Inflation/Deflation

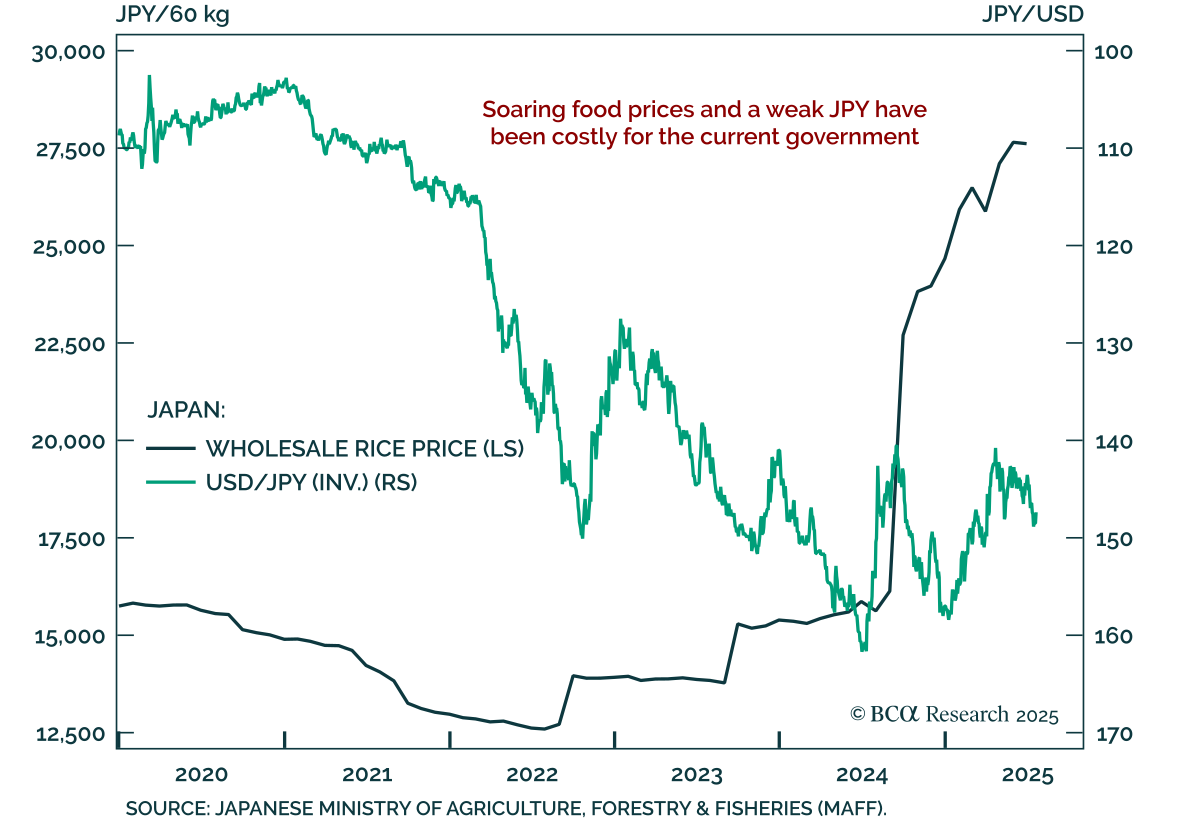

The Upper House loss of Japan’s ruling coalition reflects growing political uncertainty, reinforcing our underweight in JGBs and bullish stance on the yen. The LDP-led ruling coalition has lost control of both houses of parliament for the first time…

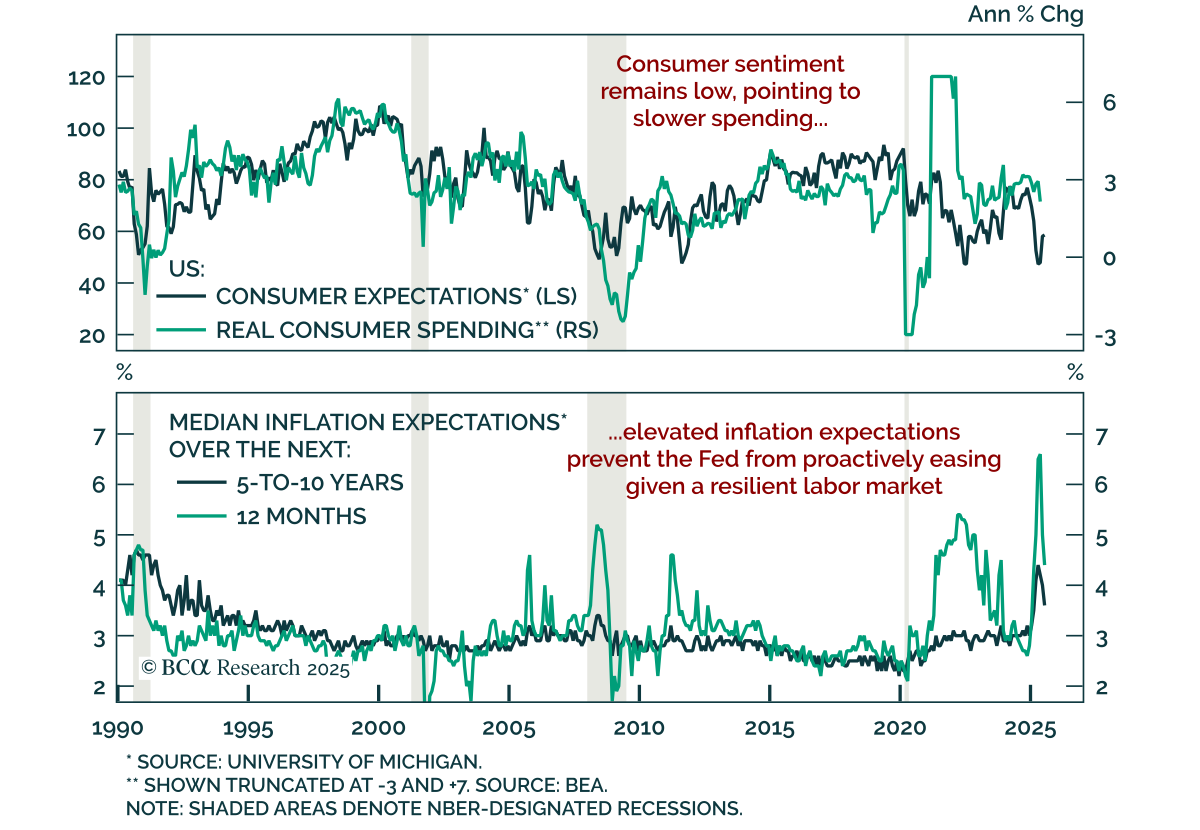

Consumer sentiment improved modestly in July, but remains at levels that still point to subdued spending, reinforcing our defensive stance. The preliminary University of Michigan index rose to 61.8 from 60.7 in June. Expectations edged up to 58.6, while…

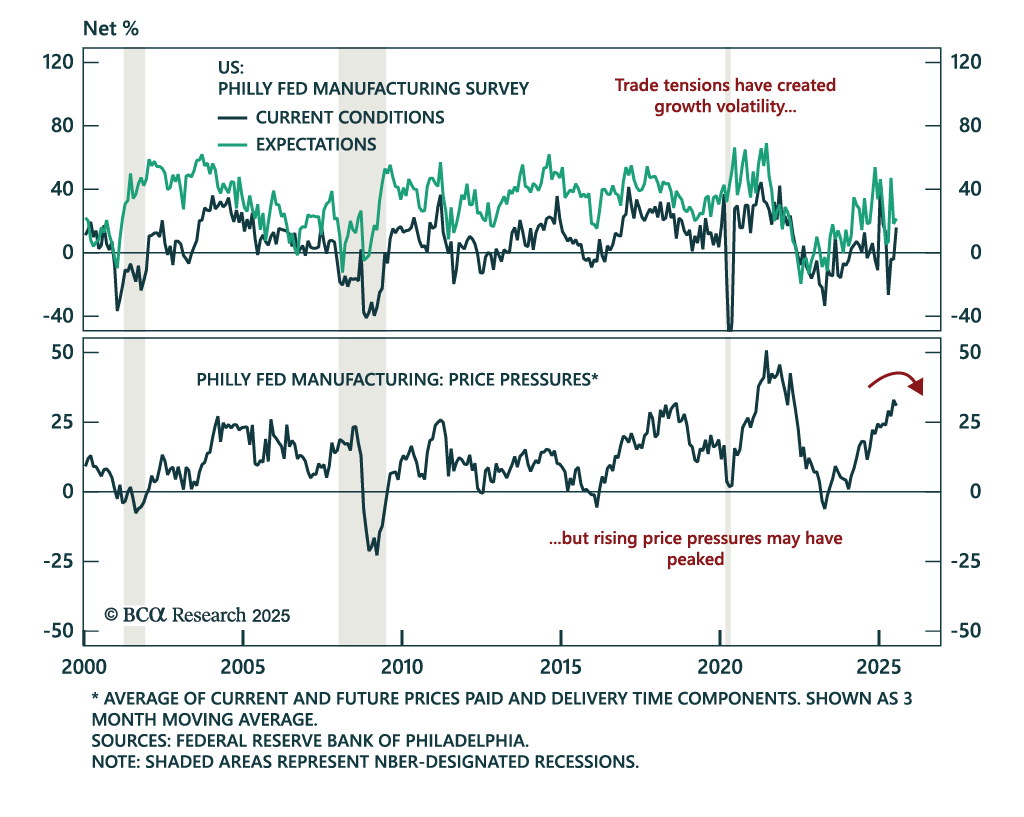

The July Philly Fed beat expectations with broad improvement in activity, but low growth, inventory buildup and margin pressure remains a risk for equities. The headline index rose to 15.9 from -4.0 in June. New orders, shipments, and employment all…

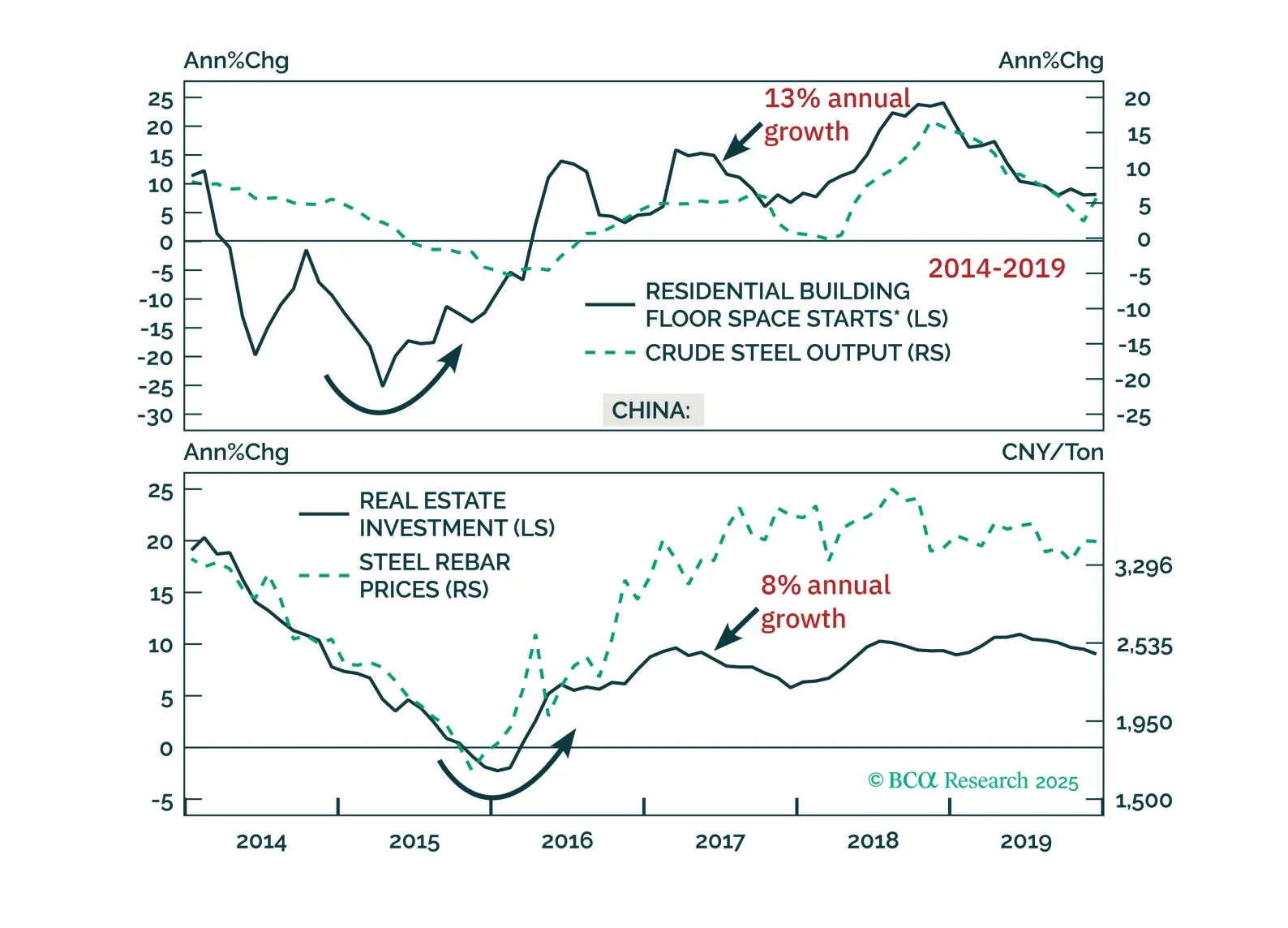

Beijing’s supply-side push faces steeper hurdles than in 2016. With limited demand support and tighter constraints on cutting capacity, today’s reforms are unlikely to pack the same punch.

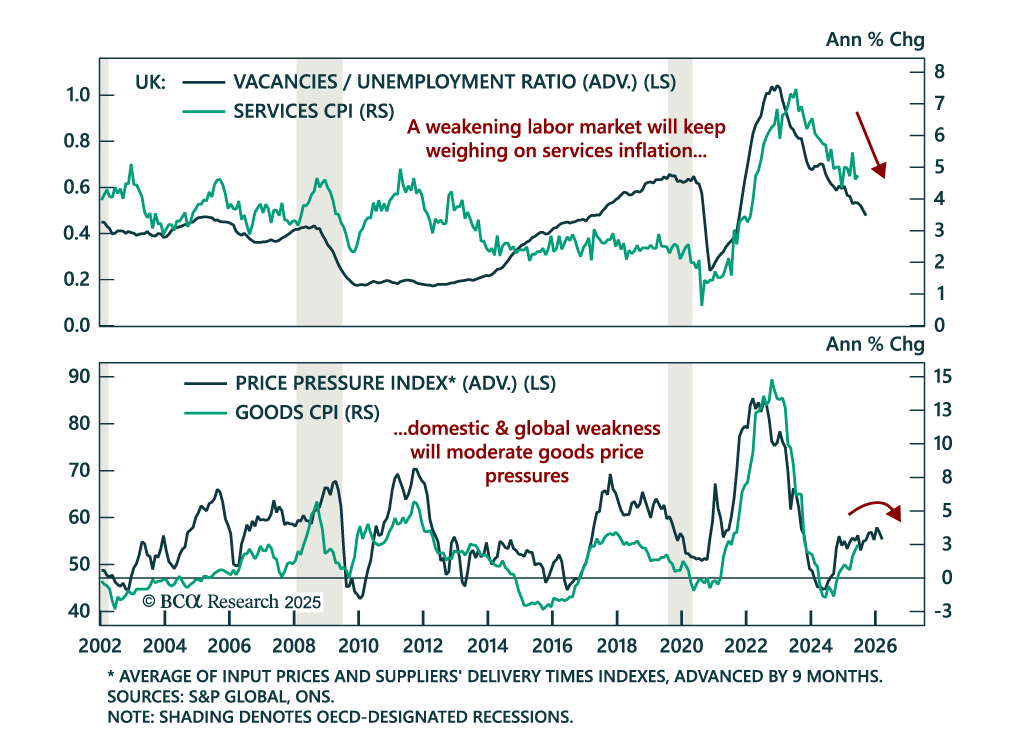

June UK CPI surprised to the upside, but weakening leading indicators point to disinflation ahead. Stay overweight Gilts. Headline inflation accelerated to 3.6% y/y from 3.4%, and core rose to 3.7% from 3.5%. Services inflation held at 4.7%, also above…

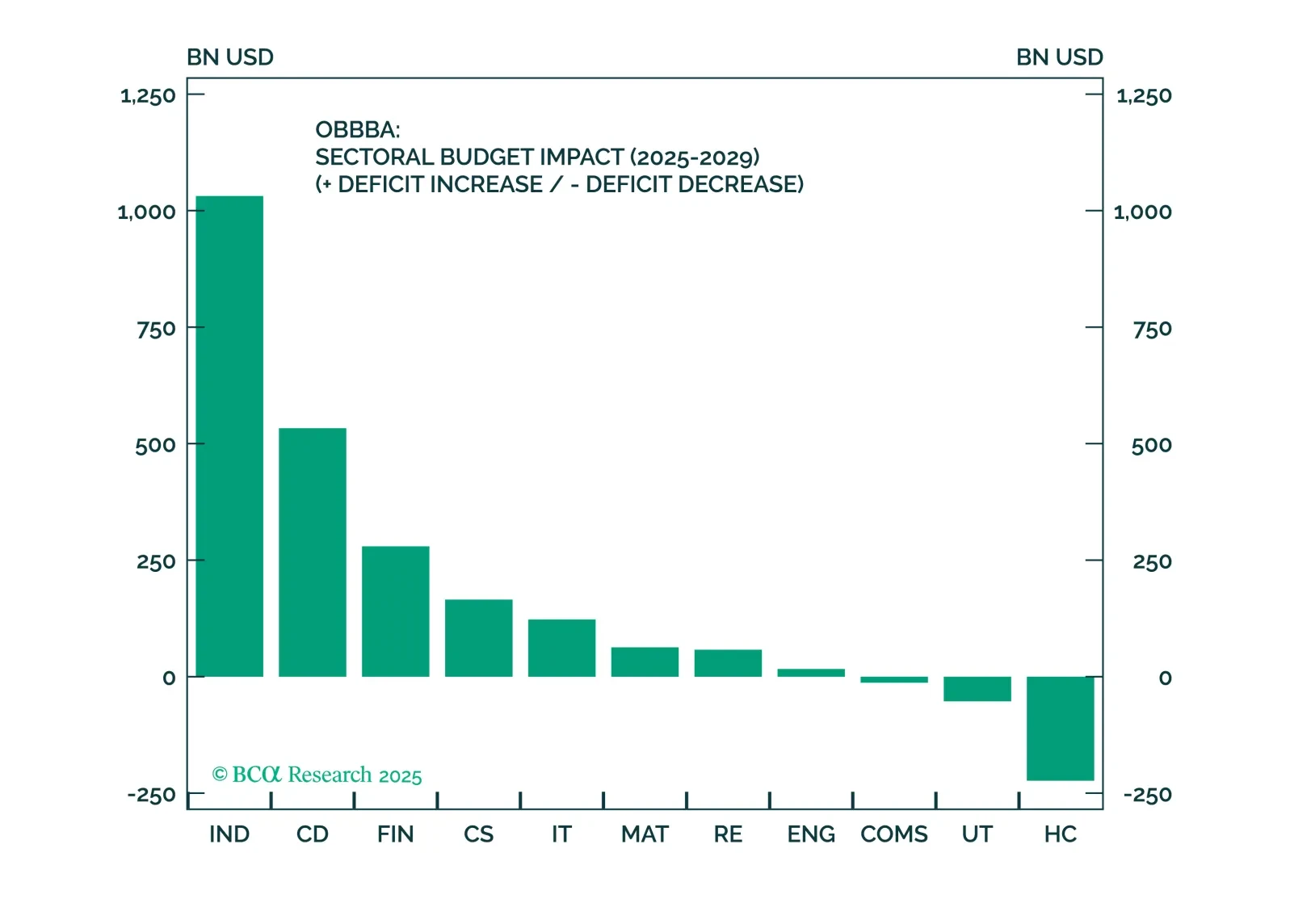

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

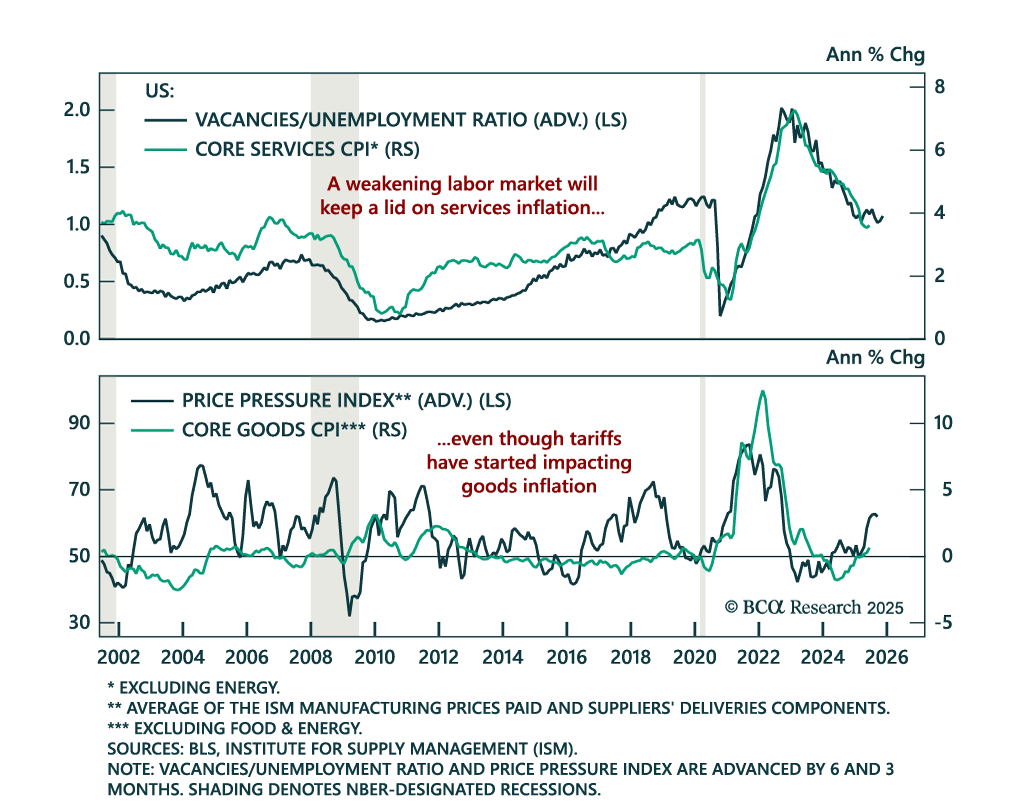

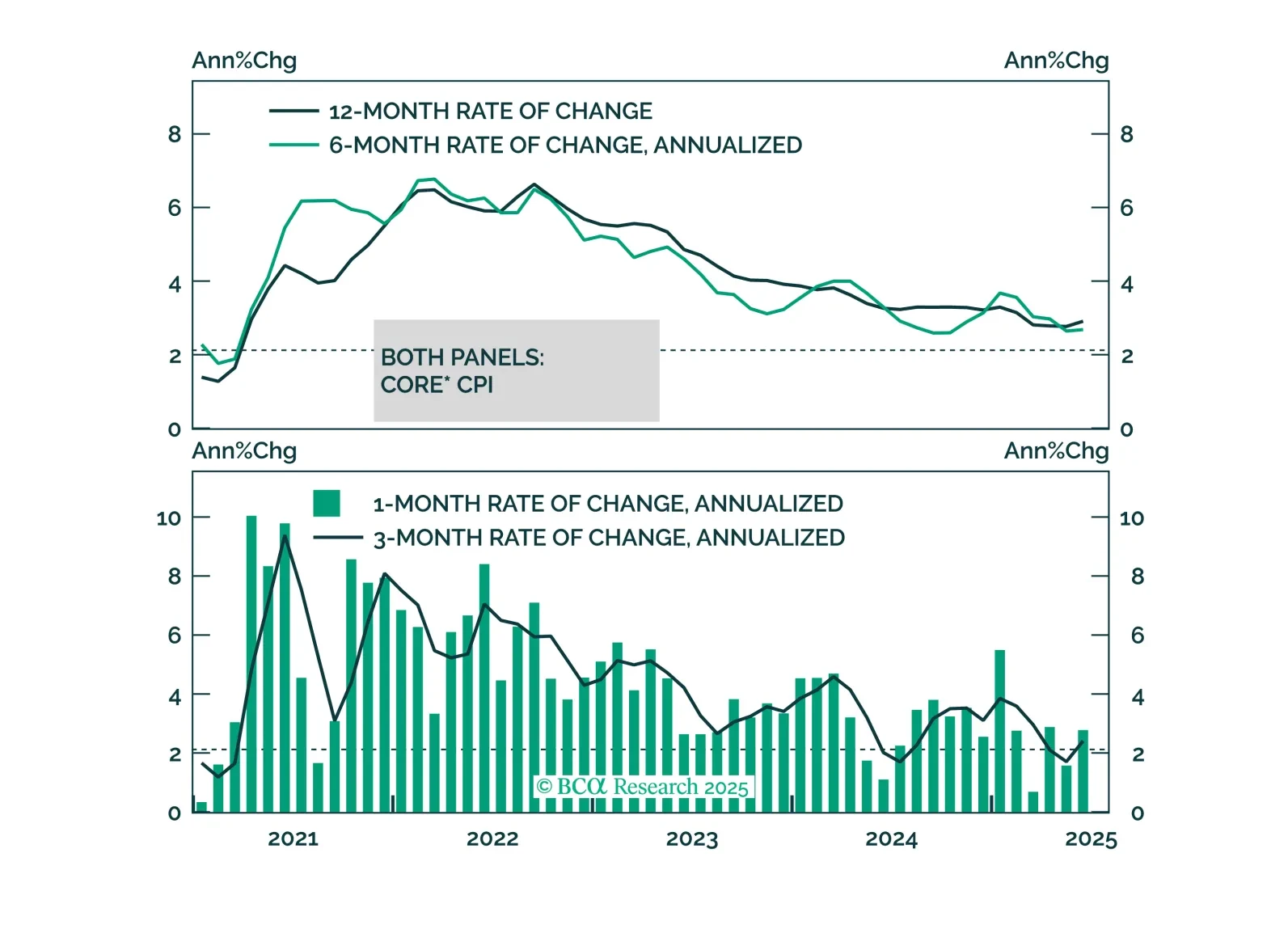

June CPI was broadly in line with expectations, with tariff passthrough building in goods but broader inflation pressures likely to remain contained. Headline inflation came in slightly above expectations at 2.7% y/y (0.3% m/m), while core matched estimates…

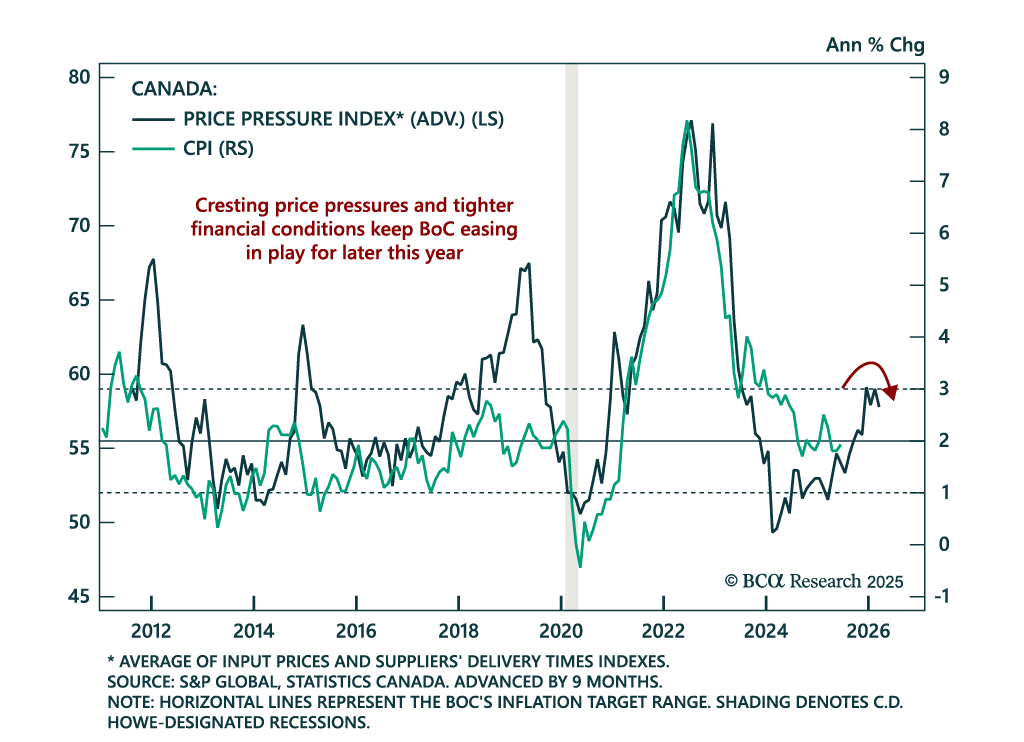

Canada’s inflation re-acceleration makes a BoC July cut unlikely, but softening growth and tight financial conditions keep easing on the table. June headline inflation rose to 1.9% y/y from 1.7%, roughly in line with expectations. Core trim and median…

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.

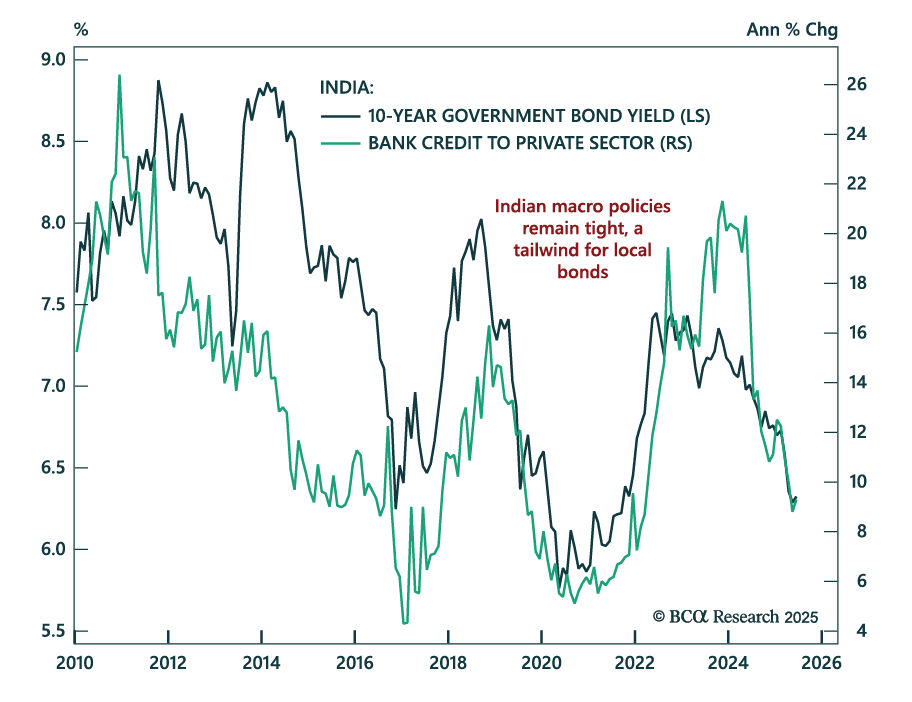

With inflation at a six-year low and restrictive policy weighing on growth, our EM strategists remain long Indian bonds and underweight equities. Headline CPI fell to 2.1% y/y, largely driven by lower food prices, bringing inflation to the lower bound of the…