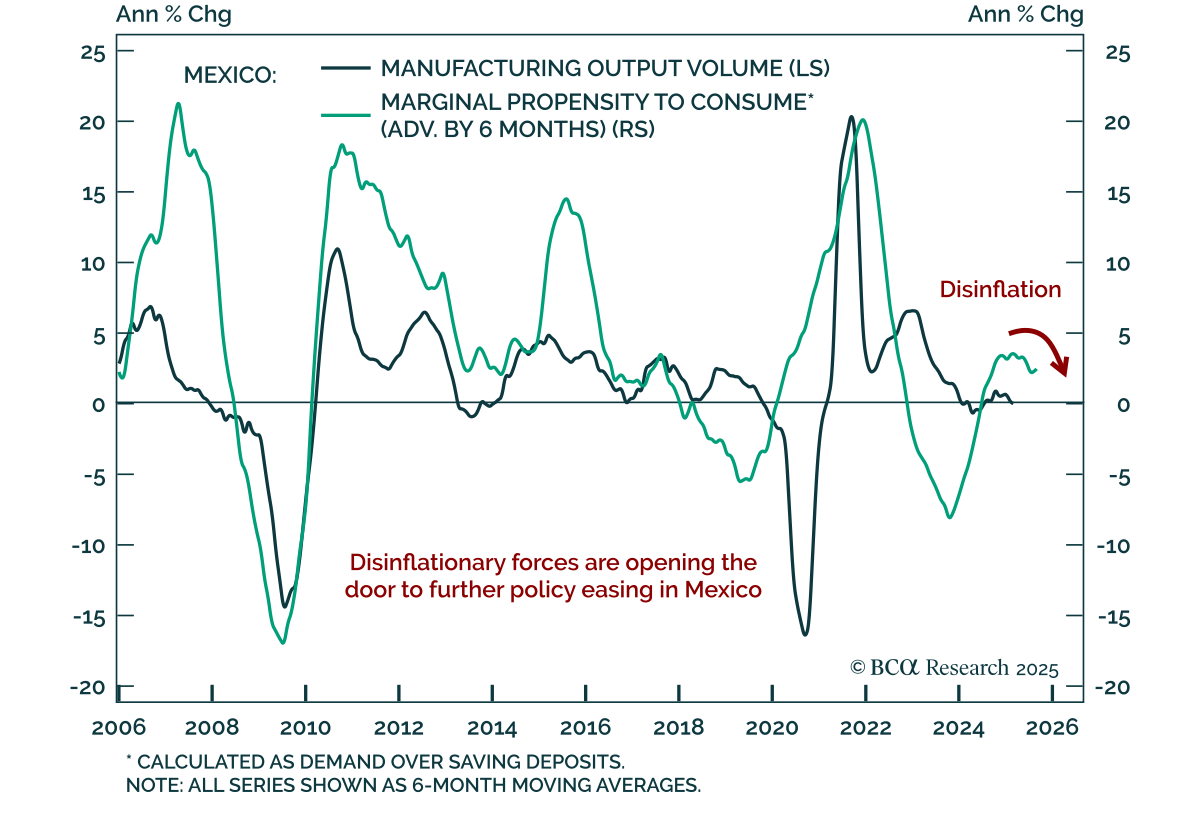

Banxico’s latest rate cut reinforces our bullish view on Mexican domestic bonds. Mexico’s central bank eased policy by another 25 basis points to 7.75%. Investors should bet on further easing. Inflation will continue falling within the target range…

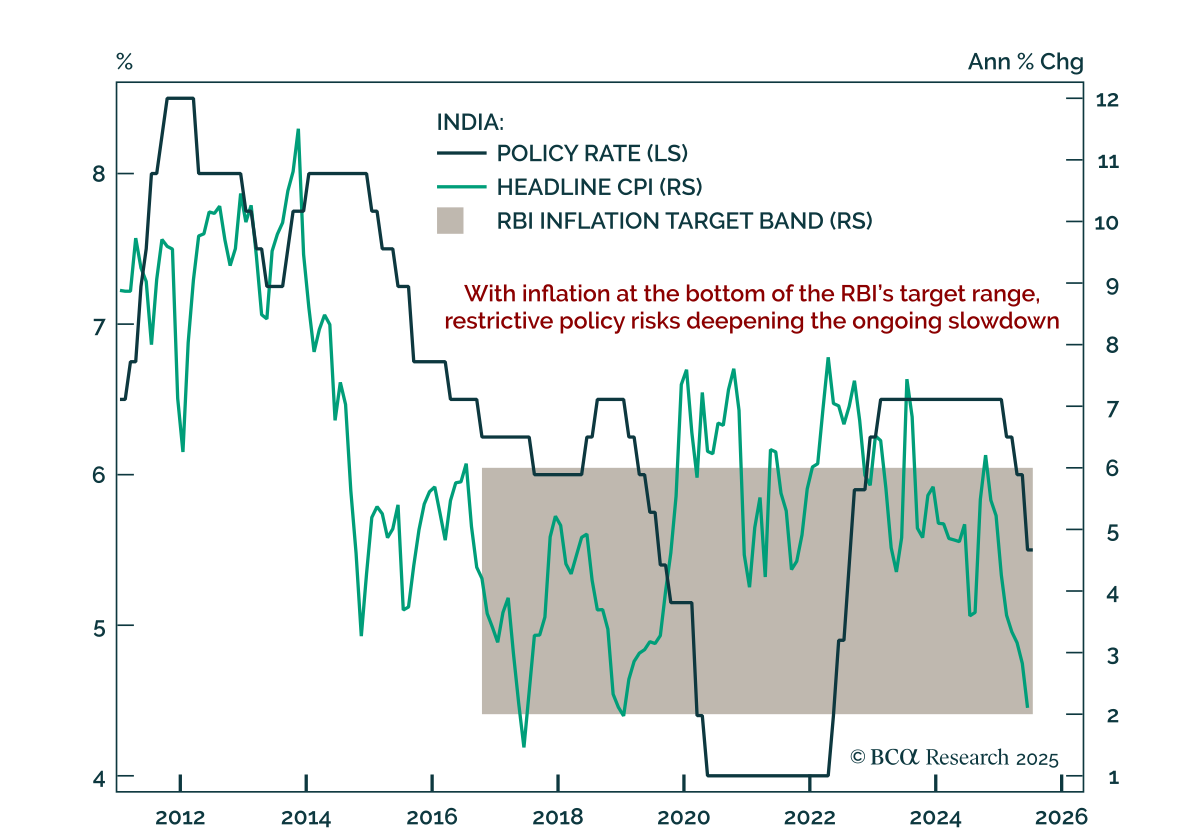

India’s central bank held rates at 5.5%, but restrictive policy, weak credit impulse, and rising external risks support further easing and a long bond position. Real lending rates remain near decade highs, and the negative credit impulse already weighs…

Our Portfolio Allocation Summary for August 2025.

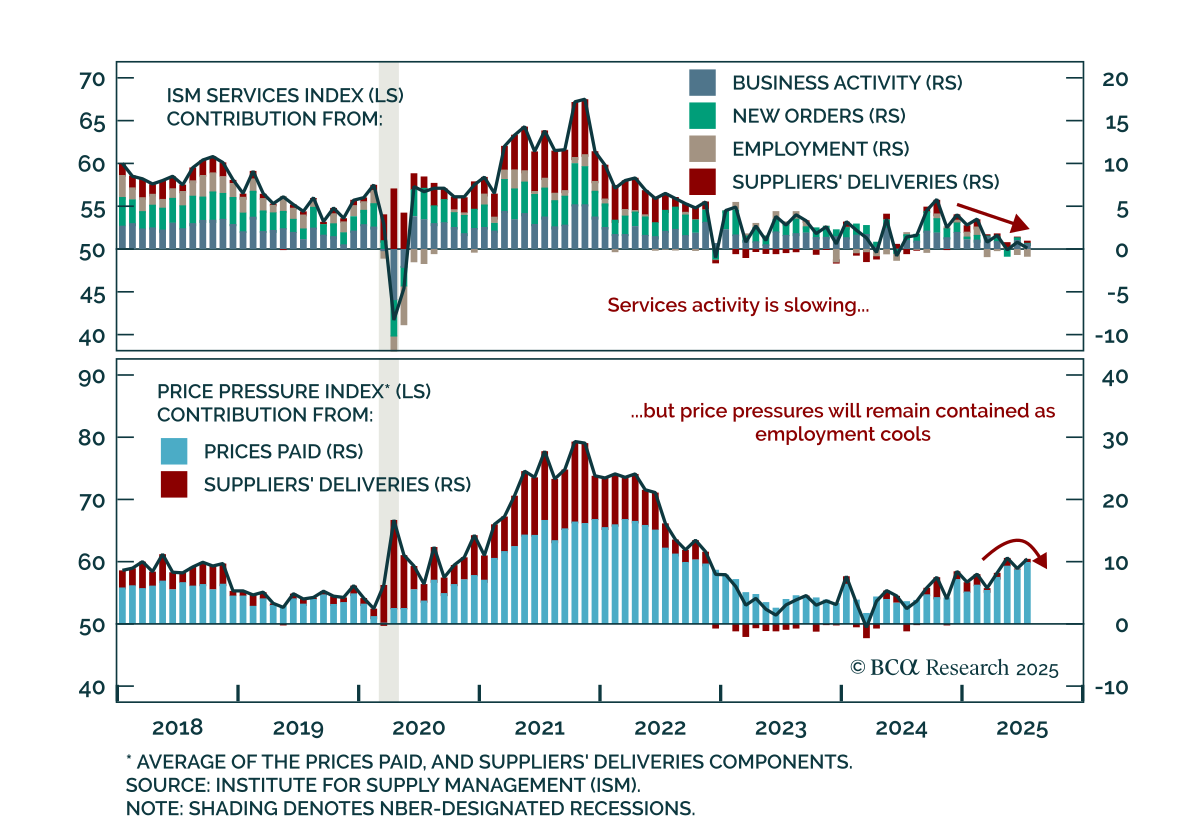

The July ISM Services report showed a stagflationary impulse, but soft labor momentum reinforces the view that price pressures remain contained. The headline index fell to 50.1 from 50.8, missing expectations. New orders softened to 50.3, while employment…