Inflation/Deflation

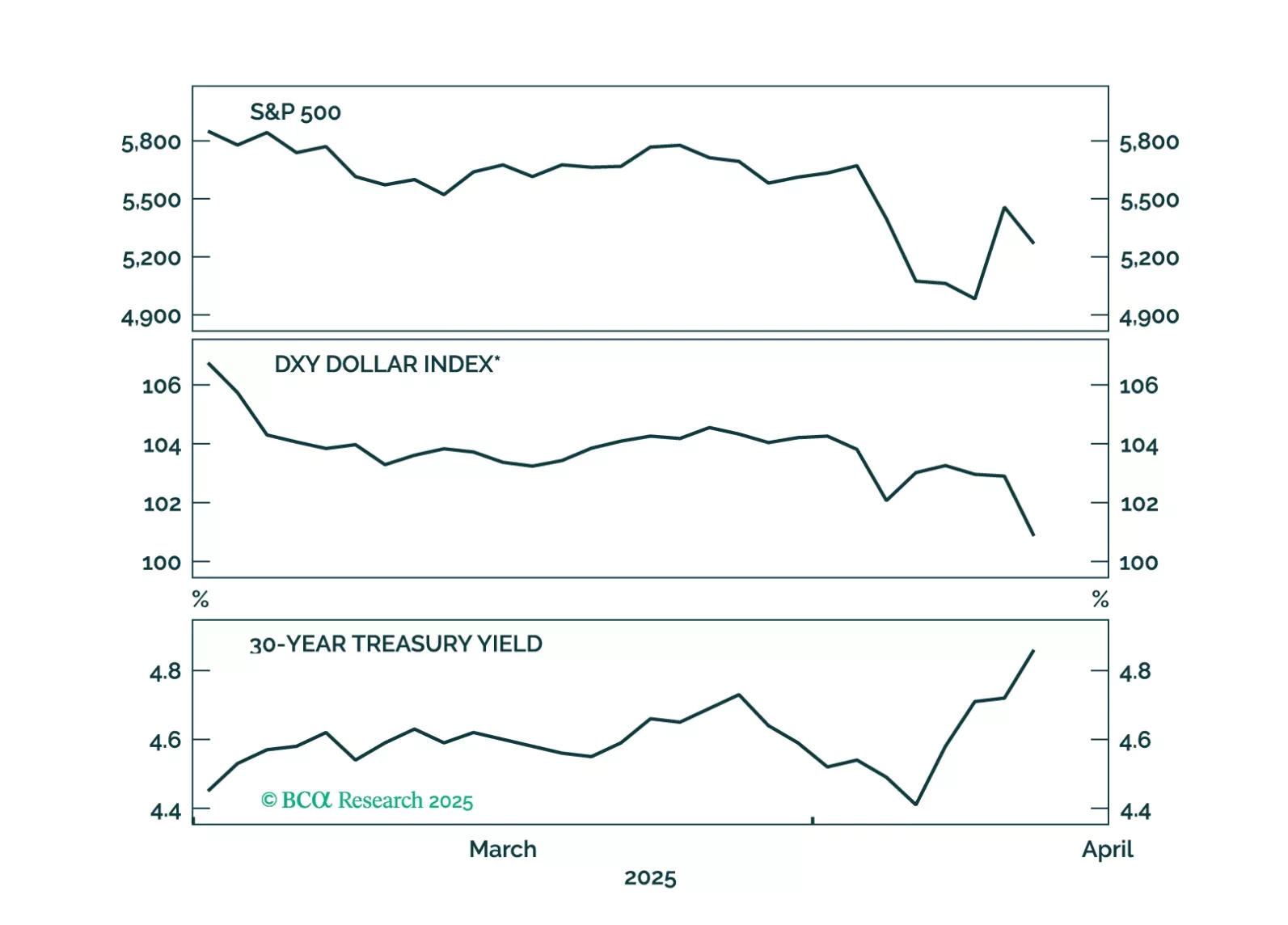

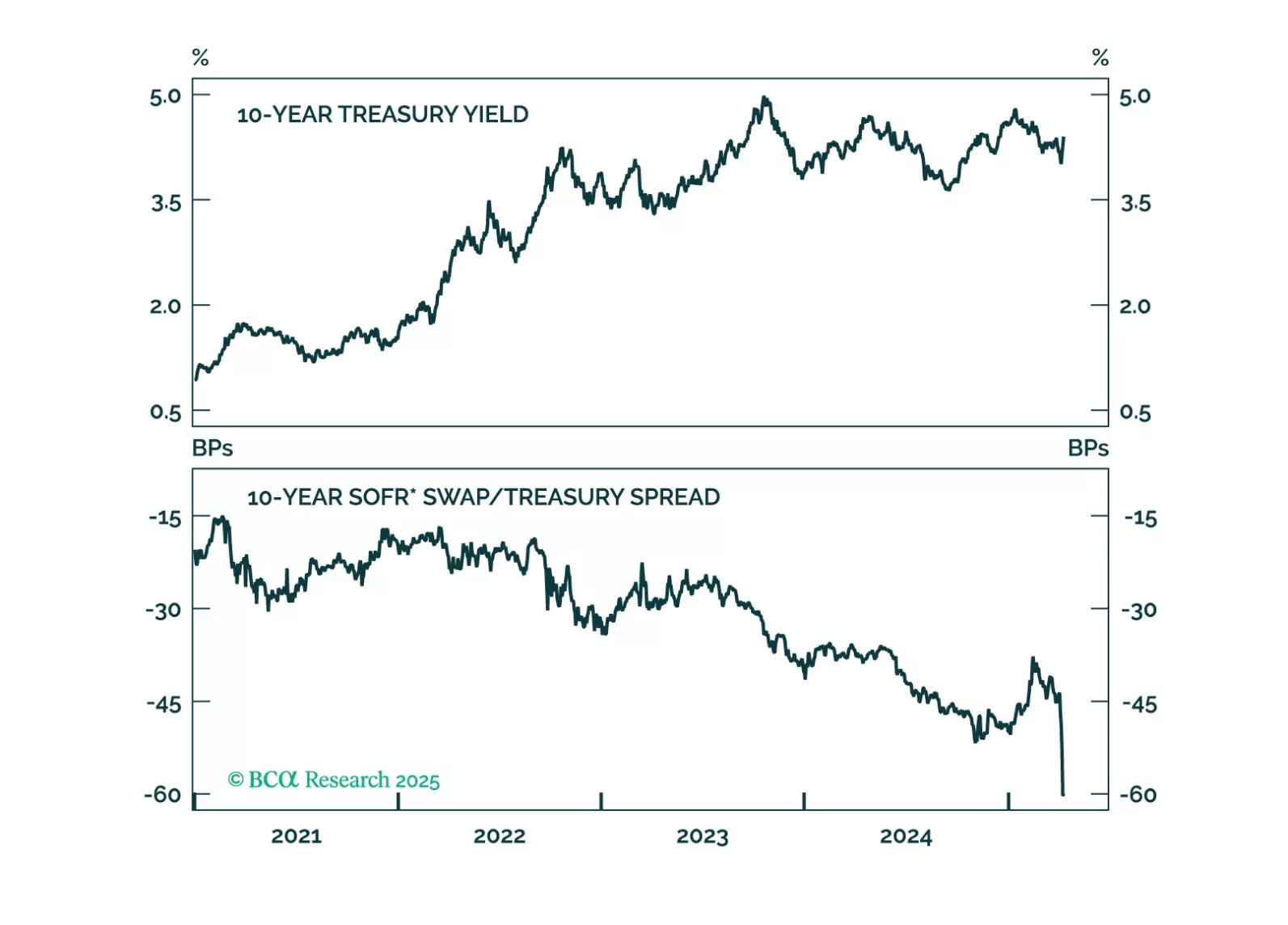

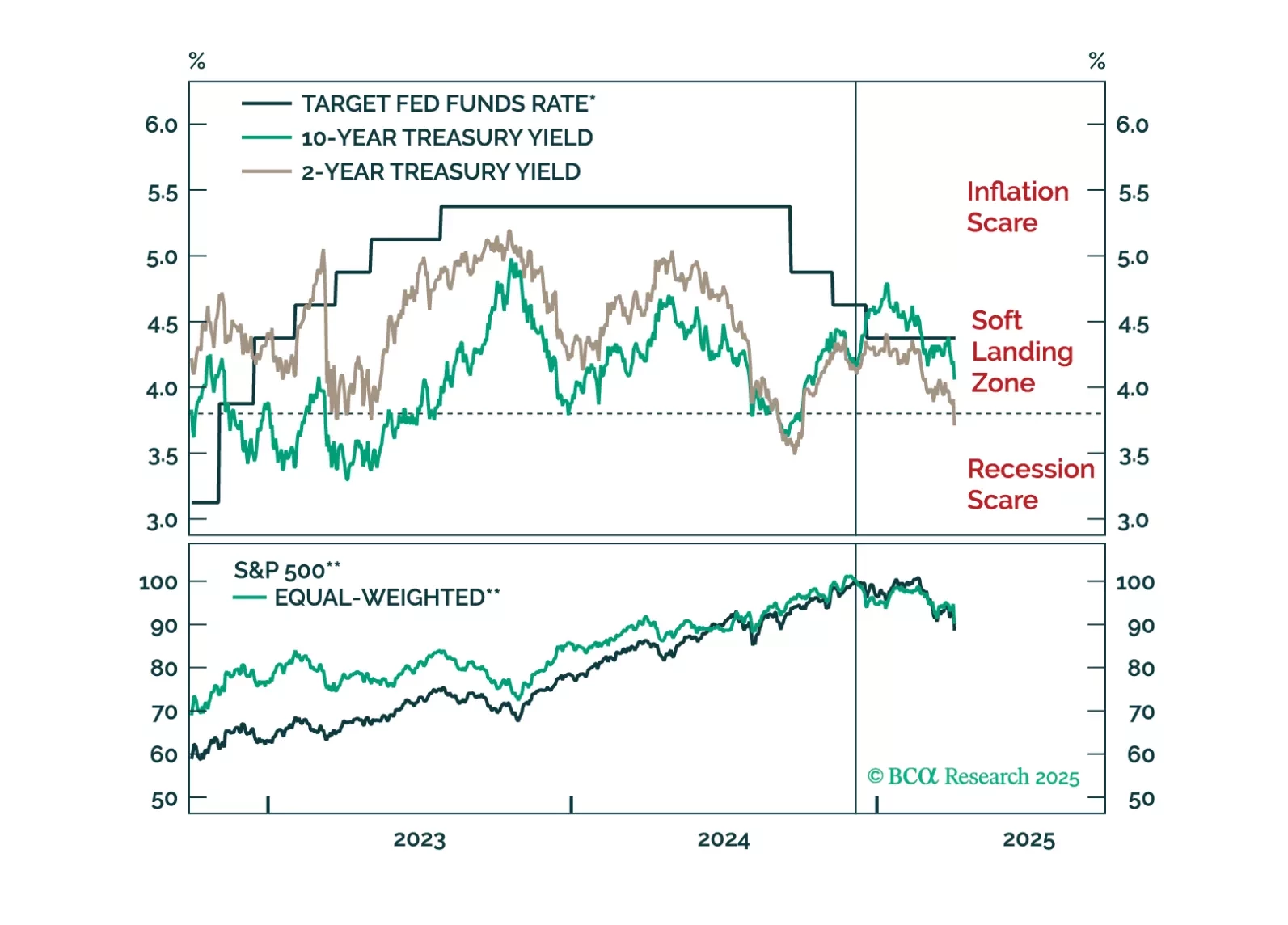

The combination of dollar weakness and rising US yields suggests global investors are questioning the safe-haven status of US Treasuries.

Our Portfolio Allocation Summary for April 2025.

The stimulus measures driving the post-COVID expansion were beginning to wane after five years and pointing the economy in the direction of an organically occurring recession. Now that DOGE and the multi-front trade war have sped up the timetable, we reiterate our risk-off recommendations.

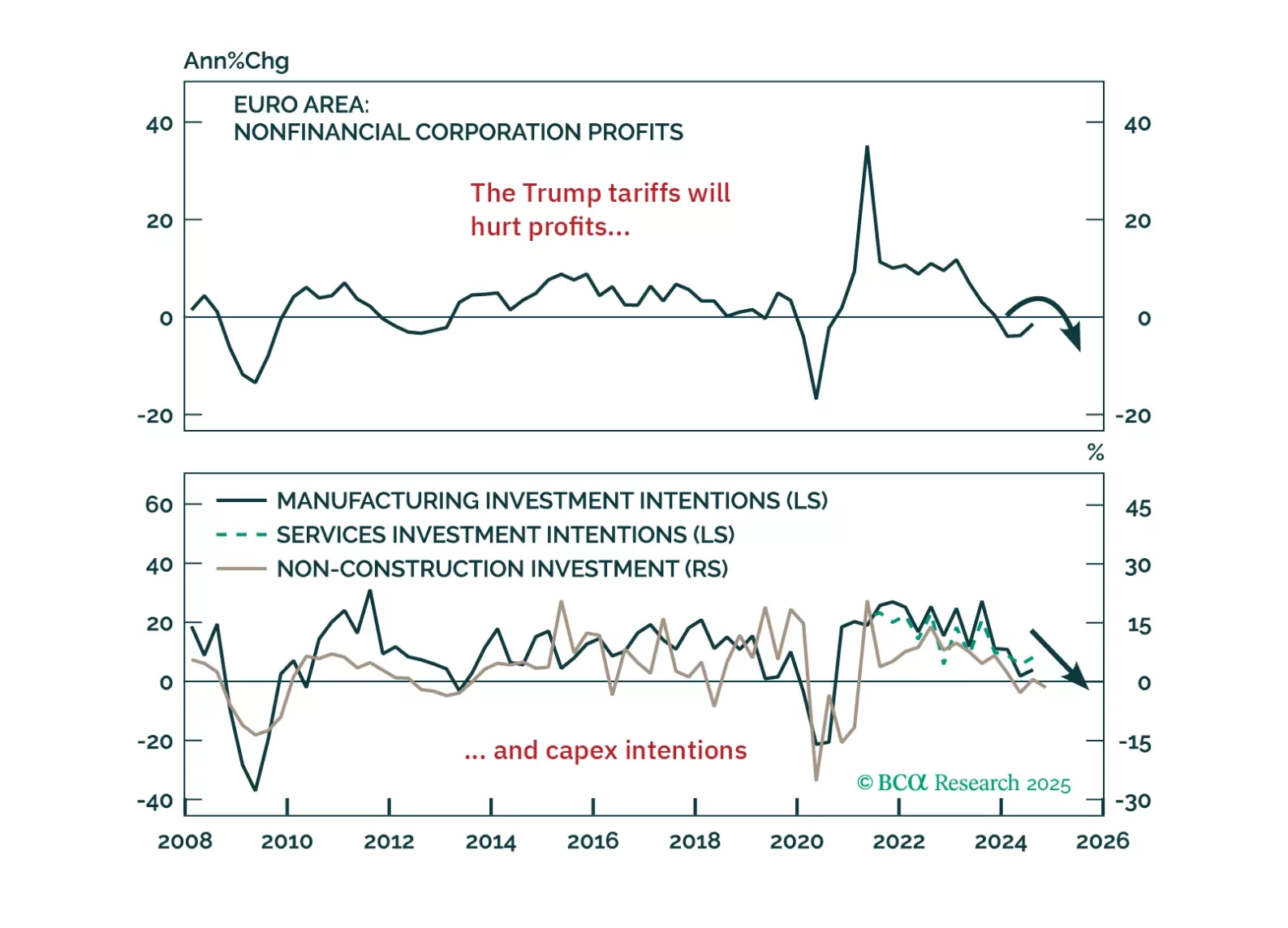

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

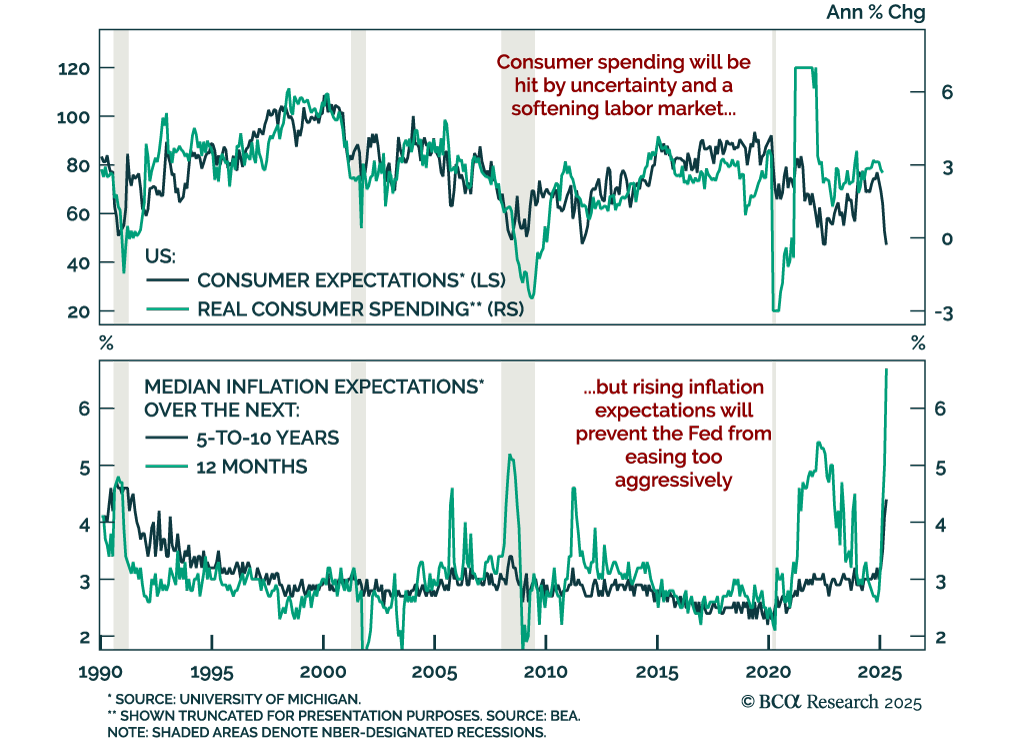

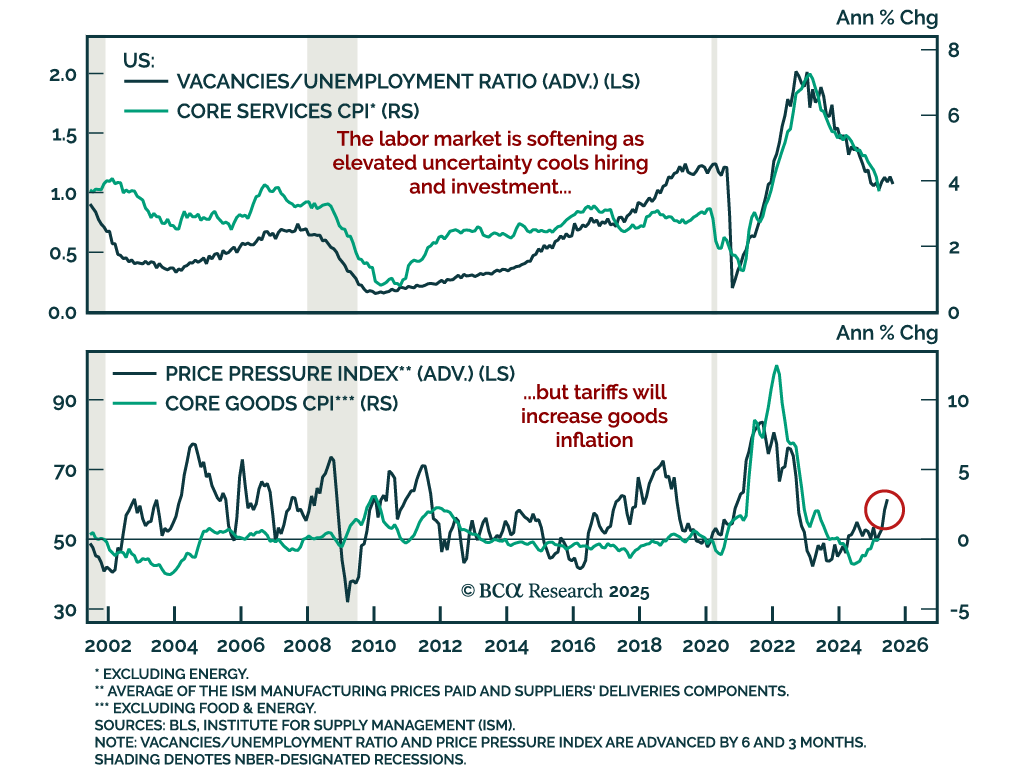

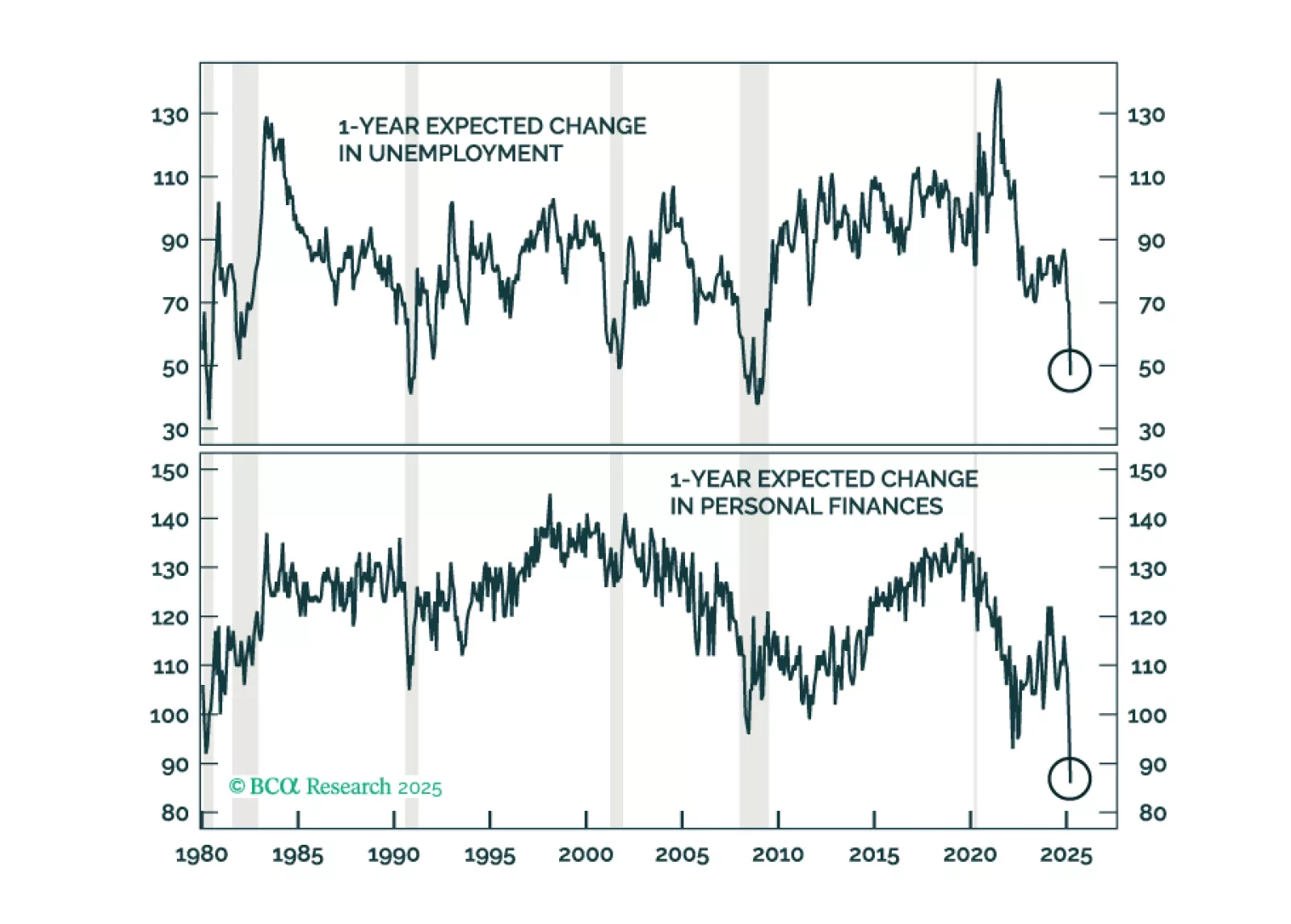

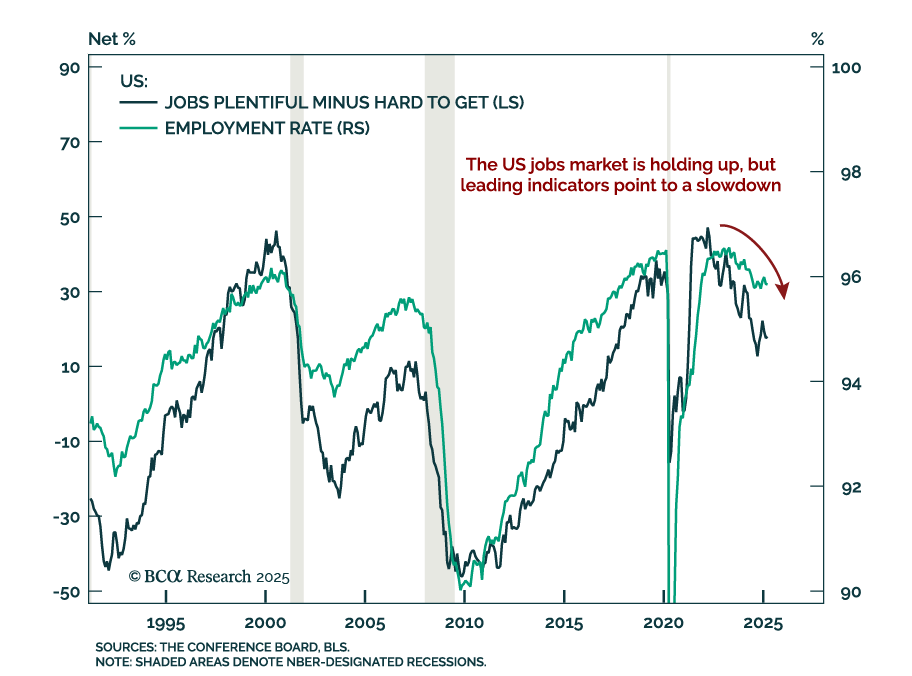

The March employment report showed strong job growth, but the labor market remains in a fragile state and the demand shock from tariffs could be the catalyst that tips it over the edge into recession.