Inflation/Deflation

Highlights US Treasuries: The uptrend in US Treasury yields has more room to run. However, the primary driver is starting to shift from increased inflation expectations to higher real yields amid greater confidence on the cyclical US economic outlook. Fed Outlook: It is still too soon to expect the Fed to begin signaling a move to turn less accommodative. However, rising realized US inflation amid dwindling spare economic capacity will make the Fed more nervous about its ultra-dovish policy stance in the second half of 2021. This will trigger a repricing of the future path of US interest rates embedded in the Treasury curve, but a Taper Tantrum repeat will be avoided. US Duration: Maintain below-benchmark US duration exposure, with the 10-year Treasury yield likely to soon test the 1.5% level. Feature Chart 1A Cyclical Rise In Global Bond Yields

A Cyclical Rise In Global Bond Yields

A Cyclical Rise In Global Bond Yields

The selloff in global government bond markets that began in the final few months of 2020 has gained momentum over the past few weeks. The benchmark 10-year US Treasury yield now sits at 1.37%, up 45bps so far in 2021, while the 30-year Treasury yield is at a six-year high of 2.22%. Yields are on the move in other countries, as well, with longer-maturity yields moving higher in the UK, Canada, Australia, New Zealand – even Germany, where the 30yr is now back in positive yield territory at 0.20%, a 34bp increase over the past month alone. The main reason for this move higher in yields can be summed up in one word: “optimism”. Economic growth expectations are improving according to investor surveys like the global ZEW, which is a reliable leading indicator of global bond yields (Chart 1). Falling global COVID-19 case numbers with rising vaccination rates, combined with very large US fiscal stimulus measures proposed by the Biden administration, have given investors hope that a return to some form of pre-pandemic economic normalcy can be achieved later this year. That means faster global growth and a risk of higher inflation, both of which must be reflected in higher bond yields. With the 10-year US Treasury yield now already in the middle of our 2021 year-end target range of 1.25-1.5%, and the macro backdrop remaining bond-bearish, we think it is timely to discuss the possibility that our yield target is too conservative Good Cyclical News Is Bad News For Treasuries The more recent move higher in US Treasury yields is notable because it has not been all about higher inflation breakevens, as has been the case since yields bottomed in mid-2020; real yields are finally starting to inch higher. The 30-year TIPS yield now sits in positive territory at +0.09%, ending a period of negative real yields dating back to the pandemic-induced market shock of last spring (Chart 2). Real yields across the rest of the TIPS curve are also starting to stir, even at the 2-year point, yet remain negative. Thus, the price action has supported one of US Bond Strategy’s Key Views for 2021 that the real yield curve will steepen.1 This uptick in US real yields has occurred alongside a string of positive developments on the US economy, suggesting that improved growth prospects – and what that means for future US inflation and Fed policy - are the key driver. Improving US domestic demand US economic data is not only showing resilience but gaining positive momentum. The preliminary US Markit composite PMI (combining both manufacturing and services industries) for February rose to the highest level in six years (Chart 3). Retail sales in January rose by an eye-popping 5.3% versus the month prior, due in no small part to the impact of government stimulus checks issued in the December pandemic relief package. The Conference Board measure of consumer confidence also picked up in January. The improving trend in US data so far in 2021 is pointing to some potentially big GDP numbers – the New York Fed’s “Nowcast” is calling for Q1 real GDP growth of 8.3%. Chart 2US Real Yields Starting Are Stirring

US Real Yields Starting Are Stirring

US Real Yields Starting Are Stirring

Chart 3US Growing Faster Than Lockdown-Stricken Europe

US Growing Faster Than Lockdown-Stricken Europe

US Growing Faster Than Lockdown-Stricken Europe

Vaccine rollout success After a sloppy start to the COVID-19 vaccination program in the US, the numbers are starting to improve with 19% of the US population having received at least one dose (Chart 4). Numbers of new cases and hospitalizations due to the virus have been collapsing as well, a sign that new lockdowns can be avoided, particularly in the larger US coastal cities. The vaccination numbers are even higher in the UK, where Prime Minister Boris Johnson this week revealed an ambitious plan to fully reopen the UK economy by June. While the pace of inoculation has been far slower within the euro area and other developed countries like Canada, developments in the US and UK are a hopeful sign that the vaccines can help free the world economy from the shackles of COVID-19. Chart 4The US & UK Leading The Way On The Vaccine Rollout

Optimism Reigns Supreme

Optimism Reigns Supreme

Even more fiscal stimulus Our US political strategists expect the Biden Administration’s $1.9 trillion pandemic relief package (the “American Rescue Plan”) to be passed by the US Senate in mid-March via a simple majority through a reconciliation bill.2 A second bill is likely to be passed this autumn or next spring with a much larger number, potentially up to $8 trillion worth of spending on infrastructure, health care, child care and green projects over the next ten years (Chart 5). These are big numbers for a $21 trillion US economy that will increasingly need less stimulus as lockdowns ease. Chart 5Biden’s Agenda AFTER The American Rescue Plan

Optimism Reigns Supreme

Optimism Reigns Supreme

Chart 6Welcome Back, Inflation?

Welcome Back, Inflation?

Welcome Back, Inflation?

Chart 7Price Pressures From US Manufacturing Bottlenecks

Price Pressures From US Manufacturing Bottlenecks

Price Pressures From US Manufacturing Bottlenecks

The combined impact of fiscal stimulus, accommodative monetary policy, easy financial conditions and fewer pandemic related economic restrictions has the potential to boost US economic growth quite sharply this year. If US GDP growth follows the Bloomberg consensus forecasts, the US output gap will be fully closed by Q1/2022 (Chart 6).That would be a much faster elimination of the spare capacity created by the 2020 recession compared to the post-2009 experience, raising the risk of upside inflation surprises later this year and in 2022. Signs of growing inflation pressures will make many FOMC members increasingly uncomfortable, even under the Fed’s new Average Inflation Targeting strategy where inflation overshoots will be more tolerated. Already, there are signs of sharply increased price pressures in the US economy stemming from factory bottlenecks (Chart 7). US manufacturers have had to deal with pandemic-induced disruptions to supply chains, in addition to the unexpectedly fast recovery of US consumer demand from last year’s recession that left companies short of inventory.3 The ISM Manufacturing Prices Paid index hit a 10-year high in January, fueled by surging commodity prices, which is already showing up in some inflation data. The US Producer Price Index for finished goods jumped 1.3% in January – the largest monthly surge since 2009 – boosting the annual inflation rate to 1.7% from 0.8% the prior month. Chart 8A Boost To US Inflation Coming Soon From Base Effects

A Boost To US Inflation Coming Soon From Base Effects

A Boost To US Inflation Coming Soon From Base Effects

Chart 9Additional Upside US Inflation Risks

Additional Upside US Inflation Risks

Additional Upside US Inflation Risks

Chart 10US Shelter Inflation Set To Bottom Out

US Shelter Inflation Set To Bottom Out

US Shelter Inflation Set To Bottom Out

A pickup in US annual inflation rates over the next few months was already essentially a done deal because of base effect comparisons versus the collapse in inflation during the 2020 COVID-19 recession (Chart 8). Additional inflation pressures stemming from factory bottlenecks could provide an additional lift to realized inflation rates. When looking at the main components of the US inflation data, there is scope for a broad-based pickup that goes beyond simple base effect moves. Core Goods CPI inflation is now rising at a 1.7% year-over-year rate, the highest since 2012, with more to come based on the acceleration of growth in US non-oil import prices (Chart 9). Core Services CPI inflation has plunged during the pandemic and is now growing at a 0.5% annual rate. As the US economy reopens from pandemic restrictions, services inflation should begin to recover and add to the rising trend of goods inflation. This will especially be true if the Shelter component of US inflation also begins to recover in response to a tightening demand/supply balance for US housing (Chart 10). Bottom Line: US Treasury yields are rising in response to positive upward momentum in US economic growth, the likelihood of some pickup in inflation over the next 6-12 months and, most importantly, shifting expectations that the Fed will turn less dovish later this year. Evaluating The Fed’s Next Moves Fed officials have continued to signal that they are not yet ready to consider any change to monetary policy settings or forward guidance on future rate moves. In his semi-annual testimony before US Congress this week, Fed Chair Jerome Powell reiterated that the pace of the Fed’s asset purchases would only begin to slow once “substantial progress” has been made towards the Fed’s inflation and unemployment objectives. Powell also stuck to his previous messaging that the Fed would “continue to clearly communicate our assessment of progress toward our goals well in advance of any change in the pace of purchases”.4 According to the New York Fed’s Primary Dealer and Market Participant surveys for January, however, the Fed is not expected to stay silent on the topic of tapering for much longer. According to the surveys, the Fed is expected to begin tapering its purchases of Treasuries and Agency MBS in the first quarter of 2022 (Chart 11). A full tapering to zero (net of rollovers of maturing debt) is expected by the first quarter of 2023. Clearly, bond traders and asset managers believe that US growth and inflation dynamics will both improve over the course of this year such that the Fed will have little choice but to begin the signaling of tapering sometime before the end of 2021. Chart 11Fed Surveys Expect A Full QE Tapering In 2022

Optimism Reigns Supreme

Optimism Reigns Supreme

The Fed has been a bit more transparent on the conditions that must be in place before rate hikes would begin. Labor market conditions must be consistent with full employment, while headline PCE inflation must reach at least 2% and be “on track” to moderately exceed that target for some time. On that front, markets believe these conditions will all be met by early 2023, based on pricing in the US overnight index swap (OIS) curve. The first 25bp rate hike is now priced to occur in February 2023 (Chart 12). This is a big shift from the start of the year, when Fed “liftoff” was expected to occur in October 2023. Thus, in a span of just six weeks, interest rate markets have pulled forward the timing of the first Fed rate hike by eight months. Liftoff would occur almost immediately after the Fed was done fully tapering asset purchases, based on the timetable laid out in the New York Fed surveys, although Fed officials have noted that rate hikes could begin before tapering is complete. Chart 12Pulling Forward The Timing Of Future Fed Rate Hikes

Pulling Forward The Timing Of Future Fed Rate Hikes

Pulling Forward The Timing Of Future Fed Rate Hikes

In our view, the timetable laid out in the New York Fed surveys and in the US OIS curve is not only plausible but probable. If the US economy does indeed print the 4-5% real GDP consensus growth forecasts during the second half of this year, with realized inflation approaching 2% as outlined above, then it will be very difficult for the Fed to justify the need to maintain the current pace of asset purchases. The Fed will want to avoid another 2013 Taper Tantrum by signaling less QE well in advance, to avoid triggering a spike in Treasury yields that could upset equity and credit markets or cause an unwelcome appreciation of the US dollar. However, the New York Fed surveys indicate that the bond market is well prepared for a 2022 taper, so the Fed only has to meet those expectations to prevent an unruly move in the Treasury market. That means the Fed will likely signal tapering toward the end of this year. Chart 13Markets Expect A Negative Real Fed Funds Rate

Optimism Reigns Supreme

Optimism Reigns Supreme

The Fed can maintain caution on signaling the timing of the first rate hike once tapering begins, based on how rapidly the US unemployment rate falls towards the Fed’s estimate of full employment. The median projection from the FOMC’s latest Summary of Economic Projections is for the US unemployment rate to fall to 4.2% in 2022 and 3.7% in 2023, compared to the median longer-run estimate of 4.1%. Thus, if the Fed sticks to current guidance on the employment conditions that must be in place before rate hikes can begin, then liftoff would occur sometime in late 2022 or early 2023 – not far off current market pricing – as long as US inflation is at or above the Fed’s 2% target at the same time. Once the Fed begins rate hikes, the pace of the hikes relative to inflation will determine how high real bond yields can rise. The 10-year TIPS yield has become highly correlated over the past few years to the level of the real fed funds rate (Chart 13). The current forward pricing in US OIS and CPI swap curves indicates that the markets are priced for a negative real fed funds rate until at least 2030. That is highly dovish pricing that will be revised higher once the Fed begins tapering and the market begins to debate the timing and pace of the Fed’s next rate hike cycle. Thus, it is highly unlikely that real Treasury yields will stay as low as implied by the forward curves over the next few years. Bottom Line: It is still too soon to expect the Fed to begin signaling a move to turn less accommodative. However, rising realized US inflation amid dwindling spare economic capacity will make the Fed more nervous about its ultra-dovish policy stance in the second half of 2021. This will trigger a repricing of the future path of US interest rates embedded in the Treasury curve, but a Taper Tantrum repeat will be avoided. How High Can Treasury Yields Go In The Current Move? Our preferred financial market-based cyclical bond indicators are still trending in a direction pointing to higher Treasury yields (Chart 14). The ratio of the industrial commodity prices (copper, most notably) to the price of gold, the relative equity market performance of US cyclicals (excluding technology) to defensives, and the total return of a basket of emerging market currencies are all consistent with a 10-year US Treasury yield above 1.5%. With regards to other valuation measures, the 5-year/5-year Treasury forward rate is already at or close to the top of the range of the longer-run fed funds rate projection from the New York Fed surveys (Chart 15). We have used that range to provide guidance as to how high Treasury yields can go during the current bond bear market. On this basis, longer maturity yields do not have much more upside unless survey respondents start to revise up their fed fund rate expectations, something that could easily happen if inflation surprises to the upside in the back-half of the year. Chart 14Cyclical Indicators Support Rising UST Yields

Cyclical Indicators Support Rising UST Yields

Cyclical Indicators Support Rising UST Yields

Chart 15A Rapid Move Higher In UST Forward Rates

A Rapid Move Higher In UST Forward Rates

A Rapid Move Higher In UST Forward Rates

Chart 16This UST Selloff Not Yet Stretched

This UST Selloff Not Yet Stretched

This UST Selloff Not Yet Stretched

Finally, the rising uptrend in longer-maturity Treasury yields is not overly stretched from a technical perspective (Chart 16). The 10-year yield is currently 55bps above its 200-day moving average, but yields got as high as 80-90bps above the moving average during the previous cyclical troughs in 2013 and 2016. The survey of fixed income client duration positioning from JP Morgan shows that bond investors are running duration exposure below benchmarks, but not yet at the bearish extremes seen in 2011, 2014 and 2017. A similar message can be seen in the Market Vane Treasury Sentiment indicator, which has been falling but remains well above recent cyclical lows. Summing it all up, it appears that the 1.5% ceiling of our 2021 10-year Treasury yield target range may prove to be too low. A move 20-30bps above that is quite possible, although those levels would only be sustainable if the Fed alters the forward guidance to pull forward the timing of rate hikes. We view that as a risk for 2022, not 2021. Bottom Line: Maintain below-benchmark US duration exposure, with the 10-year Treasury yield likely to soon test the 1.5% level. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research US Bond Strategy Special Report, "2011 Key Views: US Fixed Income", dated December 15, 2020, available at usbs.bcaresearch.com. 2 Please see BCA Research US Political Strategy Weekly Report, "Don’t Forget Biden’s Health Care Policy", dated February 17, 2021, available at usps.bcaresearch.com. 3https://www.wsj.com/articles/consumer-demand-snaps-back-factories-cant-keep-up-11614019305?page=1 4https://www.federalreserve.gov/newsevents/testimony/powell20210223a.htm Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Optimism Reigns Supreme

Optimism Reigns Supreme

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights US inflation is set to increase sharply over the coming months as base effects kick in. Higher fuel prices, fiscal stimulus, and the partial relaxation of lockdown measures should also boost inflation. The Fed is unlikely to react hawkishly to higher inflation, arguing that it is largely transitory in nature. While the Fed’s relaxed attitude towards inflation risks may be justified in the near term, there is a high probability that inflation will get out of hand later this decade. Contrary to conventional wisdom, many of the factors that led to high inflation in the 1970s could reassert themselves. Investors should overweight stocks for now, but be prepared to reduce equity exposure in about two years. US Inflation Has Bottomed US inflation surprised on the downside in January. The core CPI was flat on the month, compared with the consensus estimate for an increase of 0.2%. We expect US inflation to move higher over the coming months. The weakness in January’s inflation print was concentrated in sectors of the economy that have been hard hit by the pandemic. Airline fares dropped 3.2%, hotel rates fell 1.9%, and entertainment admission prices declined 5.5%. Prices in these sectors should rise on a year-over-year basis as base effects kick in (Chart 1). The relaxation of lockdown measures should also help to partially restore demand in these areas. WTI crude prices have risen 70% since the end of October. Rising energy prices should push up headline inflation, with some bleed-through to core prices. Chart 2 shows that there is a strong correlation between gasoline prices and headline inflation. If gasoline prices evolve in line with what is predicted by the futures market, headline inflation could temporarily rise to 4% this spring. Chart 1Base Effects Will Push Inflation Higher

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Chart 2Strong Link Between Gasoline Prices And Headline Inflation

Strong Link Between Gasoline Prices And Headline Inflation

Strong Link Between Gasoline Prices And Headline Inflation

In addition, the lagged effects from a weaker dollar should translate into higher goods prices in the US (Chart 3). A stronger labor market and a slower pace of rent forgiveness should also boost housing inflation (Chart 4). Chart 3A Weaker Dollar Will Be A Tailwind For Inflation

A Weaker Dollar Will Be A Tailwind For Inflation

A Weaker Dollar Will Be A Tailwind For Inflation

Chart 4Stronger Labor Market Will Boost Housing Inflation

Stronger Labor Market Will Boost Housing Inflation

Stronger Labor Market Will Boost Housing Inflation

Fiscal stimulus should further supercharge demand, adding to inflationary pressures. Ironically, Republican unwillingness to offer modest, politically palatable cuts to President Biden’s proposed aid bill has opened the door to the Democrats ramming through the entire $1.9 trillion package via the reconciliation process. As we discussed last week, the amount of stimulus in the pipeline easily dwarfs the size of the output gap. From Reflation To Inflation? Deflation is bad for stocks, just as is high and accelerating inflation. Somewhere between deflation and inflation, however, lies reflation. Reflation is good for stocks. Chart 5Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

We are currently in a reflationary Goldilocks zone, where inflation expectations have risen but not by enough to force the Fed’s hand. There is a high probability we will stay in this Goldilocks zone for the remainder of the year. The 5-year/5-year forward TIPS breakeven rate is still below the level that the Fed regards as consistent with its long-term inflation objective, and even farther below the level that would cause the Fed to panic (Chart 5). Jay Powell told The Economic Club of New York last week that the Fed is unlikely to “even think about withdrawing policy support” anytime soon. The Fed minutes released on Wednesday echoed this view. That ‘70s Show? The path to higher interest rates is lined with lower interest rates. A period of ultra-easy monetary policy can sow the seeds for economic overheating, rising inflation, and ultimately, much higher interest rates. Since this is precisely what happened during the 1970s, it is prudent to ask whether something like that could happen again. Investors certainly do not believe a replay of the 70s is in the cards, at least if long-term CPI swaps are any guide (Chart 6). Yet, we think that a 1970s-style inflationary episode is a greater risk than most investors realize. As we discuss below, much of what investors believe about how inflation emerged during that period is either based on myths, or at best, half-truths. Let’s examine each of these misconceptions in turn. Myth #1: High inflation in the 1970s was primarily driven by supply disruptions, with oil shocks being the most prominent. Fact: Oil shocks exacerbated the inflation problem in the 1970s, but it was an overheated economy that permitted inflation to rise in the first place. Inflation took off in 1966, seven years before the first oil shock. By 1969, core CPI inflation was running at close to 6% (Chart 7). Chart 6Investors Do Not Expect Inflation To Vault Higher

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Chart 7Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Similar to today, fiscal policy was exceptionally accommodative in the mid-1960s. The escalation of the Vietnam War produced a surge in military expenditures. Social spending rose dramatically with the introduction of Lyndon Johnson’s “Great Society” programs. Medicare and Medicaid took effect in July 1966. Amy Finkelstein has estimated that Medicare, the larger of the two health care programs, led to a 37% increase in real hospital expenditures between 1965 and 1970. Johnson’s “guns and butter” policies caused government spending to surge in the second half of the decade. The budget deficit, which was broadly balanced during the first half of the 60s, swelled to 4% of GDP (Chart 8). As fiscal policy was loosened, the economy began to overheat. The unemployment rate fell to 3.8% in 1966, two percentage points below what economists later concluded had been its full-employment level. Chart 8US "Guns And Butter" Policies In The 1960s Caused Government Spending To Swell

US "Guns And Butter" Policies In The 1960s Caused Government Spending To Swell

US "Guns And Butter" Policies In The 1960s Caused Government Spending To Swell

Myth #2: The Phillips curve is much flatter today. Chart 9The Increase In Inflation In 1966 Was Broad-Based

The Increase In Inflation In 1966 Was Broad-Based

The Increase In Inflation In 1966 Was Broad-Based

Fact: The Phillips curve was also flat during the 1960s. Core inflation was remarkably stable during the first half of the 60s, averaging about 1.5%, even as the unemployment rate steadily declined. Then, starting in 1966, core inflation more than doubled within the span of ten months. As Chart 9 illustrates, the sudden spike in inflation in 1966 was fairly broad-based. A “kink” in the Phillips curve had been reached. That the relationship between inflation and unemployment turned out to be non-linear is not surprising. As long as there is some slack in the labor market, employers are likely to resist raising wages. Thus, a decline in unemployment from a high level to a merely moderate level is unlikely to lead to meaningful wage inflation. It takes a truly overheated labor market – one that forces firms to engage in a tit-for-tat battle to entice workers – for the relationship between unemployment and inflation to reassert itself. In the near term, there is little risk that the US economy will reach a kink in the Phillips curve. Jason Furman estimates that the unemployment rate stood at 8.3% in January if one adjusts for the drop in labor force participation and methodological problems with how the BLS defines temporarily furloughed workers. This is well above the level that could trigger a price-wage spiral. Chart 10Is The Phillips Curve Really Dead?

Is The Phillips Curve Really Dead?

Is The Phillips Curve Really Dead?

Yet, it would be naïve to think that such a spiral could not materialize in a few years. As Chart 10 shows, over the past 40 years, every time the US labor market was on the cusp of overheating, something would invariably come along to push up unemployment. Last year, it was the pandemic. In 2008, it was the Global Financial Crisis. In 2000, it was the dotcom bust. In the early 1990s, it was the collapse in commercial real estate prices following the Savings and Loan Crisis. Admittedly, only the pandemic qualifies as a truly exogenous shock. The preceding three recessions were fomented by growing economic imbalances, which were ultimately laid bare by a Fed hiking cycle. One can debate the degree to which the US economy is suffering from non-pandemic related imbalances today, but one thing is certain: The Fed is not keen on raising rates anytime soon. Thus, whatever imbalances exist today may not be exposed before the economy has had the chance to overheat. Myth #3: Inflation expectations are better anchored these days. Chart 11Long-Term Bond Yields Lagged Inflation During The 1960s

Long-Term Bond Yields Lagged Inflation During The 1960s

Long-Term Bond Yields Lagged Inflation During The 1960s

Fact: Inflation expectations certainly became unmoored in the 1970s. However, there is not much evidence that expectations were adrift prior to the sudden increase in inflation in 1966. At the time, the US had not experienced a major episode of inflation since the Civil War. While long-term bond yields did rise in the second half of the 60s, they generally lagged inflation, suggesting that investors were caught off-guard (Chart 11). It should also be noted that the US and other major economies operated under the Bretton Woods system of fixed exchange rates during the 1960s. Each US dollar was convertible into gold at the official rate of $35 per ounce. The existence of this quasi-gold standard helped anchor inflation expectations. The system began to fall apart in the late 1960s as inflation rose. When President Nixon suspended the dollar’s convertibility into gold in August 1971, the US CPI had already increased by nearly 30% from its 1965 level. While the collapse of the Bretton Woods system in the early 1970s undoubtedly caused inflation expectations to become further unhinged, the breakdown of the system would not have occurred if inflation had not risen in the first place. Myth #4: Widespread wage indexation and powerful trade unions fueled an acceleration in the 1960s. Fact: Just as was the case with the unmooring of inflation expectations, wage indexation was more a response to rising inflation than a cause of it. Chart 12 shows that the share of workers covered by cost of living adjustments only jumped after inflation had accelerated. Chart 12Higher Inflation Led To More Inflation-Indexed Wage Contracts, Not The Other Way Around

Higher Inflation Led To More Inflation-Indexed Wage Contracts, Not The Other Way Around

Higher Inflation Led To More Inflation-Indexed Wage Contracts, Not The Other Way Around

As far as unions are concerned, the US unionization rate peaked by the end of the 1950s and was already on a downward path when inflation began to rise. Revealingly, Canada experienced a similar decline in inflation as the US in the early 1980s even though unionization rates remained elevated (Chart 13). This suggests that union power was not a dominant driver of inflation. Chart 13Inflation Fell In Canada, Despite A High Unionization Rate

Inflation Fell In Canada, Despite A High Unionization Rate

Inflation Fell In Canada, Despite A High Unionization Rate

Myth #5: Today’s globalized economy will limit inflationary pressures. Fact: The empirical evidence generally suggests that the impact of globalization on US inflation has been smaller than widely supposed.1 This is not surprising. The US is a fairly closed economy. Imports account for only 15% of GDP. As a result, a fairly large change in relative prices is necessary to prompt Americans to shift a meaningful fraction of their expenditures towards foreign-made goods. Such a shift in spending would require a real appreciation of the US dollar. A real appreciation could occur either if US inflation exceeds inflation abroad or if the nominal value of the dollar strengthens against other currencies. (Admittedly, the standard terminology can be a bit confusing; just think of a real US dollar appreciation as anything that makes the US economy less competitive). Here’s the thing though: The US dollar is unlikely to strengthen unless the Federal Reserve starts to sound more hawkish. If the Fed remains in the dovish camp, real rates could fall as inflation edges higher. This will put downward pressure on the dollar, leading to a smaller trade deficit and even more aggregate demand. Myth #6: Demographics are much more deflationary now than they were in the past. Fact: Demographic trends arguably did help push down inflation over the past few decades. However, population aging is likely to boost inflation going forward. Chart 14 shows that the ratio of workers-to-consumers in the US and around the world – the so-called “support ratio” – rose steadily in the 1980s, 1990s, and 2000s as more women entered the labor force and the number of dependent children per household declined. An increase in the ratio of workers-to-consumers is equivalent to an increase in the ratio of production-to-consumption. A rising support ratio is thus deflationary. More recently, however, the support ratio has begun to decline as baby boomers retire but continue to spend. Consumption actually increases in old age once health care spending is included in the tally (Chart 15). As production falls in relation to consumption, inflation could rise. Chart 14Support Ratios Are Declining Globally After Rising Steadily For Three Decades

Support Ratios Are Declining Globally After Rising Steadily For Three Decades

Support Ratios Are Declining Globally After Rising Steadily For Three Decades

Chart 15Consumption Increases In Old Age Once Health Care Spending Is Factored In

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Myth #7: Today’s fast pace of technological innovation will keep inflation down. Chart 16Total Factor Productivity Growth Is Lower Than It Was During The Great Inflation

Total Factor Productivity Growth Is Lower Than It Was During The Great Inflation

Total Factor Productivity Growth Is Lower Than It Was During The Great Inflation

Fact: Total factor productivity growth – a broad measure of innovation – is not just low by historic standards today; it is lower than during the period of the Great Inflation spanning from 1966 to 1982 (Chart 16). Some have argued that productivity growth is mismeasured. We have examined this argument in the past and found it wanting. In any case, economic theory does not necessarily say that technological innovation should be deflationary. Economic theory states that faster innovation should lead to higher real incomes. It does not say whether the increase in real income should come via rising nominal income or falling inflation. Indeed, to the extent that faster innovation leads to higher potential GDP growth, it could fuel inflation. This is because stronger trend growth will tend to raise the neutral rate of interest, implying that monetary policy will become more stimulative for any given policy rate. Myth #8: Policymakers have learned from their mistakes. It is easy to dismiss this claim, but it is worth considering it seriously. Some of the mistakes that policymakers made during the 60s and 70s were far from obvious at the time. Athanasios Orphanides, who formerly served as a member of the ECB’s Governing Council, has documented that central banks in the US and other major economies systematically overestimated the amount of slack in their economies (Chart 17). They also overestimated trend growth, with the result that they came to see the combination of sluggish growth and seemingly high unemployment as evidence of inadequate demand. Chart 17Central Banks Overestimated The Degree Of Slack In Their Economies During The Great Inflation

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Is it possible that economic analysis has improved so much over the past 40 years that such mistakes would not be repeated today? Perhaps, but it is worth noting that not only did most economists fail to predict the productivity boom in the late 1990s, most were not even aware that it had happened until after it had ended. Knowing what is happening to the economy in real time is hard enough. Predicting what will happen to such things as trend growth and the natural rate of unemployment is even more difficult. Myth #9: The Fed is a lot more independent now. Fact: We will only know for sure when this independence is tested. History clearly shows that inflation tends to be higher in countries which lack independent central banks (Chart 18). The Fed’s independence was compromised in the 1970s. In his exhaustive study of the Nixon tapes, Burton Abrams documented how Richard Nixon sought, and Fed Chairman Arthur Burns obligingly delivered, an expansionary monetary policy in the lead-up to the 1972 election. Chart 18Inflation Is Higher In Countries Lacking Independent Central Banks

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Starting with the appointment of Paul Volcker, the Fed sought to regain its independence. Most recently, Jay Powell publicly resisted Donald Trump’s efforts to prod the Fed to ease monetary policy. Yet, the Fed’s independence may turn out to be illusory. The Fed wasted little time in slashing rates and relaunching its QE program once the pandemic began. But will it be as quick to tighten monetary policy if inflation starts getting out of hand? Jay Powell’s four-year term as chair runs through February 2022. He will need to stay in Joe Biden’s good graces if he hopes to be reappointed to a second term. The fact that government debt levels are so high further complicates matters. Higher interest rates would force the government to shift funds from social programs towards bond holders. Will the Fed raise rates even if it faces strong political opposition? Time will tell. Investment Conclusions Chart 19Social Unrest Can Fuel Inflation

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

While no two periods are exactly the same, there are a number of striking similarities between the late 1960s and the present day. As is the case today, fiscal policy was highly expansionary back then. The same goes for monetary policy: Just like today, the Fed kept interest rates well below the growth rate of the economy. In the 1960s, the Federal Reserve was still focused on avoiding a repeat of the Great Depression and the deflationary wave that accompanied it. Today, the Fed is equally focused on reflating the economy. The 1960s was a decade of rising political and social unrest. Crime rates went through the roof, a trend that was eerily matched by rising inflation rates (Chart 19). Early estimates suggest that the US homicide rate jumped by 37% in 2020 – easily the largest one-year increase on record. As was the case in the 1960s, most of the news media has ignored this disturbing development. What should investors do? Our tactical MacroQuant model is flagging some near-term risks for stocks. Nevertheless, as long as the economy is growing solidly and the Fed remains on the sidelines, it is too early for investors with a 12-month horizon to bail on equities. Instead, equity investors should favor sectors that could benefit from higher inflation. Commodity producers are a natural choice. Banks could also gain from an uptick in inflation. Chart 20 shows the remarkably strong correlation between the performance of US banks relative to the S&P 500 and the 10-year Treasury yield. Higher bond yields would boost bank net interest margins, leading to higher profits. Banks are also very cheap and have started to see their earnings estimates rise faster not only relative to the broader market but even relative to tech stocks (Chart 21). Chart 20Bank Shares Are A Buy (I)

Bank Shares Are A Buy (I)

Bank Shares Are A Buy (I)

Fixed-income investors should keep duration risk low. They should also favor inflation-protected securities over nominal bonds. Chart 21Bank Shares Are A Buy (II)

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Looking further out, the secular bull market in stocks will end when inflation rises to a high enough level that even the Fed cannot ignore. That day will arrive, but probably not for another two years. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Footnotes 1 Globalization is often cited as a potential reason behind low inflation in advanced economies, including the US. However, a number of empirical studies have found that globalization did not play a major role. In general, domestic economic conditions are seen as the main factor in the inflation process. Please see Jane Ihrig, Steven B. Kamin, Deborah Lindner, and Jaime Marquez, “Some Simple Tests of the Globalization and Inflation Hypothesis,” Board of Governors of the Federal Reserve System (International Finance Discussion Papers No. 891) (April 2007); Laurence M. Ball, “Has Globalization Changed Inflation?” National Bureau of Economic Research Working Paper Series 12687 (November 2006), and associated blog post “Has Globalization Changed Inflation?” National Bureau of Economic Research, (June 2007); Janet. L. Yellen, 'Panel discussion of William R. White “Globalisation and the Determinants of Domestic Inflation”,' Presentation to the Banque de France International Symposium on Globalisation, Inflation and Monetary Policy (March 2008); Fabio Milani, “Global Slack And Domestic Inflation Rates: A Structural Investigation For G-7 Countries,” Journal of Macroeconomics, (32:4) (2010); and and Lei Lv, Zhixin Liu, and Yingying Xu, “Technological progress, globalization and low-inflation: Evidence from the United States,” PLoS ONE, (14:4), (April 2019). Global Investment Strategy View Matrix

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Special Trade Recommendations

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Current MacroQuant Model Scores

1970s-Style Inflation: Yes, It Could Happen Again

1970s-Style Inflation: Yes, It Could Happen Again

Dear Client, This week, the US Bond Strategy service is hosting its Quarterly Webcast (today at 10:00 AM EST, 3:00 PM GMT, 4:00 PM CET, 11:00 PM HKT). In addition, we are sending this Quarterly Chartpack that provides a recap of our key recommendations and some charts related to those recommendations and other areas of interest for US bond investors. Please tune in to the Webcast and browse the Chartpack at your leisure, and do let us know if you have any questions or other feedback. To view the Quarterly Chartpack PDF please click here. Best regards, Ryan Swift, US Bond Strategist

Highlights The amount of fiscal stimulus in the pipeline is more than enough to close the US output gap. Inflation is likely to surprise on the upside this year. The Fed will brush off any evidence of economic overheating during the coming months, stressing the “transitory” nature of the problem. Still, long-term bond yields, over which the Fed has less control, will rise. As long as bond yields move higher in conjunction with improving growth expectations, stocks will remain in an uptrend. The bull market in equities will only end when the Fed starts to sound more hawkish. That is not in the cards for the next 12 months at least. Stimulus Smackdown During the past month, a debate has erupted over how much additional fiscal stimulus the US economy needs. The side arguing that the sea of red ink has gotten too deep includes an unlikely cast of characters like Larry Summers, who has famously contended that sustained large budget deficits are necessary to stave off secular stagnation. It also includes Olivier Blanchard, who previously served as the IMF’s chief economist and pushed the multilateral lender to abandon its historic adherence to fiscal austerity. Chart 1Generous Government Transfers Boosted Household Savings

Generous Government Transfers Boosted Household Savings

Generous Government Transfers Boosted Household Savings

Rather than citing debt sustainability concerns, these newfound stimulus skeptics worry that large-scale fiscal easing at the present juncture risks overheating the economy. They point out that President Biden’s proposed $1.9 trillion package, coming on the heels of the $900 billion stimulus bill Congress passed in late December, would inject another 13% of GDP into the economy, on the back of the lagged boost from the first stimulus package. We estimate that US households had accumulated $1.5 trillion in excess savings (7% of GDP) as of the end of 2020, thanks to the fiscal transfers they received under the CARES Act (Chart 1). US real GDP in the fourth quarter of 2020 was 2.5% below its level in the fourth quarter of 2019. Assuming trend growth of 2%, this implies that the output gap – the difference between what the economy is capable of producing and what it actually is producing – has widened by about 4.5% of GDP since the onset of the pandemic. The Congressional Budget Office (CBO) believes the US economy was operating 1% above potential in Q4 of 2019, suggesting that the output gap is around 3.5% of GDP. As it has in the past, the CBO is probably understating the amount of slack in the economy. Our guess is that the US was close to full employment in the months leading up to the pandemic, which implies that the output gap is currently somewhere between 4% and 5% of GDP. While fairly large in absolute terms, it is still smaller than the amount of stimulus currently in the pipeline. Gentle Jay Not So Worried About Overheating Stimulus advocates argue that households will continue to use stimulus checks to fortify their balance sheets, rather than rush out to spend the windfall. They also note that unemployment payments will come down if the labor market recovers more quickly than projected. And even if the economy does temporarily overheat, “so what” they say. The Fed has been trying to engineer an inflation overshoot for years. Now is its chance. Jay Powell seems to sympathize with this thesis. Speaking at a virtual conference organized by The Economic Club of New York this week, Powell repeated his call for fiscal easing and told attendees that the Fed is unlikely to “even think about withdrawing policy support” anytime soon. His words echo remarks made at the press conference following January’s FOMC meeting, where he said “I’m much more worried about falling short of a complete recovery and losing people’s careers,” before adding: “Frankly, we welcome slightly higher inflation.” Most other FOMC members have struck a similar tone. Earlier this year, Fed Governor Lael Brainard noted that “The damage from COVID-19 is concentrated among already challenged groups. Federal Reserve staff analysis indicates that unemployment is likely above 20 percent for workers in the bottom wage quartile, while it has fallen below 5 percent for the top wage quartile.” How Big Is The Fiscal Multiplier From Stimulus Checks? Chart 2Service Inflation Fell During The Pandemic, While Goods Inflation Rose

Service Inflation Fell During The Pandemic, While Goods Inflation Rose

Service Inflation Fell During The Pandemic, While Goods Inflation Rose

One of the reasons that households saved much of last year’s stimulus checks was because there was not much to spend them on. Officially measured service inflation was well contained last year, but many services were simply not available for purchase. In contrast, goods prices, which usually fall over time, rose (Chart 2). As the economy opens up, total spending will recover. Rising household spending will have a multiplier effect. The simplest version of the Keynesian multiplier for fiscal transfer payments is equal to MPC/(1-MPC), where MPC is the marginal propensity to consume. Assuming that households initially spend 50 cents of every dollar they receive, the multiplier would be 0.5/(1-0.5)=1. In other words, every dollar of direct stimulus payments will eventually generate one additional dollar of aggregate demand. One could argue that this multiplier estimate overstates the impact on demand because it ignores the fact that households will regard stimulus checks as one-time payments rather than a continuous flow of income. One could also point out that taxes and imports will cut into the multiplier effect on domestic spending. There is truth to all these arguments, but they are not as compelling as they seem. According to a recent US Census study, only 37% of Americans reported no difficulty in paying for usual household expenses during the pandemic. A mere 16% of workers with incomes below $35,000 reported no difficulty, compared with more than two-thirds of workers with incomes above $100,000 (Chart 3). In the euphemistic parlance of economics, most US households are “liquidity constrained,” meaning that they are likely to spend a large chunk of any income they receive, even if it is a one-off grant.1 Chart 3The Pandemic Has Put A Spotlight On The Liquidity Constraints Of US Households

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

As for taxes, while the income from subsequent spending will be taxed, the stimulus checks that households receive will remain untaxed. Granted, some of the demand generated by stimulus checks will leak abroad in the form of higher imports. However, keep in mind that the US is a fairly closed economy – imports account for only 15% of GDP. Moreover, the full impact on imports depends on what happens to the value of the dollar. If the Fed keeps rates unchanged but inflation rises, the accompanying decline in short-term real rates could weaken the dollar, curbing imports and boosting exports in the process. This could lead to a higher multiplier rather than a lower one. Lastly, higher consumption is likely to boost corporate capex, as companies scramble to raise capacity in anticipation of strong demand (Chart 4). Economists call this the “accelerator effect.” Investment spending is 2.5-times as volatile as consumption. Hence, even modest increases in consumption can trigger large increases in investment. Chart 4Stronger Consumption Tends To Boost Capex

Stronger Consumption Tends To Boost Capex

Stronger Consumption Tends To Boost Capex

Unemployment Benefits: Adding To Aggregate Demand But Subtracting From Supply? As Chart 5 shows, stimulus payments to households account for 17% of the December stimulus bill and 26% of Biden’s proposed package for a combined total of around $650 billion (3% of GDP, or around two-thirds of the current output gap). The balance consists of expanded unemployment benefits, health and education funding, support for small businesses, and aid to state and local governments. Chart 5Stimulus Package Breakdowns

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

Unemployment benefits are likely to be spent fairly quickly since, in most cases, they replace lost income that had previously been used to finance consumption. More generous unemployment benefits could temporarily reduce aggregate supply. Higher federal unemployment benefits would more than offset the lost income of close to half of jobless workers, potentially creating a disincentive to seek employment. Inflation Expectations Will Continue To Rise Aggregate demand is likely to outstrip the economy’s supply-side potential over the coming months. Hence, inflation will probably surprise on the upside this year, although not by enough to force the Fed to abandon its easy money stance. Inflation expectations have recovered since the depths of the pandemic. However, the 5-year/5-year forward TIPS breakeven rate is still below the level that BCA’s bond strategists believe the Fed regards as consistent with its long-term inflation objective, and even farther below the level that would cause the Fed to panic (Chart 6). This suggests that the Fed will brush off any evidence of overheating during the coming months, stressing the “transitory” nature of the problem. Still, rising inflation expectations will push up long-dated bond yields. At present, the 5-year/5-year forward Treasury yield stands at 1.89%. This is below the median estimate of the long-run equilibrium fed funds rate from the New York Fed’s Survey of Primary Dealers (Chart 7). With policy rates on hold, higher long-term bond yields will translate into steeper yield curves. We expect the 10-year Treasury yield to rise to 1.5% by the end of the year from the current level of 1.16%, with risks to yields tilted to the upside. Chart 6Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

Inflation Expectations Have Recovered But Are Still Below Levels That Would Cause Concern For The Fed

Chart 7Forward Treasury Yields Are Below Primary Dealers' Projections

Forward Treasury Yields Are Below Primary Dealers' Projections

Forward Treasury Yields Are Below Primary Dealers' Projections

Can Stocks Stand The Heat? To what extent will higher bond yields hurt stocks? To get a sense of the answer, it is useful to consider a dividend discount model. The simplest model, the Gordon Growth Model, says that the price of a stock, P, should equal the dividend that it pays, D, divided by the difference between the long-term discount rate, r, and the expected dividend growth rate, g:

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

We can write the discount rate as the combination of the long-term risk-free rate and the equity risk premium such that r = rf + ERP and then solve for the dividend yield:

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

Note that the value of the stock market becomes increasingly sensitive to changes in the risk-free rate when the dividend yield is low to begin with. For example, if the dividend yield is 2%, a 10-basis-point rise in the long-term risk-free rate will push down stock prices by 5%. In contrast, if the dividend yield is 1%, a 10-basis-point rise in the long-term risk-free rate will push down stock prices by 10%. Today, dividend and earnings yields for most global equity sectors are quite low, although not as low as they were in 2000 (Chart 8). Watch The Correlation Between r And g The fact that dividend and earnings yields are below their long-term average does make stocks vulnerable to a rise in bond yields. This is especially the case for relatively expensive equity sectors such as tech and consumer discretionary. Nevertheless, there is an important mitigating factor at work: Increases in the risk-free rate have generally been accompanied by stronger growth expectations. Chart 9 shows that S&P 500 forward earnings estimates have moved in lockstep with the 10-year Treasury yield, a proxy for the long-term risk-free rate. Chart 8Global Dividend And Earnings Yields Are Quite Low, Although Not As Low As In 2000

Global Dividend And Earnings Yields Are Quite Low, Although Not As Low As In 2000

Global Dividend And Earnings Yields Are Quite Low, Although Not As Low As In 2000

Chart 9Earnings Estimates Move In Lockstep With Bond Yields

Earnings Estimates Move In Lockstep With Bond Yields

Earnings Estimates Move In Lockstep With Bond Yields

This suggests that the main danger to equity investors is not higher bond yields per se, but a rise in bond yields in excess of upward revisions to growth expectations, or worse, against a backdrop of faltering growth. Such a predicament could eventually manifest itself. However, it is only likely to happen when the Fed turns hawkish. This is not in the cards for the next 12 months at least. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Footnotes 1 The difficulty that many households have had in making ends meet predates the pandemic. For example, in May 2019, the Consumer Finance Protection Bureau found that about 40% of US consumers claimed that they had difficulty paying bills and expenses. Among those with annual household incomes of $20,000 or less, difficulties were experienced by 6 out of 10 people. Moreover, about half of consumers reported that they would be able to cover expenses for no more than two months if they lost their main source of income by relying on all available sources of funds, including borrowing, savings, selling assets, or even seeking help from family and friends. Global Investment Strategy View Matrix

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

Special Trade Recommendations

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

Current MacroQuant Model Scores

Higher Bond Yields: Where Is The Breaking Point?

Higher Bond Yields: Where Is The Breaking Point?

Dear client, On behalf of the China Investment Strategy team, I would like to wish you a very happy, healthy, and prosperous Chinese New Year of the Ox (Bull)! Gong Xi Fa Chai, Jing Sima, China Strategist Highlights A projected 8% increase in China’s real GDP for 2021 will not be an acceleration from the V-shaped economic recovery from the second half of last year. Excluding an exceptionally strong year-over-year economic expansion in Q1, the average growth in the rest of this year will be slower than in 2H20, which implies China’s economic growth momentum has already passed its peak. On a quarter-over-quarter basis, an expected 18% annual growth in Q1 would mean that China’s economic growth momentum has moderated from Q4 last year. Chinese policymakers are not in a hurry to press the stimulus accelerator again, with good reason. Commodity and risk-asset prices will be the most vulnerable to a weakened demand growth. Feature China’s real GDP is expected to grow by more than 8% this year, which would be a significant improvement over last year’s 2.3%.1 However, it is misleading to compare this year’s growth with that of 2020 as a whole. The first three months of this year will undergo an exceptionally high year-on-year growth (YoY) rate due to the deep contraction experienced in Q1 last year. An 8% annual growth for 2021 would imply that the rate of economic expansion in the rest of this year will be slower than the sharp recovery in 2H20. From a policy perspective, an 8% real GDP growth in 2021 implies an average rate of 5% over the 2020-2021 period, within the long-term growth range targeted in China’s 14th Five-Year Plan - this removes policymakers’ incentives to further stimulate the economy. The annual National People's Congress (NPC) in early March should provide clues about the government's growth priorities and policy directions. If policymakers set 2021’s real GDP growth target at around 8%, our interpretation is that Chinese leaders are not looking to accelerate growth beyond where it ended in 2020. Major equity indexes are already richly valued. A moderating growth momentum from China will weigh on commodity and risk asset prices, both in China and globally. We reiterate our view that downside risks are high in the near term; the market could take the easing demand growth from China as a reason for a long overdue correction. A Perspective On Growth In 2021 Investors should put this year’s GDP growth projections into perspective given last year’s distortions in China’s economic conditions and data. On a YoY basis, data in the first quarter this year will be artificially boosted due to the deep contraction in Q1 last year. The market consensus is that Q1 2021 will register an 18% YoY rate of real GDP expansion. If we assume the economy can expand by 8% this year over 2020, then the YoY GDP growth rates in the rest of this year will average less than 6%. This would be below the 6.5% YoY rate in the fourth quarter of 2020 – meaning that on a YoY basis, China’s growth momentum has peaked (Chart 1). Importantly, sequential growth, such as month-over-month (MoM) and quarter-over-quarter (QoQ), drives the financial markets. On a QoQ basis, Q1 business activities are typically weaker due to the Chinese New Year. However, when we compare the rate of QoQ slowdown in Q1 this year with previous years, an 18% YoY increase would mean China’s output in the first three months of 2021 would be one of the worst in the past 20 years (Chart 2). Chart 1Q1 GDP Growth Will Be Artificially Boosted, On A YoY Basis

Q1 GDP Growth Will Be Artificially Boosted, On A YoY Basis

Q1 GDP Growth Will Be Artificially Boosted, On A YoY Basis

Chart 2…But Will Be On The Weaker Side, On A QoQ Basis

Understanding China’s Growth Arithmetic For 2021

Understanding China’s Growth Arithmetic For 2021

The moderating growth momentum in Q1 this year was already reflected in high-frequency data in January. Most major components in last week’s PMI surveys in both the manufacturing and service sectors had larger setbacks than in January of previous years. Prices in major commodities as well as the Baltic Dry Index softened (Chart 3). Cyclical sector stocks in China’s onshore market, which is highly sensitive to domestic economic policies, have halted their outperformance relative to defensive stocks (Chart 4). Chart 3Chinese Economic Growth May Be Showing Signs Of Moderation

Chinese Economic Growth May Be Showing Signs Of Moderation

Chinese Economic Growth May Be Showing Signs Of Moderation

Chart 4Outperformance In Onshore Cyclical Stocks Is Rolling Over

Outperformance In Onshore Cyclical Stocks Is Rolling Over

Outperformance In Onshore Cyclical Stocks Is Rolling Over

Furthermore, it is useful to look past the growth outliers in the previous four quarters to gain insight into the status of China’s business cycle. On a two-year smoothed term, an 8% annual output growth in 2021 would represent a continuation of China’s downward economic growth trend (Chart 5). Chart 5This Years Rebound In Headline GDP Growth Does Not Alter Chinas Structural Downtrend

This Years Rebound In Headline GDP Growth Does Not Alter Chinas Structural Downtrend

This Years Rebound In Headline GDP Growth Does Not Alter Chinas Structural Downtrend

Bottom Line: It is misleading to consider an 8% YoY real GDP growth rate in 2021 as an acceleration in China’s economic recovery. On a quarterly basis, Q1 will undergo a moderation in growth momentum. The economy in the rest of the year will remain on a downward growth trend. No Rush To Stimulate Anew If Q1 growth turns out to be weaker than the market anticipates, then will Beijing continue to dial back stimulus? Or, will it become concerned about the underlying fragility in the economy and provide more support? So far, all signs point to a continuation of a stimulus pullback. Chart 6Tighter Monetary Conditions are Starting To Bite the Economy

Tighter Monetary Conditions are Starting To Bite the Economy

Tighter Monetary Conditions are Starting To Bite the Economy

The resurgence of domestic COVID-19 cases contributed significantly to January’s shaky demand. However, tighter monetary conditions in 2H20 are likely another reason for the growth moderation (Chart 6). Here are some factors that may have prompted Chinese authorities to stay on track to scale back stimulus: Policymakers appear to consider the massive fiscal stimulus last year overdone. In contrast with the previous two years, local governments are not issuing special-purpose bonds (SPBs) before the NPC sets its quota in early March. China’s broader fiscal budgetary deficit widened to 11% of GDP in 2020 from 6% in 2019. Local governments issued nearly 70% more SPBs in 2020 than in the previous year (Chart 7). SPBs are mostly used for investing in infrastructure projects and last year’s fiscal support along with substantial credit expansion helped to speed up infrastructure investment. However, towards the end of last year local governments reportedly experienced a shortage in profitable investment projects and thus, parked more than 400 billion yuan of proceeds from last year’s SPB issuance at the central bank (Chart 8). This will likely convince the central government to reduce the SPB quota by a large margin this year. Chart 7Fiscal Stimulus Last Year May Be Overdone

Fiscal Stimulus Last Year May Be Overdone

Fiscal Stimulus Last Year May Be Overdone

Chart 8Local Governments Reportedly Ran Out Of Profitable Infrastructure Projects To Invest Last Year

Local Governments Reportedly Ran Out Of Profitable Infrastructure Projects To Invest Last Year

Local Governments Reportedly Ran Out Of Profitable Infrastructure Projects To Invest Last Year

In addition, government revenues in 2020 were surprisingly strong and spending was well below budgeted annual expenditures, resulting in 2.5 trillion yuan in idle funds (Chart 9). Based on China’s fiscal budget laws, any unspent funds from the previous year will be carried over to the next year. In other words, the 2.5 trillion yuan will contribute to fiscal deficit reduction this year and are not extra savings that can be distributed. In addition, asset price bubbles are a perennial concern. Land sales and housing demand for top-tier cities roared back last year due to cheap loans and a relaxed policy environment (Chart 10). In our opinion, Chinese leaders allowed the real estate market to temporarily heat up last year to avoid a deep economic recession. As the economy recovered to its pre-pandemic level by late 2020, policymakers have sharply reduced their tolerance for the booming housing market and substantially tightened restrictions in the real estate sector. Chart 9Unspent Fiscal Stimulus Checks Do Not Lead To Higher Government Spending Next Year

Unspent Fiscal Stimulus Checks Do Not Lead To Higher Government Spending Next Year

Unspent Fiscal Stimulus Checks Do Not Lead To Higher Government Spending Next Year

Chart 10Housing Market Heats Up Again

Housing Market Heats Up Again

Housing Market Heats Up Again

The domestic labor market has been surprisingly resilient, removing the leadership’s political constraints and incentives to further stimulate the economy. Labor market conditions and household income are improving. The gap between household disposable income and spending growth has narrowed, the unemployment rate is back to its pre-pandemic level and consumer confidence has rebounded (Chart 11). More importantly, China’s labor market in urban areas is tightening again, with migrant workers receiving higher pay than prior to the pandemic (Chart 12). Chart 11Labor Market Is On The Mend

Labor Market Is On The Mend

Labor Market Is On The Mend

Chart 12China’s Urban Labor Market Is Tightening Again

Understanding China’s Growth Arithmetic For 2021

Understanding China’s Growth Arithmetic For 2021

Bottom Line: Growth rates will moderate, but policymakers will wait for more evidence of a pronounced slowdown in economic conditions before they ease policies. Concerns about financial risks and excesses in the property market entail authorities to allow stimulus of 2020 to relapse. It will take a much deeper slowdown in the business cycle before easing is re-introduced. Investment Implications Our baseline view indicates that credit growth will decelerate by two to three percentage points in 2021 from 2020, and the local government SPB quota will drop by 10%. The projected pullbacks on stimulus are small and more measured than the last policy tightening cycle in 2017/18. Nevertheless, a smaller stimulus and tighter policy environment will consequently lead to moderating growth momentum in China’s domestic economy and demand, particularly in the second half of this year. Chart 13How Far Can Chinas Inventory Restocking Cycle Go Without More Policy Tailwinds

How Far Can Chinas Inventory Restocking Cycle Go Without More Policy Tailwinds

How Far Can Chinas Inventory Restocking Cycle Go Without More Policy Tailwinds

Commodity prices may be at high risk of easing demand. The strong rebound in China’s commodity imports in 2H20 was not only due to a recovery in domestic consumption, but also inventory restocking from an extremely low level. Chart 13 shows that the change in China’s industrial inventories relative to exports has risen substantially from a two-year contraction. Going forward, the pace of inventory accumulation will slow following a weaker policy tailwind and growth momentum, which will weigh on the demand for and prices of key industrial raw materials. Corporate profits should continue to recover, albeit at a slower rate than in 2H20. At the same time, risks are tilted to the downside, and policy initiatives should be closely monitored going forward. As such, we maintain a cautious view on Chinese stocks. Jing Sima China Strategist jings@bcaresearch.com Footnote: 1 IMF World Economic Outlook and World Bank Global Outlook, January 2021 Footnotes Cyclical Investment Stance Equity Sector Recommendations

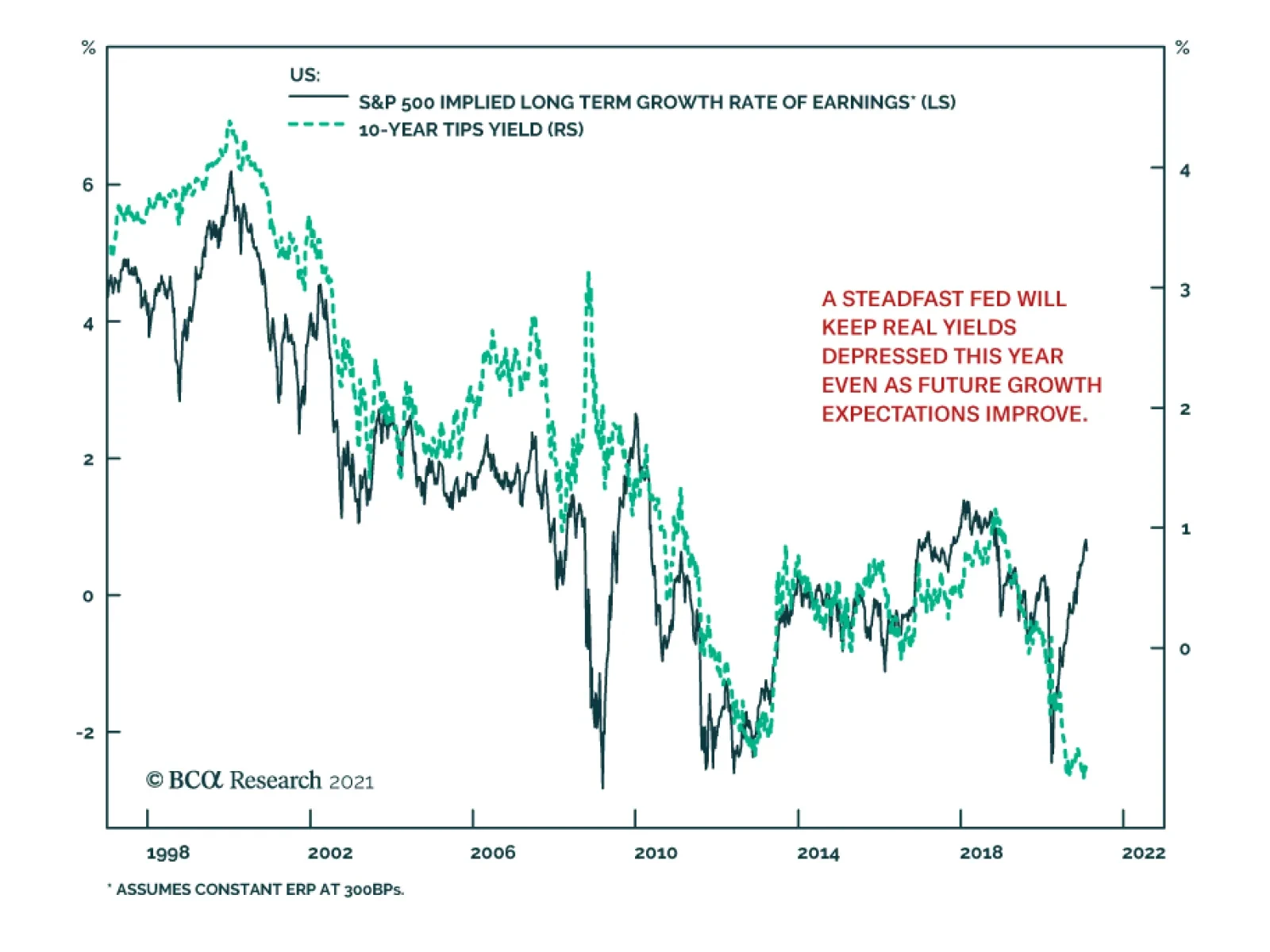

The long-term outlook for earnings growth and the 10-year TIPS yield typically move in tandem because they are both driven by expectations of future growth. However, this long-standing relationship has recently broken down. The 10-year TIPS yield has remained…

Highlights US inflation expectations will continue to grind higher as commodity markets tighten, and financial markets price to an ultra-accommodative Fed over the next 2-3 years. The US stock-market rally is reducing equity yields and squeezing equity risk premiums, which acts as a drag on gold prices. Higher earnings, lower stock prices or both are needed to reduce this effect. Pandemic uncertainty continues to fuel safe-haven demand for the USD, which remains a headwind for gold and silver. Vaccination availability needs to reach a level that convinces markets global contagion risk has been minimized. Until then, this remains the dominant downside risk to gold and commodities. The balance of risks continues to favor gold: US real rates will remain weak as the Fed remains behind the inflation-vs-rates curve, and the USD will be pushed lower (Chart of the Week). We continue to expect gold prices to push to $2,000/oz. We remain bullish silver, and view the recent retail-spec price blip as transitory. Fundamentally, silver supply growth is weakening, and demand is strengthening as the renewable-energy buildout accelerates and consumer spending revives. We expect silver's price to trade back to $30/oz. Feature US inflation expectations will continue to grind higher, as tightening markets for industrial commodities push oil and base metals prices higher (Chart 2).1 As is apparent in Chart 2, these real-economy factors feed directly into five-year inflation expectations, which are important to policy makers and portfolio managers managing risk in trading markets.2 Continued Fed accommodation of massively expansive US fiscal policy also will stoke inflation expectations, and keep real rates negative or weak at low positive levels as realized inflation and inflation expectations increase. These real and financial effects will be positive for gold prices, as the Chart of the Week illustrates. Chart of the WeekRising Inflation Expectations vs. Falling Risk Premiums Restrain Gold

Rising Inflation Expectations vs. Falling Risk Premiums Restrain Gold

Rising Inflation Expectations vs. Falling Risk Premiums Restrain Gold

Chart 2Tightening Commodity Markets Push Inflation Expectations Higher

Tightening Commodity Markets Push Inflation Expectations Higher

Tightening Commodity Markets Push Inflation Expectations Higher

Battling against this tailwind is the historic US equity rally, which has crushed stock yields and the equity risk premium vs bond yields.3 Gold prices are positively correlated with equity risk premiums – the positive economic forces that push dividend yields higher also tend to push gold and commodity prices higher – which means the falling risk premiums are acting as a headwind to gold prices (Chart 3).4 If, as the global economy recovers, the rate of growth in earnings is greater than that of equity prices, stock yields will expand, which will be supportive of gold prices. That said, we do not expect the contraction of the equity risk premium to dominate the evolution of gold prices. Tightening fundamentals in the real economy and continued monetary accommodation at the Fed will dominate gold- and silver-pricing dynamics. Chart 3Falling Stock Yields Pressure Equity Risk Premiums

Falling Stock Yields Pressure Equity Risk Premiums

Falling Stock Yields Pressure Equity Risk Premiums

Balance of Risks Favors Gold Fed policy pronouncements point to continued accommodation of massive fiscal stimulus in the US, with the central bank strongly indicating it will, as a matter of policy, remain behind the inflation-vs-rate-hikes curve for at least another 2-3 years. Taking the Fed at its word, this means US real rates will remain weak, and the USD will be pushed lower as the central bank continues to accommodate higher US budget deficits at the federal level. However, as we have repeatedly noted, the broad trade-weighted USD has found strong support at current levels following a precipitous fall from its COVID-19-induced highs in 1Q20: As pandemic uncertainty feeds into global policy uncertainty, USD safe-haven demand remains elevated (Chart 4).5 While we concentrate on five-year inflation expectations in our modeling, indications of price pressures are showing up in the manufacturing sector in the US (Chart 5), as our colleagues in BCA Research’s US Bond Strategy note in their report this week.6 This confirms that the price strength seen in commodity markets for raw materials used in manufacturing are showing up in the economy as a whole. Chart 4Lower USD, Stronger GDP Bullish For Copper Prices

Lower USD, Stronger GDP Bullish For Copper Prices

Lower USD, Stronger GDP Bullish For Copper Prices

Chart 5Inflation Indicators Hook Up

Inflation Indicators Hook Up

Inflation Indicators Hook Up

Our price target for gold remains $2,000/oz. The sooner vaccines are deployed globally – so that markets can reasonably assign lower odds to a resurgence of COVID-19 and its more insidious variants forcing new lockdowns – the sooner the pandemic uncertainty keeping the USD well bid will dissipate as a fundamental factor restraining a continuation of gold’s rally. Silver Is Not GameStop The Reddit-powered surge in retail silver trading this past week, which lifted silver prices some ~ 11% on Monday to $30/oz, is all but a memory now that the white metal is again pricing in line with fundamentals. We turned bullish silver in July of last year, arguing fundamentals suggested silver could outperform gold in 2H20, which it did.7 Supportive fundamentals remain in place, with total supply (mine output and recycling) falling, demand rising and balances tightening (Chart 6). We expect the supply side of the market to remain under pressure this year and the next, given the physical deficits we are forecasting for the copper market over the next two year: The supply side of silver is a function of copper, zinc and lead mine output (i.e., silver largely is a byproduct). On the demand side, continued recovery of consumer spending and the decade-long buildout of renewable-energy generation – which is heavily reliant on copper and silver to a lesser degree – will force prices higher. We remain bullish silver. However, given our expectation its price will trade again to $30/oz, we do not expect any dramatic tightening of the gold/silver ratio this year (Chart 7). Chart 6Silver Market Tightens, Along With Other Commodities

Higher Inflation Expectations Battle Lower Risk Premia In Gold Markets

Higher Inflation Expectations Battle Lower Risk Premia In Gold Markets

Chart 7Expect Gold/Silver Ratio To Continue To Narrow

Expect Gold/Silver Ratio To Continue To Narrow

Expect Gold/Silver Ratio To Continue To Narrow

Bottom Line: Tightening commodity fundamentals and continued monetary accommodation at the Fed will dominate gold- and silver-pricing dynamics this year and the next. The contraction of the equity risk premium will not dominate the evolution of gold prices. At the margin, if earnings growth exceeds equity-price increases, equity yields will expand, which will support gold prices. We expect gold and silver to trade to $2,000/oz and $30/oz this year – i.e., close to ~ 10% gains for both. Therefore, we do not expect much movement in the gold/silver ratio this year Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Bullish OPEC 2.0’s Joint Technical Committee (JTC) lowered its estimated demand growth for 2021 to 5.6mm b/d from its 5.9mm b/d estimate last month, at its Tuesday meeting. The JTC also is expecting the oil market to be in a deficit this year, which will, by the Committee’s estimate, peak at 2mm b/d in May 2021, according to reuters.com. This is in line with our maintained hypothesis that the producer coalition led by Saudi Arabia and Russia will continue to calibrate production in line with demand to keep global storage levels drawing. The JTC was not expected to recommend any change in production policy to oil ministers on Wednesday when they met. We expect OECD oil inventories to hit their rolling five-year average in 1H21, largely because of OPEC 2.0’s production discipline and production losses outside the coalition (Chart 8). Base Metals: Bullish Battery-grade lithium carbonate soared 40% y/y in January in China to $9,450/MT, according to mining.com. The reporting service noted strong demand for lithium iron phosphate (LFP) batteries used to power subsidized short-range autos, public transport infrastructure electrification, and power generation. Precious Metals: Bullish COVID-19-induced demand destruction pushed gold demand down 14% y/y in 2020, to just under 3,760 tons, according to the World Gold Council’s 2020 supply-demand tallies. At 4,633 tons, gold supply lost 4% y/y, the most since 2013, according to the WGC. Supplies were disrupted by COVID-19 as well. (Chart 9). Ags/Softs: Neutral Despite poor weather conditions in South America, US farmers are beginning to worry about record or near-record crops in the current growing season, according to farmprogress.com. grains are trading lower following recent rallies on concerns the upcoming harvest could be better than expected. Tomorrow’s USDA WASDE report will be eagerly awaited for the Department’s latest assessments. Chart 8OPEC 2.0 Keeps Supply Growth Below Demand Growth

OPEC 2.0 Keeps Supply Growth Below Demand Growth

OPEC 2.0 Keeps Supply Growth Below Demand Growth

Chart 9Gold Below 200 Day Moving Average

Gold Below 200 Day Moving Average

Gold Below 200 Day Moving Average