Inflation/Deflation

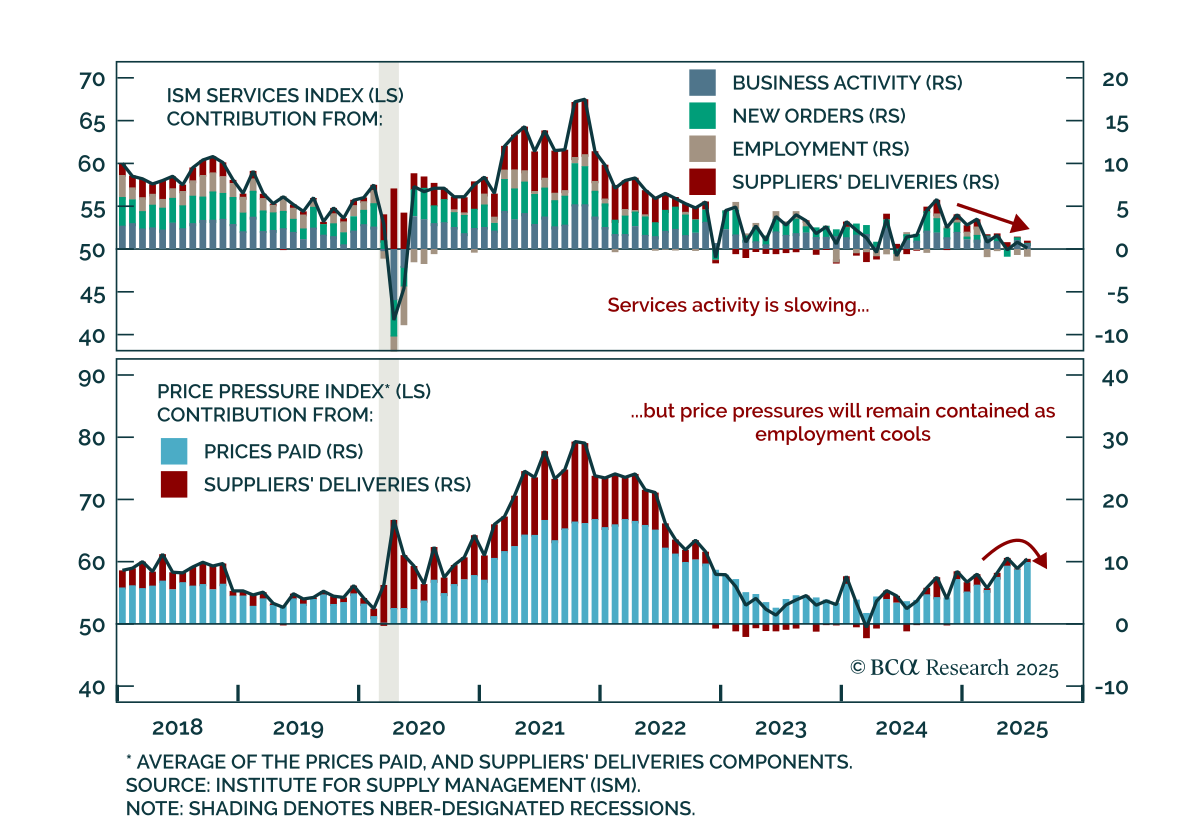

The July ISM Services report showed a stagflationary impulse, but soft labor momentum reinforces the view that price pressures remain contained. The headline index fell to 50.1 from 50.8, missing expectations. New orders softened to 50.3, while employment…

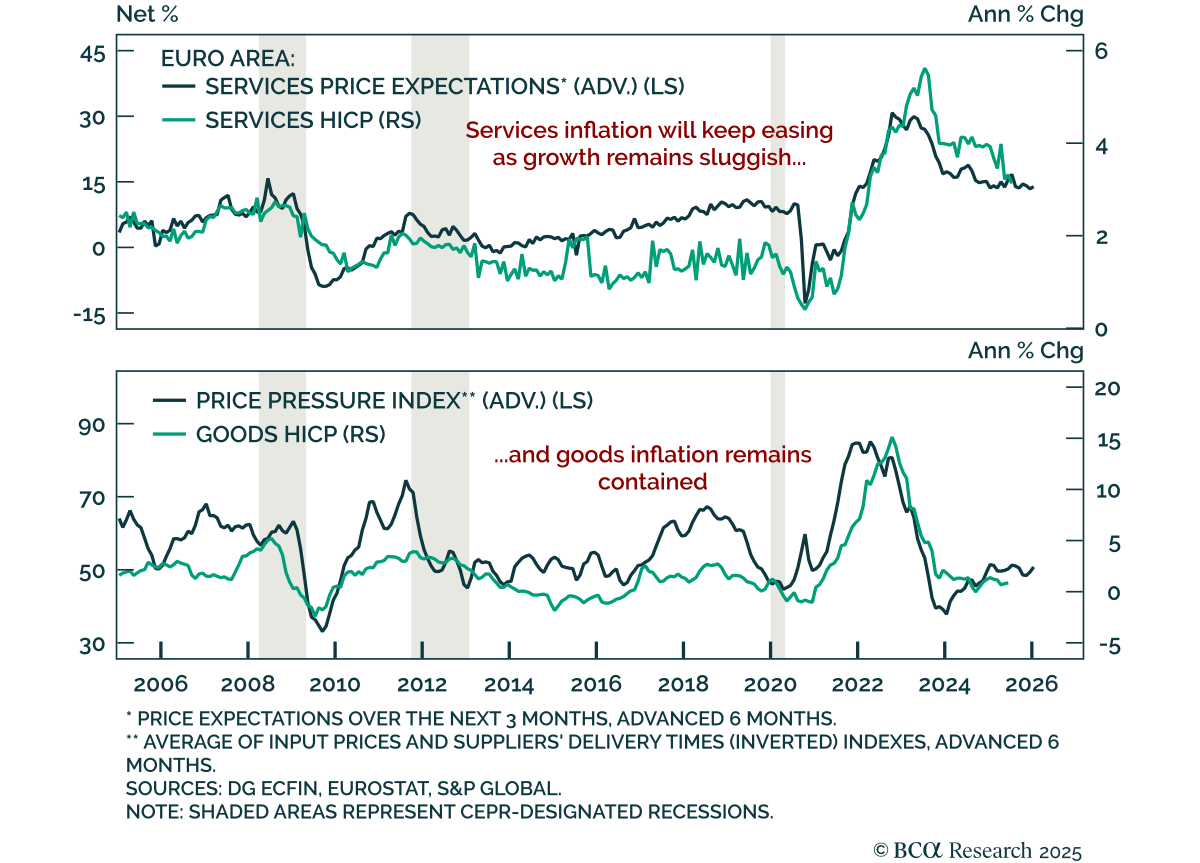

Euro area inflation held steady in July, but near-term risks remain. Long-term investors should buy on dips. Headline and core HICP came in at 2.0% and 2.3% y/y, roughly in line with expectations. The ECB held its deposit rate at 2% at its last meeting…

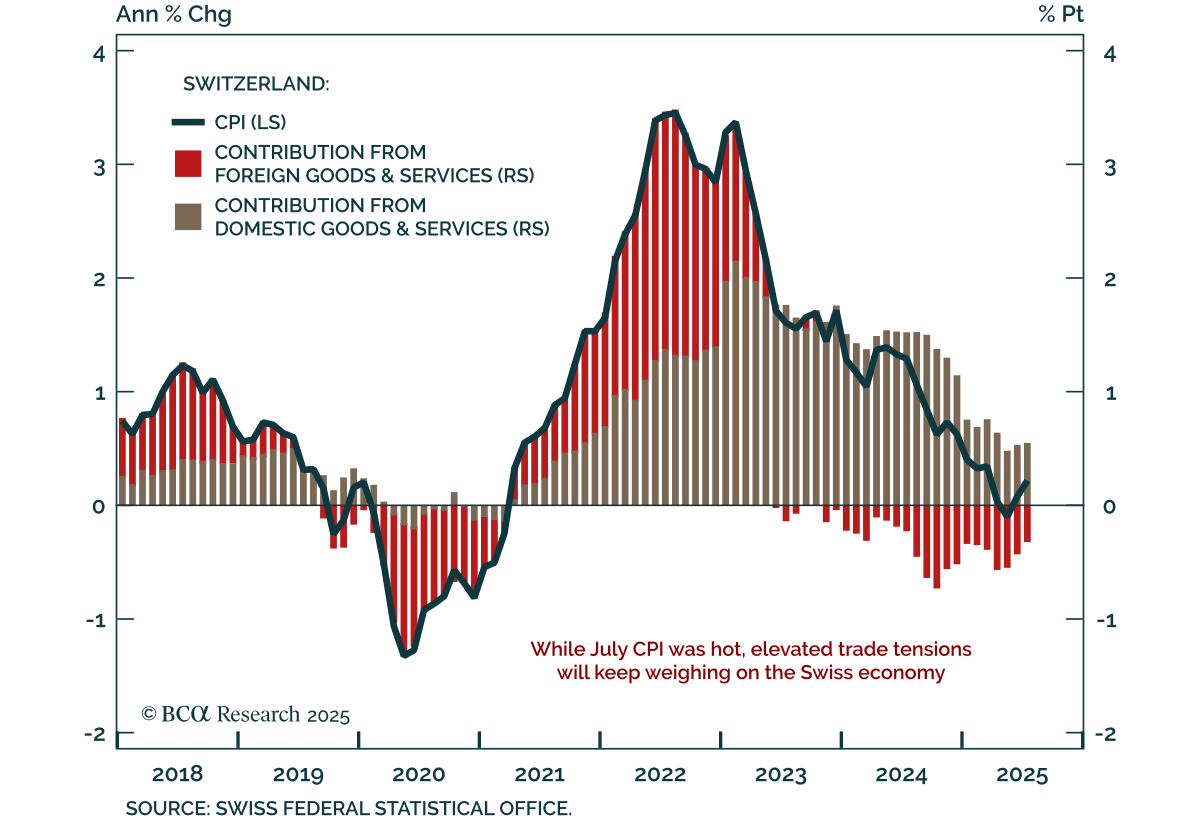

Hot July inflation does little to alter Switzerland’s near-term deflationary outlook, as soft data and trade risks support a defensive stance and preference for bonds over equities. CPI ticked up to 0.2% y/y from 0.1%, with core rising to 0.8%, both…

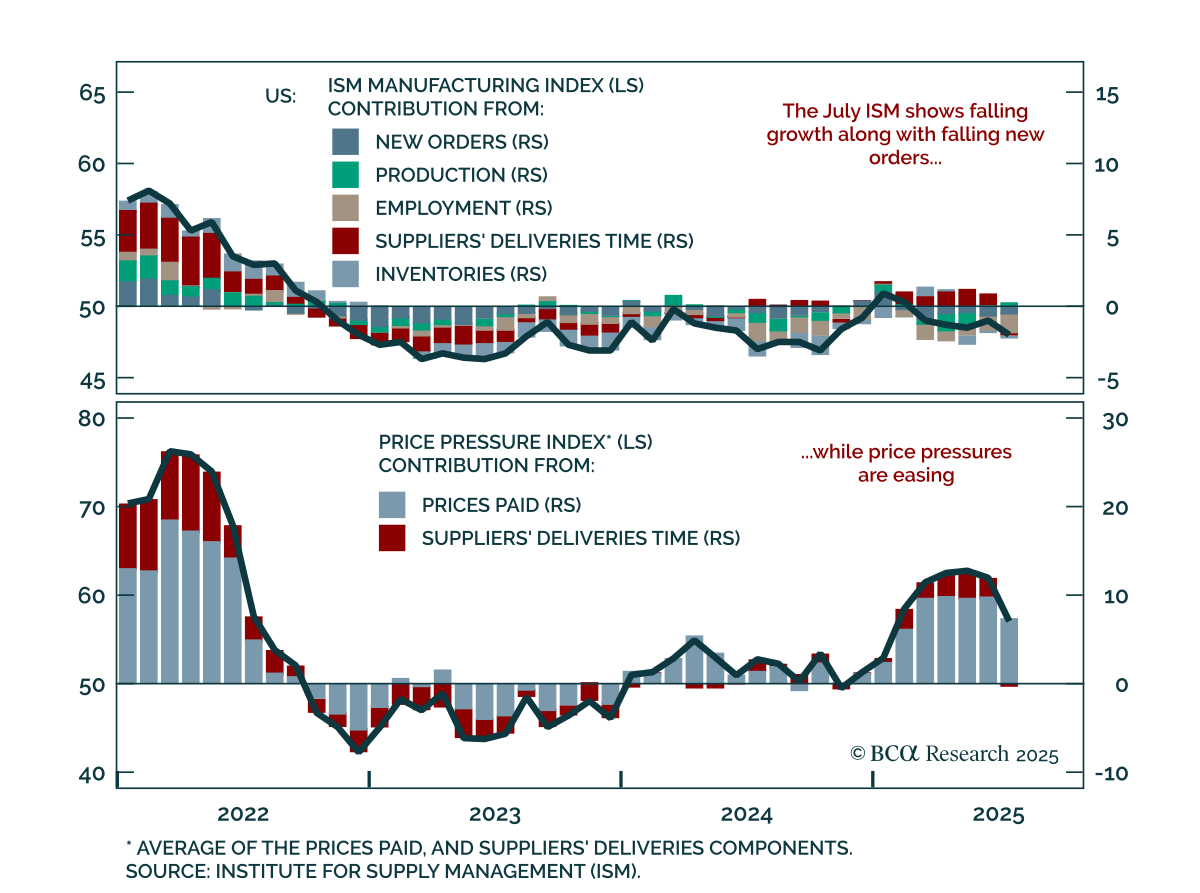

The July ISM Manufacturing miss shows weakening growth and decelerating inflation, reinforcing our long-duration stance. The index fell to 48.0 from 49.0, with only the production component contributing positively. New orders remain weak, and the drop in…

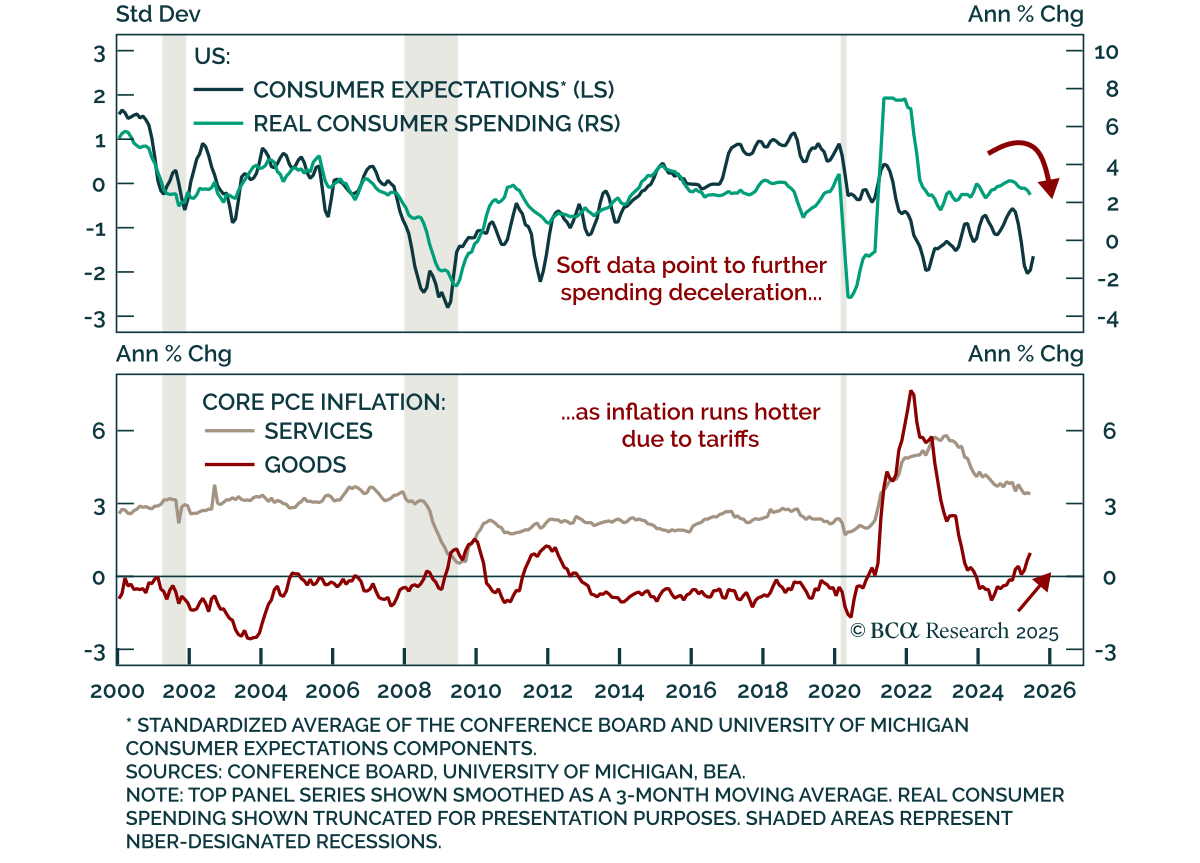

June US income and spending shows softening demand and rising goods inflation pressure, reinforcing our long-duration stance. Real personal spending only rose 0.1% m/m, in line with expectations. Personal income increased 0.3% m/m, but real income…

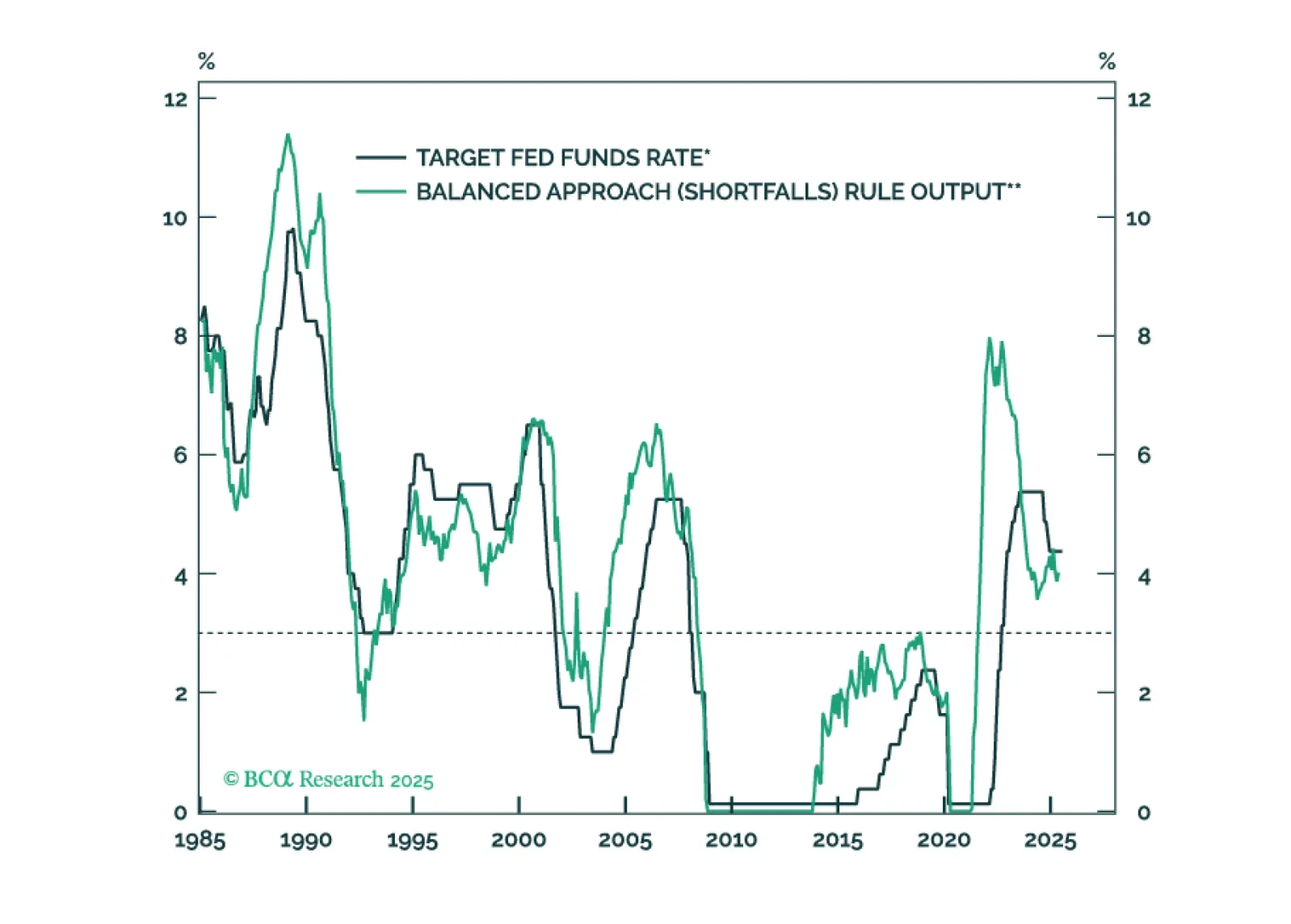

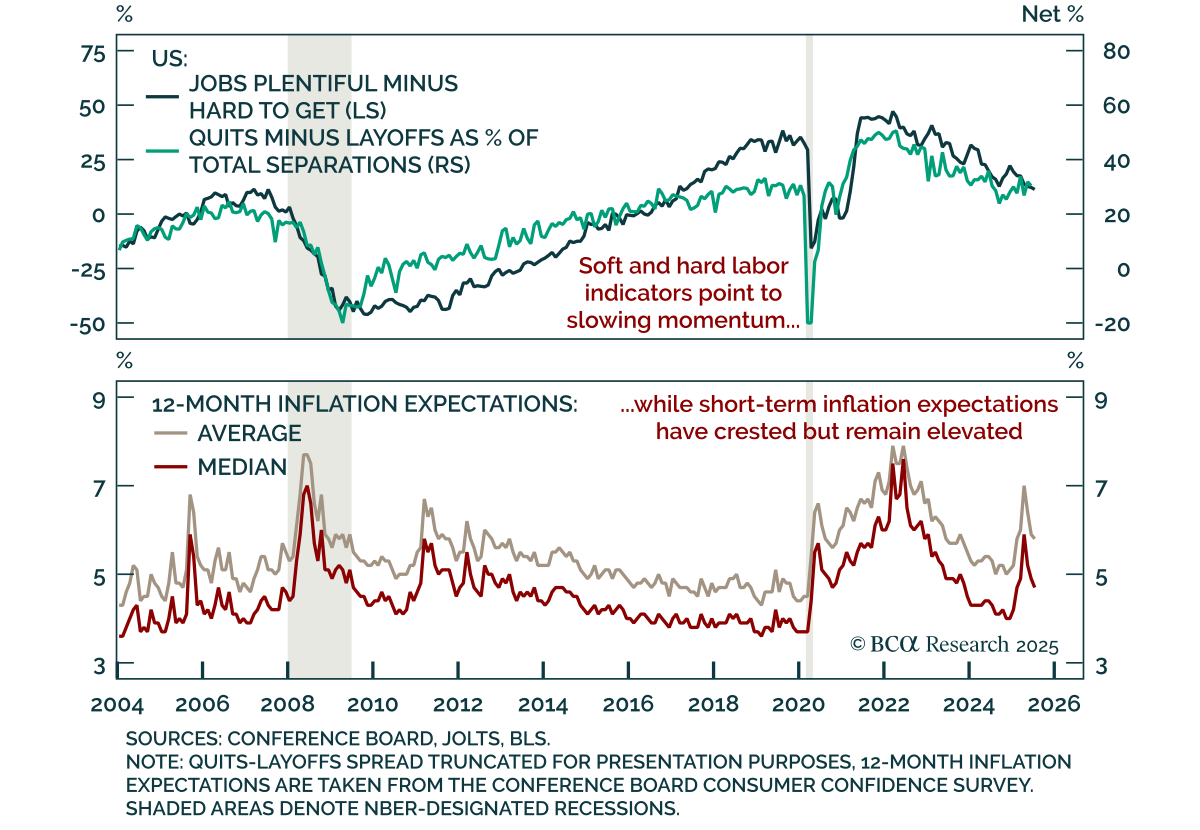

The Fed will keep rates on hold until the unemployment rate forces its hand.

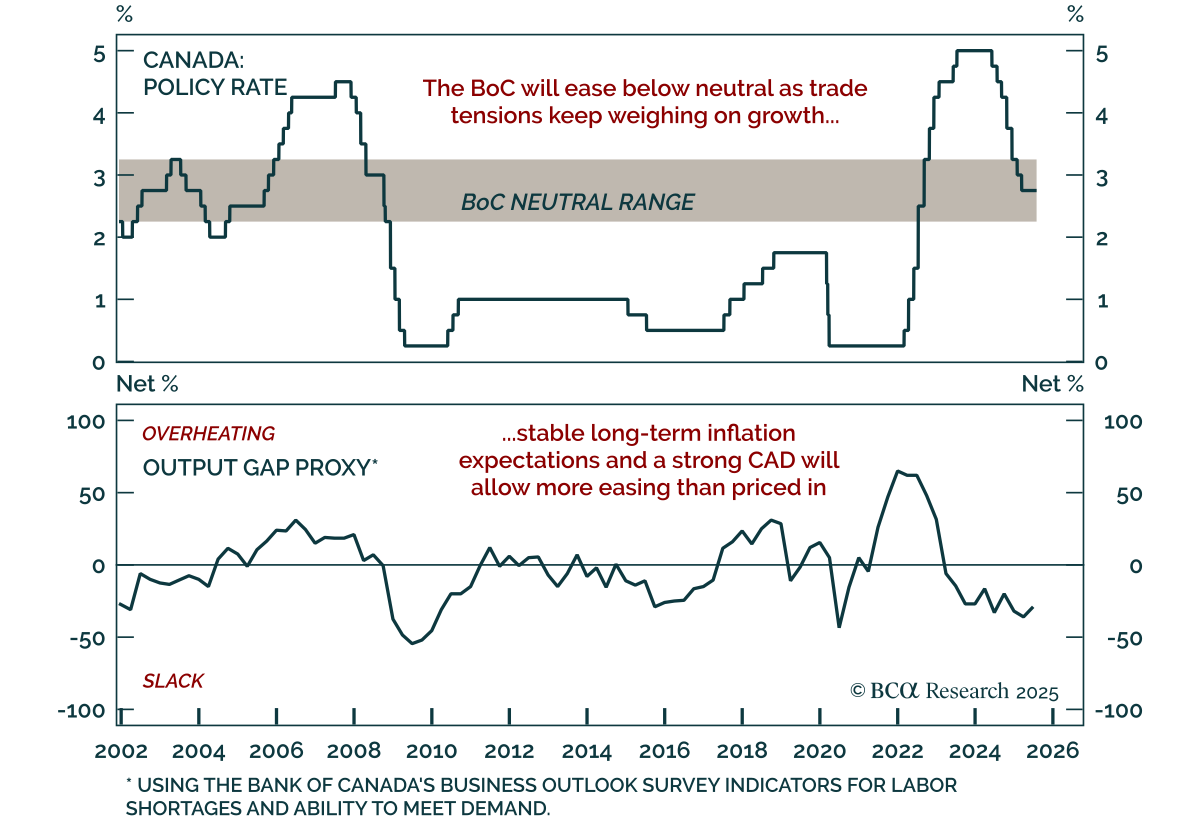

The BoC held rates at 2.75% for a third consecutive meeting, but a weak growth outlook and contained inflation reinforce our overweight in Canadian bonds. With policy within the 2.25%–3.25% neutral range, the BoC remains comfortable waiting for clarity…

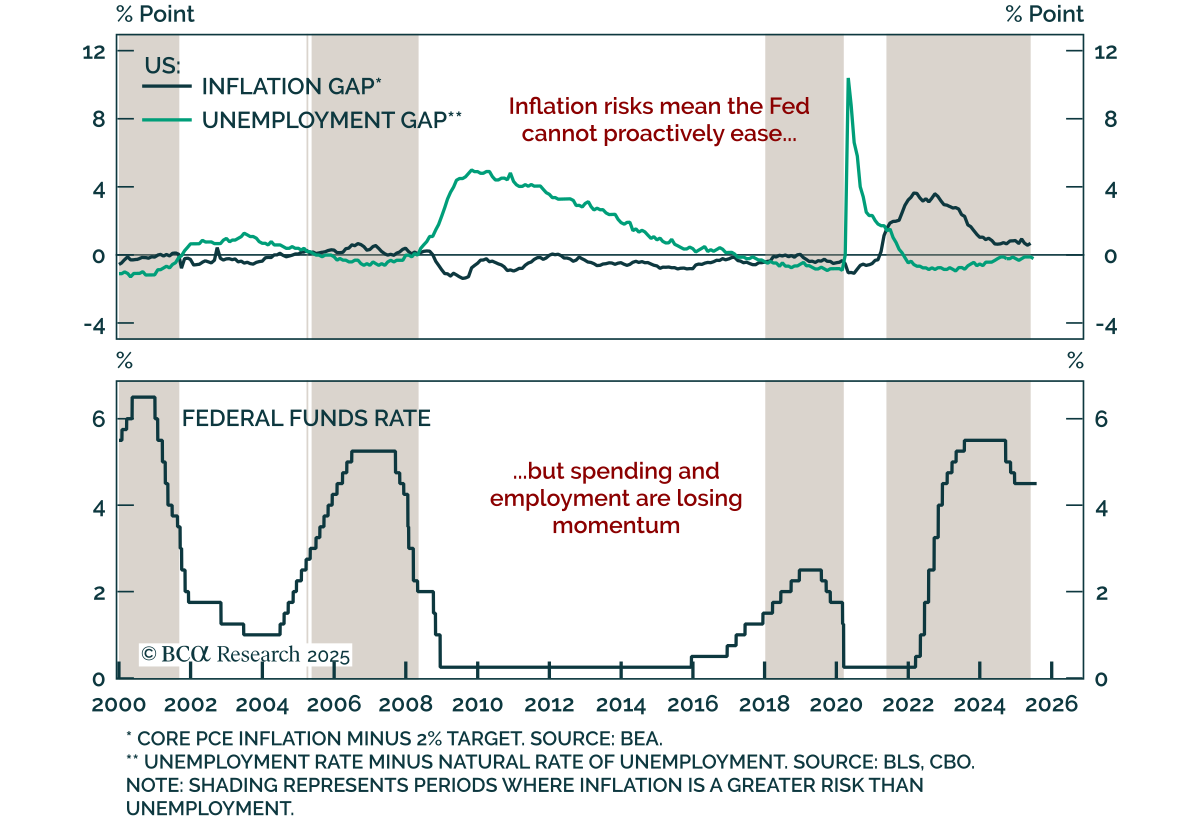

The Fed held rates steady for a fifth straight meeting, with a divided FOMC and resilient growth keeping policy on hold, supporting our long-duration stance. The target range remains at 4.25%–4.50%, with the statement reflecting only a modest downgrade to the…

The July Conference Board Consumer Confidence report showed improved expectations but weaker current conditions, reinforcing our defensive stance and preference for downside protection. The headline index rose to 97.2 from a revised 95.2 on the back of better…

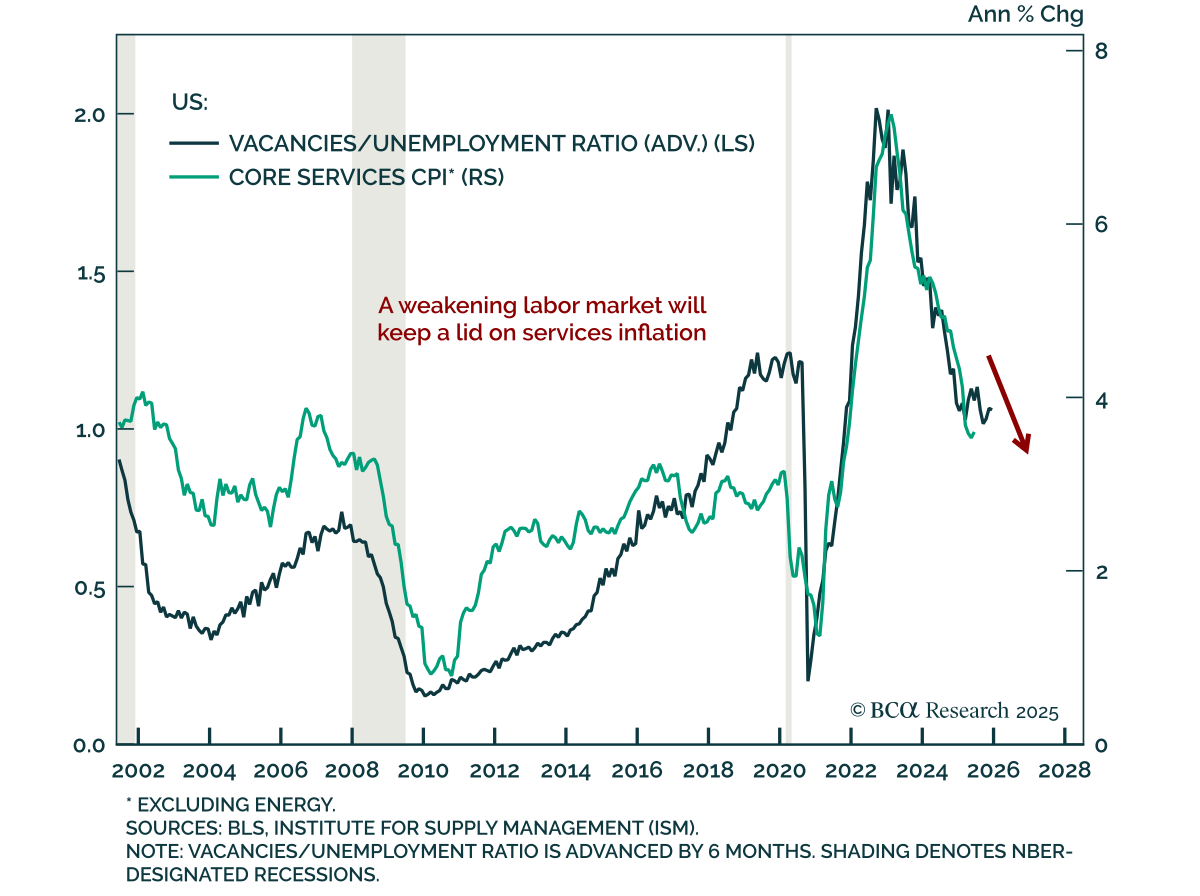

The June JOLTS report showed further weakening in US labor market momentum, reinforcing our overweight duration stance and preference for steepeners. Job openings fell more than expected to 7.4m from a downwardly revised 7.7m, while quits declined to 3.1m and…