Inflation/Deflation

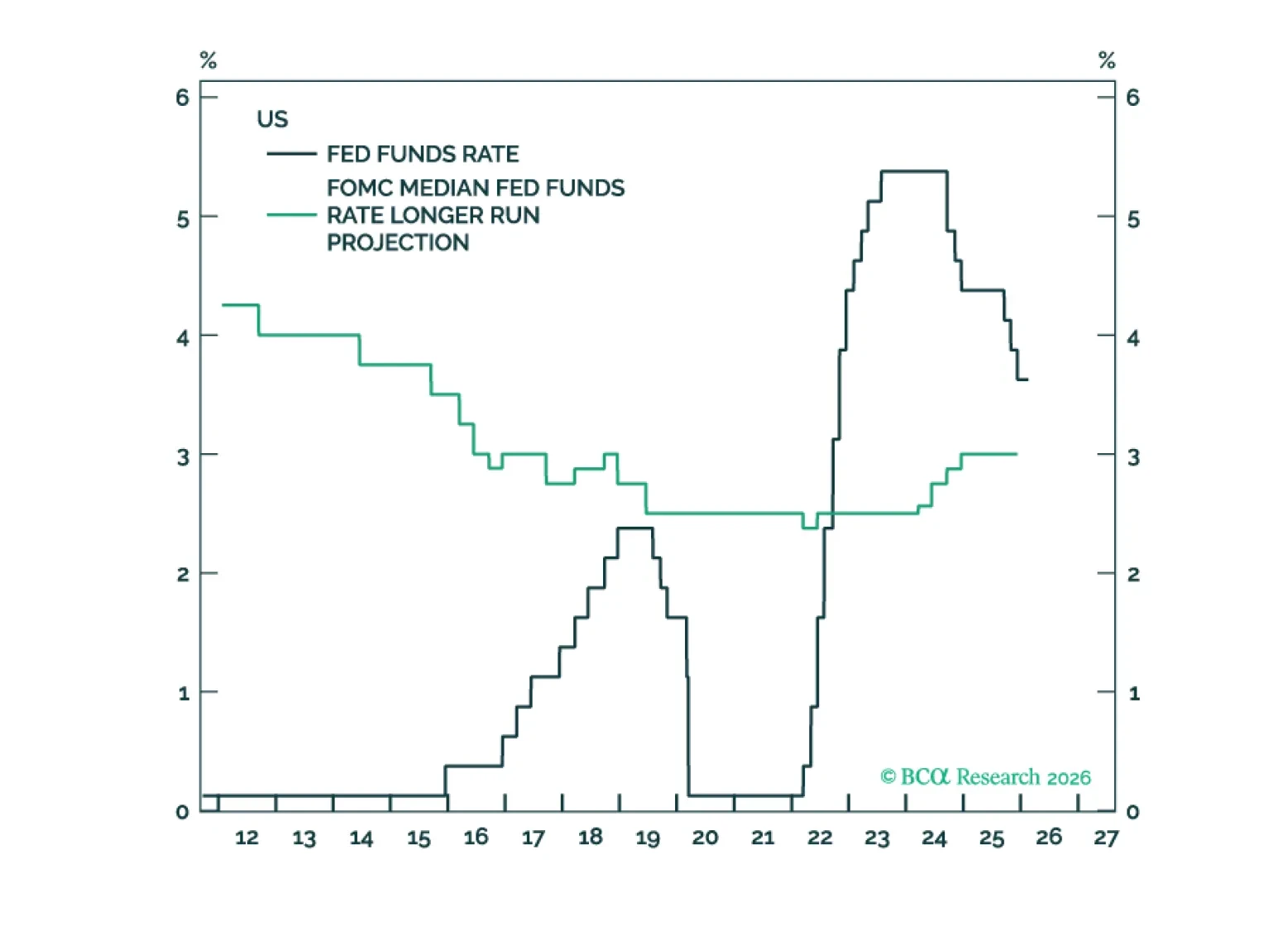

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

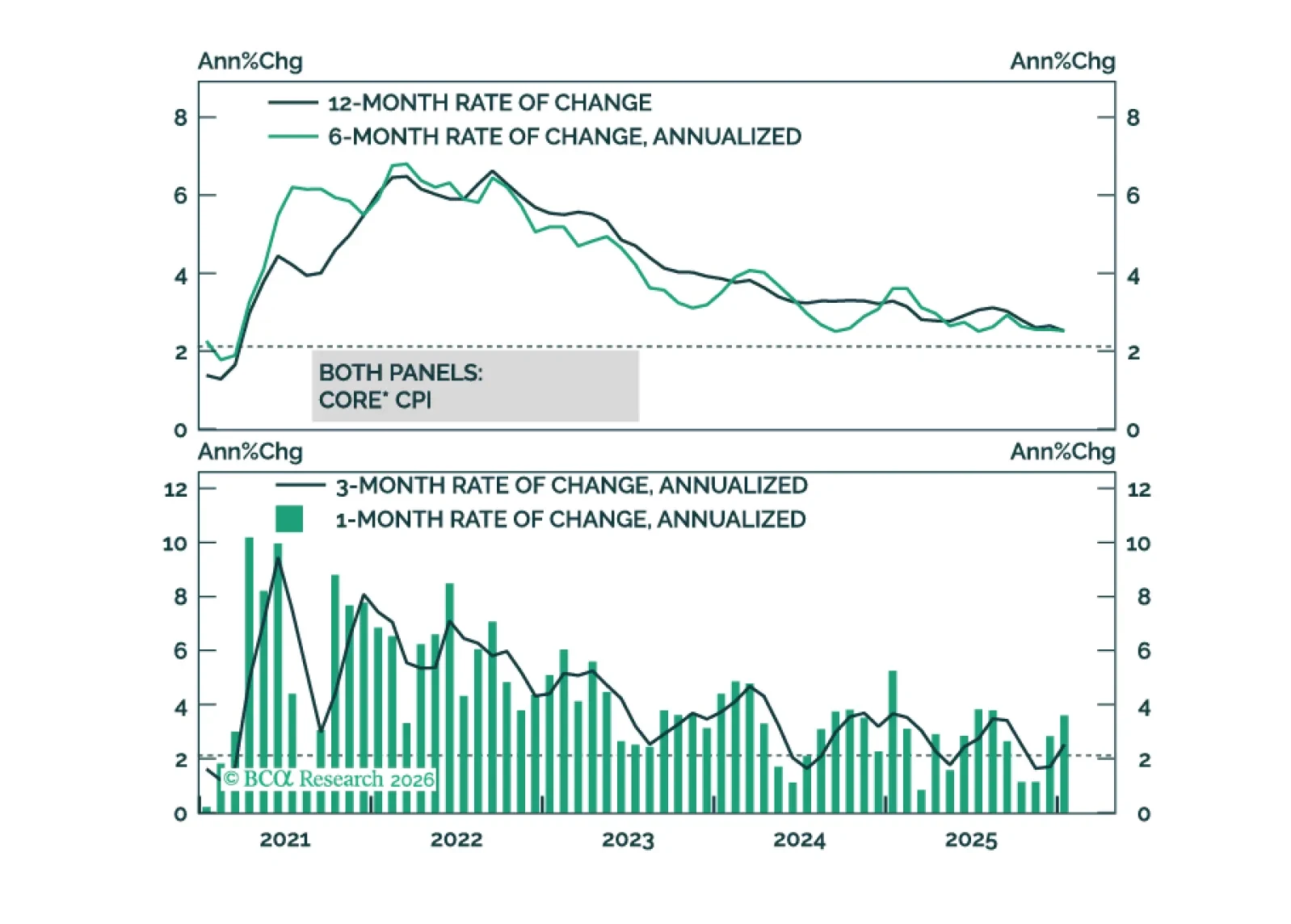

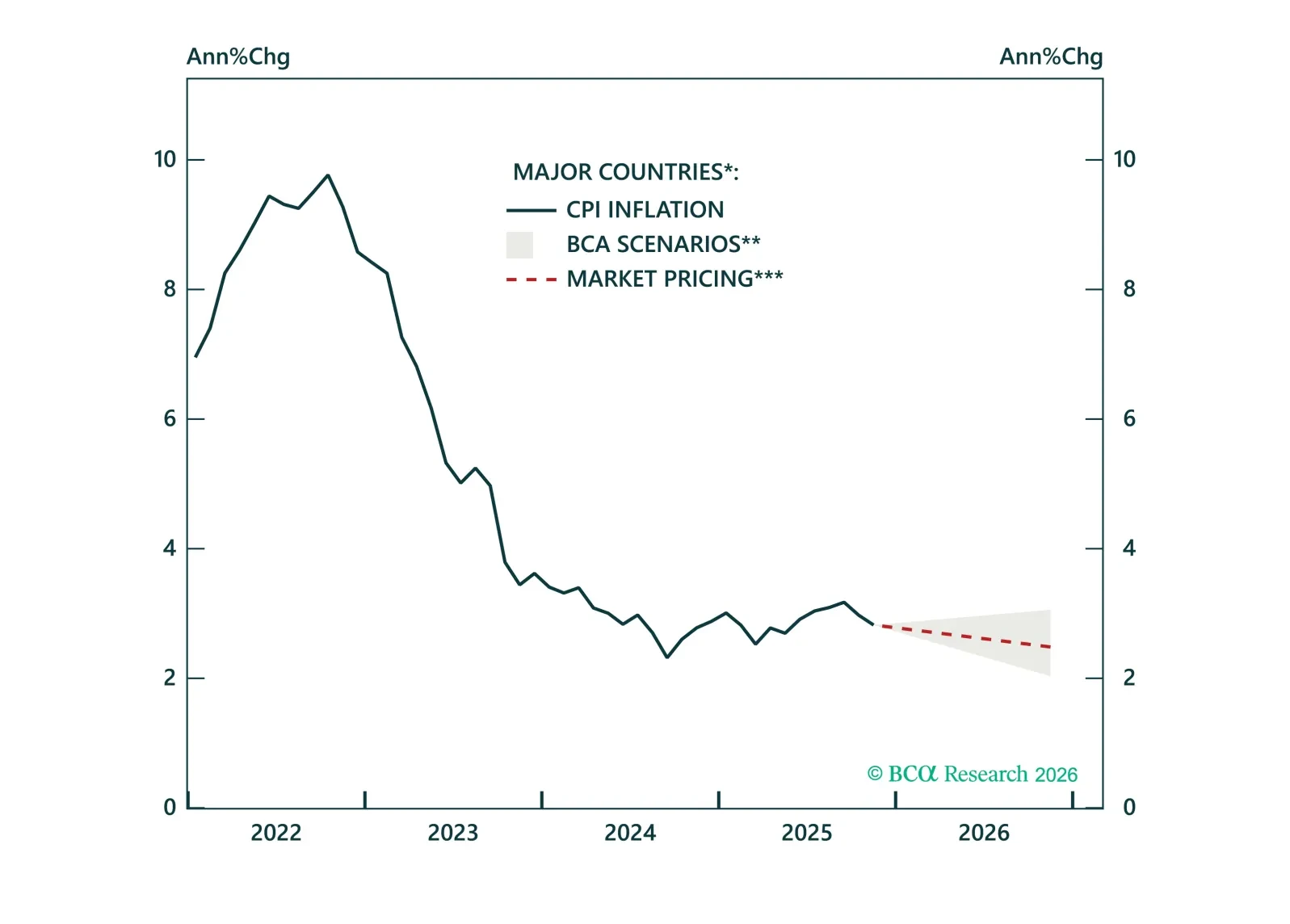

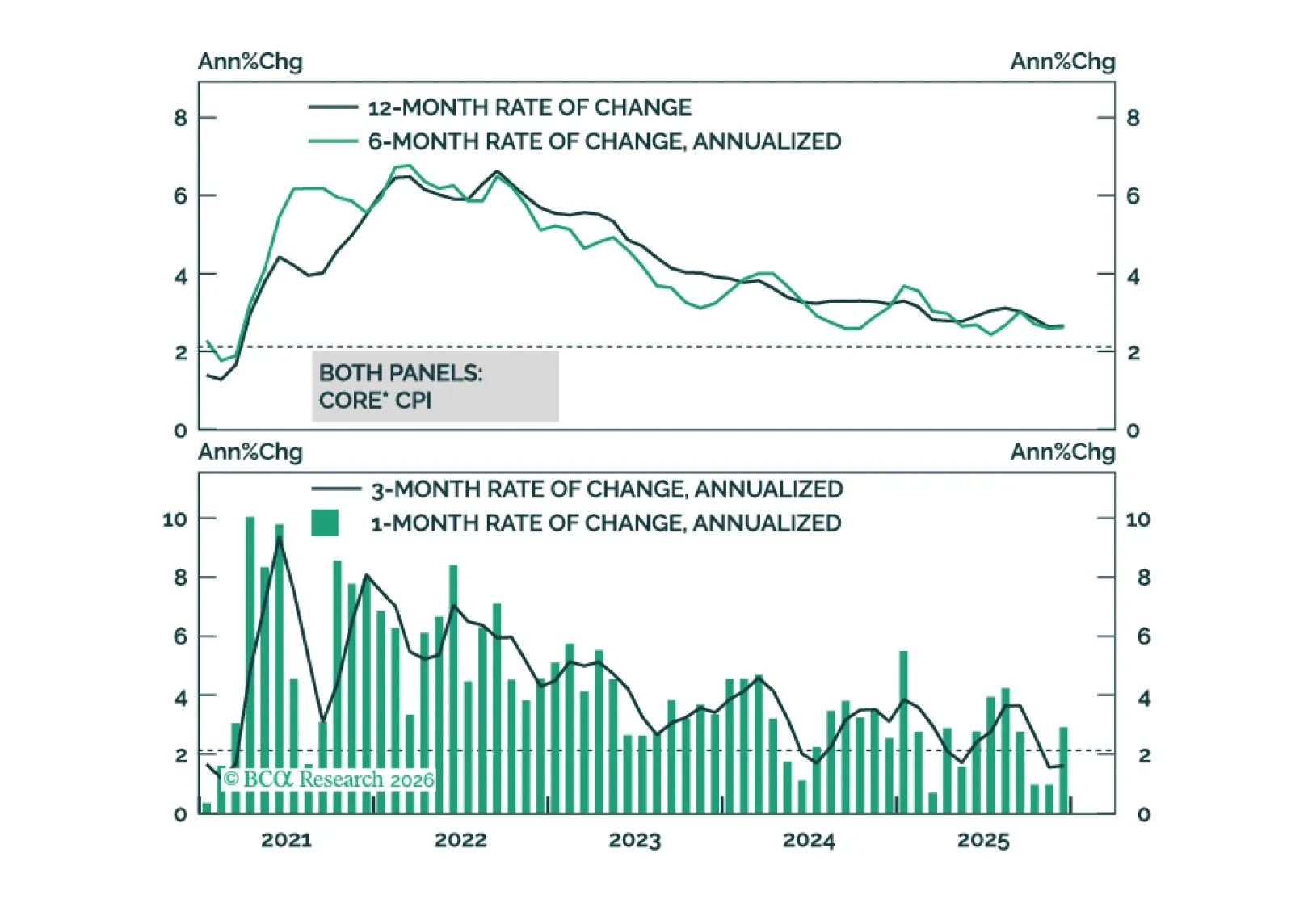

Core inflation will get close to the Fed’s 2% target by the end of this year.

Our Portfolio Allocation Summary for February 2026.

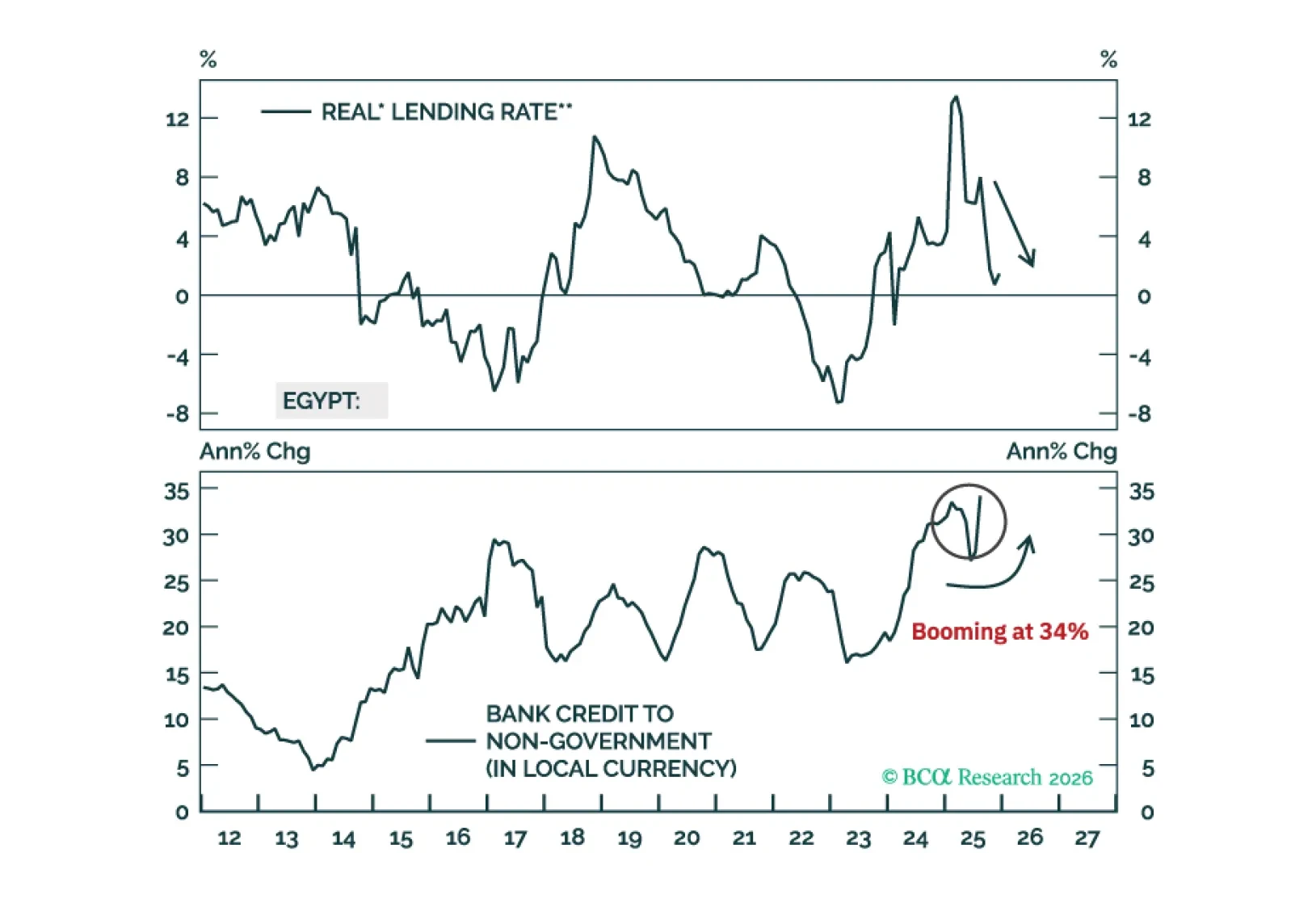

Egypt’s underlying inflation pressures are much higher than the headline CPI numbers imply. Real interest rates have plunged. As such, domestic bond yields have stayed high for a reason. Steer clear.

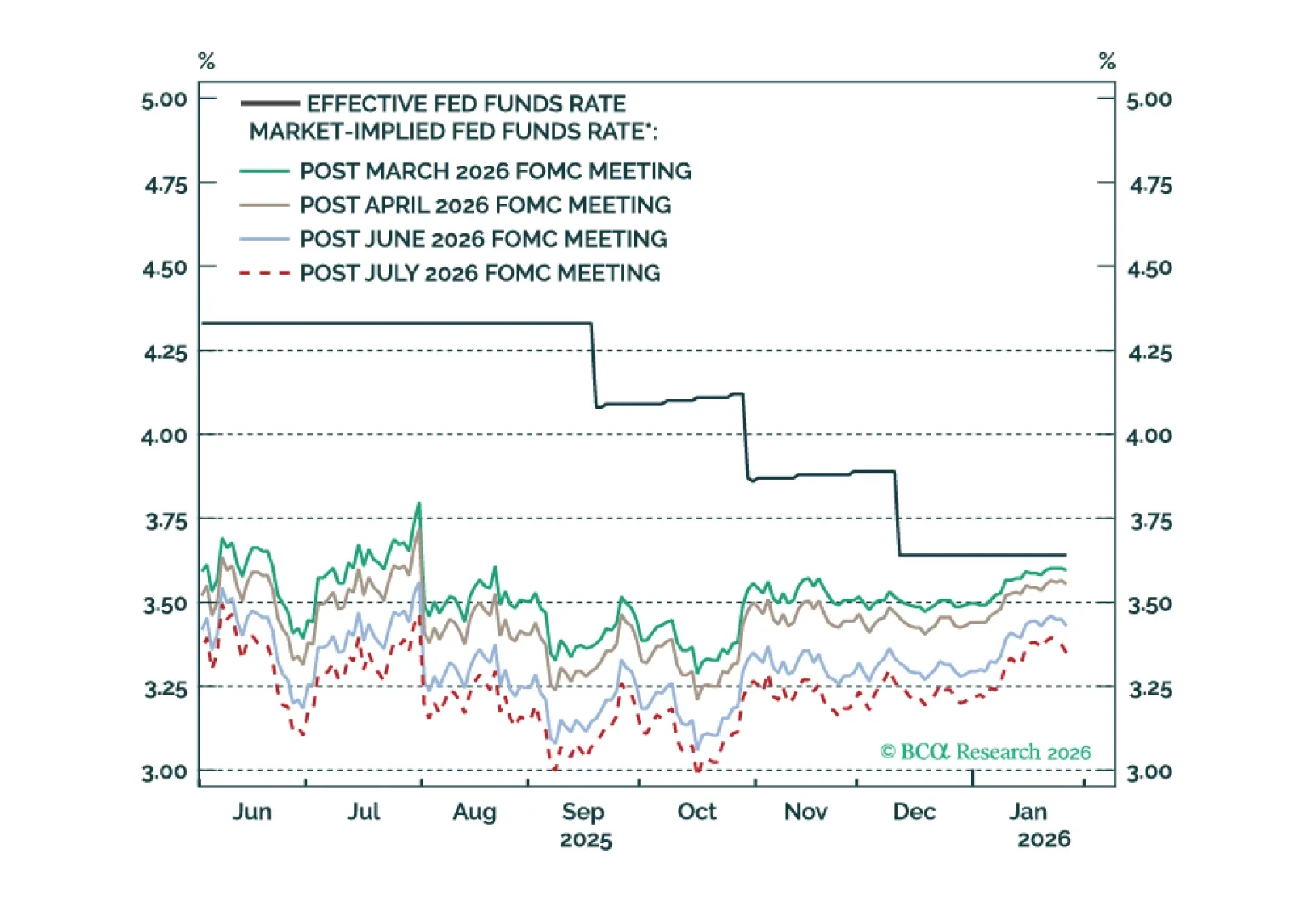

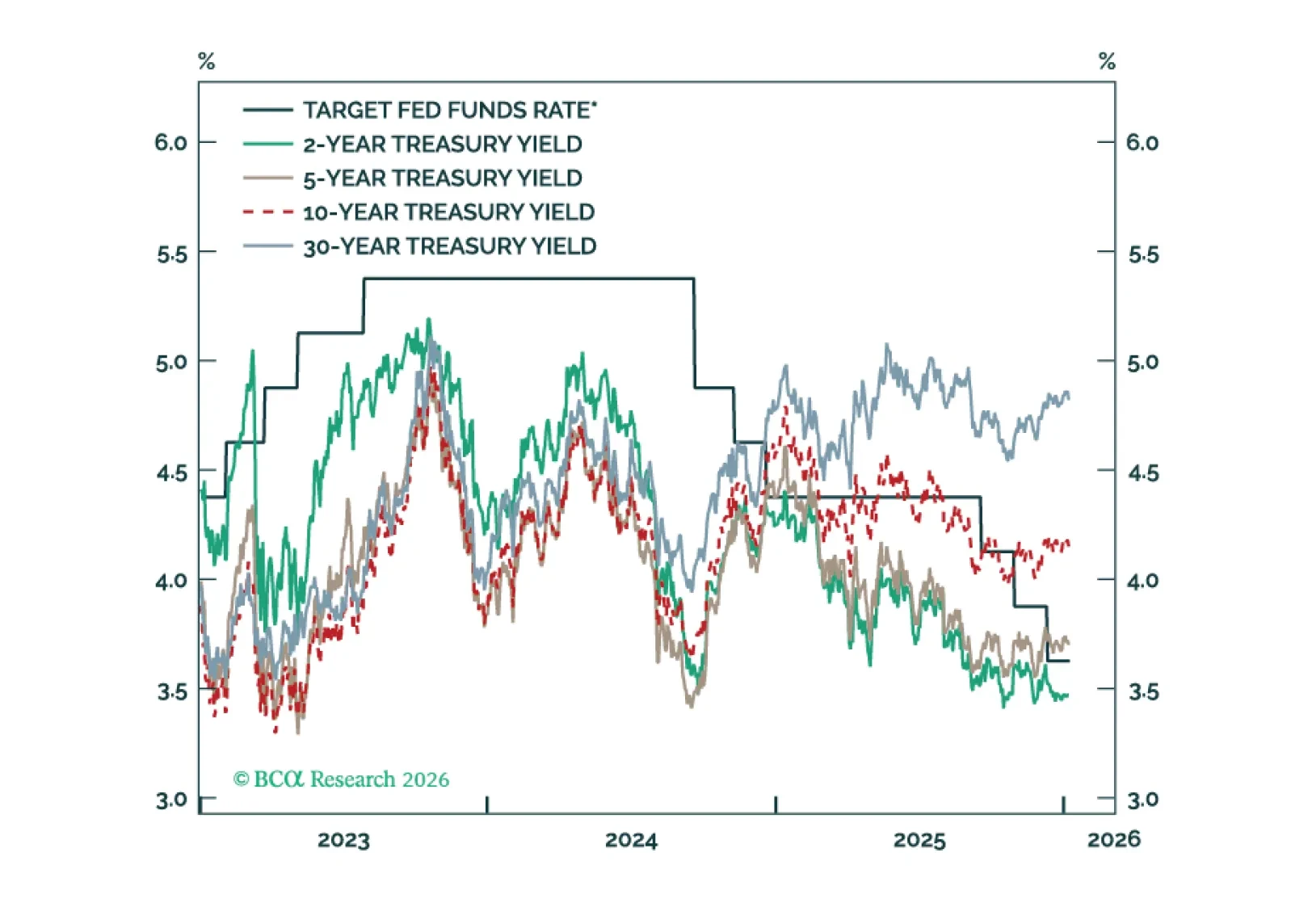

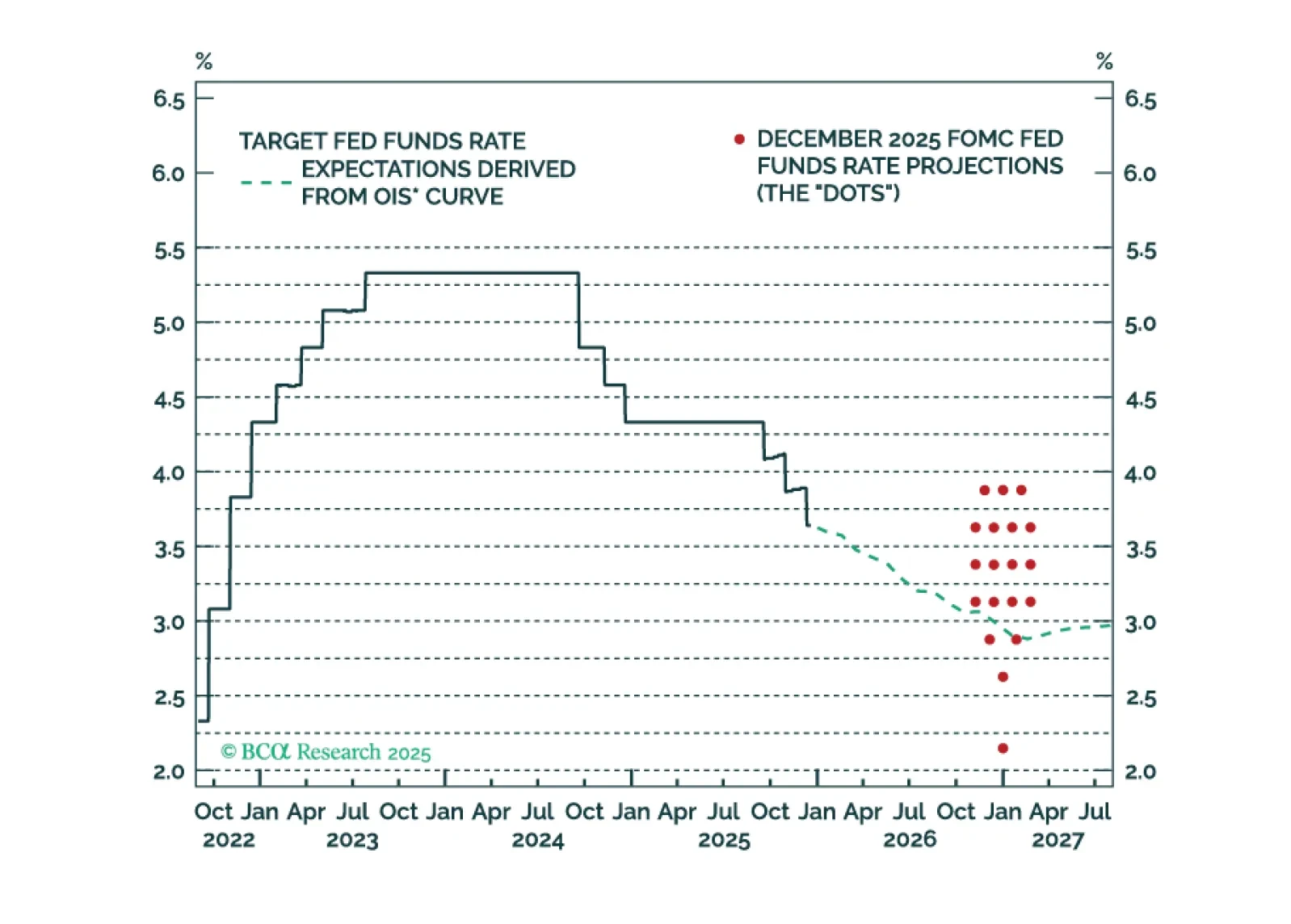

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

In our 2026 inflation outlook, we explain why 2026 will bring more disinflation, upside risks remain contained, and how to position in ILBs across major markets.

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

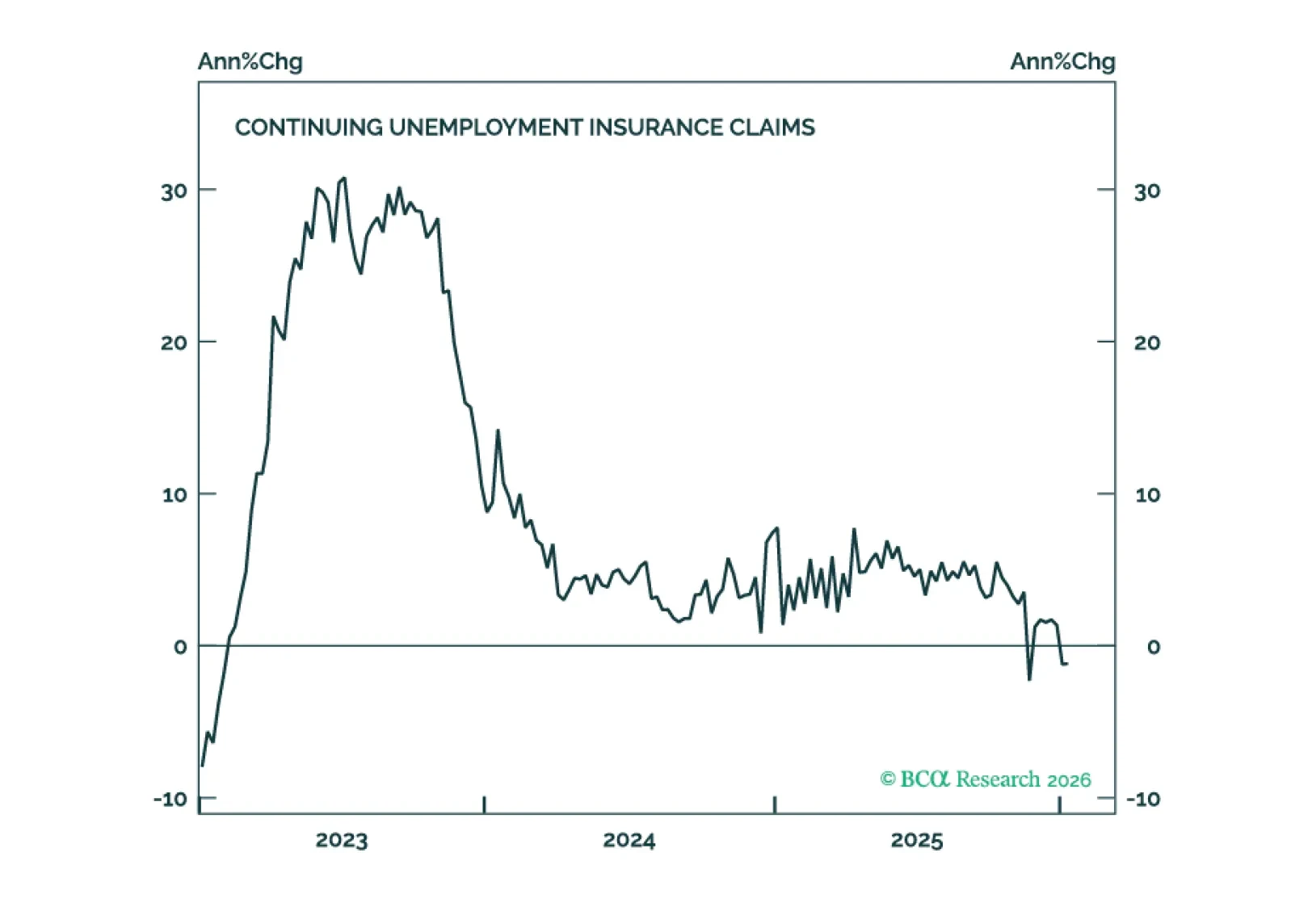

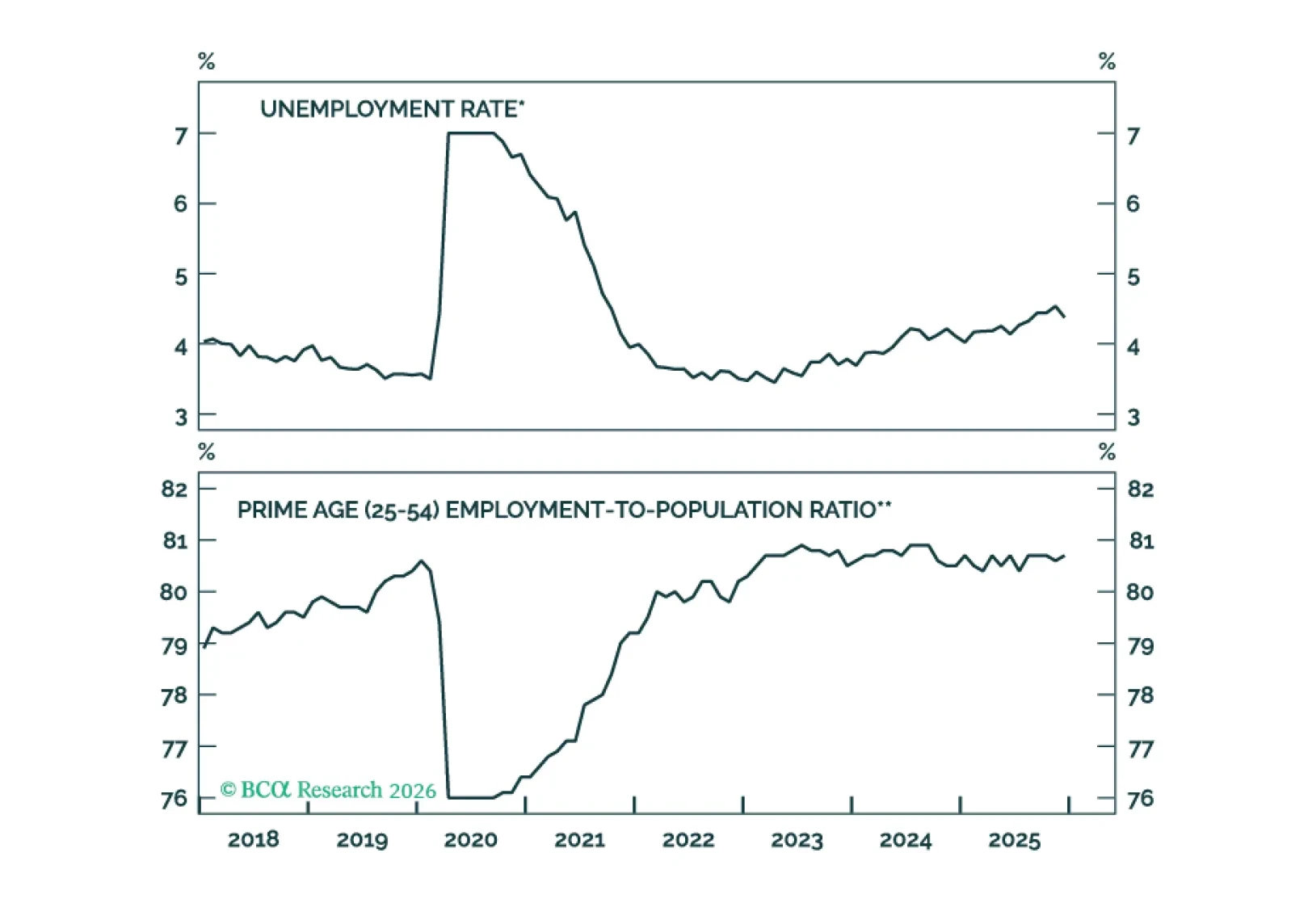

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

Our Portfolio Allocation Summary for January 2026.

Our outlook for Fed policy in 2026.